Trump says Nvidia not allowed to sell advanced AI chips to China- 60 Minutes

Introduction & Market Context

Associated Banc-Corp (NYSE:ASB) presented its third quarter 2025 earnings results on October 23, revealing solid performance driven by commercial loan growth and stable interest margins. The bank reported earnings per share of $0.73, exceeding analyst expectations of $0.68 by 7.35%. Following the announcement, ASB shares edged up 0.4% to close at $25.22, continuing a positive trend that has seen the stock rise 12.49% over the past year.

The Midwest regional bank’s results reflect its ongoing strategic shift toward commercial lending while maintaining disciplined credit standards in a potentially challenging economic environment.

Quarterly Performance Highlights

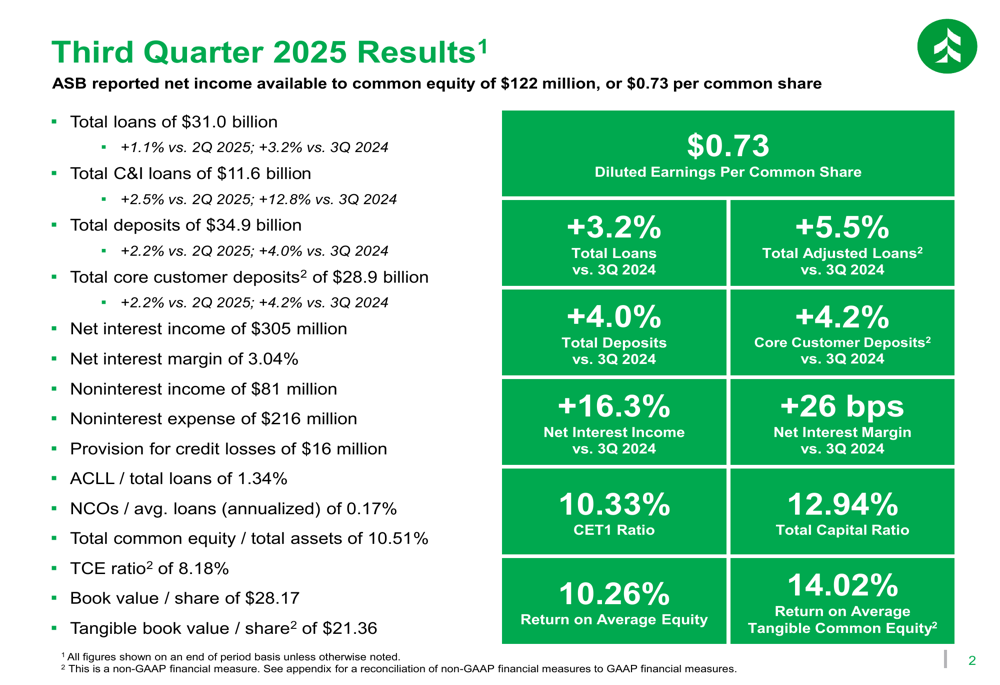

Associated Banc-Corp reported net income of $122 million or $0.73 per common share for Q3 2025. The bank achieved record net interest income of $305 million, representing a 16.3% increase compared to the same period last year, while maintaining a stable net interest margin of 3.04%.

As shown in the following comprehensive overview of key financial metrics:

Total loans grew to $31.0 billion, up 1.1% from the previous quarter and 3.2% year-over-year. Commercial and industrial (C&I) loans were particularly strong at $11.6 billion, increasing 2.5% quarter-over-quarter and 12.8% year-over-year, demonstrating the success of the bank’s strategic focus on commercial lending.

Total deposits reached $34.9 billion, growing 2.2% from Q2 2025 and 4.0% year-over-year. Core customer deposits, which represent a more stable funding source, increased by 2.2% quarter-over-quarter to $28.9 billion, reflecting a 4.2% gain from Q3 2024.

The bank’s efficiency ratio improved to 54.8%, down from 59.5% in Q3 2024, indicating better operational efficiency. Return on average tangible common equity reached 14.02%, showing solid profitability.

Strategic Initiatives

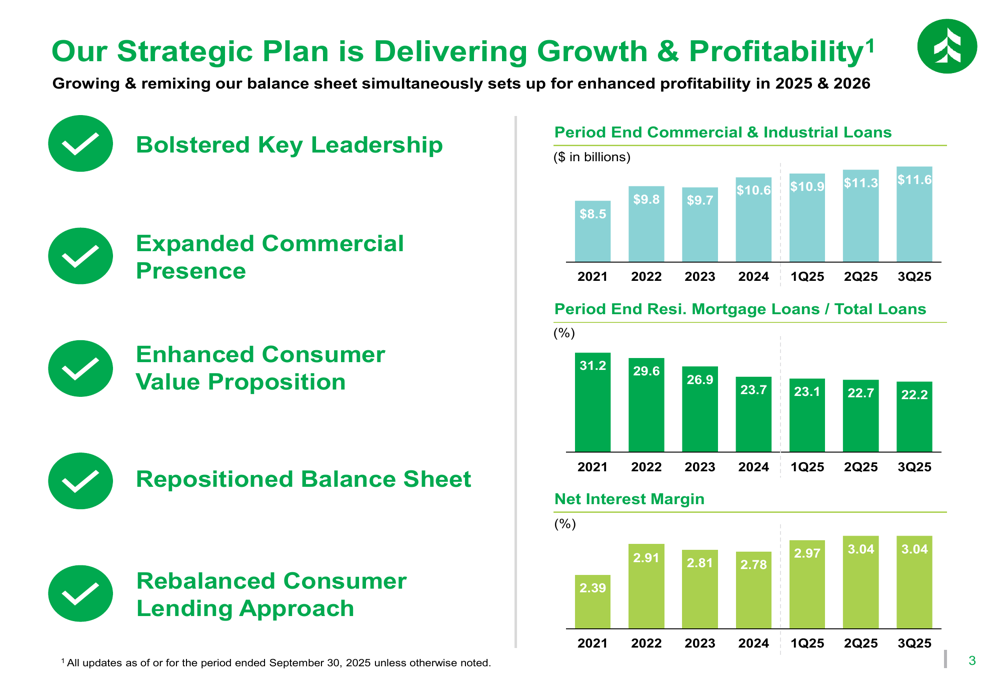

Associated Banc-Corp’s presentation highlighted the progress of its strategic plan in delivering growth and profitability. The bank has been systematically repositioning its balance sheet, with a focus on expanding commercial lending while reducing its reliance on residential mortgages.

The following chart illustrates the company’s strategic progress over time:

C&I loans have grown steadily from $8.5 billion in 2021 to $11.6 billion in Q3 2025, while residential mortgage loans as a percentage of total loans have decreased from 31.2% in 2021 to 22.2% in Q3 2025. This shift has contributed to the improvement in net interest margin from 2.39% in 2021 to the current 3.04%.

CEO Andy Harmening emphasized this strategic direction during the earnings call, stating, "We’re proving that we can grow and deepen our customer base organically," while maintaining that "credit discipline remains foundational to our strategy."

Detailed Financial Analysis

Net interest income, a key driver of the bank’s performance, showed consistent growth over the past five quarters, as illustrated in this chart:

Net interest income increased by $5 million from the previous quarter to $305 million, representing a substantial 16.3% increase from Q3 2024. The net interest margin remained stable at 3.04%, unchanged from Q2 2025 but up 26 basis points year-over-year.

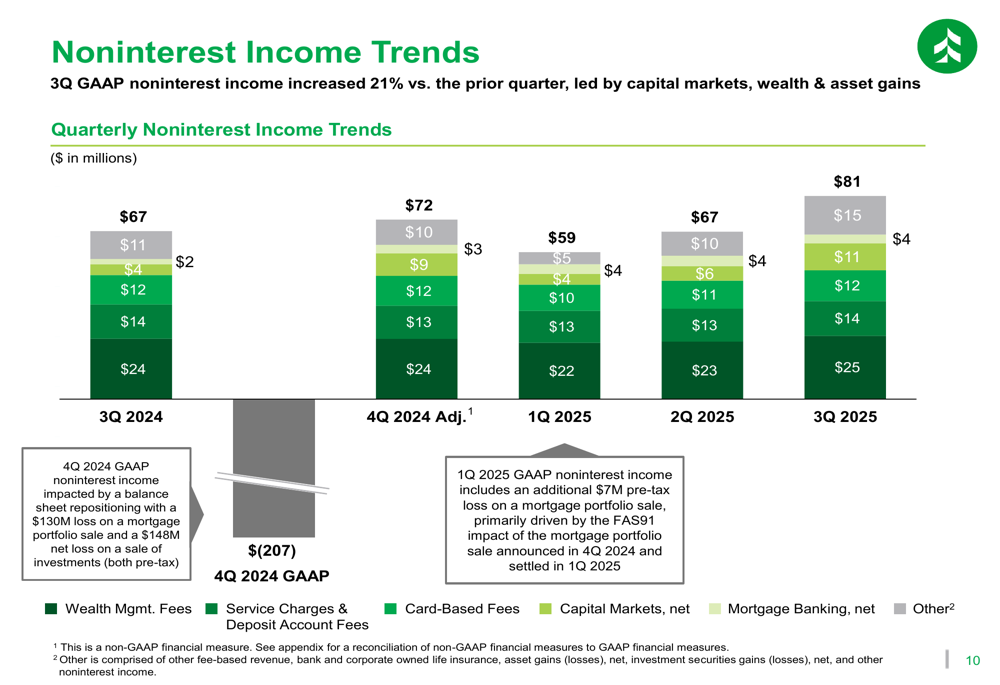

Noninterest income showed significant improvement, increasing 21% quarter-over-quarter to $81 million, led by gains in capital markets, wealth management, and asset management:

Wealth management revenue reached $25 million, while capital markets income more than doubled from $5 million in Q1 2025 to $11 million in Q3 2025, demonstrating the bank’s success in diversifying revenue streams.

Noninterest expenses increased by $7 million from the previous quarter to $216 million, with the increase primarily attributed to performance-based compensation:

Despite the increase in expenses, the efficiency ratio improved to 54.8%, reflecting better operational efficiency compared to 59.5% in Q3 2024.

Capital and Credit Quality

Associated Banc-Corp maintained strong capital ratios, with a Common Equity Tier 1 (CET1) ratio of 10.33%, within the bank’s target range of 10-10.5% for 2025. The tangible common equity ratio improved to 8.18%, up from 7.50% in Q3 2024.

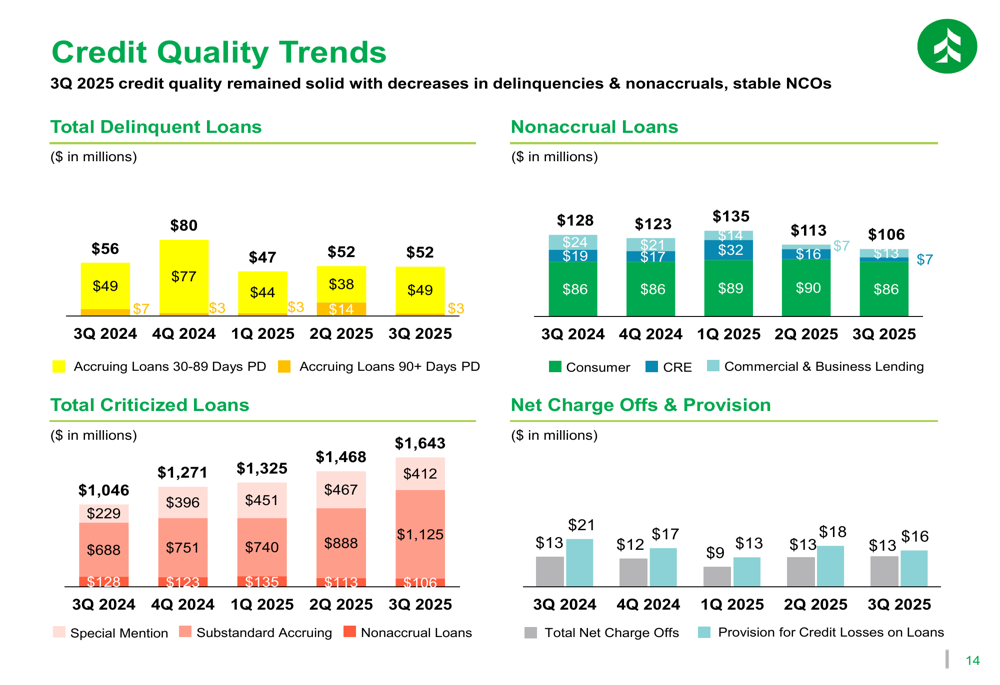

Credit quality remained solid with decreases in delinquencies and nonaccrual loans. Nonaccrual loans decreased to $106 million from $113 million in the previous quarter. The allowance for credit losses on loans (ACLL) stood at 1.34% of total loans, down slightly from 1.35% in Q2 2025. Net charge-offs remained stable at an annualized rate of 0.17% of average loans.

Forward-Looking Statements

Associated Banc-Corp provided an updated outlook for fiscal year 2025, maintaining most of its previous guidance while adjusting a few key metrics:

The bank continues to target loan growth of 5-6% and deposit growth of 1-3% for the full year. Net interest income is expected to increase by 14-15% compared to 2024. The bank raised its noninterest income growth forecast from 1-2% to 5-6%, reflecting the strong performance in fee-based businesses.

The effective tax rate guidance was lowered from 19-21% to 18-19%, which could positively impact net income. The bank maintained its CET1 capital ratio target of 10-10.5% and its noninterest expense growth projection of 5-6%.

For 2026, management indicated during the earnings call that expenses are expected to rise by less than 2%, with continued focus on commercial and industrial lending growth.

Risks and Challenges

Despite the strong quarterly performance, Associated Banc-Corp faces several potential challenges. The earnings presentation and call highlighted proactive steps taken to reduce asset sensitivity and protect net interest income in a falling rate environment, suggesting concerns about potential interest rate cuts.

The bank has seen an increase in criticized loans, which grew to $1.64 billion in Q3 2025 from $1.05 billion a year earlier. While this hasn’t translated into higher delinquencies or charge-offs yet, it bears monitoring as a potential early warning sign.

Additionally, the InvestingPro analysis mentioned in the earnings article suggests the stock may be overvalued with a P/E ratio of 32.28x, significantly above industry averages, which could limit further share price appreciation.

Other risks include potential economic slowdown impacting loan growth, inflationary pressures affecting cost structures, and competitive pressures in the banking sector challenging market share expansion.

Conclusion

Associated Banc-Corp’s Q3 2025 results demonstrate the success of its strategic shift toward commercial lending and balance sheet repositioning. The bank’s focus on organic growth, coupled with disciplined credit management, has delivered improved profitability and efficiency.

With strong capital ratios, stable net interest margin, and growing fee-based income, the bank appears well-positioned to navigate the current economic environment. However, investors should monitor credit quality trends and valuation metrics as potential areas of concern going forward.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.