TSX futures tick up after index logs fresh record high close

Introduction & Market Context

Atmos Energy Corporation (NYSE:ATO) presented its fiscal third-quarter 2025 results on August 7, showing continued financial strength and operational progress. The natural gas distributor reported significant earnings growth, raised its full-year guidance, and highlighted substantial capital investments focused on safety and reliability.

The company’s stock closed at $156.63 on August 6, 2025, up 0.25% ahead of the earnings announcement, and has shown strong performance with the stock trading near its 52-week high of $167.45.

Quarterly Performance Highlights

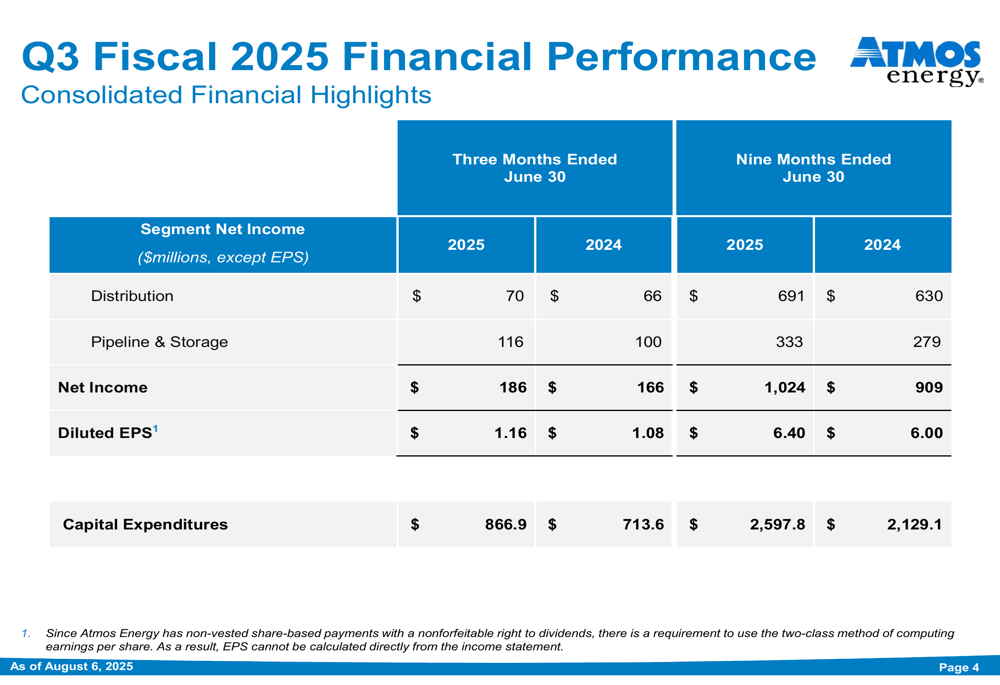

Atmos Energy reported Q3 fiscal 2025 diluted earnings per share (EPS) of $1.16, an increase from $1.08 in the same period last year. For the nine months ended June 30, 2025, diluted EPS reached $6.40, up from $6.00 in the comparable period of 2024, representing a 6.7% increase.

Net income for the quarter rose to $186 million, compared to $166 million in Q3 fiscal 2024. Year-to-date net income reached $1,024 million, a substantial increase from $909 million in the prior year period.

As shown in the following consolidated financial highlights:

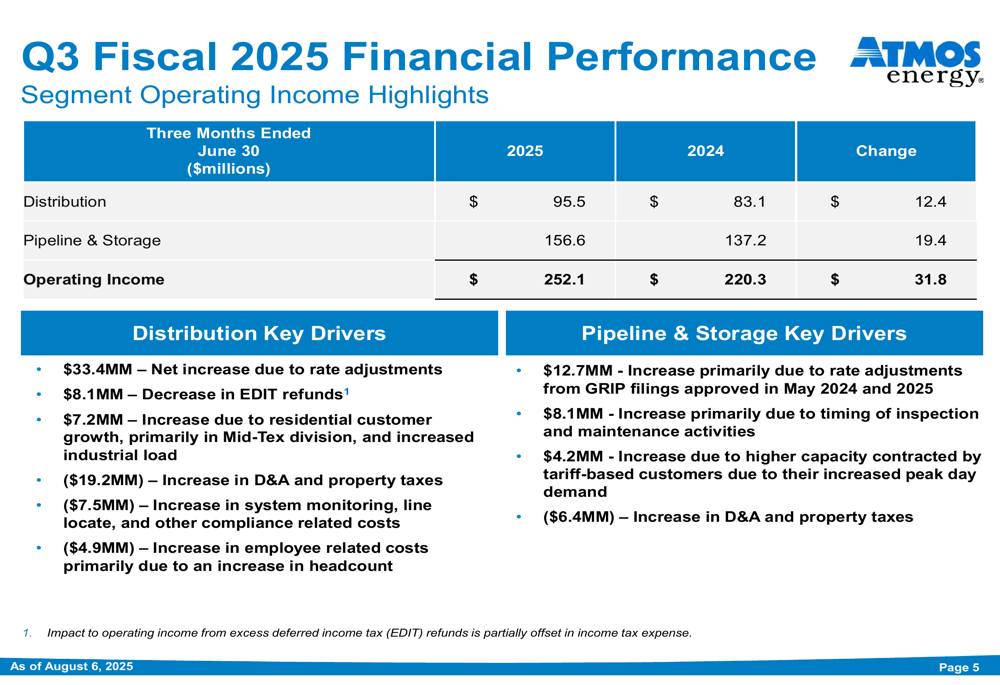

Both of the company’s operating segments contributed to the strong performance. The Distribution segment reported Q3 operating income of $95.5 million, up from $83.1 million in the prior year, while the Pipeline & Storage segment delivered operating income of $156.6 million, compared to $137.2 million in Q3 2024.

The detailed segment breakdown reveals the key drivers behind this growth:

For the nine-month period, Distribution operating income increased to $895.2 million from $789.8 million, while Pipeline & Storage operating income rose to $445.3 million from $380.6 million. These improvements were primarily driven by rate adjustments, customer growth, and increased industrial load.

Capital Spending and Safety Focus

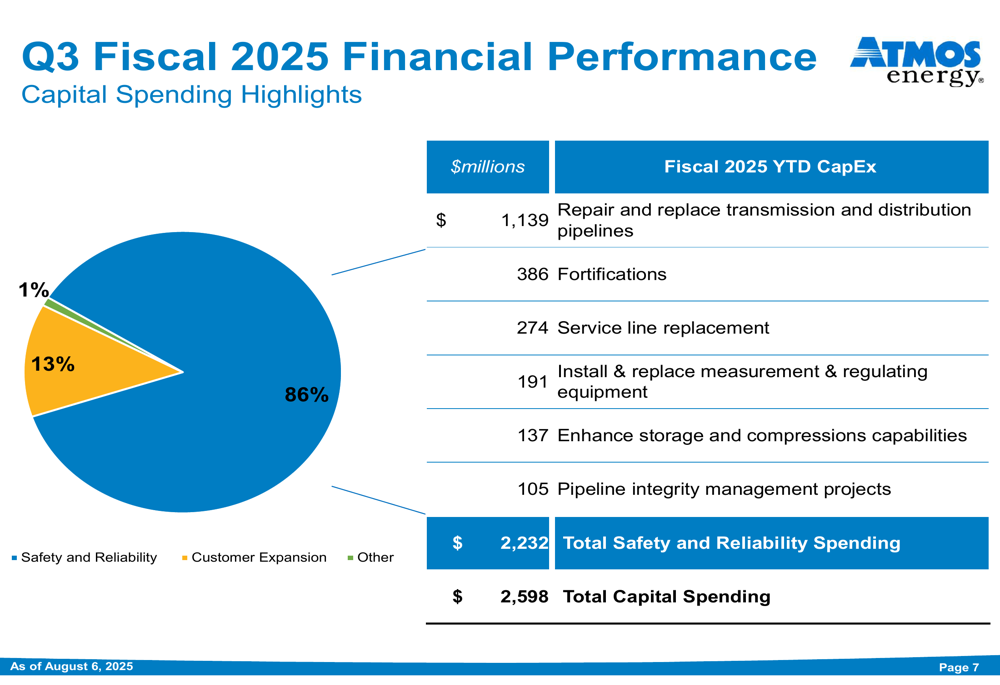

Atmos Energy continues to prioritize safety and reliability in its capital allocation strategy. The company reported $2.6 billion in capital spending for the nine months ended June 30, 2025, with 86% allocated to safety and reliability initiatives.

The following chart illustrates the company’s capital spending priorities:

The largest portion of safety and reliability spending, $1,139 million, was directed toward repairing and replacing transmission and distribution pipelines. Other significant investments included $386 million for fortifications, $274 million for service line replacement, and $191 million for installing and replacing measurement and regulating equipment.

Regulatory Strategy and Progress

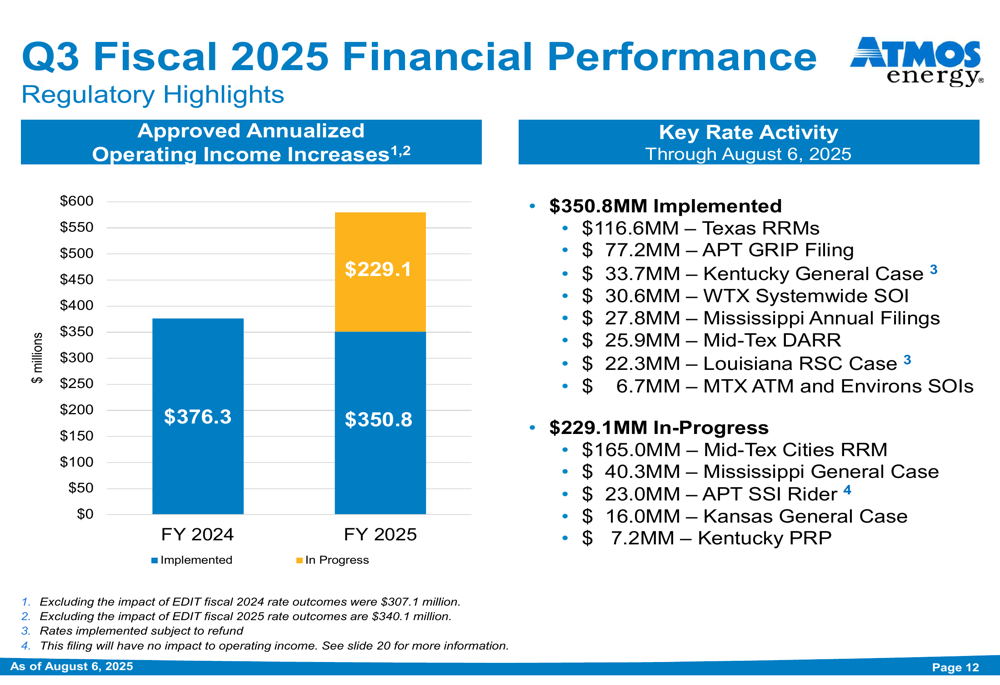

Atmos Energy’s regulatory strategy continues to yield positive results. As of August 6, 2025, the company had implemented $350.8 million in annualized operating income increases, with an additional $229.1 million currently in progress.

The regulatory highlights demonstrate the company’s success in securing rate adjustments across its service territories:

Key implemented rate adjustments include $116.6 million from Texas Rate Review Mechanisms (RRMs), $77.2 million from APT GRIP filing, and $33.7 million from a Kentucky general case. Significant in-progress regulatory actions include $165.0 million from Mid-Tex Cities RRM and $40.3 million from a Mississippi general case.

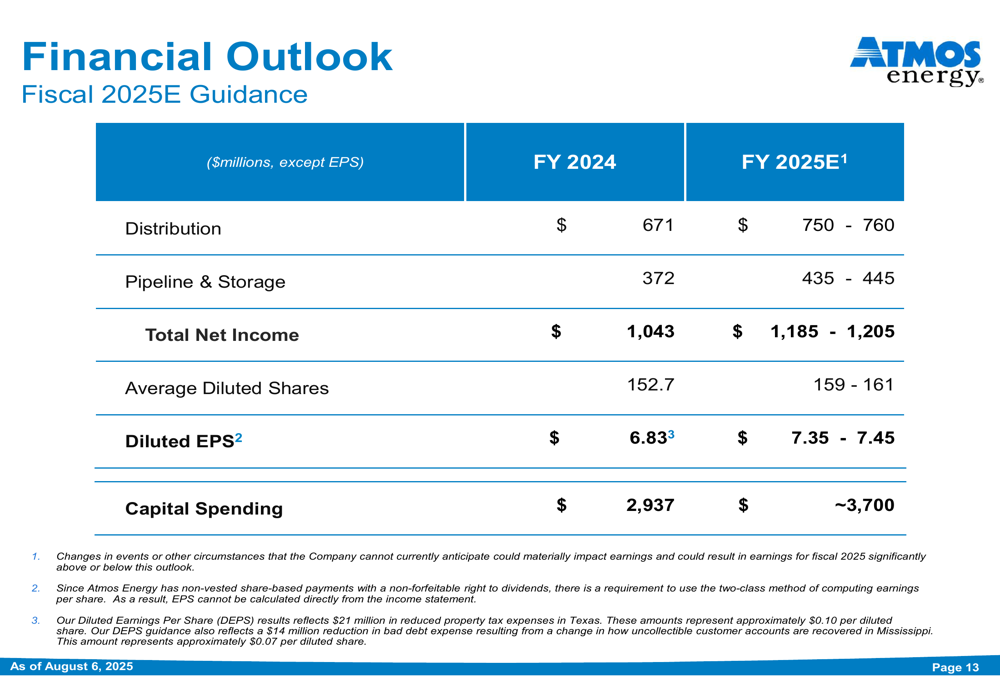

Financial Outlook and Guidance

Based on strong year-to-date performance, Atmos Energy has raised its fiscal 2025 EPS guidance range to $7.35-$7.45, up from the previous range of $7.20-$7.30. This represents the second guidance increase this fiscal year, as the company had previously raised its outlook following Q1 results.

The updated financial outlook projects continued growth across both business segments:

The company expects Distribution net income of $750-760 million and Pipeline & Storage net income of $435-445 million for fiscal 2025. Capital spending is projected to reach approximately $3.7 billion for the full year, up from $2.937 billion in fiscal 2024.

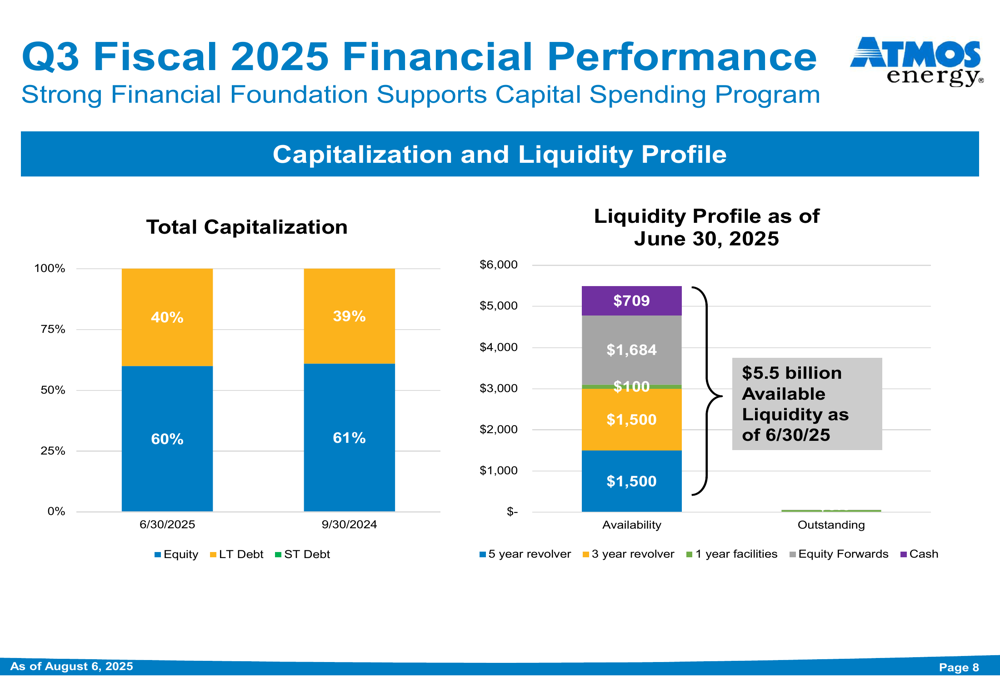

Balance Sheet and Liquidity

Atmos Energy maintains a strong balance sheet with a healthy equity-to-debt ratio. As of June 30, 2025, the company’s capitalization consisted of 60% equity and 40% long-term debt, compared to 61% equity and 39% long-term debt as of September 30, 2024.

The company’s liquidity profile remains robust:

Available liquidity totaled approximately $5.5 billion as of June 30, 2025, including $1.5 billion from a five-year revolver, $100 million from a three-year revolver, $1.684 billion from one-year facilities, and $709 million from equity forwards.

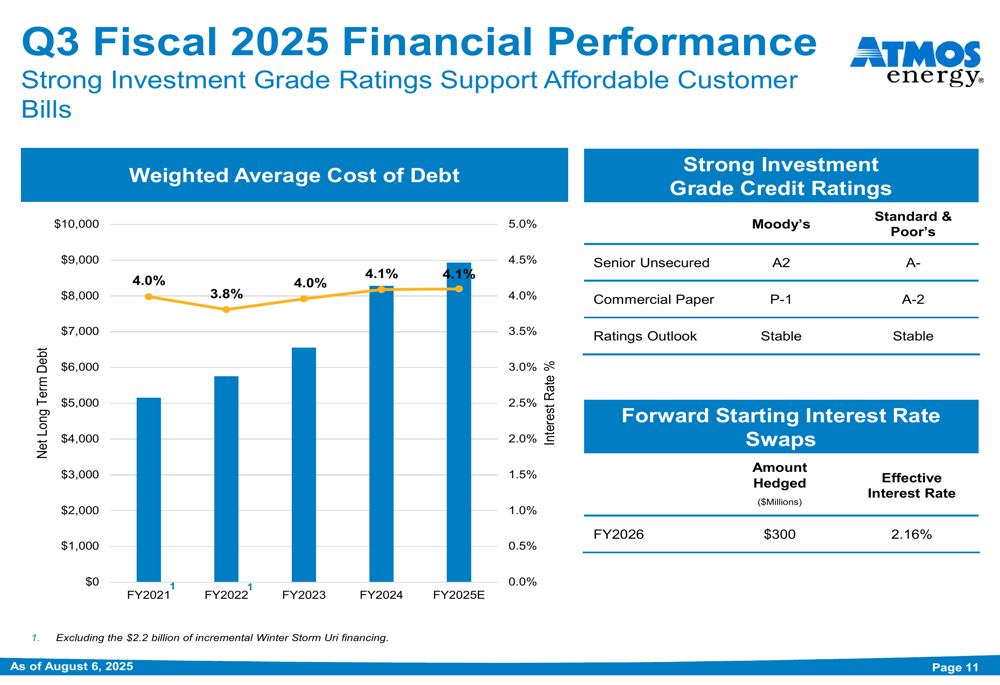

Atmos Energy has successfully executed its financing strategy, issuing $1.15 billion of long-term debt, including $650 million in 30-year senior notes at 5.00% in October 2024 and $500 million in 10-year senior notes at 5.20% in June 2025.

The company’s weighted average cost of debt has remained relatively stable despite the rising interest rate environment:

Atmos Energy maintains strong investment-grade credit ratings, with Moody’s rating its senior unsecured debt at A2 and Standard & Poor’s at A-. Both agencies maintain a stable outlook on the company.

Dividend Growth

Continuing its long history of shareholder returns, Atmos Energy announced an 8.1% increase in its fiscal 2025 indicated annual dividend to $3.48 per diluted share. This marks the company’s 41st consecutive year of dividend increases, highlighting its commitment to returning value to shareholders while investing in infrastructure improvements.

The combination of consistent dividend growth, strong operational performance, and effective regulatory strategy positions Atmos Energy for continued success as it executes its capital investment program focused on safety, reliability, and customer growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.