Palantir to report; Trump on Nvidia chip exports - what’s moving markets

Introduction & Market Context

Atmus Filtration Technologies Inc (NYSE:ATMU) presented its second quarter 2025 earnings results on August 8, 2025, revealing solid sales growth and improved profitability metrics. The filtration specialist’s stock responded positively, rising 4.71% to close at $40.46, after gaining 2.59% in premarket trading.

The company, which specializes in filtration solutions primarily for transportation and industrial markets, continued its positive momentum from Q1 2025, when it exceeded analyst expectations with both revenue and earnings. This quarter’s results further strengthened investor confidence in Atmus’s business model and growth strategy.

Quarterly Performance Highlights

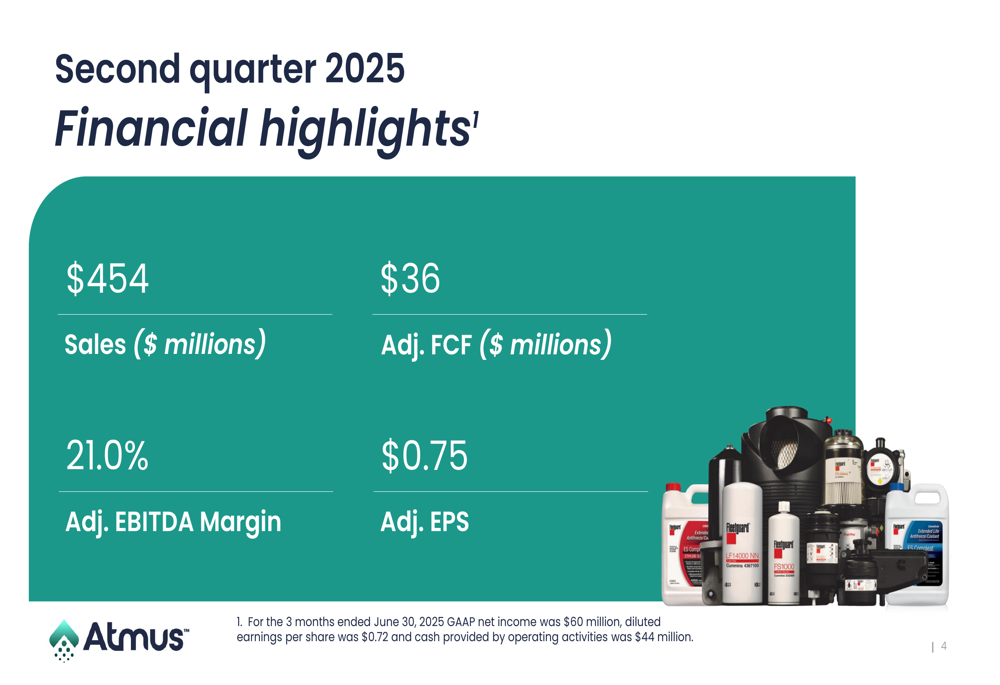

Atmus reported Q2 2025 sales of $454 million, representing a 4.8% increase compared to $433 million in the same period last year. The company achieved an adjusted EBITDA of $95 million with a margin of 21.0%, slightly down from 21.4% in Q2 2024.

As shown in the following financial highlights slide:

Net income for the quarter reached $60 million, up 7.1% from $56 million in Q2 2024, while diluted earnings per share increased to $0.72 from $0.67 a year ago. On an adjusted basis, which excludes one-time separation costs, EPS came in at $0.75, compared to $0.71 in the prior-year period.

The company generated $36 million in adjusted free cash flow during the quarter, demonstrating strong cash conversion capabilities. This performance builds on the momentum seen in Q1, when Atmus reported $417 million in revenue and $0.63 in adjusted EPS.

Detailed Financial Analysis

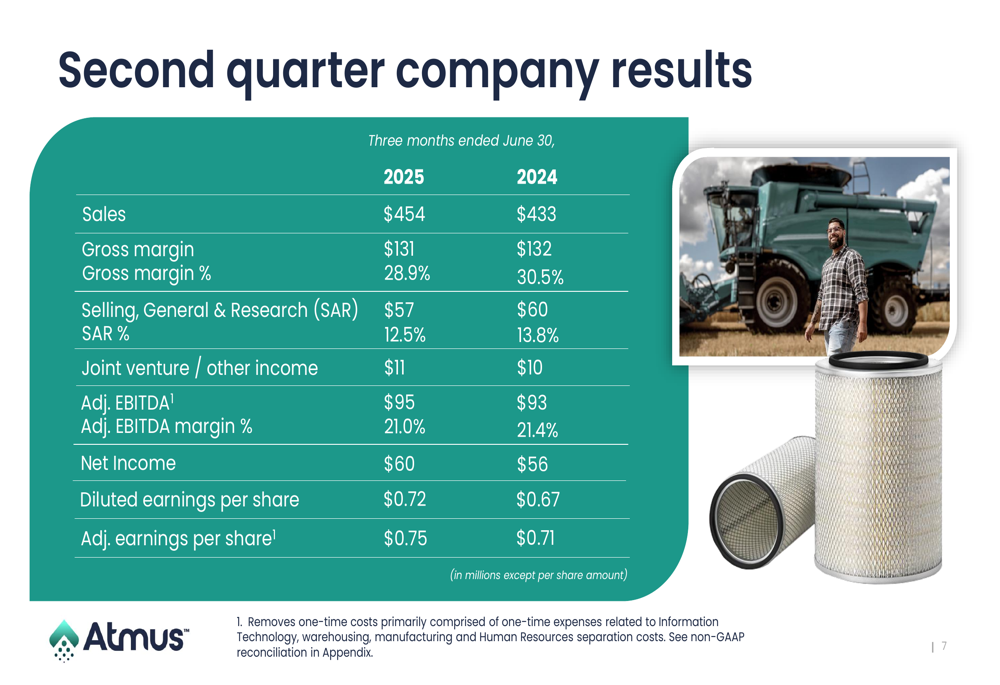

A closer examination of Atmus’s Q2 2025 results reveals mixed performance across key financial metrics. While sales increased year-over-year, gross margin percentage declined to 28.9% from 30.5% in Q2 2024. However, the company improved operational efficiency, with selling, general and research expenses decreasing to 12.5% of sales compared to 13.8% in the prior year.

The detailed quarterly comparison is illustrated in the following slide:

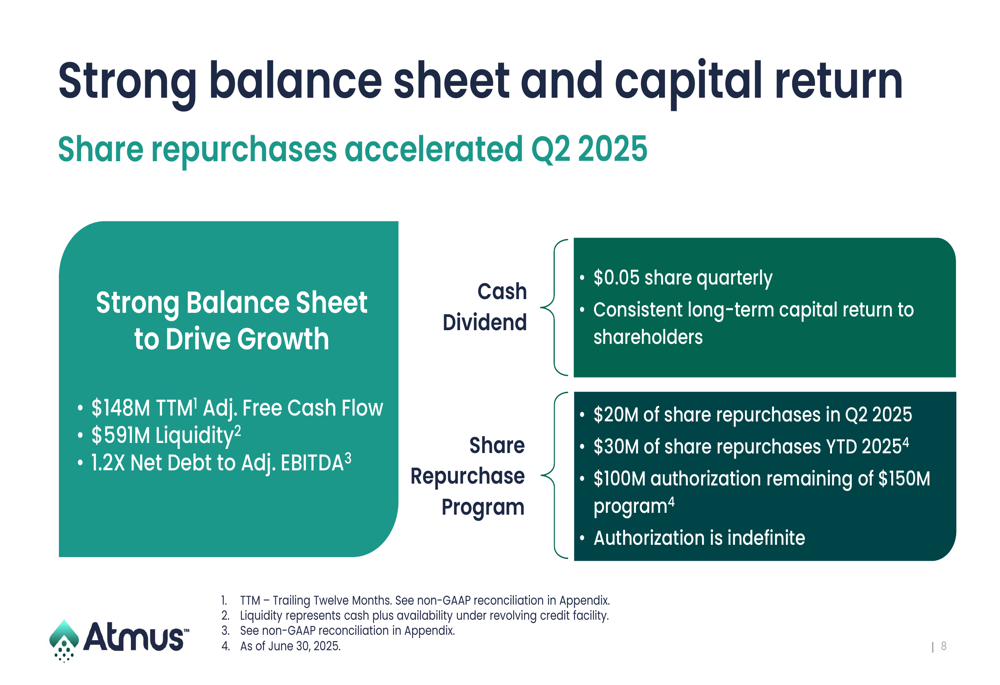

Atmus maintained a strong balance sheet with $591 million in liquidity and a net debt to adjusted EBITDA ratio of 1.2x. The company’s trailing twelve-month adjusted free cash flow reached $148 million, providing substantial financial flexibility.

The financial strength enabled Atmus to continue its shareholder return program, which included a quarterly cash dividend of $0.05 per share and $20 million in share repurchases during Q2 2025. Year-to-date, the company has repurchased $30 million in shares, with $100 million remaining from its $150 million authorization.

As shown in the following capital return slide:

Strategic Initiatives

During the presentation, Atmus highlighted its investment thesis and growth strategy. The company positions itself as a provider of mission-critical products in predictable and growing end markets, with strong brand recognition and consistent financial results.

The investment case for Atmus is summarized in this slide:

Atmus’s growth strategy consists of four key pillars: growing market share in first-fit core markets, accelerating profitable growth in the aftermarket, transforming the supply chain, and expanding into industrial filtration markets. This diversified approach aims to balance growth opportunities with the stability provided by the company’s strong aftermarket business.

The company’s strategic roadmap is illustrated in the following slide:

CEO Steph Disher and CFO Jack Kienzler led the earnings call, reinforcing the company’s commitment to executing this strategy while maintaining financial discipline.

Forward-Looking Statements

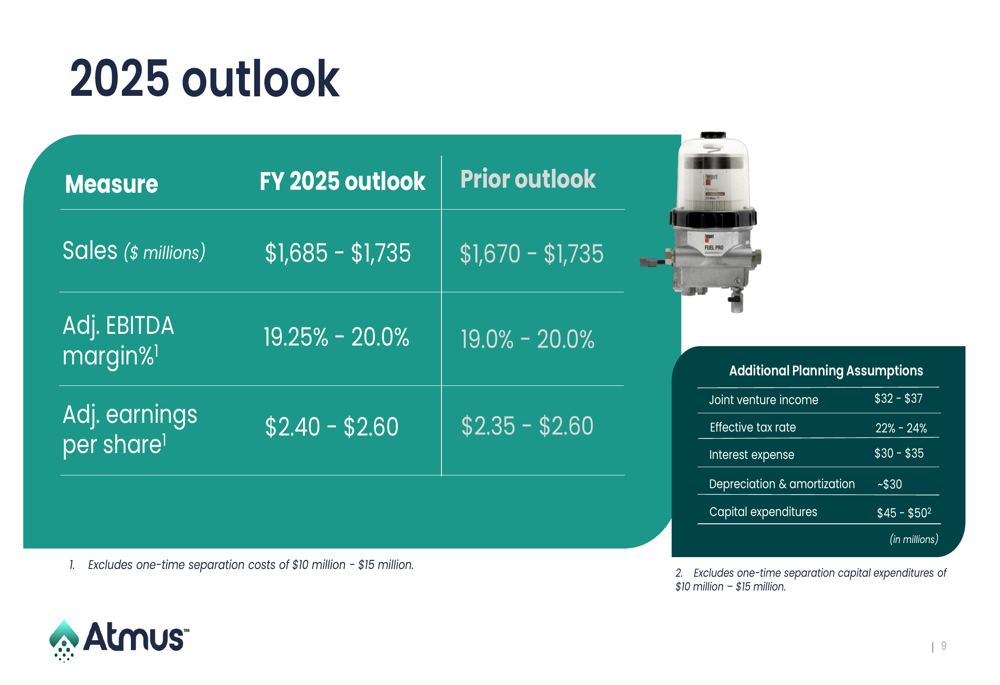

Atmus raised its full-year 2025 guidance, reflecting confidence in its business outlook despite ongoing macroeconomic uncertainties. The company now projects annual sales between $1,685 million and $1,735 million, slightly raising the lower end from the previous guidance of $1,670 million.

Similarly, Atmus increased the lower end of its adjusted EBITDA margin guidance to 19.25%-20.0% from the previous 19.0%-20.0%, and adjusted EPS guidance to $2.40-$2.60 from $2.35-$2.60.

The updated outlook and planning assumptions are detailed in this slide:

Additional planning assumptions for 2025 include joint venture income of $32-$37 million, an effective tax rate of 22%-24%, interest expense of $30-$35 million, depreciation and amortization of approximately $30 million, and capital expenditures of $45-$50 million.

This guidance excludes one-time separation costs as Atmus continues to establish itself as a fully independent entity following its separation from Cummins (NYSE:CMI). In Q1 2025, the company had indicated these separation costs would range between $5-10 million for the full year.

The positive market reaction to Atmus’s Q2 results and raised guidance suggests investors are confident in the company’s ability to navigate industry challenges while delivering consistent financial performance and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.