Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

AtriCure Inc (NASDAQ:ATRC), a leader in technologies for the treatment of atrial fibrillation (Afib) and post-operative pain, presented its Q1 2025 investor presentation in April, highlighting the company’s strong financial performance and strategic positioning in growing markets. With a current market capitalization of $1.7 billion, AtriCure has established itself as a significant player in addressing serious cardiac conditions and pain management.

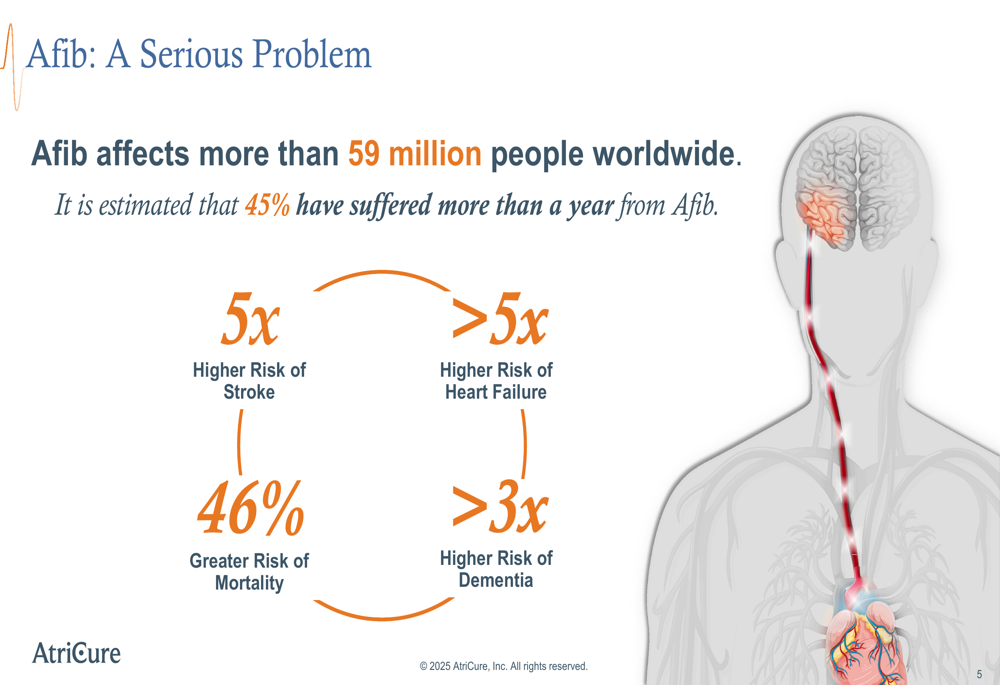

The company’s presentation emphasized the substantial market opportunity, noting that Afib affects more than 59 million people worldwide, with 45% of those suffering for more than a year. This condition presents serious health risks that AtriCure aims to address through its innovative solutions.

As shown in the following image, Afib significantly increases the risk of several serious health conditions:

Quarterly Performance Highlights

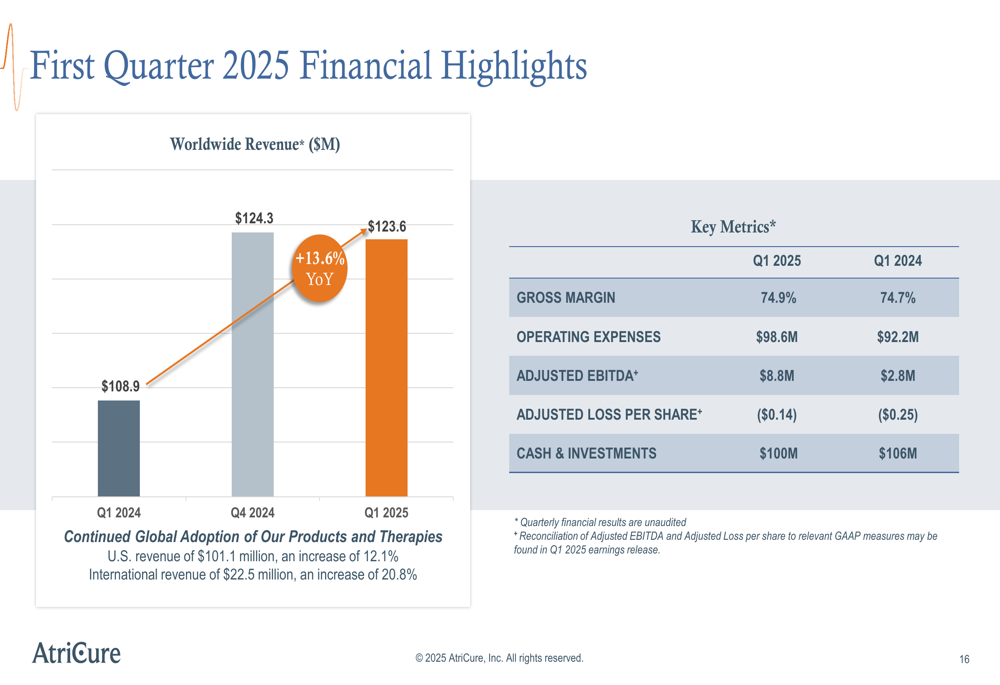

AtriCure reported impressive financial results for Q1 2025, with worldwide revenue reaching $123.6 million, representing a 13.6% year-over-year increase. The company maintained a strong gross margin of 74.9% while achieving an adjusted EBITDA of $8.8 million, which according to the earnings call represents over a 200% increase from Q1 2024. The adjusted loss per share improved to $0.14, better than both the previous year’s Q1 loss of $0.25 and analysts’ expectations of a $0.22 loss.

The company’s financial performance was driven by strong sales across both U.S. and international markets. U.S. revenue reached $101.1 million (up 12.1%), while international revenue grew by 20.8% to $22.5 million, demonstrating the company’s successful global expansion strategy.

The following chart illustrates AtriCure’s recent revenue trajectory:

Following the earnings release, AtriCure’s stock price increased by 2.9% in after-hours trading, reflecting investor confidence in the company’s performance and outlook. However, as of the most recent trading data, the stock has settled at $31.18, down 1.14% from its previous close.

Strategic Initiatives and Market Opportunity (SO:FTCE11B)

AtriCure’s presentation outlined a compelling growth strategy focused on four key areas: innovation, clinical science, expansion, and profitable growth. The company is targeting vastly underpenetrated markets with significant growth potential, projecting that its addressable market will expand to more than $10 billion by 2030.

The company segments its market opportunity into three primary categories:

1. Cardiac Surgery: Open ablation and left atrial appendage management (LAAM) for concomitant treatment of pre-operative Afib

2. Pain Management: Ablation for thoracic procedures

3. Hybrid Therapy: Minimally invasive surgical ablation and LAAM for standalone treatment of long-standing persistent Afib

As illustrated in the following image, AtriCure sees substantial growth potential across these segments:

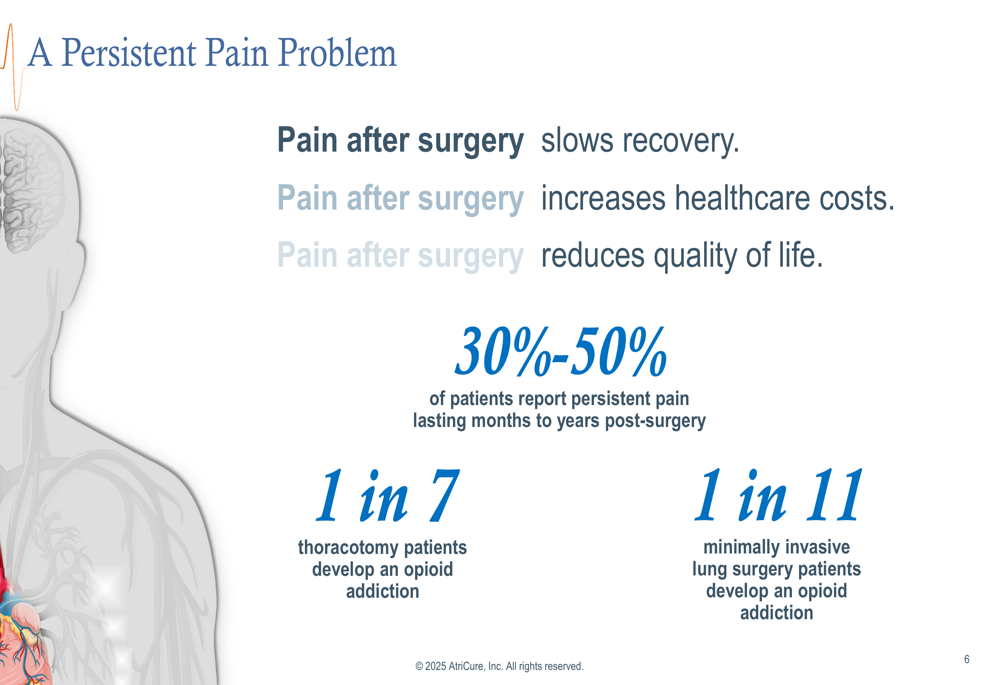

The company’s pain management solutions address a significant clinical need, as 30-50% of patients report persistent pain lasting months to years post-surgery, and 1 in 7 thoracotomy patients develop an opioid addiction. AtriCure’s technologies aim to reduce these complications while improving patient outcomes and reducing healthcare costs.

Forward-Looking Statements

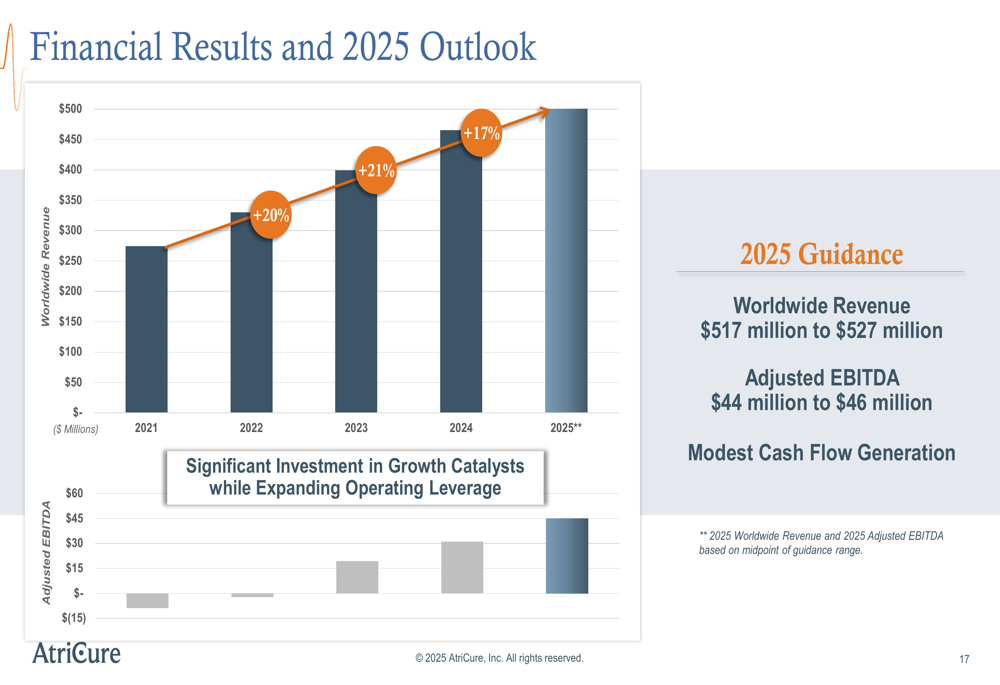

AtriCure has raised its outlook for 2025, projecting worldwide revenue between $517 million and $527 million, representing growth of 11-13% compared to 2024. The company also increased its adjusted EBITDA guidance to $44-46 million and anticipates modest cash flow generation for the year.

This guidance builds on AtriCure’s consistent growth trajectory, which has seen revenue increase by approximately 20% annually in recent years. The company expects this momentum to continue as it expands its product portfolio and global reach.

During the earnings call, CEO Mike Carroll noted: "Our first quarter performance reflects the strength of our broad platform of products." However, he also cautioned that 2025 would be "a pressure year for us," acknowledging challenges in maintaining momentum amidst market shifts. Carroll highlighted the significance of the LEAPS trial, stating it "will create great differentiation by giving us a stroke label."

Competitive Industry Position

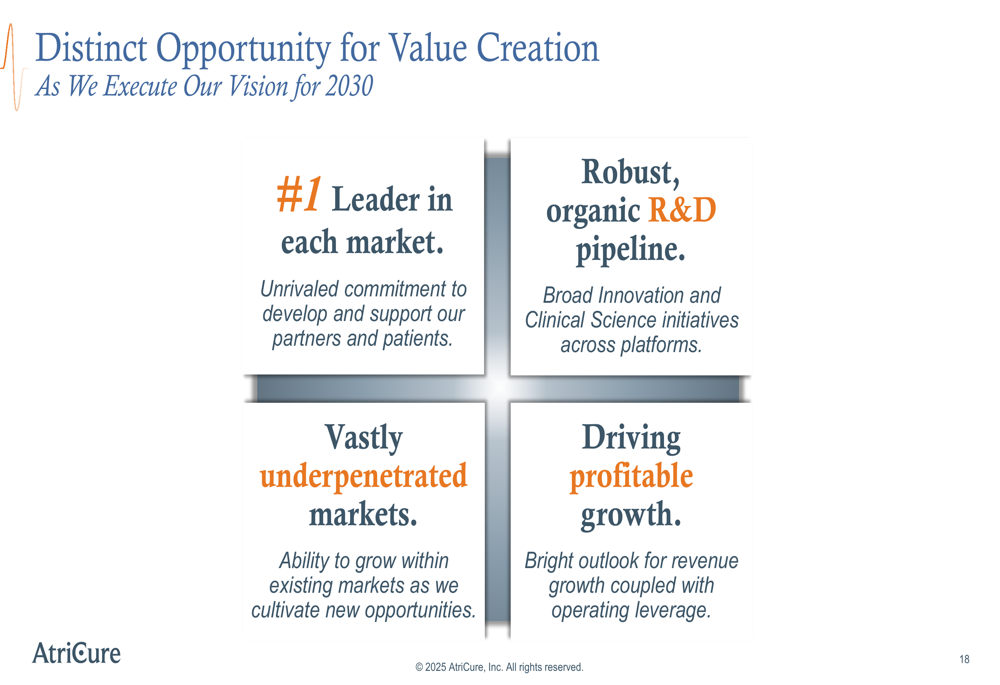

AtriCure positions itself as the #1 leader in each of its target markets, with a commitment to developing and supporting partners and patients. The company’s robust R&D pipeline and broad clinical science initiatives across platforms provide a competitive edge in addressing vastly underpenetrated markets.

The presentation highlighted improved reimbursement conditions that support adoption of AtriCure’s technologies, including $8,000-$14,000 for addition of ablation for CABG plus Surgical Ablation and $15,000-$20,000 for combination Epicardial Ablation plus Epicardial LAA.

The company’s value creation strategy is summarized in the following image:

Despite its strong positioning, AtriCure faces several challenges, including potential tariff impacts on gross margins, competitive pressures from emerging technologies like pulsed field ablation (PFA), and maintaining growth in the minimally invasive surgery ablation segment. The company is addressing these challenges through continued investment in innovation and clinical evidence generation.

AtriCure’s focus on creating a world-class platform for treating Afib and post-operative pain, combined with its improving financial performance and expanding market opportunity, positions the company for continued growth. As the company progresses toward profitability and positive cash flow, investors will be watching closely to see if AtriCure can fully capitalize on its $10 billion market opportunity while navigating competitive and economic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.