ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

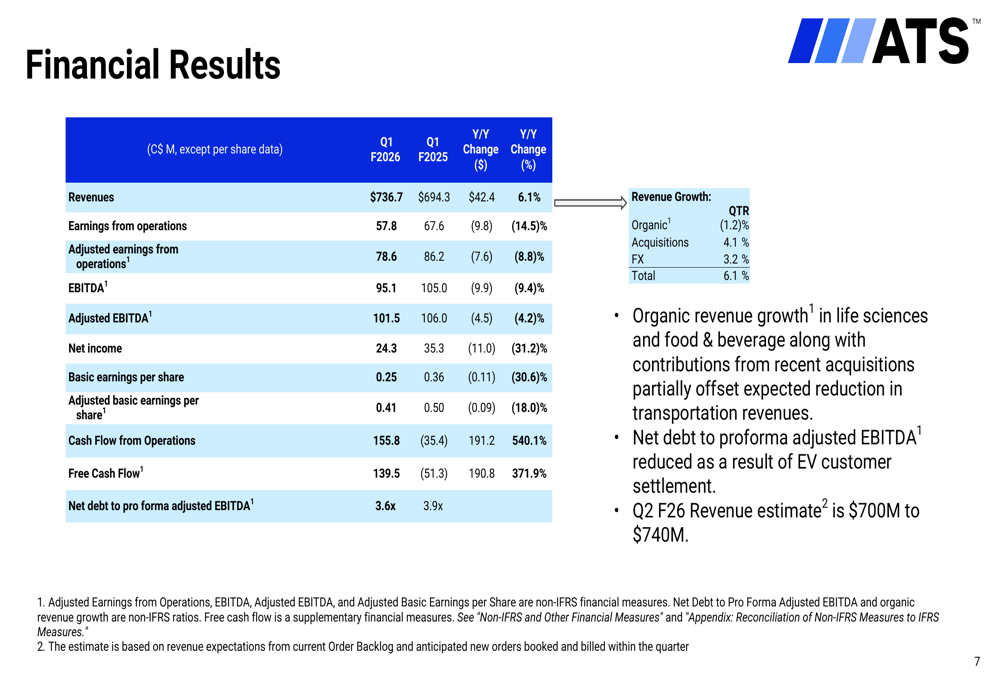

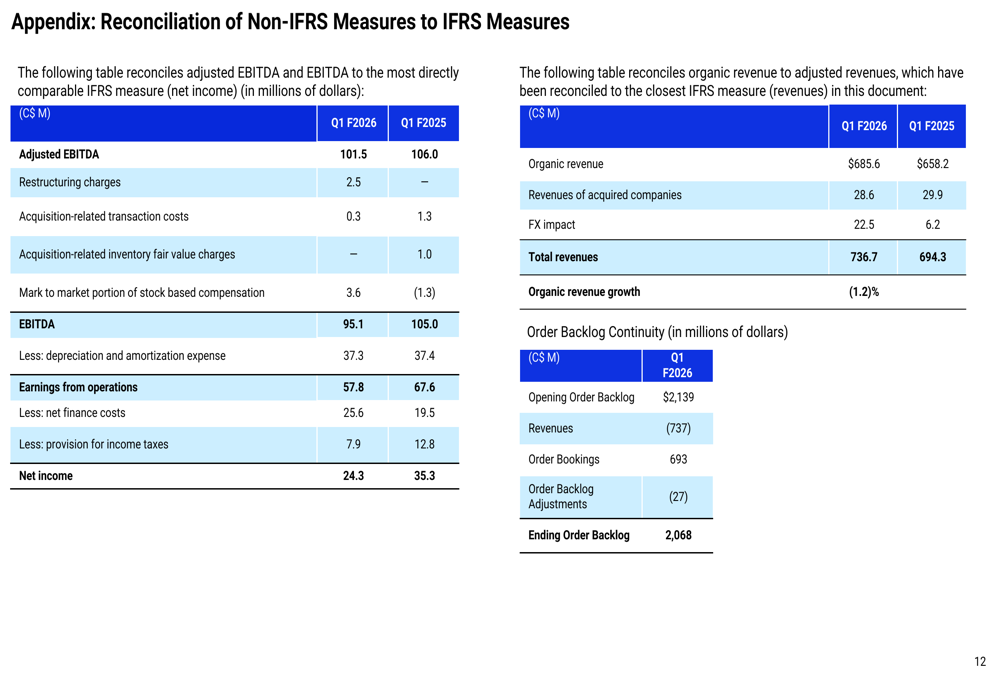

ATS Corp (NYSE:ATS) presented its Q1 fiscal 2026 earnings results on August 7, 2025, revealing a mixed performance characterized by revenue growth but declining profitability metrics. The automation solutions provider reported a 6.1% year-over-year revenue increase to $736.7 million, while net income fell 31.2% to $24.3 million compared to the same period last year.

The company’s performance reflects its ongoing transition away from heavy dependence on the transportation sector, particularly electric vehicles (EV), toward greater diversification across life sciences, food and beverage, and consumer products. This strategic pivot follows challenges in the EV segment that were highlighted in previous quarters.

Quarterly Performance Highlights

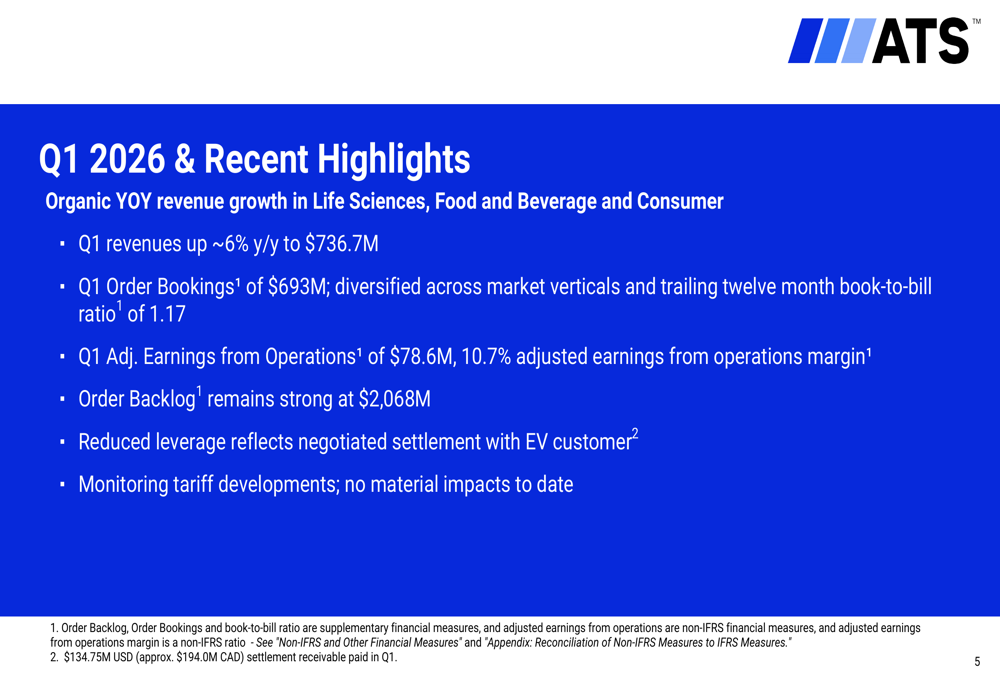

ATS reported Q1 revenues of $736.7 million, representing a 6.1% increase year-over-year. However, this growth was primarily driven by acquisitions (4.1%) and favorable foreign exchange impacts (3.2%), while organic revenue actually declined by 1.2%.

As shown in the following financial results summary:

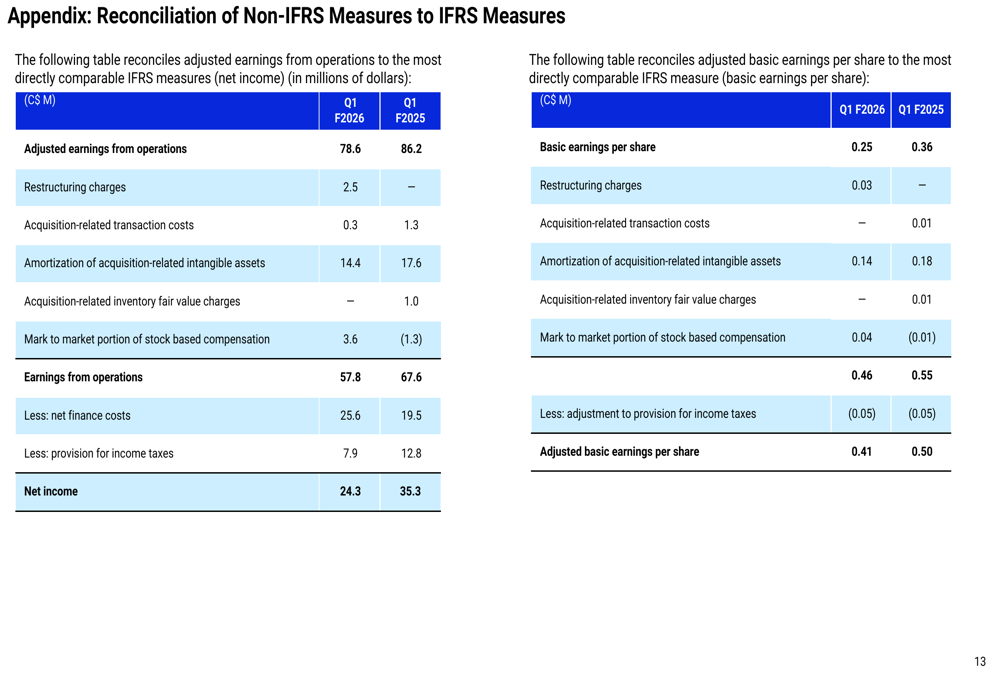

Despite the revenue growth, profitability metrics declined across the board. Earnings from operations fell 14.5% to $57.8 million, while adjusted earnings from operations decreased 8.8% to $78.6 million. The adjusted earnings from operations margin stood at 10.7%, down from the previous year. Basic earnings per share dropped 30.6% to $0.25, while adjusted basic EPS fell 18.0% to $0.41.

The company’s order bookings for the quarter reached $693 million, with a diversified distribution across market verticals. The trailing twelve-month book-to-bill ratio remained healthy at 1.17, indicating continued demand for ATS’s automation solutions.

As illustrated in the recent highlights:

Detailed Financial Analysis

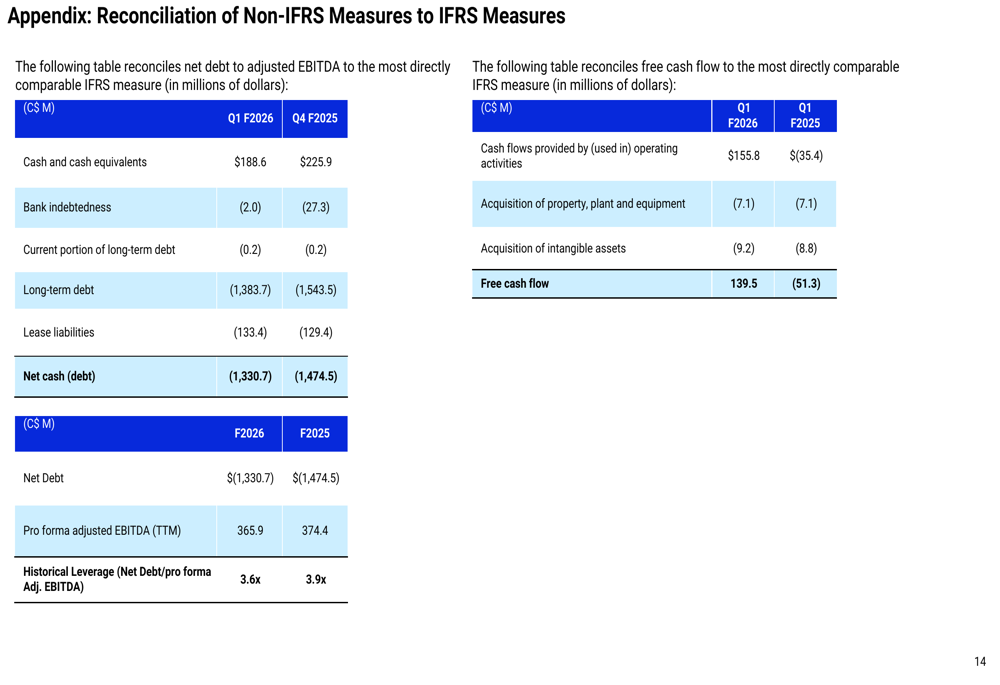

The most dramatic improvement in ATS’s financial metrics came from cash flow. Cash flow from operations surged 540.1% to $155.8 million, while free cash flow increased 371.9% to $139.5 million. This substantial improvement reflects the impact of a negotiated settlement with an EV customer worth $134.75 million USD (approximately $194.0 million CAD).

This settlement also helped reduce the company’s leverage, with the net debt to pro forma adjusted EBITDA ratio now standing at 3.6x. This represents progress toward the company’s target range of 2 to 3 times, which was mentioned in previous earnings communications.

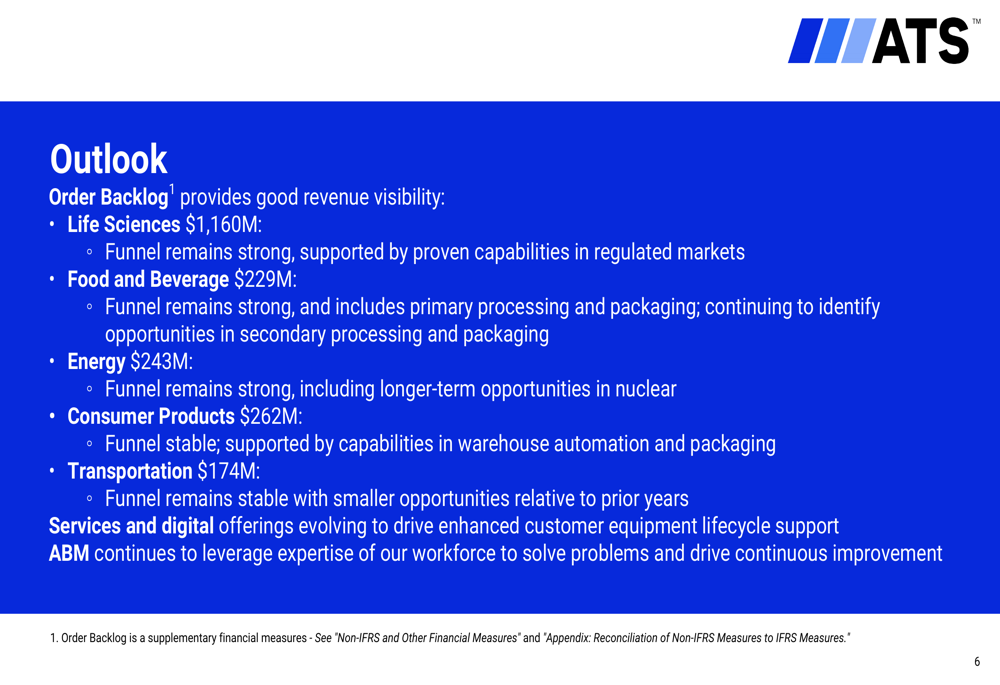

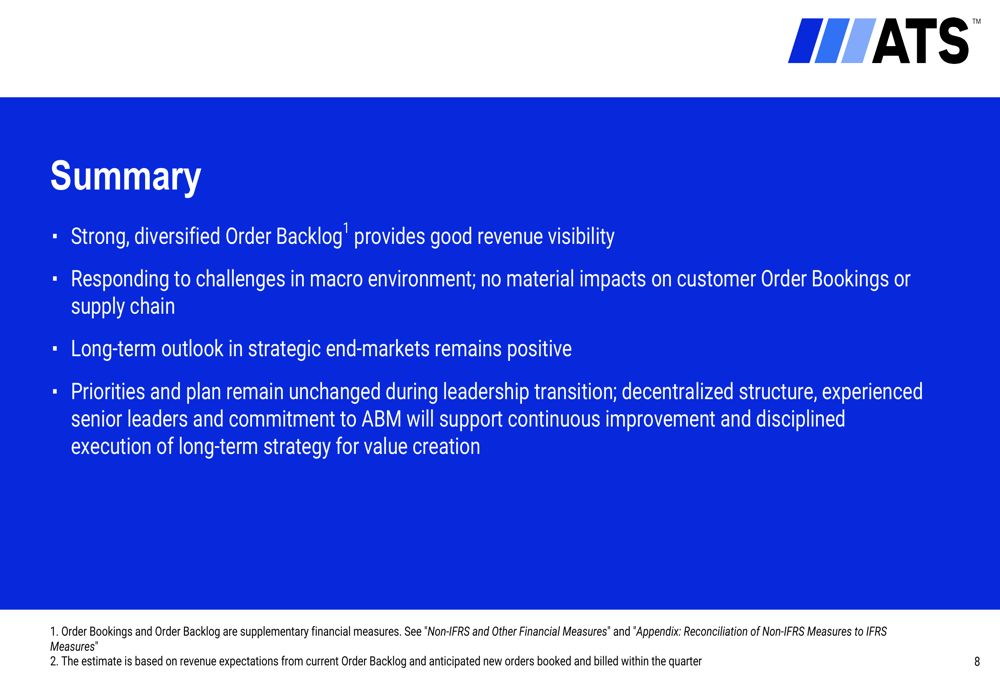

The company’s order backlog remains robust at $2,068 million, providing good revenue visibility for upcoming quarters. The backlog is diversified across sectors, with Life Sciences representing the largest portion at $1,160 million.

The sector breakdown of the order backlog provides insight into ATS’s market positioning:

Strategic Initiatives & Outlook

ATS continues to focus on diversifying its revenue streams across multiple sectors, with particular emphasis on life sciences, food and beverage, and consumer products. The company reported organic year-over-year revenue growth in these segments, partially offsetting the expected reduction in transportation revenues.

For the upcoming quarter (Q2 F2026), ATS provided revenue guidance of $700 million to $740 million, suggesting relatively stable performance compared to the current quarter.

The company’s management highlighted that its decentralized structure, experienced senior leadership, and commitment to the ATS Business Model (ABM) will support continuous improvement and disciplined execution of its long-term strategy for value creation.

As summarized in the company’s outlook:

Forward-Looking Statements

ATS management expressed confidence in the company’s strategic direction, noting that the long-term outlook in its strategic end-markets remains positive despite current macroeconomic challenges. The company is monitoring tariff developments but reported no material impacts to date.

The reconciliation of non-IFRS measures provides additional context for understanding the company’s financial performance:

The company’s focus on services and digital offerings continues to evolve, with an emphasis on enhancing customer equipment lifecycle support. This strategy aligns with ATS’s goal of increasing recurring revenue streams, which was highlighted as a priority in previous communications.

While the transportation sector faces challenges with smaller opportunities relative to prior years, ATS noted that its Life Sciences funnel remains strong, supported by proven capabilities in regulated markets. Similarly, the Food and Beverage segment shows a strong funnel, including opportunities in both primary processing and packaging, as well as potential growth in secondary processing and packaging.

ATS’s ability to navigate the ongoing transition away from heavy EV dependence while capitalizing on growth in other sectors will be crucial for its performance in the coming quarters. Investors will likely focus on whether the company can maintain its revenue growth while reversing the trend of declining profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.