Five things to watch in markets in the week ahead

Introduction & Market Context

AutoCanada Inc. (TSX:ACQ) presented its Q2 2025 investor update on August 13, highlighting the company’s strategic transformation efforts amid a resilient Canadian automotive market. Despite a slight revenue decline, the dealership group reported substantial profit improvements as its cost-cutting initiatives gained traction.

The Canadian automotive retail leader operates in a $211.7 billion market, where it currently holds a 2% share of the OEM franchise segment. The broader market environment remains favorable, with Canadian new light vehicle sales growing 7.8% year-over-year in Q2, and a full-year 2025 outlook of 1.8-1.9 million units.

As shown in the following map of AutoCanada’s nationwide presence:

The company maintains a significant footprint with 64 new light vehicle OEM franchises representing 23 automotive brands, over 1,378 service bays, and a network of 30 collision shops across Canada. This established infrastructure serves as the foundation for the company’s renewed strategic focus.

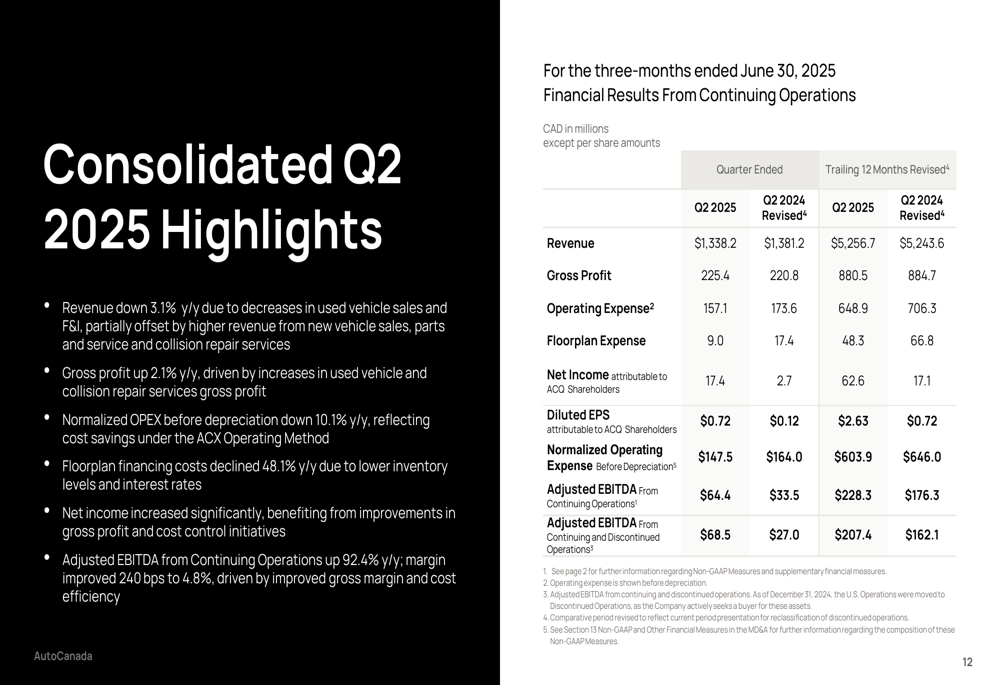

Quarterly Performance Highlights

AutoCanada’s Q2 2025 financial results demonstrated the impact of its transformation initiatives, with profitability metrics showing marked improvement despite a modest revenue decline.

The following slide summarizes the key financial highlights:

Revenue decreased by 3.1% year-over-year to $1.34 billion, slightly below analyst expectations of $1.35 billion. However, gross profit increased by 2.1% to $225.4 million, while normalized operating expenses before depreciation declined by 10.1% year-over-year, reflecting successful cost management.

Most notably, net income attributable to AutoCanada shareholders surged to $17.4 million, compared to just $2.7 million in Q2 2024. This translated to diluted earnings per share of $0.72, significantly exceeding the forecast of $0.5512 and representing a 500% increase from the $0.12 reported in the same period last year.

The company’s adjusted EBITDA nearly doubled, increasing by 92.4% to $64.4 million, underscoring the effectiveness of the company’s cost-cutting measures and operational improvements.

Strategic Transformation Plan

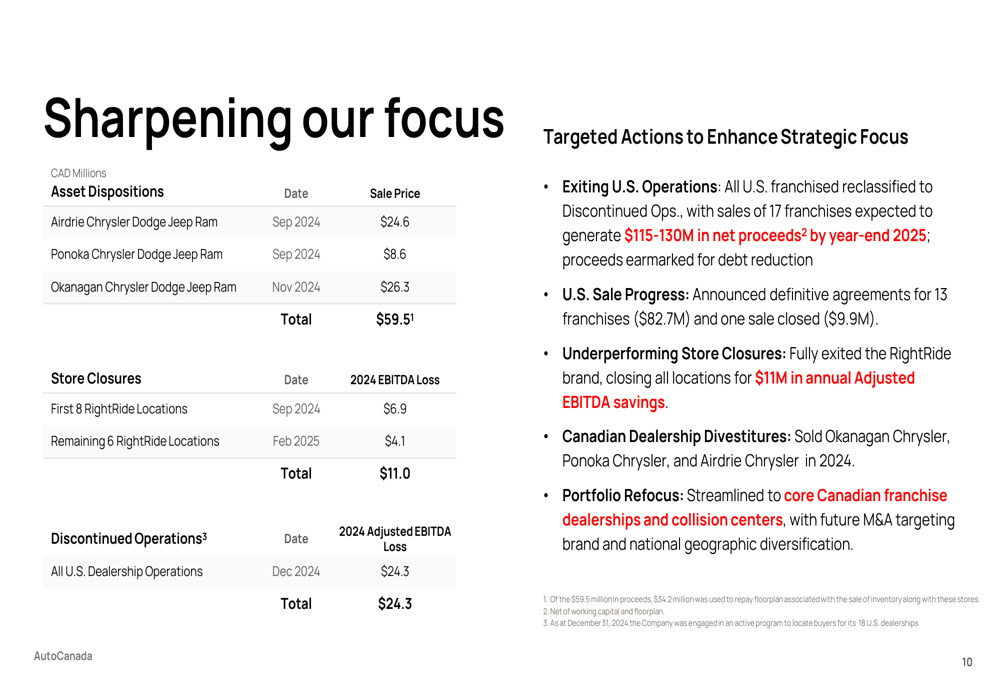

AutoCanada’s presentation emphasized 2025 as a transformational year, with a comprehensive plan to refocus the business on its core Canadian operations while optimizing costs and efficiency.

The strategic roadmap is outlined in the following slide:

The three-pronged approach includes optimizing costs and efficiency, refining core operations, and strengthening the company’s financial position. A key target is reducing leverage to 2-3x Net Funded Debt/Adjusted Bank EBITDA through divestitures and debt reduction.

As part of this transformation, AutoCanada is exiting its underperforming U.S. operations, which contributed a $24.3 million adjusted EBITDA loss in 2024. The company has also divested several Canadian dealerships and closed its RightRide locations to focus resources on more profitable segments.

The following slide details these strategic divestments:

Executive Chairman Paul Anthony emphasized the depth of the company’s transformation efforts during the earnings call, stating, "We took the business down to the studs to rebuild with the right cost structure." This approach appears to be yielding results, as evidenced by the significant improvement in profitability metrics.

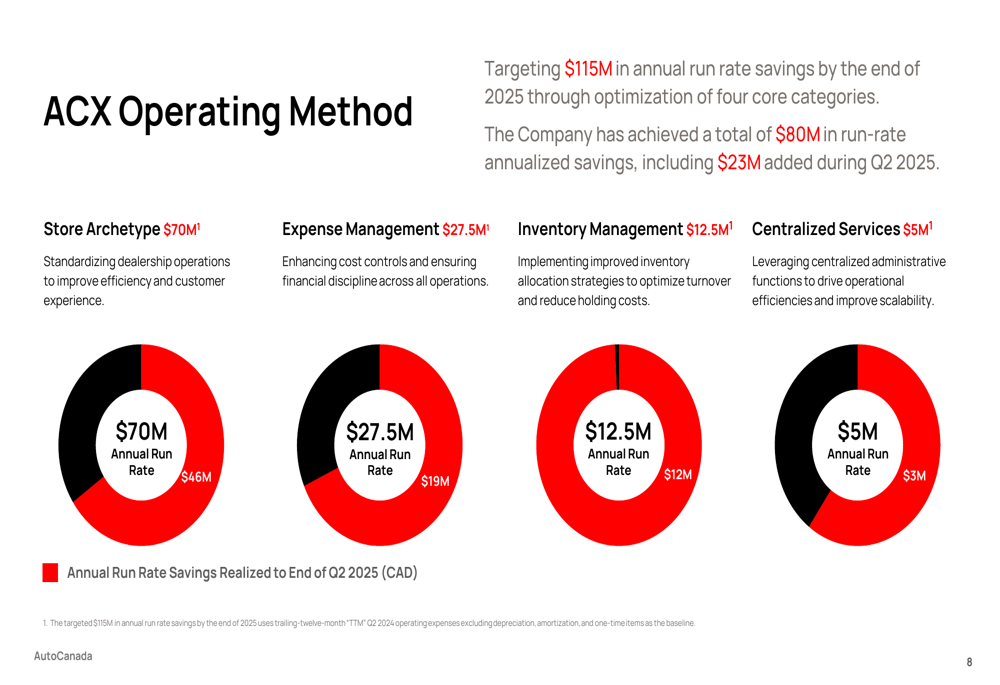

ACX Operating Method and Cost Savings

Central to AutoCanada’s transformation is the implementation of its proprietary ACX Operating Method, which targets $115 million in annual run-rate savings by the end of 2025.

The following slide breaks down the components of this cost-saving initiative:

The ACX Operating Method focuses on four core categories: Store Archetype ($70 million in targeted annual savings), Expense Management ($27.5 million), Inventory Management ($12.5 million), and Centralized Services ($5 million). By the end of Q2 2025, the company had already realized $80 million in run-rate savings.

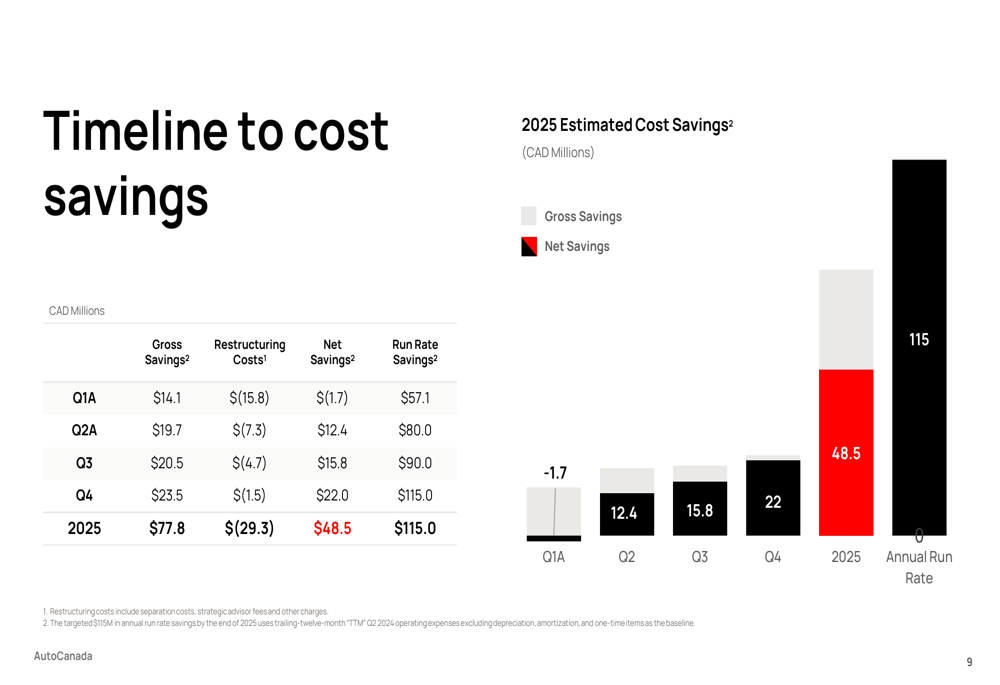

The implementation timeline shows progressive improvement throughout 2025:

For the full year 2025, AutoCanada expects to achieve net savings of $48.5 million after accounting for $29.3 million in restructuring costs. The company’s progress to date suggests it is on track to meet its annual run-rate target of $115 million by year-end.

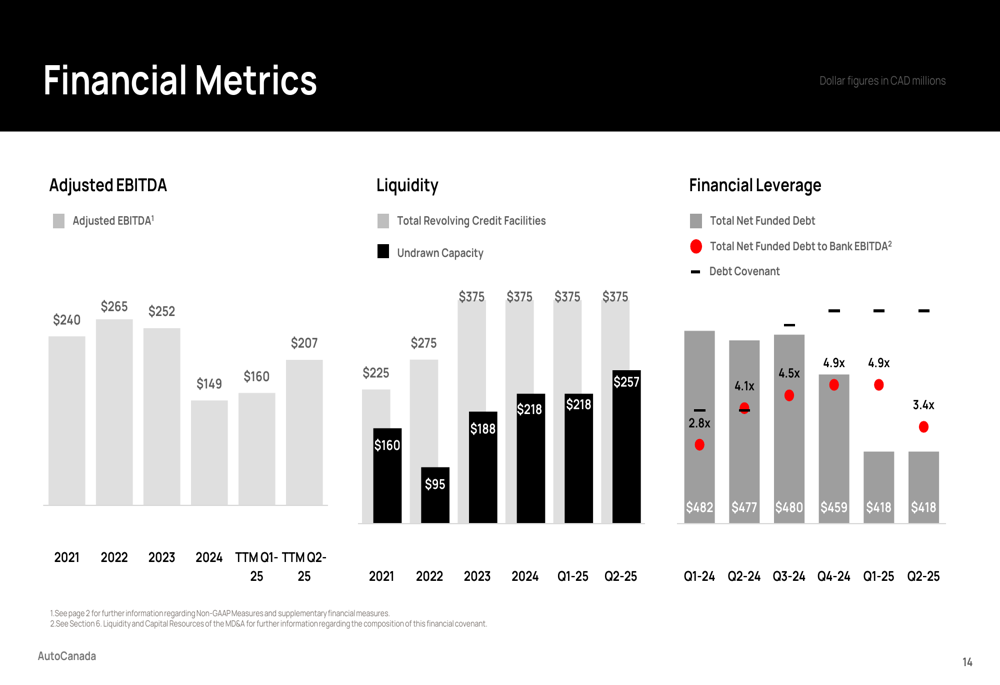

Financial Position and Outlook

AutoCanada’s financial metrics show improving trends, particularly in its leverage ratio, which has decreased from 4.9x in Q4 2024 to 3.4x in Q2 2025, moving closer to the target range of 2-3x.

The following slide illustrates key financial metrics:

Adjusted EBITDA has grown from $240 million in 2021 to $252 million on a trailing twelve-month basis as of Q2 2025. The company reported $62.4 million in cash on hand and available liquidity of $257.4 million, providing flexibility for future growth initiatives.

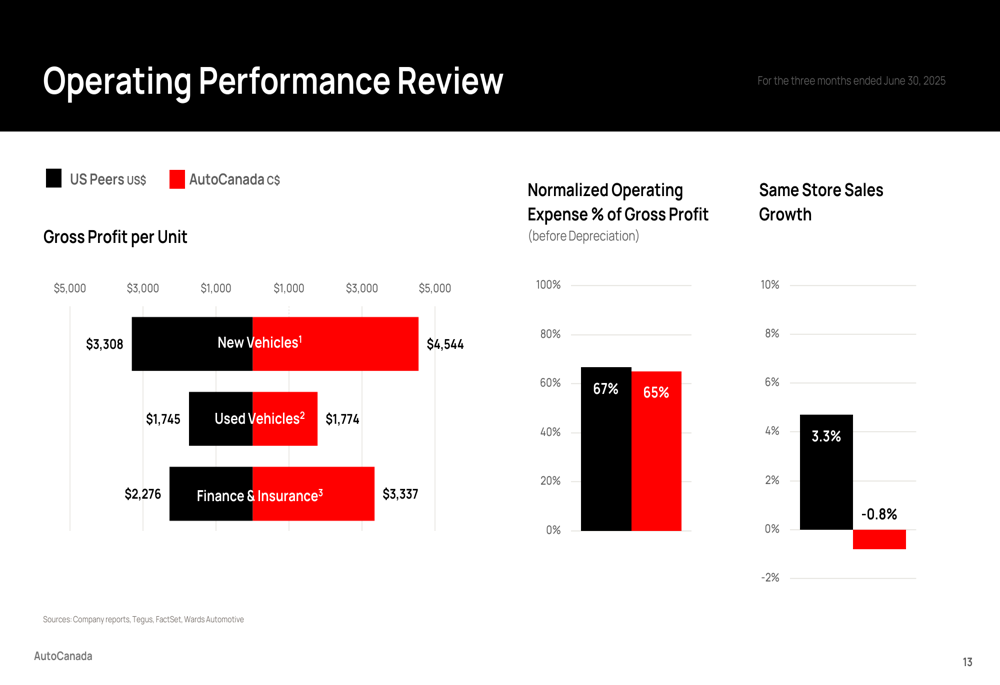

When comparing operational performance against U.S. peers, AutoCanada shows competitive gross profit per unit in used vehicles but has opportunities for improvement in new vehicles and finance & insurance segments:

Looking ahead, AutoCanada plans to complete the rollout of its ACX operating method and shift focus toward volume growth. The company is also exploring potential M&A opportunities within the Canadian market to strengthen its competitive position.

Conclusion

AutoCanada’s Q2 2025 presentation reveals a company in the midst of a significant transformation that is already yielding tangible financial benefits. Despite a slight revenue decline, the substantial improvements in profitability metrics and reduction in leverage demonstrate the effectiveness of the company’s strategic initiatives.

The market has responded positively to these developments, with AutoCanada’s stock price rising 0.97% following the earnings announcement to close at $29.23, approaching its 52-week high of $30.65. With a clear roadmap for continued operational improvements and a strengthened focus on its core Canadian operations, AutoCanada appears well-positioned to build on this momentum through the remainder of 2025.

As the company progresses with its transformation plan, investors will be watching closely to see if the projected cost savings materialize fully and translate into sustained profitability and growth in the competitive Canadian automotive retail landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.