Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

AutoStore Holdings Ltd (OTC:AUTO) presented its second quarter 2025 financial results on August 14, 2025, revealing a significant sequential recovery from a challenging first quarter. The company’s stock closed at $6.69 on August 13, down 3.61% ahead of the earnings release, and remains well below its 52-week high of $13.18, reflecting ongoing market uncertainty in the warehouse automation sector.

The cubic storage automation provider demonstrated resilience in Q2, with substantial quarter-over-quarter improvements across key metrics, though year-over-year comparisons remained challenging. The results come amid AutoStore’s continued execution of its transformation strategy announced earlier this year, which focuses on cost efficiency and innovation.

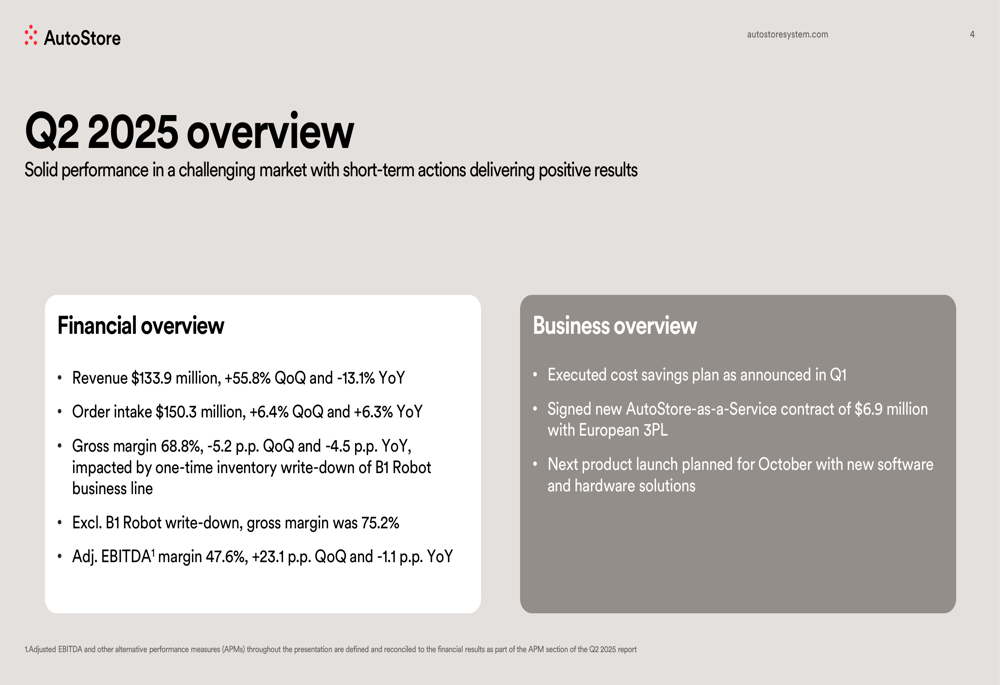

As shown in the company’s financial overview slide, AutoStore achieved notable sequential improvements while managing through industry headwinds:

Quarterly Performance Highlights

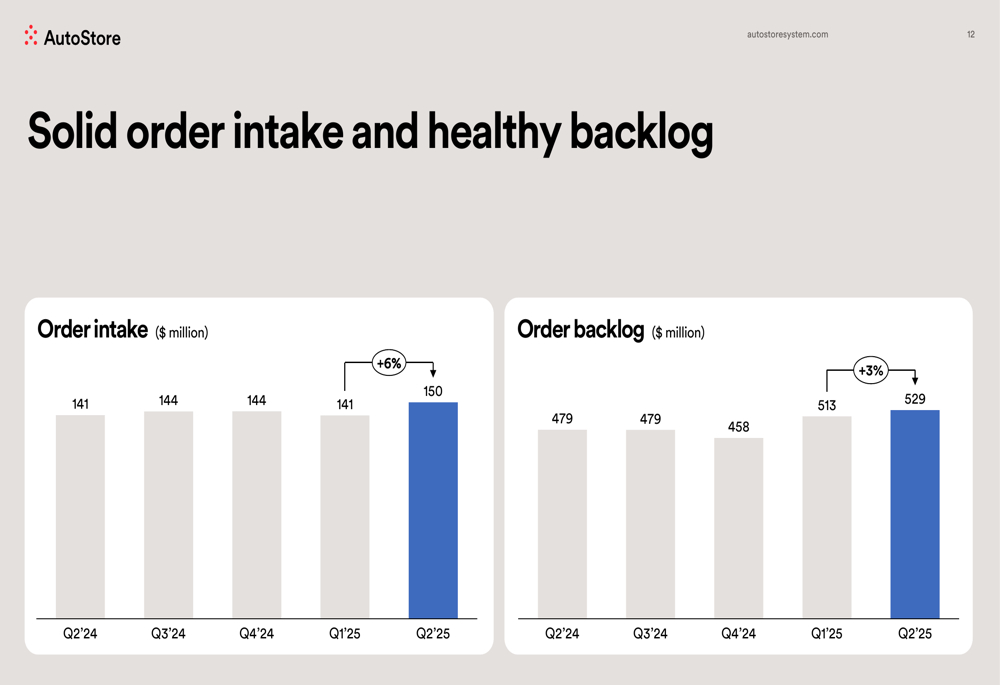

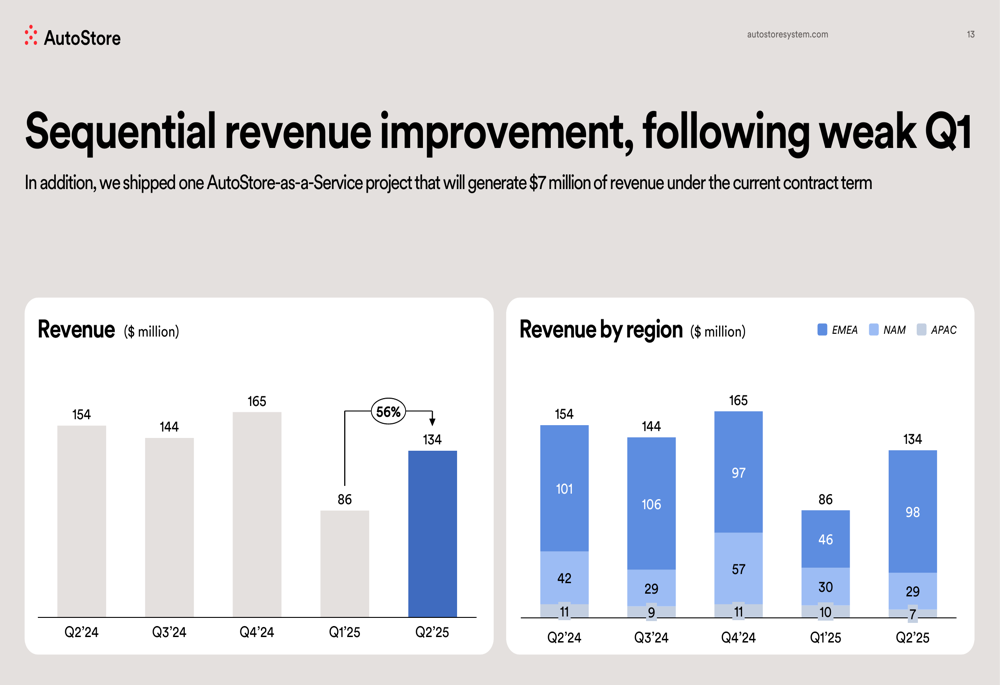

AutoStore reported Q2 2025 revenue of $133.9 million, representing a robust 55.8% increase from Q1’s $86 million, though still down 13.1% year-over-year. Order intake showed positive momentum at $150.3 million, increasing 6.4% sequentially and 6.3% compared to the same quarter last year. The company’s order backlog reached $529 million, up 3% from the previous quarter and 11% year-over-year, providing visibility for future revenue.

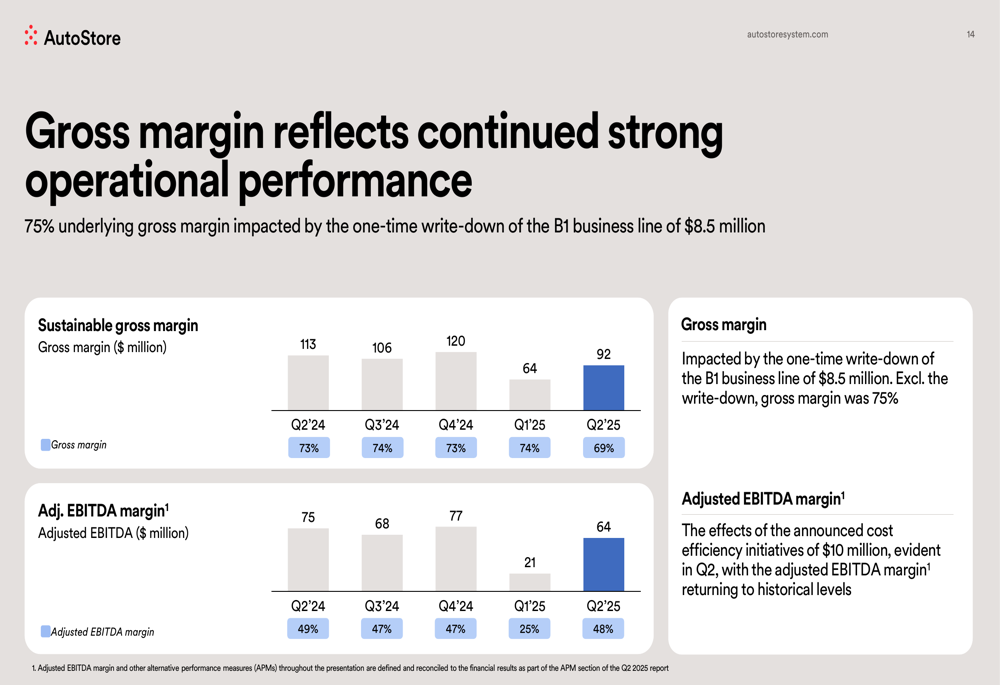

The company’s gross margin was 68.8%, declining 5.2 percentage points quarter-over-quarter and 4.5 percentage points year-over-year. However, this figure was significantly impacted by a one-time inventory write-down related to the B1 Robot business line. Excluding this write-down, the underlying gross margin would have been 75.2%, demonstrating continued strong operational performance.

Adjusted EBITDA margin showed substantial improvement at 47.6%, up 23.1 percentage points from Q1, though slightly down (1.1 percentage points) compared to Q2 2024.

The following slide illustrates the company’s order intake and backlog trends over the past five quarters, showing consistent growth:

Detailed Financial Analysis

AutoStore’s revenue recovery was evident across regions, though with varying performance. As shown in the revenue breakdown, EMEA (Europe, Middle East, and Africa) remains the company’s largest market, contributing $98 million in Q2, followed by North America at $29 million and APAC (Asia-Pacific) at $7 million.

Despite the one-time inventory write-down affecting gross margin, AutoStore maintained strong profitability metrics. The company’s adjusted EBITDA reached $64 million (48% margin) in Q2, a significant improvement from $21 million (25% margin) in Q1, and nearly matching the $75 million (49% margin) achieved in Q2 2024.

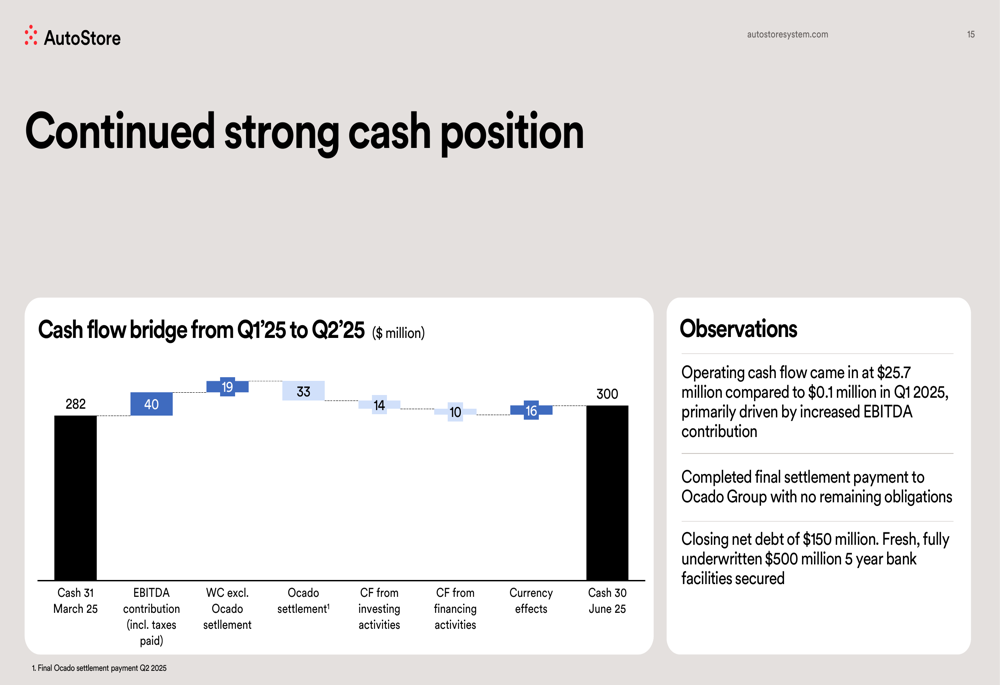

Cash flow generation remained robust, with the company increasing its cash position from $282 million at the end of Q1 to $300 million by the end of Q2. This improvement came despite a $33 million settlement payment related to the Ocado litigation, highlighting the company’s strong underlying cash generation capabilities.

Strategic Initiatives

AutoStore continues to execute on its growth strategy, which is built on three pillars: leveraging its strong foundation, implementing short-term actions, and focusing on strategic growth drivers. The company has reorganized and reallocated investments toward high-growth initiatives while sharpening its product focus to accelerate innovation.

A key component of AutoStore’s strategy is expanding its recurring revenue streams through software, Pio (its entry-level solution), and the AutoStore-as-a-Service offering. During Q2, the company signed a new AutoStore-as-a-Service contract worth $6.9 million with a European 3PL (third-party logistics) provider, demonstrating traction in this business model.

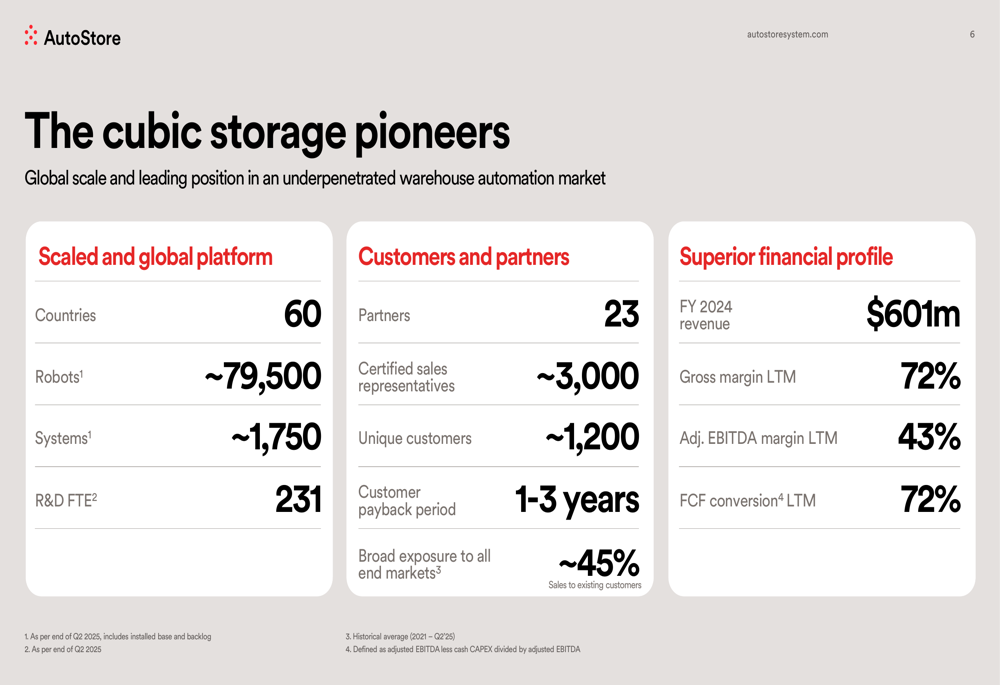

The company’s global scale provides a solid foundation for future growth, with operations in 60 countries, approximately 79,500 robots deployed, and around 1,750 systems installed. AutoStore serves a diverse range of industries, with particularly strong penetration in apparel/sports accessories, industrials, and 3PL sectors.

The company highlighted its diverse customer base across multiple end-markets, showcasing its ability to serve various industries with different requirements:

Forward-Looking Statements

Looking ahead, AutoStore plans to launch new software and hardware solutions in October 2025, continuing its focus on innovation. The company emphasized several key takeaways for investors, including the massive under-penetrated market driven by megatrends, its adaptation to uncertainty through strategic execution, and its positioning for long-term value creation.

The consistent growth in order intake and backlog suggests potential for revenue recovery in coming quarters, assuming conversion rates remain stable. The company’s strong cash position provides flexibility to navigate market uncertainties while continuing to invest in innovation.

While AutoStore faces challenges including geopolitical and macroeconomic volatility, as mentioned in its Q1 earnings call, the Q2 results demonstrate the company’s ability to execute its transformation plan effectively. The sequential improvements across key metrics suggest that AutoStore is making progress in adapting to current market conditions, though year-over-year comparisons indicate that full recovery may take additional time.

As warehouse automation adoption continues to grow globally, AutoStore’s established market position, technological leadership, and expanding service offerings position it to potentially benefit from long-term industry trends, despite near-term volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.