Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Avantor Inc (NYSE:AVTR), a leading provider of mission-critical products and services to customers in the biopharma and healthcare sectors, released its first quarter 2025 earnings presentation on April 25, 2025. The company’s shares plunged 11.48% in premarket trading to $13.72 following the release, as investors reacted to declining revenue and downward revisions to full-year guidance.

The Q1 results come after a challenging period for Avantor, which had previously shown signs of stabilization in its laboratory business and growth potential in bioprocessing. The company has been focusing on cost-cutting initiatives and recently completed the divestiture of its clinical services assets to strengthen its balance sheet.

Quarterly Performance Highlights

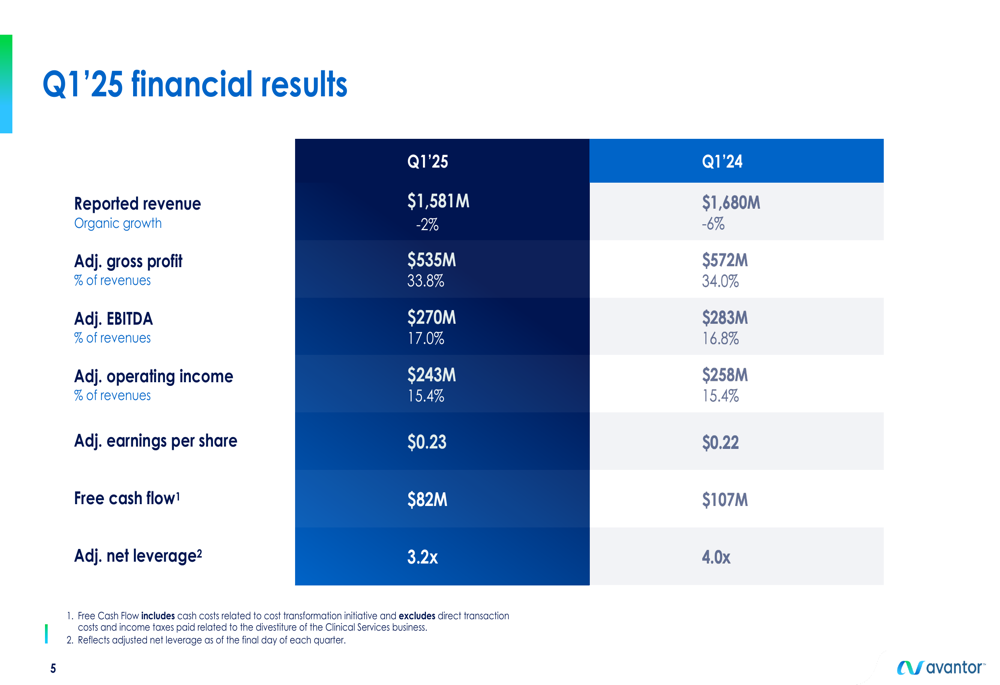

Avantor reported Q1 2025 revenue of $1.58 billion, representing a decline from $1.68 billion in the same period last year. However, the company’s organic revenue decline improved to -2% compared to -6% in Q1 2024, suggesting some progress in stabilizing its business.

As shown in the following financial highlights from the presentation:

Despite revenue challenges, Avantor managed to improve its profitability metrics. The company reported an adjusted EBITDA margin of 17.0%, slightly up from 16.8% in the prior year period. Adjusted earnings per share increased to $0.23 from $0.22, demonstrating the company’s ability to control costs effectively amid revenue pressures.

Free cash flow came in at $82 million, down from $107 million in Q1 2024, while the company improved its adjusted net leverage to 3.2x from 4.0x, reflecting progress in strengthening its balance sheet.

A more detailed comparison of financial results between Q1 2025 and Q1 2024 is presented in this comprehensive table:

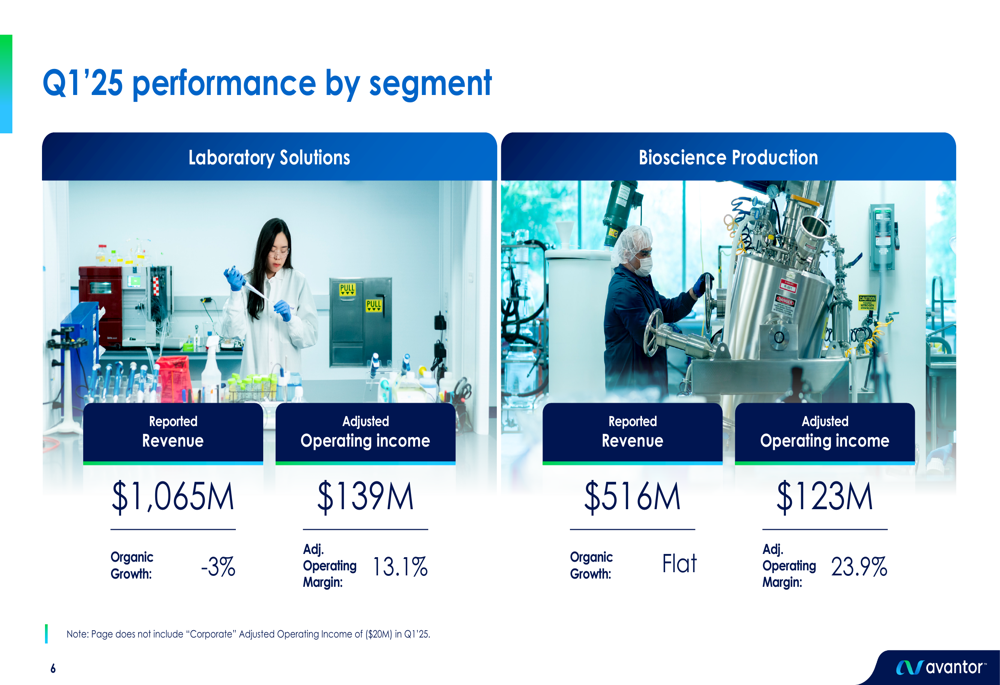

Segment Analysis

Avantor’s performance varied significantly across its two main business segments. The Laboratory Solutions segment, which represents approximately two-thirds of the company’s revenue, reported $1.065 billion in revenue with a -3% organic growth rate. This marks a reversal from the positive trend mentioned in previous quarters, where the lab business had shown signs of recovery.

The Bioscience Production segment generated $516 million in revenue with flat organic growth, which represents a stabilization compared to the 3.5% organic decline reported in Q3 2024. This segment’s performance is particularly important as Avantor has been positioning it as a key growth driver.

The following segment breakdown illustrates the performance of each business unit:

Revised Guidance & Strategic Initiatives

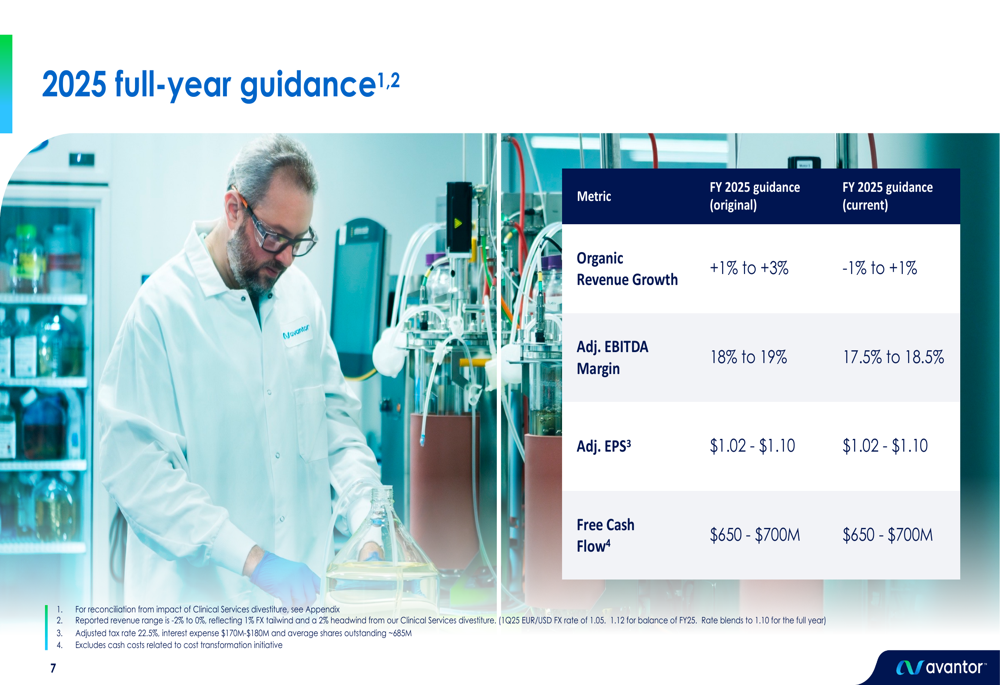

In a significant development, Avantor revised its full-year 2025 guidance downward, reflecting continued market challenges. The company now expects organic revenue growth between -1% and +1%, down from its original projection of +1% to +3%. Similarly, adjusted EBITDA margin guidance was lowered to 17.5%-18.5% from the previous 18%-19% range.

The revised guidance is detailed in the following slide:

Despite these revisions, Avantor maintained its adjusted EPS guidance of $1.02-$1.10 and free cash flow guidance of $650-$700 million, suggesting confidence in its cost control measures and cash generation capabilities.

The company highlighted three strategic priorities in its presentation:

1. Controlling the controllables amid macro volatility

2. Executing strategy to accelerate growth in Laboratory Solutions Segment

3. Enhancing cost structure

Notably, Avantor reported being on track to deliver $300 million in cost savings and has identified opportunities to expand these savings to $400 million, which could help offset revenue challenges.

Market Reaction & Outlook

The significant premarket drop in Avantor’s stock price indicates that investors are concerned about the company’s growth trajectory and revised guidance. The downward revision in organic revenue growth expectations suggests that market challenges are persisting longer than previously anticipated.

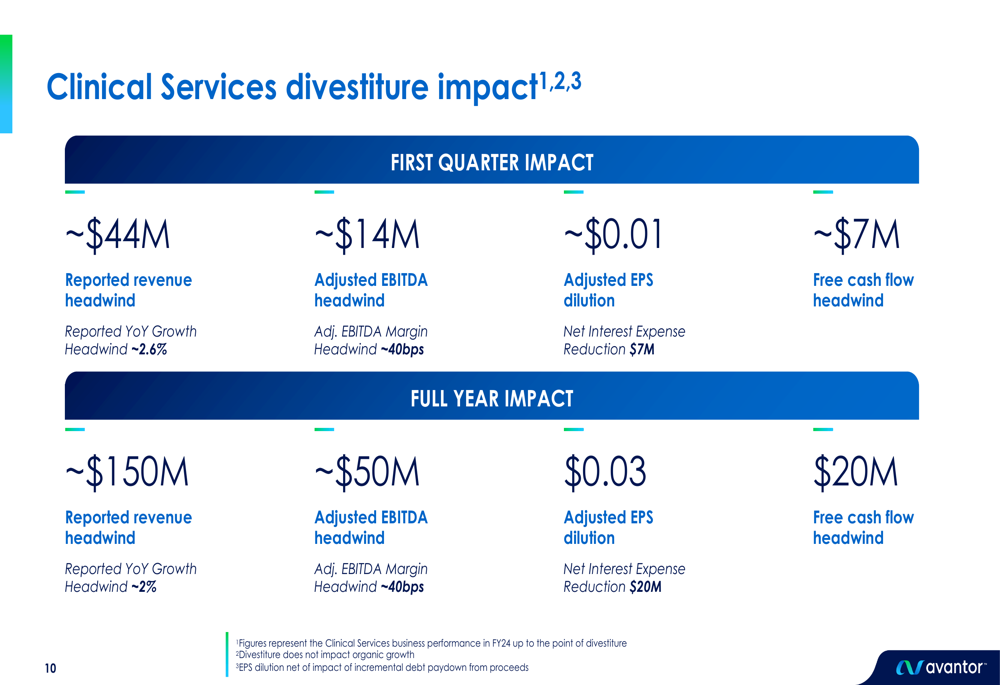

The divestiture of clinical services assets, completed in late 2024, continues to impact Avantor’s financial results. As detailed in the presentation, this divestiture created headwinds of approximately $44 million in revenue and $14 million in adjusted EBITDA for the first quarter, with full-year impacts estimated at $150 million and $50 million, respectively.

Looking ahead, Avantor faces the challenge of returning its Laboratory Solutions segment to growth while maintaining the stabilization in its Bioscience Production segment. The company’s ability to execute on its expanded cost savings initiatives will be crucial for meeting its maintained EPS and free cash flow guidance despite lower revenue expectations.

While market conditions remain challenging, Avantor’s focus on margin improvement, cost control, and strategic portfolio adjustments demonstrates management’s commitment to navigating the current environment and positioning the company for future growth when market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.