BofA update shows where active managers are putting money

Introduction & Market Context

Avantor Inc (NYSE:AVTR) released its second-quarter 2025 earnings presentation on August 1, showing flat revenue growth and a significant downward revision of its full-year guidance. The laboratory solutions provider’s stock dropped 3.05% in pre-market trading to $13.03, continuing a downward trend that has seen the stock approach its 52-week low of $11.82.

The presentation comes after a disappointing first quarter when Avantor missed revenue expectations, triggering an 11.29% stock decline. The company’s current market capitalization stands at approximately $10.56 billion, with the stock down 2.61% in the previous session.

Quarterly Performance Highlights

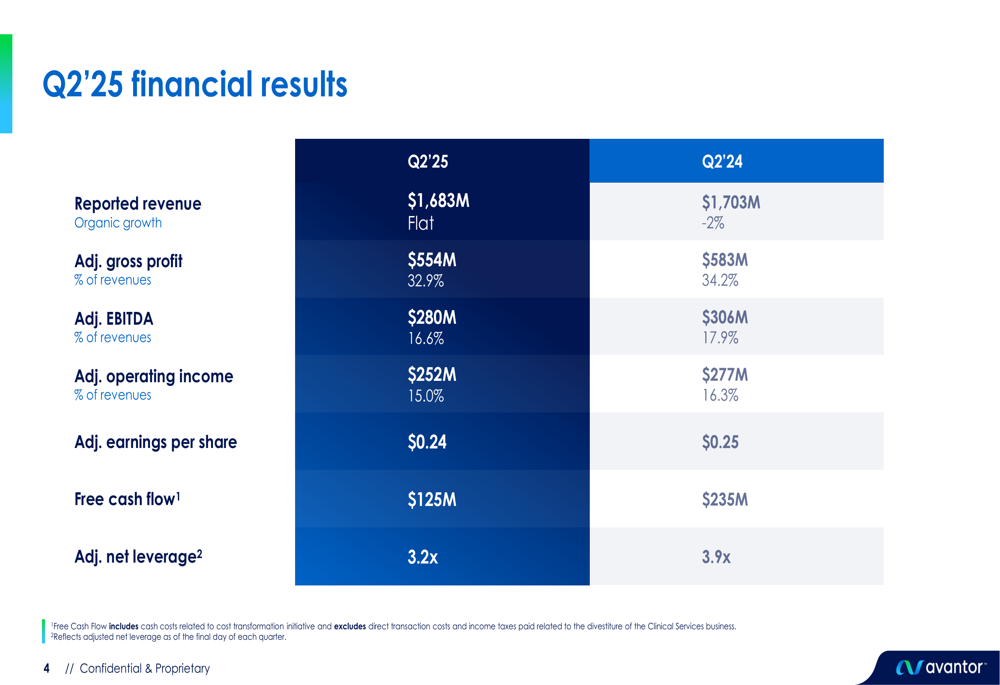

Avantor reported Q2 2025 revenue of $1.68 billion, essentially flat compared to the same period last year. Other key financial metrics showed year-over-year declines across several areas.

As shown in the following performance highlights from the presentation:

The company’s adjusted EBITDA margin contracted to 16.6% from 17.9% in Q2 2024, while adjusted earnings per share declined slightly to $0.24 from $0.25 a year earlier. Free cash flow saw a significant decrease to $125 million, down from $235 million in the comparable period.

A more detailed breakdown of the financial results reveals margin pressure across multiple metrics:

Adjusted gross profit declined to $554 million (32.9% of revenues) compared to $583 million (34.2%) in Q2 2024. Adjusted operating income fell to $252 million (15.0% of revenues) from $277 million (16.3%) a year earlier. One positive note was the improvement in adjusted net leverage to 3.2x from 3.9x in the prior year.

Segment Performance Analysis

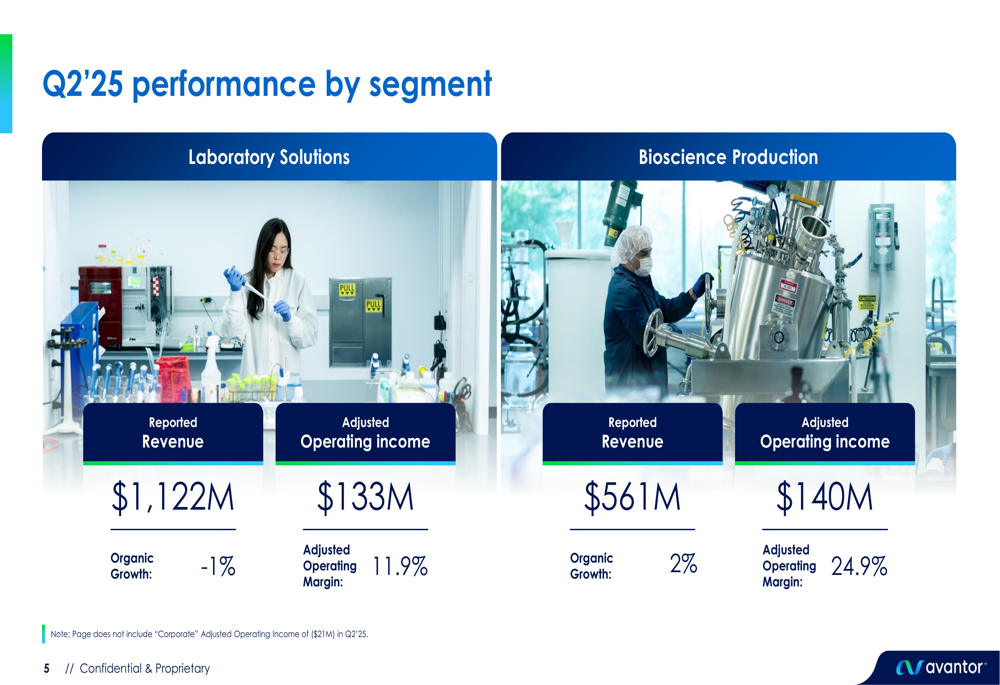

Avantor’s performance showed divergence between its two main business segments. The Laboratory Solutions segment, which represents approximately two-thirds of total revenue, experienced a 1% organic decline, while the Bioscience Production segment showed modest 2% organic growth.

The following segment breakdown illustrates this performance divergence:

The Laboratory Solutions segment generated $1.12 billion in revenue with an adjusted operating margin of 11.9%. This segment has been facing challenges in the education and government sectors, as noted in the company’s previous earnings call.

Meanwhile, the Bioscience Production segment delivered $561 million in revenue with a substantially higher adjusted operating margin of 24.9%. The presentation highlighted "double-digit silicones growth and continued strong demand for monoclonal antibody platform," though it also noted that "bioprocessing growth was flat due to customer challenges and backorders."

Revised Guidance & Outlook

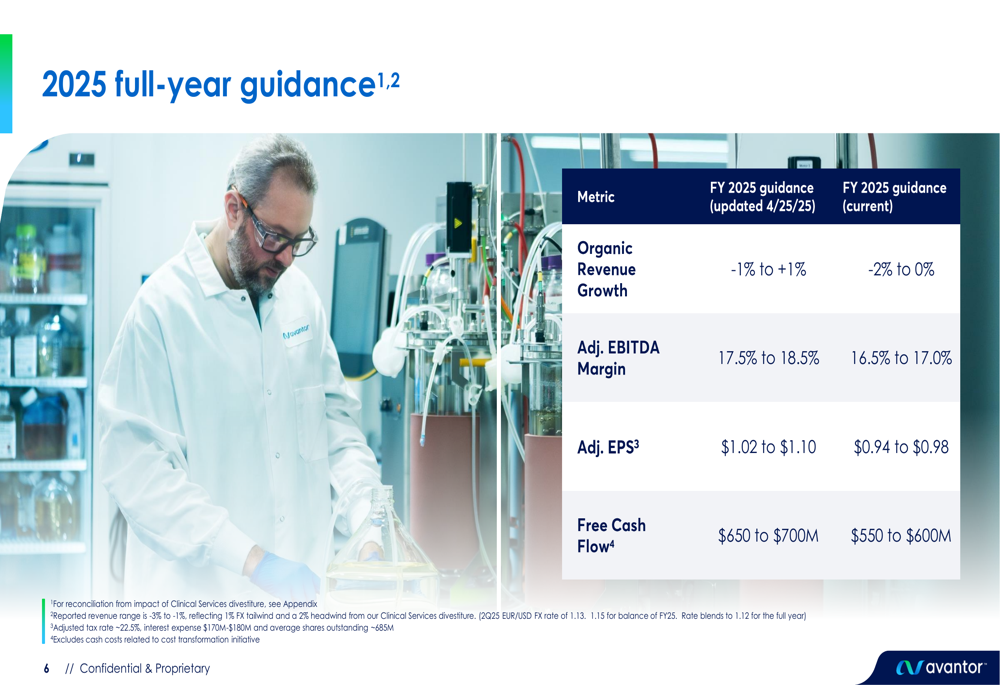

Perhaps the most significant revelation in the presentation was Avantor’s downward revision of its full-year 2025 guidance across all key metrics:

The company now expects organic revenue growth between -2% and 0%, down from its previous guidance of -1% to +1%. Adjusted EBITDA margin expectations were lowered to 16.5%-17.0% from the previous 17.5%-18.5% range. Adjusted EPS guidance was cut to $0.94-$0.98 from $1.02-$1.10, and free cash flow projections were reduced to $550-$600 million from $650-$700 million.

This downward revision follows the Q1 earnings call where CEO Michael Stubblefield acknowledged that the company was "not satisfied with our overall results" and announced plans to step down, prompting a search for his successor.

Strategic Initiatives & Challenges

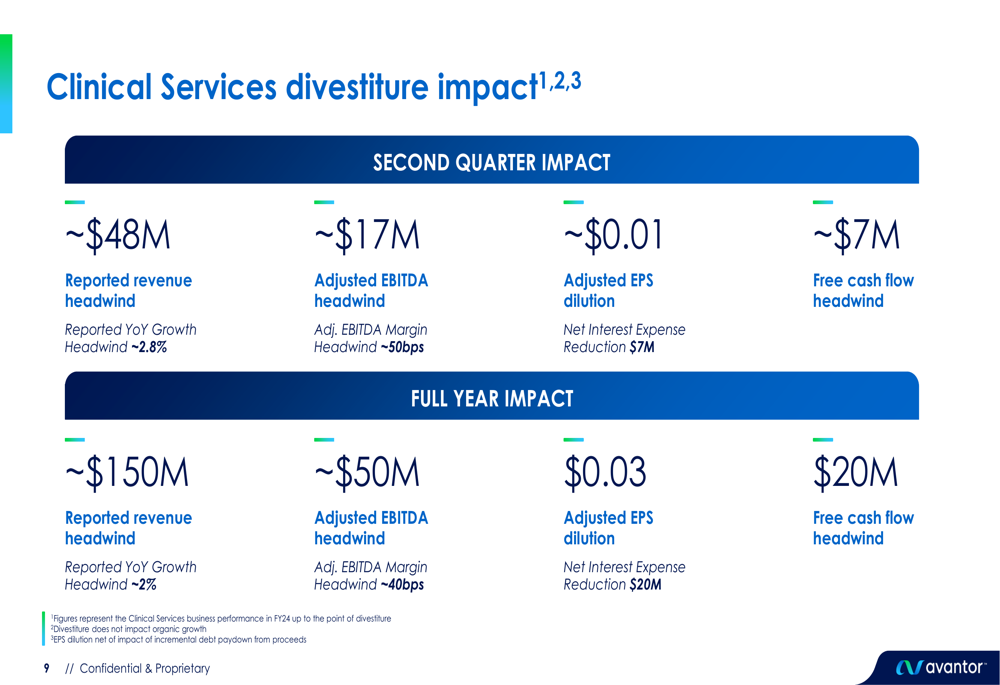

A significant factor affecting Avantor’s financial performance is the recent divestiture of its Clinical Services business. The presentation quantified this impact:

The divestiture created approximately $48 million in revenue headwind for Q2 2025, representing about 2.8% of year-over-year growth. For the full year, the impact is expected to be around $150 million in revenue, or about 2% of annual growth. The transaction also affected adjusted EBITDA by approximately $17 million in Q2 and is projected to impact full-year adjusted EBITDA by about $50 million.

Despite these challenges, the presentation highlighted several positive developments, including sequential growth in Laboratory Solutions, contract expansions/extensions (including a 5-year BIO contract extension), and the launch of a digital suite of tools and pricing optimization. The company also stated it remains on track to deliver its run-rate target of $400 million in cost savings by 2027, a transformation initiative mentioned in previous communications.

Forward-Looking Statements

Avantor faces significant headwinds as it navigates through 2025. The revised guidance suggests continued challenges in the near term, particularly in the Laboratory Solutions segment. The company’s ability to execute its cost transformation initiative will be crucial to maintaining profitability amid slower growth.

The impact of the Clinical Services divestiture will continue to affect year-over-year comparisons through 2025, though the improved leverage ratio suggests the company is making progress in strengthening its balance sheet. Investors will likely focus on whether Avantor can stabilize its Laboratory Solutions segment while continuing to drive growth in the higher-margin Bioscience Production business.

As the search for a new CEO continues, Avantor’s strategic direction and ability to return to growth remain key questions for investors evaluating the company’s long-term prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.