Bank of America just raised its EUR/USD forecast

Introduction & Market Context

Avery Dennison Corporation (NYSE:AVY) released its first quarter 2025 financial results on April 23, showing modest growth despite currency headwinds. The company reported net sales of $2.1 billion with organic sales growth of 2.3%, while adjusted earnings per share reached $2.30, up 0.4% year-over-year but approximately 4% higher when excluding currency effects.

The materials science and manufacturing company’s stock is showing significant volatility, with premarket trading indicating a 4.13% decline to $167.61 after closing up 3.43% at $174.83 the previous day. This reaction follows a quarter that demonstrated the company’s resilience but also highlighted challenges in certain segments.

Quarterly Performance Highlights

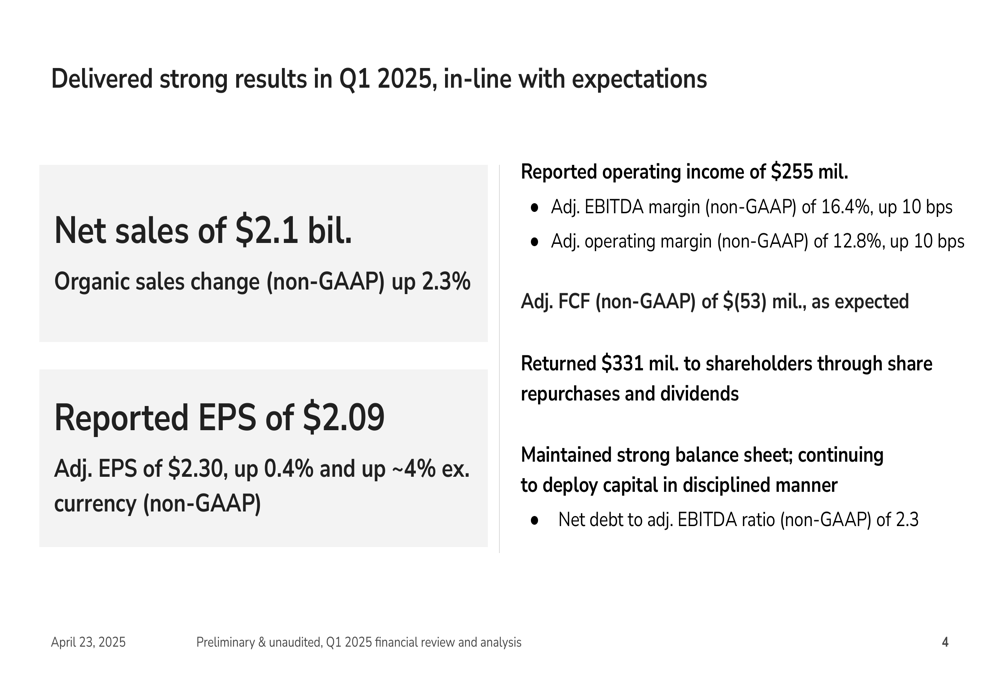

Avery Dennison’s Q1 2025 financial performance showed mixed results across key metrics. The company achieved $2.1 billion in net sales with reported EPS of $2.09 and adjusted EPS of $2.30. Operating income reached $255 million, while adjusted EBITDA margin improved slightly to 16.4%, up 10 basis points from the prior year.

As shown in the following financial highlights slide, the company returned $331 million to shareholders through share repurchases and dividends while maintaining a net debt to adjusted EBITDA ratio of 2.3:

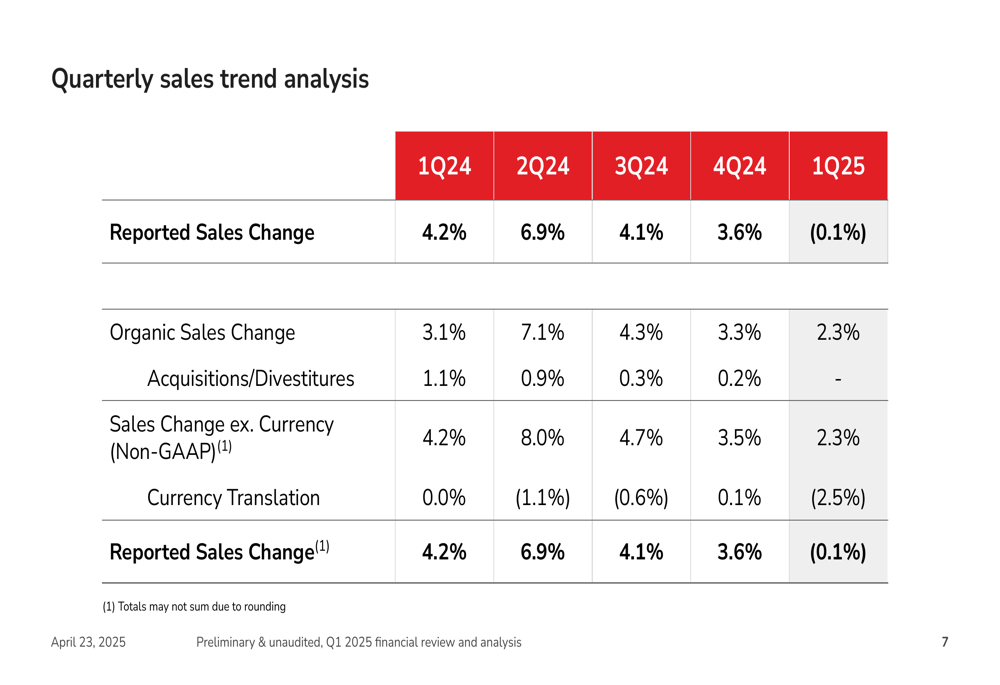

The company’s organic sales growth of 2.3% represents a sequential decline from the 3.3% growth reported in Q4 2024, continuing a gradual deceleration trend observed over the past year. This trend is illustrated in the quarterly sales analysis:

Segment Analysis

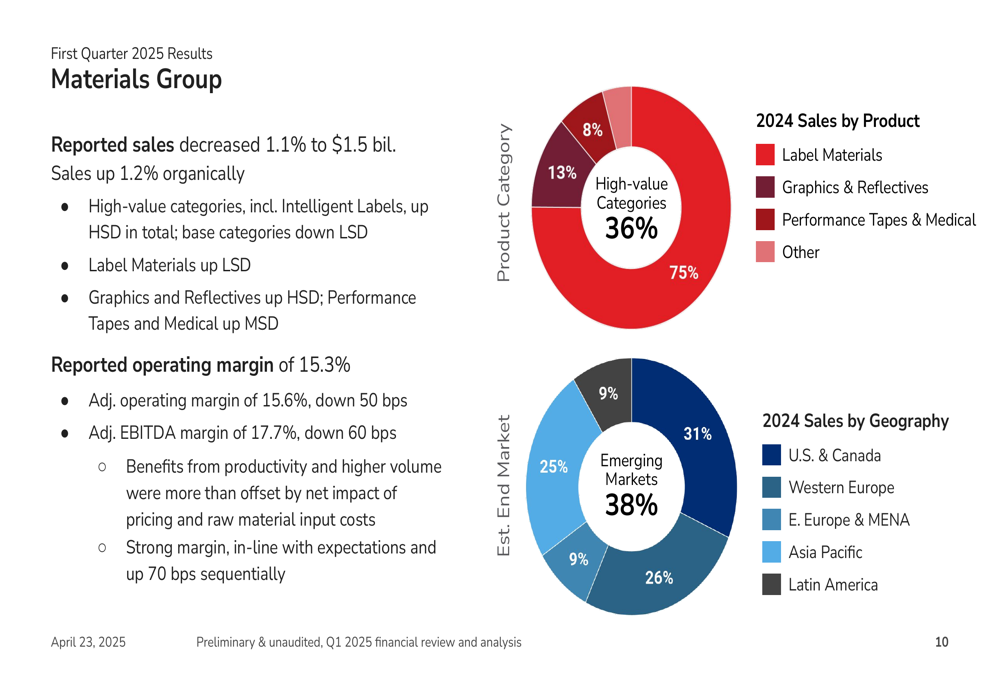

Avery Dennison’s two main business segments showed divergent performance in Q1 2025. The Materials Group, which accounts for approximately 70% of total sales, delivered 1.2% organic growth, while the Solutions Group achieved a more robust 4.9% organic growth rate.

The Materials Group reported sales of $1.5 billion, down 1.1% on a reported basis but up 1.2% organically. High-value categories within this segment performed well, showing high single-digit growth, while base categories declined slightly. The segment’s adjusted EBITDA margin of 17.7% improved sequentially but declined year-over-year.

The following slide provides a detailed breakdown of the Materials Group’s performance, including product and geographic distribution:

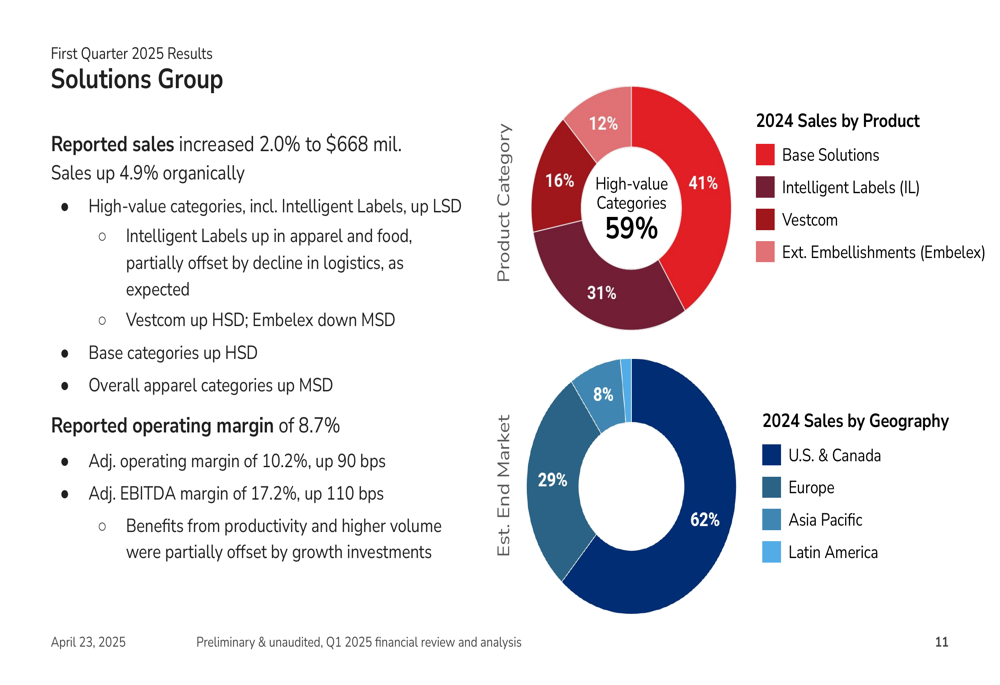

The Solutions Group demonstrated stronger performance with reported sales increasing 2.0% to $668 million and organic sales growth of 4.9%. The segment’s adjusted EBITDA margin improved significantly to 17.2%, up 110 basis points year-over-year, reflecting the success of the company’s high-value solutions strategy.

The Solutions Group’s performance breakdown, including its product and geographic mix, is illustrated below:

Strategic Initiatives

Avery Dennison continues to focus on its high-value categories, which delivered sales of approximately $1.0 billion in Q1 2025, growing at mid-single digits organically. These categories now represent nearly half of the company’s portfolio and are central to its strategy of shifting toward more differentiated, higher-margin products.

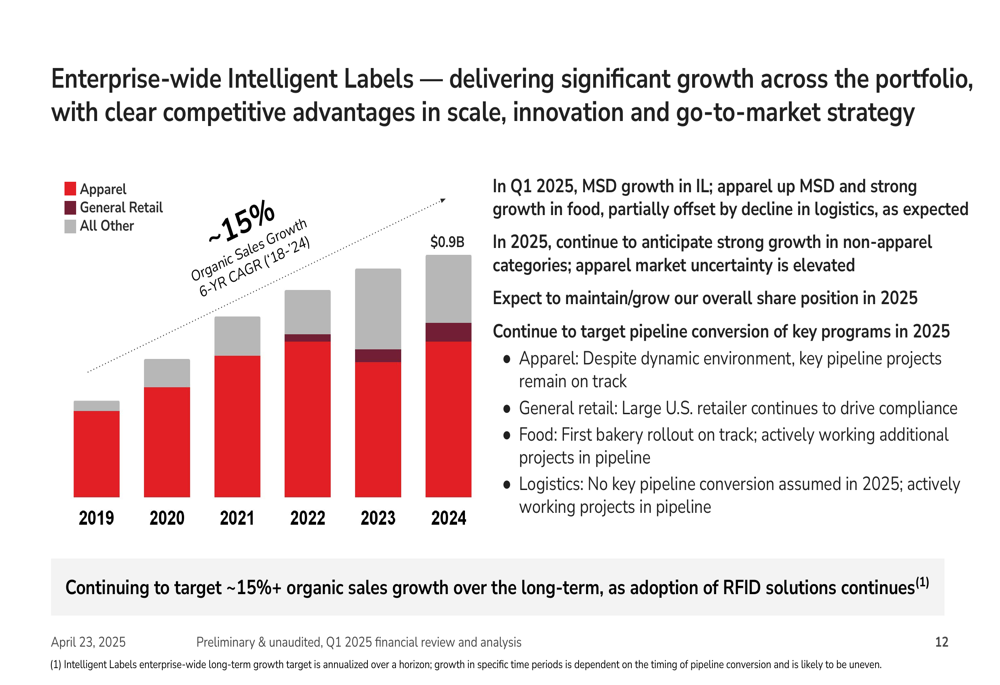

A key component of this strategy is the company’s Enterprise-wide Intelligent Labels business, which showed mid-single digit growth in Q1 2025, with apparel applications up mid-single digits and strong growth in food applications. However, this growth rate falls below the company’s long-term target of approximately 15%+ organic sales growth, raising questions about achieving full-year growth targets.

The following chart illustrates the company’s Intelligent Labels growth trajectory:

This performance comes after Intelligent Labels grew 9% organically in 2024, according to the company’s Q4 2024 earnings report. For 2025, management continues to target 10-15% growth in this segment, suggesting an expected acceleration in the coming quarters.

Forward-Looking Statements

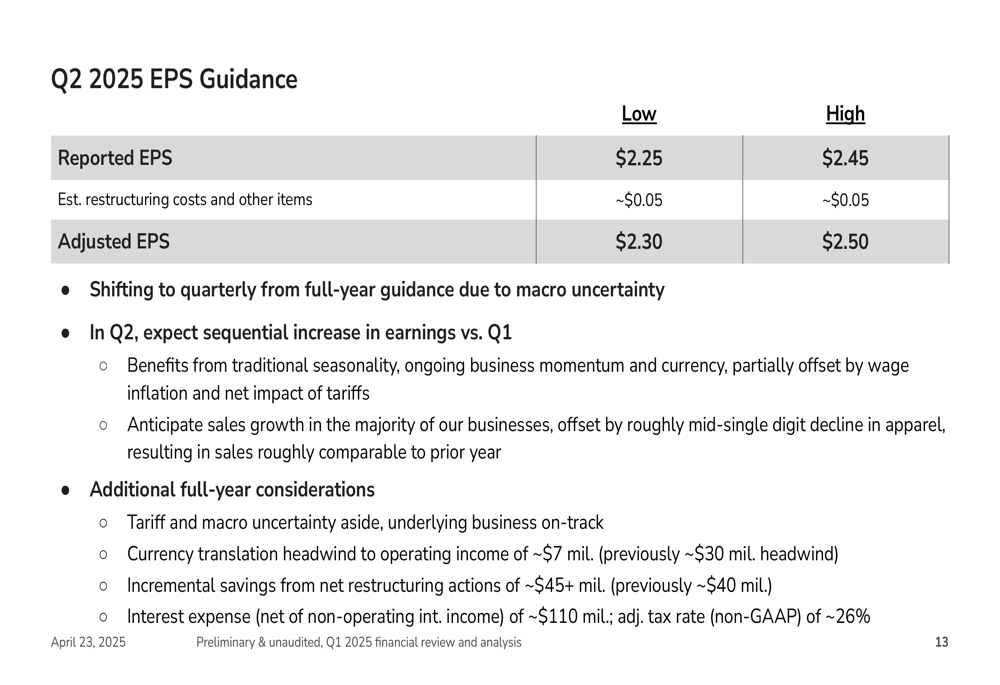

Looking ahead to Q2 2025, Avery Dennison provided adjusted EPS guidance of $2.30 to $2.50, as shown in the following guidance slide:

The company noted that it expects a sequential increase in earnings compared to Q1, reflecting anticipated improvements in volume and productivity. Due to macroeconomic uncertainty, Avery Dennison has shifted to providing quarterly guidance rather than annual forecasts.

Management highlighted that direct impact from recent tariffs is manageable, but indirect impacts remain more uncertain. Approximately 5% of the company’s total revenue is linked indirectly to Chinese exports to the U.S., primarily in apparel-related categories. The company is implementing sourcing and pricing actions to mitigate tariff impacts.

Capital Allocation and Balance Sheet

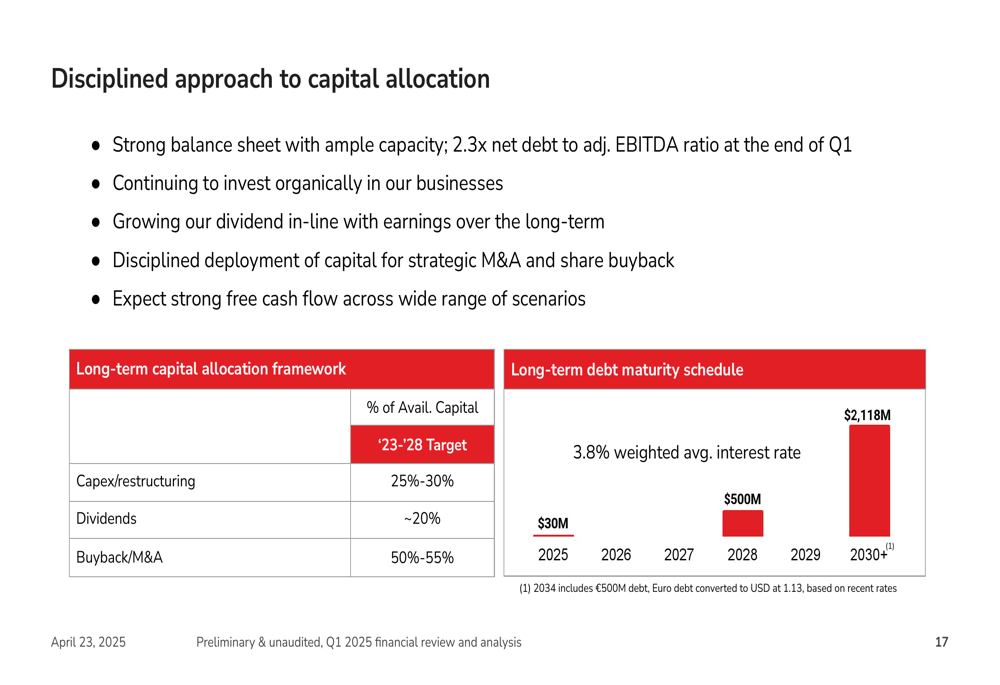

Avery Dennison continues to maintain a disciplined approach to capital allocation. The company’s framework allocates approximately 25-30% of available capital to capital expenditures and restructuring, about 20% to dividends, and 50-55% to share buybacks and acquisitions.

The company’s capital allocation strategy and debt maturity schedule are illustrated in the following slide:

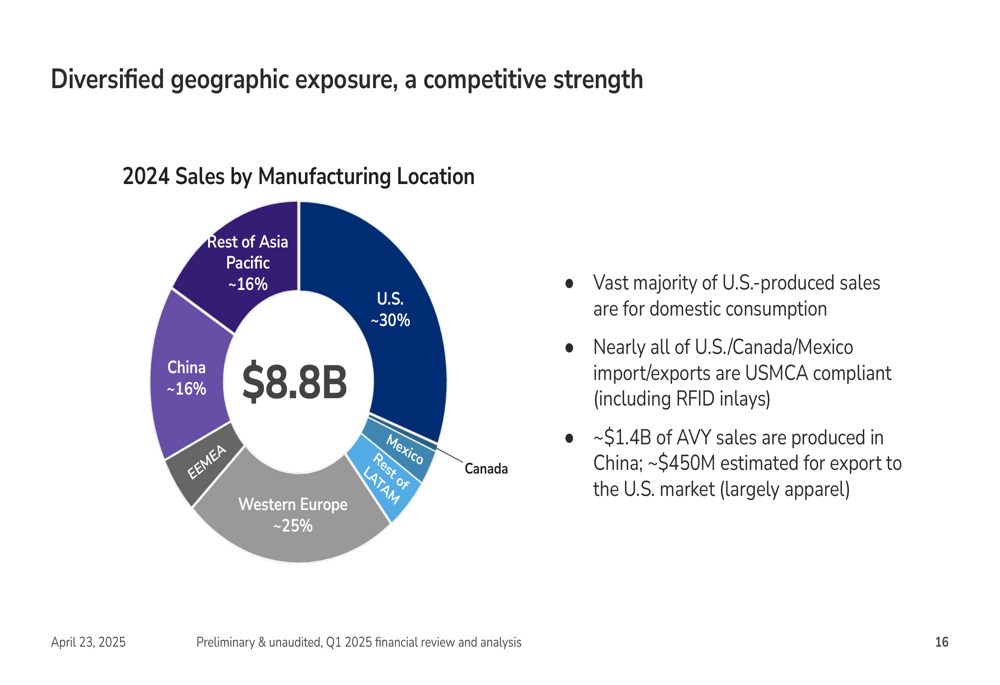

This approach has allowed Avery Dennison to maintain a strong balance sheet while returning significant value to shareholders. The company’s manufacturing footprint remains well-diversified globally, providing flexibility in responding to geopolitical challenges and trade tensions:

Conclusion

Avery Dennison’s Q1 2025 results demonstrate the company’s ability to deliver modest growth despite currency headwinds and macroeconomic uncertainties. The Solutions Group’s strong performance, particularly in high-value categories, partially offset slower growth in the Materials Group.

While the company maintains its position as a market leader with the #1 position in over 80% of its portfolio, challenges remain in accelerating growth in strategic areas like Intelligent Labels to meet long-term targets. The shift to quarterly guidance signals caution about the macroeconomic environment, though management remains confident in the company’s ability to navigate uncertainties through its diversified business model and proven playbooks.

Investors will be watching closely to see if growth accelerates in the coming quarters, particularly in the high-value categories that are central to the company’s long-term strategy. The Q2 guidance suggests management expects some improvement, but execution will be key in an increasingly uncertain global trade environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.