Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Avis Budget Group (NASDAQ:CAR) released its second quarter 2025 financial results on July 30, showing a significant improvement in profitability despite flat revenue. The company’s stock responded positively in after-hours trading, rising 3.48% to $213.20, continuing its strong momentum that has seen the stock more than triple from its 52-week low of $54.03.

The Q2 results mark a substantial recovery from the company’s disappointing first quarter, when Avis reported an adjusted EBITDA loss of $93 million and missed earnings expectations by a wide margin. The rental car giant has demonstrated resilience through effective fleet management and cost control measures, particularly in its international operations.

Quarterly Performance Highlights

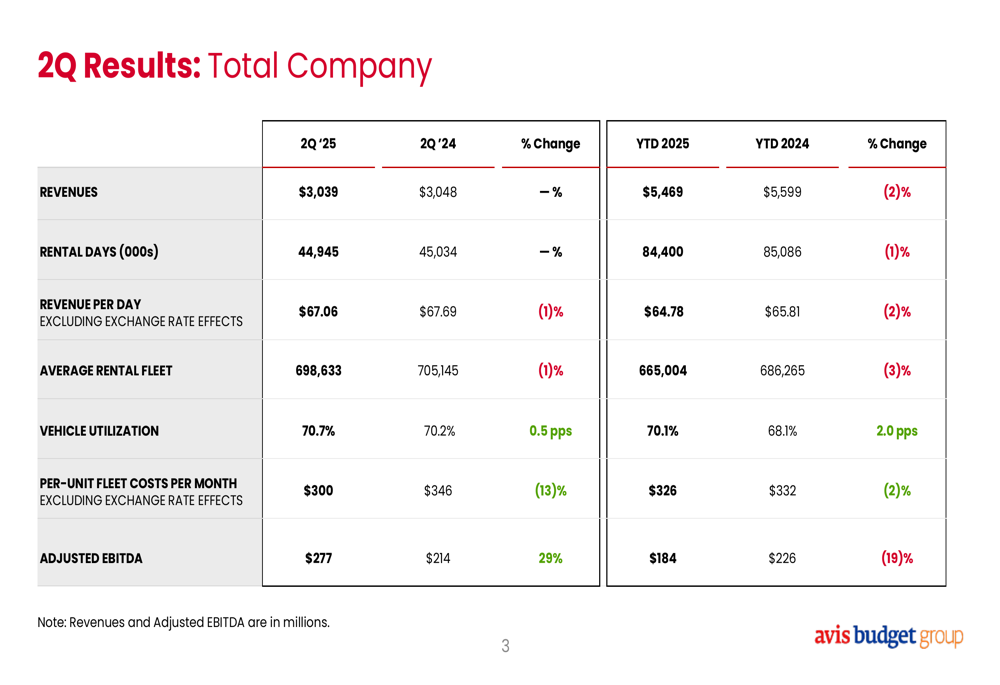

Avis Budget reported Q2 2025 revenue of $3,039 million, essentially flat compared to $3,048 million in the same period last year. However, the company achieved a remarkable 29% increase in Adjusted EBITDA, which rose to $277 million from $214 million in Q2 2024.

This improvement in profitability came despite a slight decrease in rental days and revenue per day, highlighting the company’s focus on operational efficiency. Vehicle utilization improved to 70.7%, up 0.5 percentage points year-over-year, while per-unit fleet costs decreased significantly by 13% to $300 per month.

As shown in the following comprehensive financial overview:

Year-to-date figures still show the impact of the challenging first quarter, with revenue down 2% to $5,469 million and Adjusted EBITDA down 19% to $184 million compared to the first half of 2024. However, the strong second quarter performance suggests the company is on a recovery trajectory.

Segment Analysis

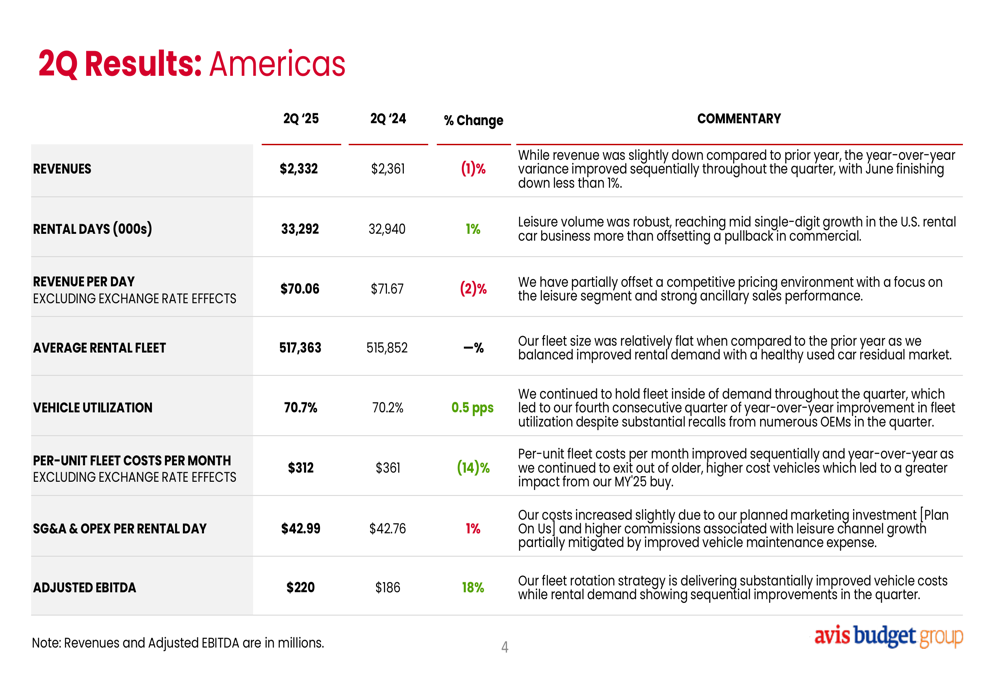

The Americas segment, which accounts for approximately 77% of total revenue, reported $2,332 million in Q2 2025, a slight 1% decrease from the previous year. Despite this, Adjusted EBITDA increased by 18% to $220 million, driven by a 14% reduction in per-unit fleet costs and a 1% increase in rental days.

The detailed Americas performance metrics reveal the effectiveness of the company’s fleet management strategy:

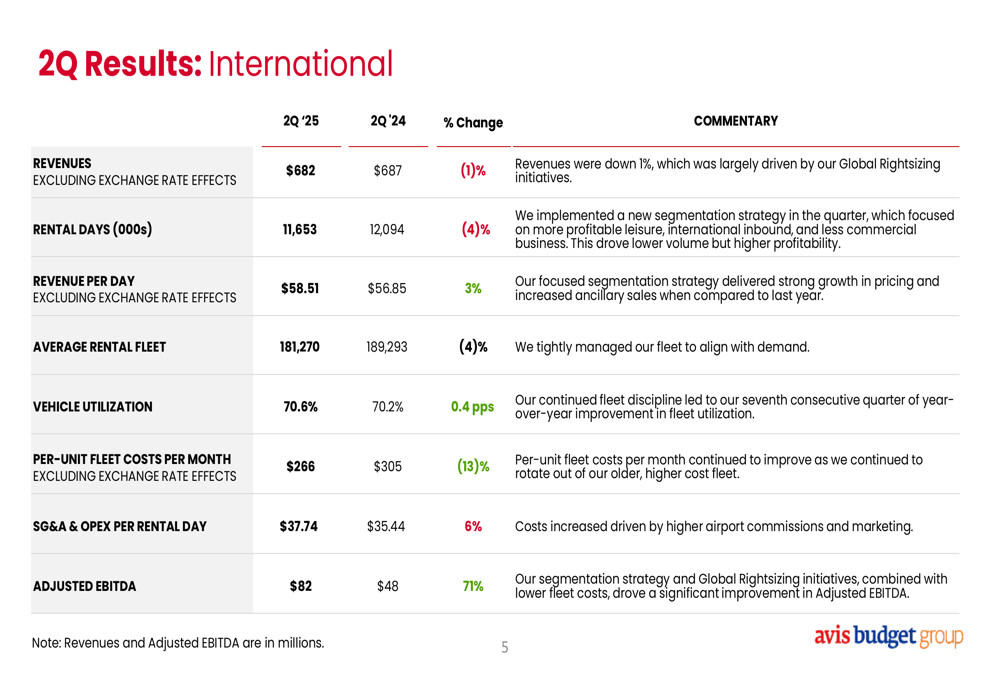

The International segment delivered exceptional results, with Adjusted EBITDA surging 71% to $82 million despite a 1% decrease in revenue (excluding exchange rate effects). This impressive performance was achieved through a 13% reduction in per-unit fleet costs and a 3% increase in revenue per day, which offset a 4% decrease in rental days.

The following chart illustrates the strong performance of the International segment:

The International results demonstrate the success of Avis Budget’s "Global Rightsizing" initiatives and new segmentation strategy, which have improved profitability despite reduced volume.

Financial Position & Liquidity

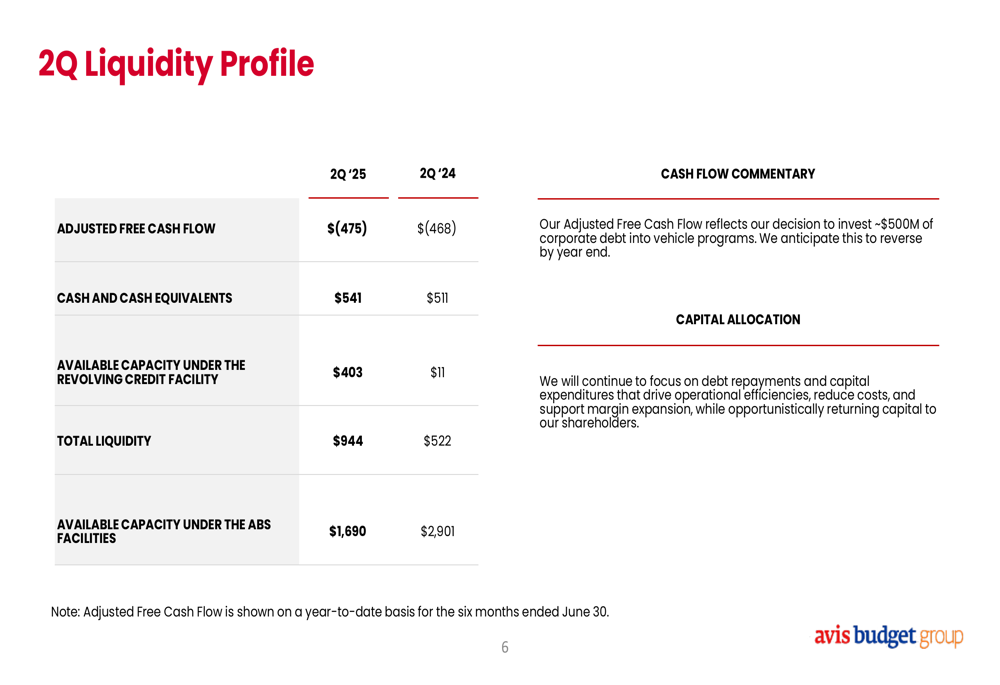

Avis Budget significantly strengthened its liquidity position in Q2 2025, with total liquidity increasing to $944 million from $522 million in the same period last year. This improvement was primarily driven by increased available capacity under the revolving credit facility, which rose to $403 million from just $11 million a year ago.

The company’s liquidity profile is detailed in the following chart:

Adjusted Free Cash Flow remained negative at $(475) million for the first half of 2025, similar to the $(468) million reported in the same period of 2024. This reflects the company’s strategic decision to invest in vehicle programs as part of its fleet management strategy.

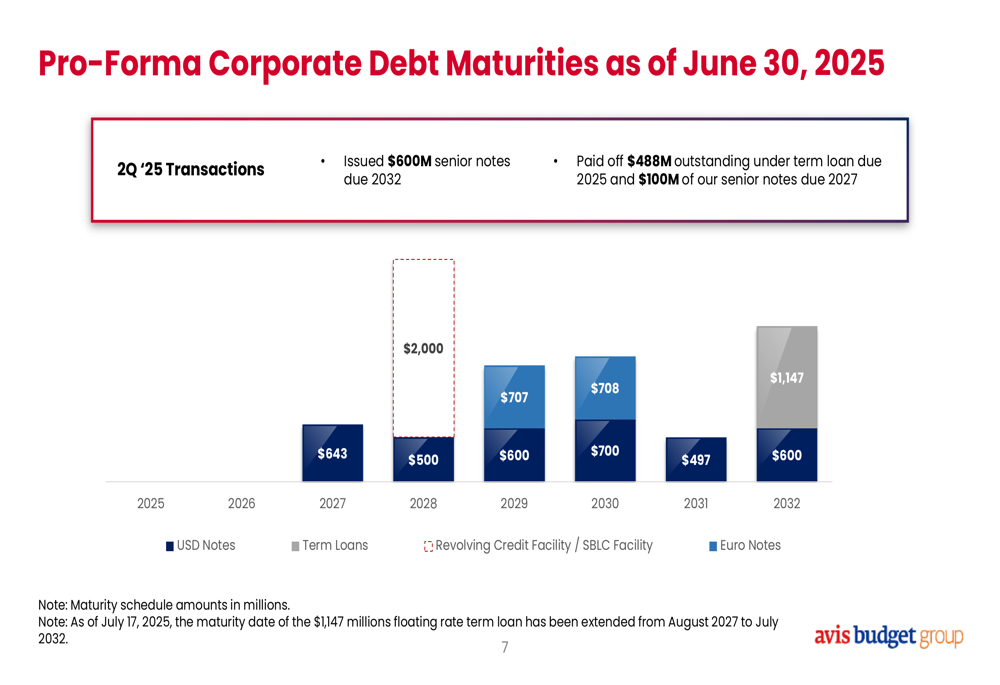

Avis Budget also made significant progress in managing its debt profile, issuing $600 million in senior notes due in 2032 and paying off $488 million outstanding under a term loan due in 2025 and $100 million of senior notes due in 2027. Additionally, the company extended the maturity date of its $1,147 million floating rate term loan from August 2027 to July 2032.

The following chart shows the company’s updated debt maturity schedule:

Forward-Looking Statements

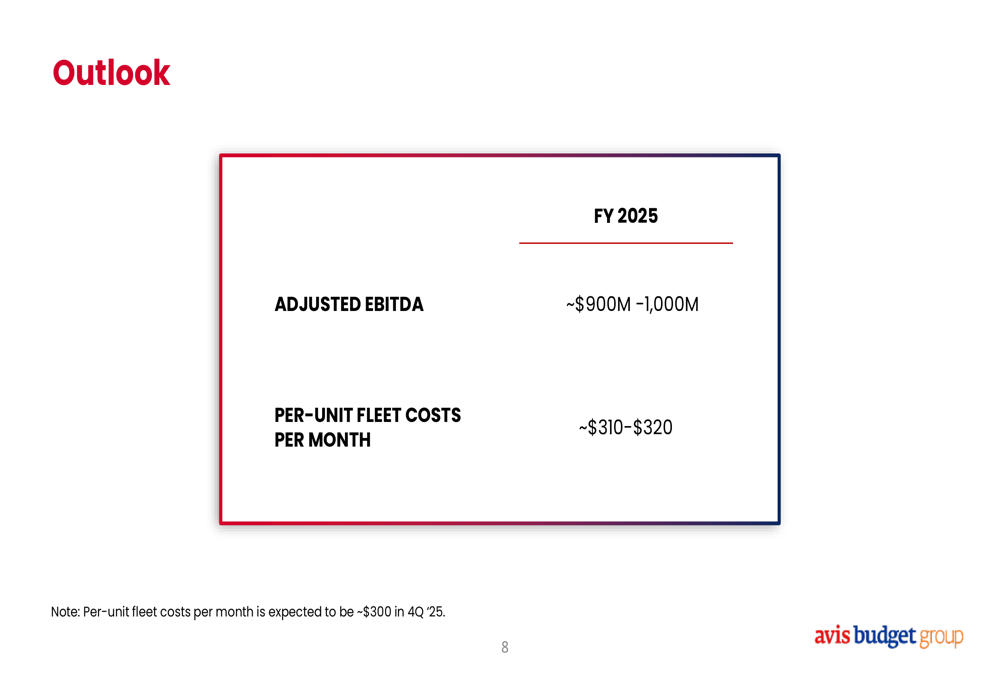

Despite the challenges faced in the first quarter, Avis Budget maintained its full-year 2025 Adjusted EBITDA guidance of approximately $900 million to $1 billion. The company expects per-unit fleet costs per month to be in the range of $310-$320 for the full year, with costs projected to decrease to approximately $300 in the fourth quarter.

The company’s outlook for the remainder of 2025 is summarized in the following slide:

This guidance aligns with management’s statements during the Q1 earnings call, where CEO Joe Ferraro (who has since announced his retirement effective June 30) emphasized the company’s strategic positioning and CFO Izzy Martins reiterated the goal of achieving at least $1 billion in Adjusted EBITDA for the year.

Detailed Financial Analysis

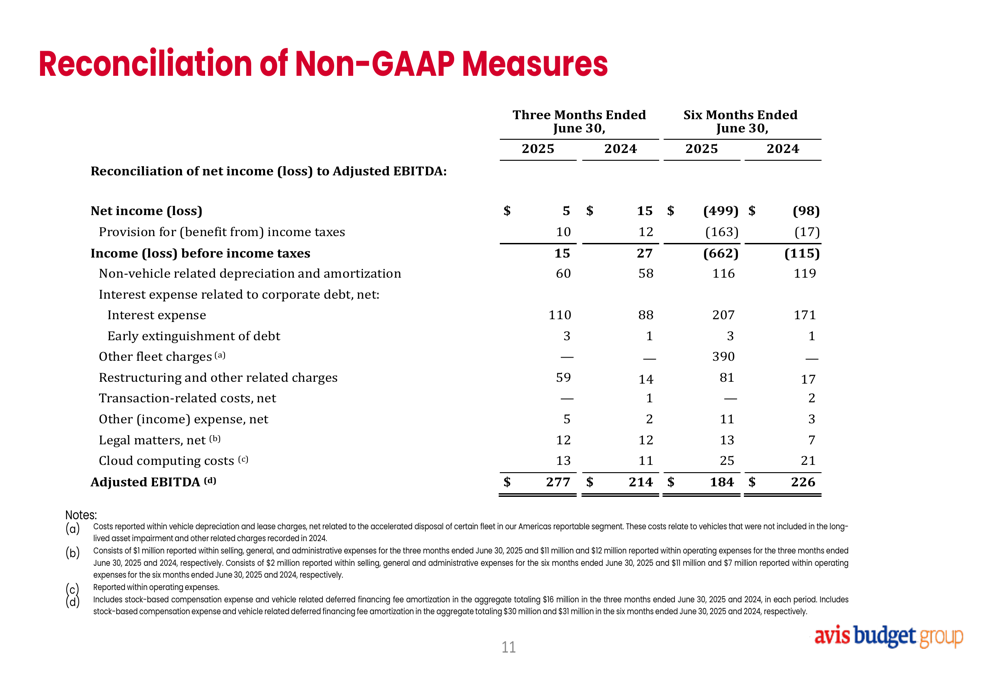

A closer examination of Avis Budget’s financial performance reveals that the improvement in Adjusted EBITDA was achieved despite challenges in net income. For Q2 2025, net income was just $5 million, down from $15 million in Q2 2024. Year-to-date net loss expanded significantly to $(499) million from $(98) million in the first half of 2024.

The reconciliation between net income and Adjusted EBITDA provides insight into the factors driving this divergence:

The substantial difference between net income and Adjusted EBITDA highlights the impact of non-vehicle related depreciation and amortization, as well as interest expenses related to corporate debt, which increased to $110 million in Q2 2025 from $88 million in Q2 2024.

The company’s ability to generate a significant improvement in Adjusted EBITDA despite these headwinds demonstrates the effectiveness of its operational strategies, particularly in fleet management and cost control. With continued execution on these initiatives and the expected reduction in per-unit fleet costs in the second half of the year, Avis Budget appears well-positioned to achieve its full-year financial targets and continue its recovery from the challenging start to 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.