Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Avista Corporation (NYSE:AVA) presented its Q2 2025 earnings results on August 6, 2025, revealing a mixed performance characterized by strong utility operations offset by weakness in its non-utility segments. The company’s stock closed at $38.25 on August 5, 2025, with a modest gain of 0.13%, as investors awaited the quarterly results.

The presentation, led by President and CEO Heather Rosentrater and CFO Kevin Christie, highlighted the company’s continued focus on regulatory outcomes, capital investment, and strategic execution despite headwinds in the clean technology sector.

Quarterly Performance Highlights

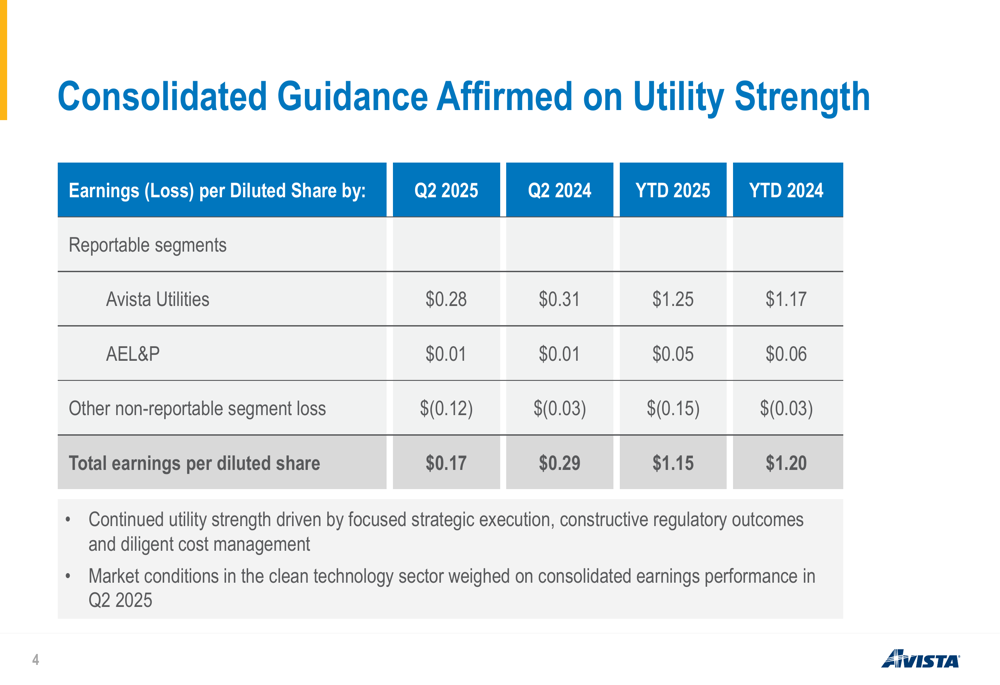

Avista reported consolidated earnings per diluted share of $0.17 for Q2 2025, a significant decrease from $0.29 in Q2 2024. Year-to-date earnings also declined slightly to $1.15 per share from $1.20 in the same period last year. The company attributed this decline primarily to losses in its non-utility businesses, which offset otherwise solid performance in its core utility operations.

As shown in the following earnings breakdown from the presentation:

The core Avista Utilities segment posted Q2 2025 earnings of $0.28 per share, down slightly from $0.31 in Q2 2024. However, year-to-date utility earnings showed improvement at $1.25 per share compared to $1.17 in 2024. The company’s Alaska Electric Light and Power (AEL&P) subsidiary maintained stable performance with $0.01 per share in Q2 and $0.05 year-to-date.

The most significant drag on performance came from Avista’s non-reportable segment, which posted a loss of $0.12 per share in Q2 2025, substantially worse than the $0.03 loss in Q2 2024. The company cited challenging market conditions in the clean technology sector as the primary factor behind this decline.

Detailed Financial Analysis

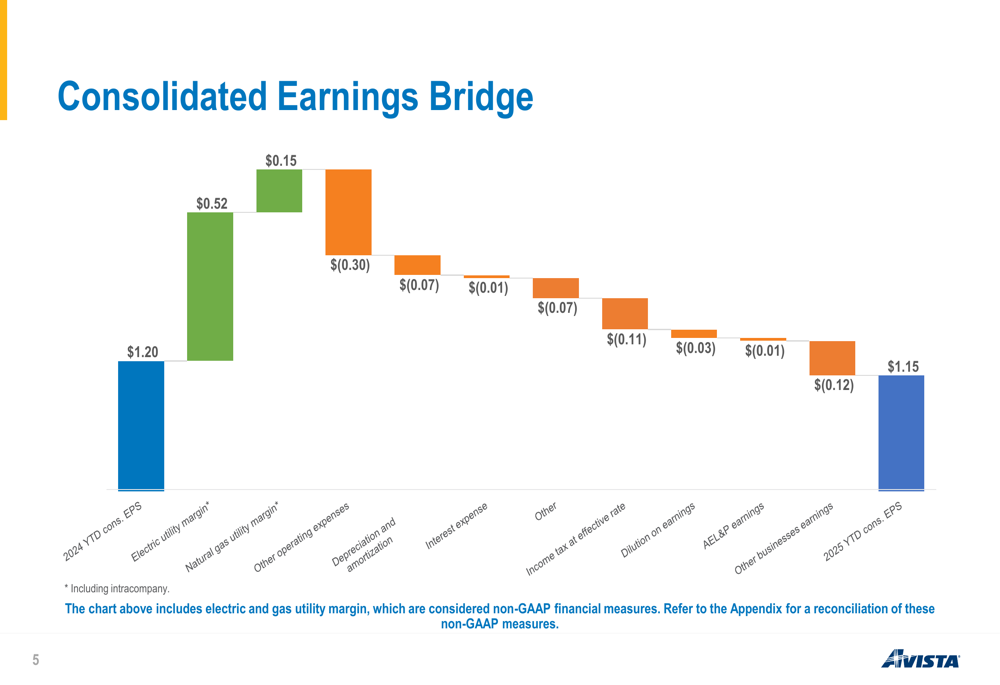

The presentation included a detailed earnings bridge that illustrated the key factors driving the change in year-to-date earnings from 2024 to 2025:

Positive contributions came from increased electric utility margin (+$0.52) and natural gas utility margin (+$0.15), reflecting the company’s successful regulatory outcomes and operational improvements. However, these gains were more than offset by increases in other operating expenses (-$0.30), depreciation and amortization (-$0.07), interest expense (-$0.01), and other factors (-$0.07).

Income tax effects (-$0.11), earnings dilution (-$0.03), slightly lower AEL&P earnings (-$0.01), and the significant decline in other businesses’ performance (-$0.12) ultimately resulted in the year-to-date earnings decrease to $1.15 per share.

This performance represents a continuation of trends observed in Q1 2025, when Avista reported earnings of $0.98 per share, slightly below analyst expectations of $1.00. The deterioration in non-utility segment performance appears to have accelerated in Q2.

Strategic Initiatives & Capital Plan

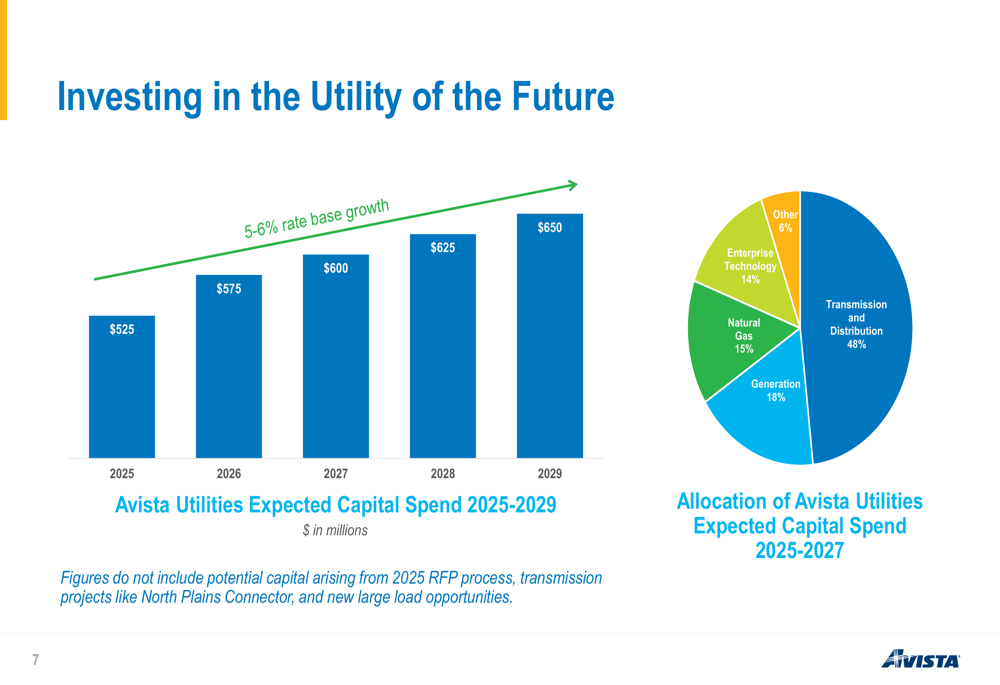

Despite near-term earnings challenges, Avista continues to execute on its long-term strategic plan with significant capital investments planned through 2029. The company outlined its capital expenditure forecast, showing steady increases from $525 million in 2025 to $650 million in 2029:

The capital plan focuses heavily on transmission and distribution infrastructure, which accounts for 48% of planned spending from 2025-2027. Other significant areas include generation (18%), natural gas infrastructure (15%), and enterprise technology (14%). This investment strategy is expected to drive rate base growth of 5-6% over the planning period.

Notably, the company indicated that these figures do not include potential additional capital for projects identified in the 2025 RFP process, transmission projects like the North Plains Connector, or new large load opportunities, suggesting possible upside to the capital plan.

Regulatory Environment

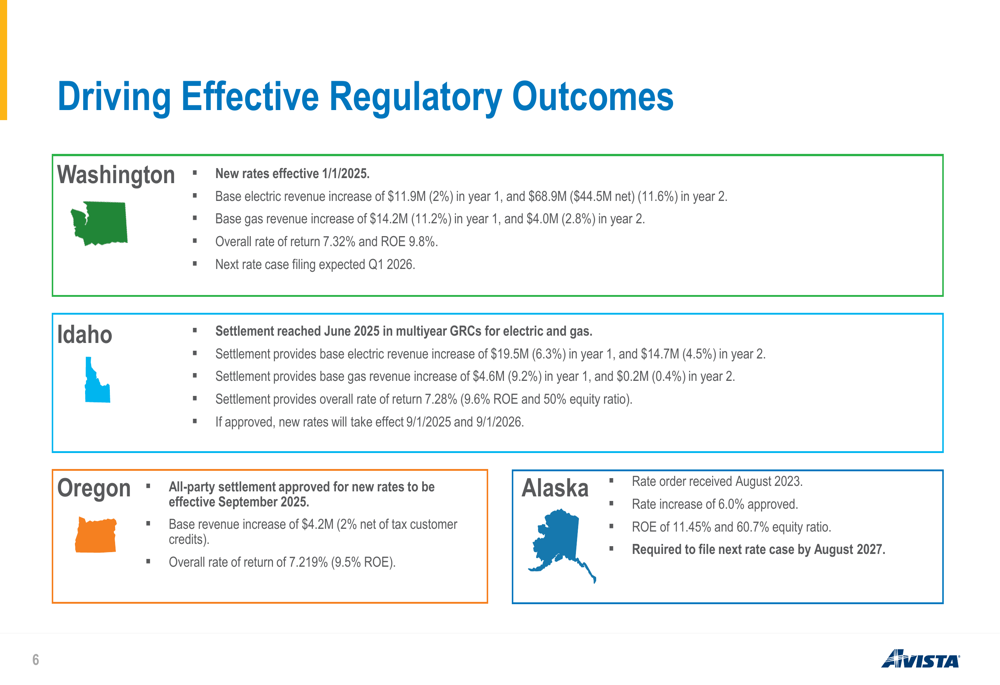

A key strength highlighted in the presentation was Avista’s success in securing favorable regulatory outcomes across its service territories. The company detailed recent developments in Washington, Idaho, Oregon, and Alaska:

In Washington, new rates effective January 1, 2025, will provide a base electric revenue increase of $11.9 million (2%) in year one and $68.9 million (11.6%) in year two. Natural gas revenue will increase by $14.2 million (11.2%) in year one and $4.0 million (2.8%) in year two.

Idaho regulatory developments include a settlement reached in June 2025 that, if approved, will provide base electric revenue increases of $19.5 million (6.3%) in year one and $14.7 million (4.5%) in year two, with new rates taking effect September 1, 2025, and September 1, 2026.

These constructive regulatory outcomes provide a solid foundation for Avista’s financial stability and support for its capital investment program.

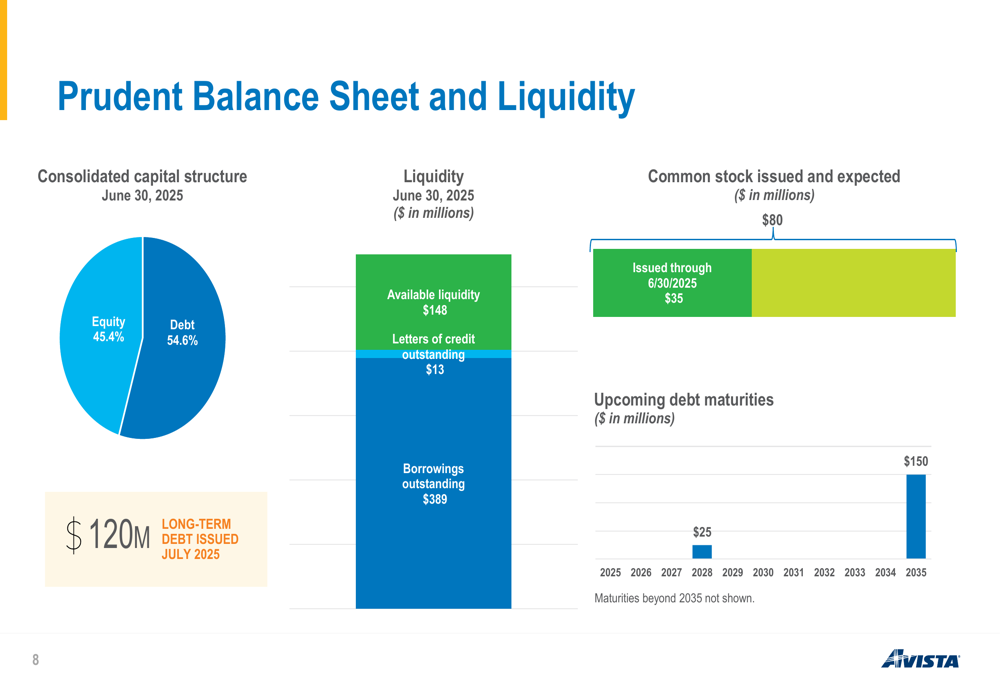

Balance Sheet and Liquidity

The presentation also addressed Avista’s financial position, highlighting a prudent balance sheet and adequate liquidity:

As of June 30, 2025, Avista’s consolidated capital structure consisted of 45.4% equity and 54.6% debt. The company reported available liquidity of $148 million, with $13 million in outstanding letters of credit and $389 million in borrowings outstanding.

The company issued $35 million in common stock through June 30, 2025, with an expectation of $80 million overall. Additionally, Avista issued $120 million in long-term debt in July 2025. Upcoming debt maturities appear manageable, with only $25 million due between 2025 and 2030, followed by $150 million in 2035.

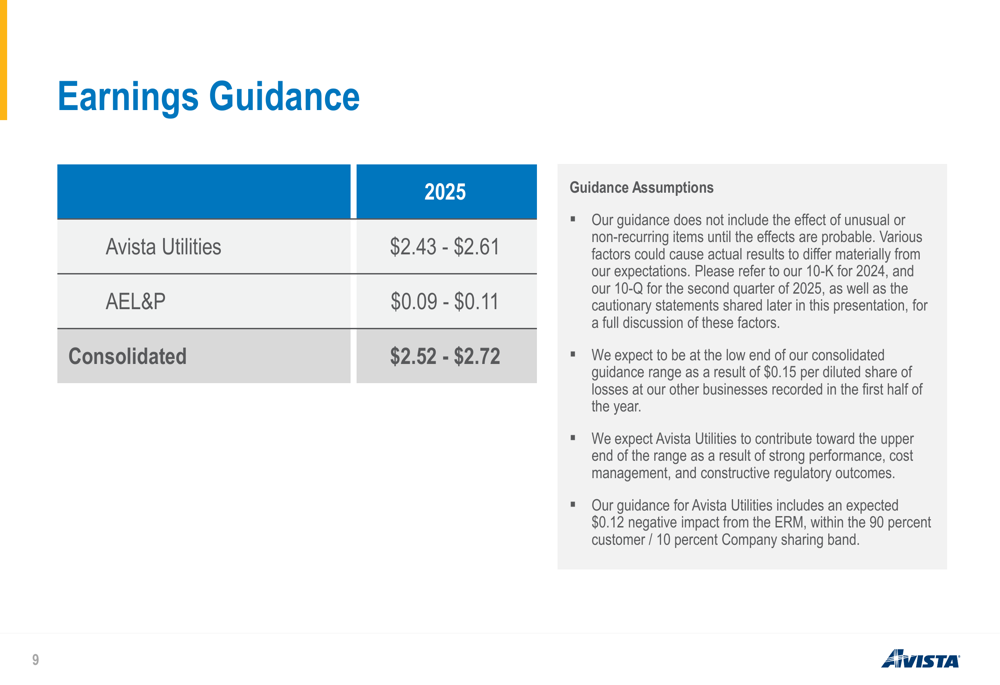

Forward-Looking Statements

Despite the Q2 earnings decline, Avista affirmed its full-year 2025 earnings guidance:

The company maintained its consolidated earnings guidance range of $2.52 to $2.72 per share, though it now expects to be at the low end of this range due to the losses in its non-utility businesses recorded in the first half of the year.

Importantly, Avista Utilities is expected to perform toward the upper end of its guidance range ($2.43 to $2.61 per share), reflecting the strength of the core utility business. The guidance includes an expected $0.12 negative impact from the Energy Recovery (NASDAQ:ERII) Mechanism (ERM).

This guidance is consistent with what the company provided after Q1 2025 results, suggesting that while the non-utility segment has underperformed, the overall financial outlook remains stable thanks to the strong utility operations.

Conclusion

Avista’s Q2 2025 presentation reveals a company navigating through sector-specific challenges while maintaining the strength of its core utility operations. The decline in quarterly earnings primarily reflects difficulties in the clean technology sector rather than fundamental issues with the company’s main business.

With strong regulatory outcomes, a clear capital investment plan, and solid utility performance, Avista appears well-positioned to weather the current headwinds in its non-utility businesses. Investors will likely focus on whether the company can improve the performance of these segments in the second half of the year to achieve its full-year guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.