TSX runs higher on rate cut expectations

Introduction & Market Context

Avita Medical Ltd (NASDAQ:RCEL) presented its second quarter 2025 financial results on August 7, revealing mixed performance with 21% year-over-year revenue growth but a significant reduction in full-year guidance due to reimbursement challenges. The market reacted negatively to the revised outlook, with shares plunging 24.54% to $4.06 in premarket trading following the presentation.

The regenerative medicine company, which specializes in burn and trauma care products, reported progress in its multi-product strategy but acknowledged that temporary Centers for Medicare & Medicaid Services (CMS) reimbursement delays have substantially impacted near-term growth prospects.

Quarterly Performance Highlights

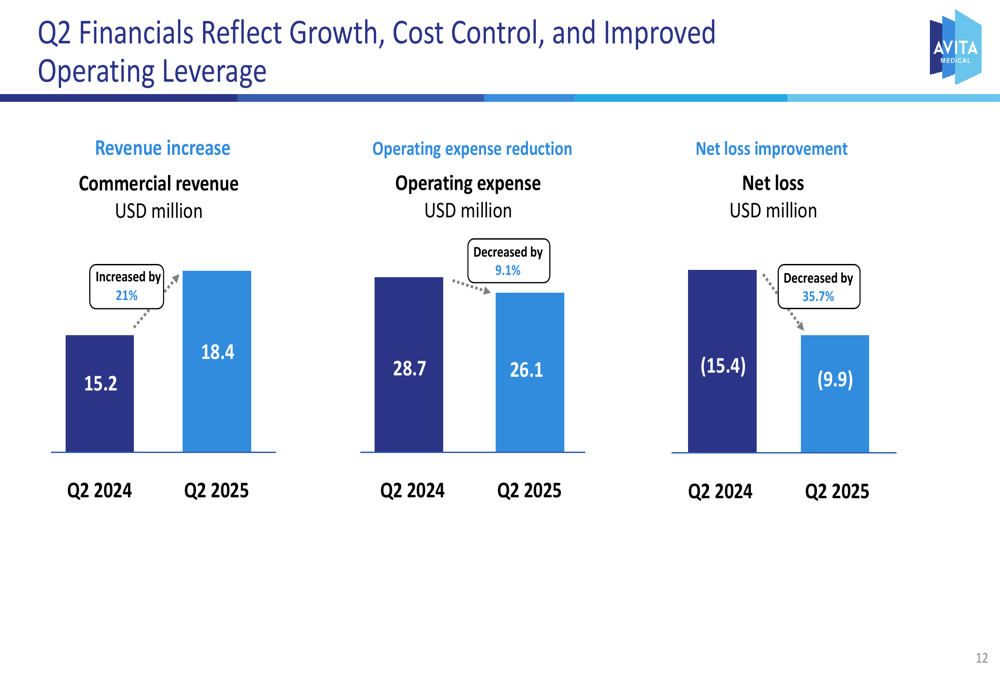

Avita Medical (TASE:BLWV) reported commercial revenue of $18.4 million for Q2 2025, representing a 21% increase compared to Q2 2024. The company also demonstrated improved operational efficiency, reducing operating expenses by 9.1% year-over-year from $28.7 million to $26.1 million.

As shown in the following financial summary:

The company’s net loss improved significantly, decreasing by 35.7% from $15.4 million in Q2 2024 to $9.9 million in Q2 2025. This improvement reflects the company’s focus on cost control while navigating temporary revenue challenges.

Guidance Revision

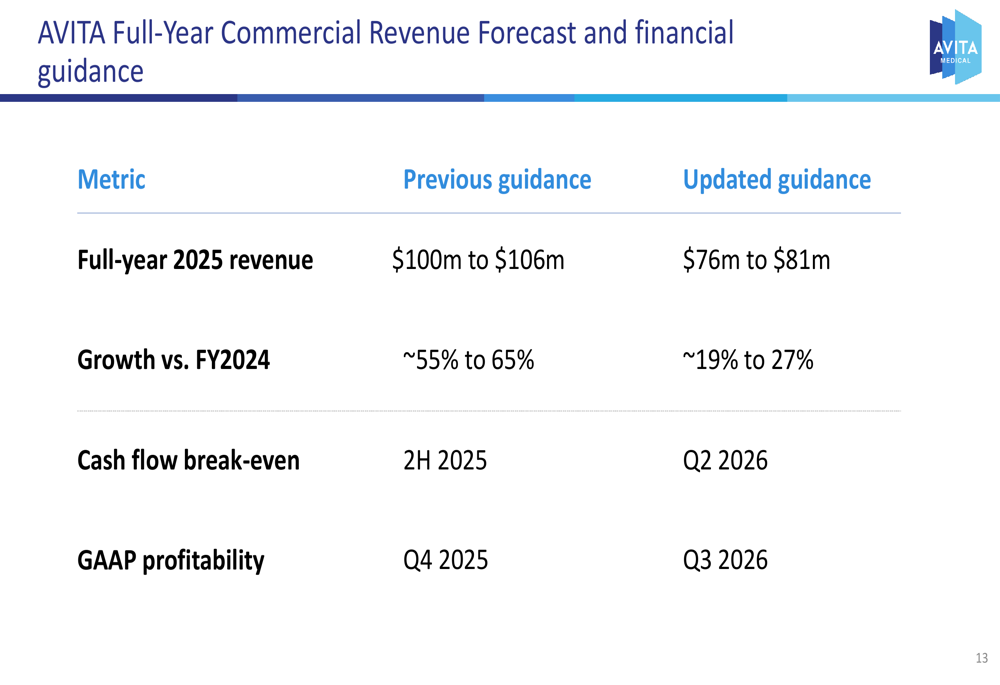

In a significant update, Avita Medical substantially reduced its full-year 2025 revenue guidance from the previously projected $100-106 million to $76-81 million. This revision represents a dramatic shift in growth expectations, with year-over-year growth now projected at 19-27% compared to the previous forecast of 55-65%.

The company has also pushed back its financial milestone targets, as illustrated in this guidance comparison:

Cash flow break-even, previously expected in the second half of 2025, is now anticipated in Q2 2026. Similarly, GAAP profitability has been delayed from Q4 2025 to Q3 2026, representing approximately a 2-3 quarter extension of the company’s path to profitability.

CMS Reimbursement Challenge

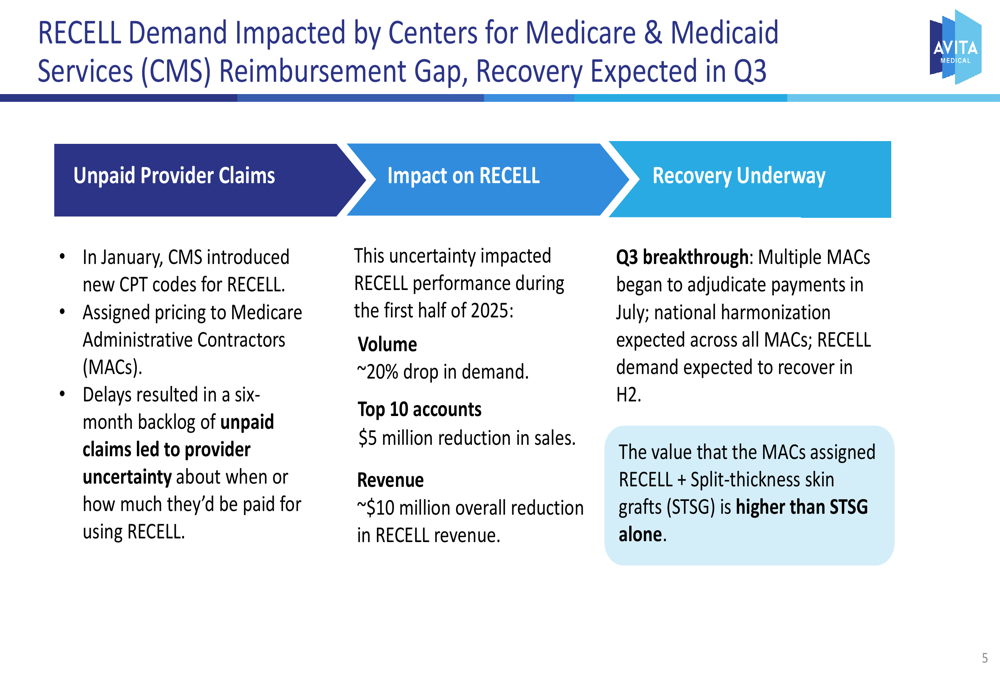

The primary factor behind the guidance reduction is a significant reimbursement issue affecting the company’s flagship RECELL product. In January 2025, CMS introduced new CPT codes for RECELL and assigned pricing responsibilities to Medicare Administrative Contractors (MACs). However, delays in implementation resulted in a six-month backlog of unpaid claims, creating uncertainty among healthcare providers.

The following slide details the impact of this reimbursement gap:

According to the company, this uncertainty led to approximately a 20% drop in RECELL demand, with top accounts reducing purchases by $5 million and an estimated $10 million overall reduction in RECELL revenue. Management indicated that resolution is underway, with multiple MACs beginning to process payments in July, and expects demand to recover in the second half of 2025.

Clinical Data & Product Portfolio

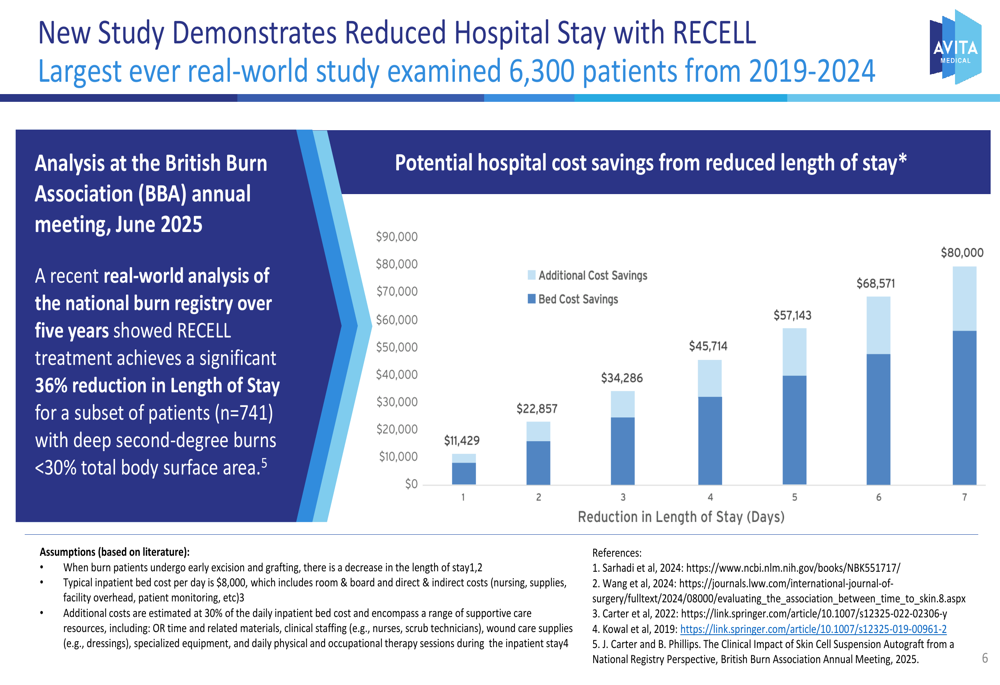

Despite the near-term challenges, Avita highlighted several positive developments in its product portfolio and clinical data. A significant new study presented at the British Burn Association annual meeting in June 2025 demonstrated that RECELL treatment achieves a 36% reduction in hospital length of stay for patients with deep second-degree burns.

The study examined real-world data from over 6,300 patients treated between 2019-2024, with potential cost savings illustrated in this chart:

The company also reported progress with its expanded product portfolio, including its recently launched Cohealyx product, which enables autograft readiness in five days compared to 2-4 weeks with conventional methods. Avita noted that Value Analysis Committee submissions are now active in approximately 25% of U.S. burn centers.

Strategic Initiatives

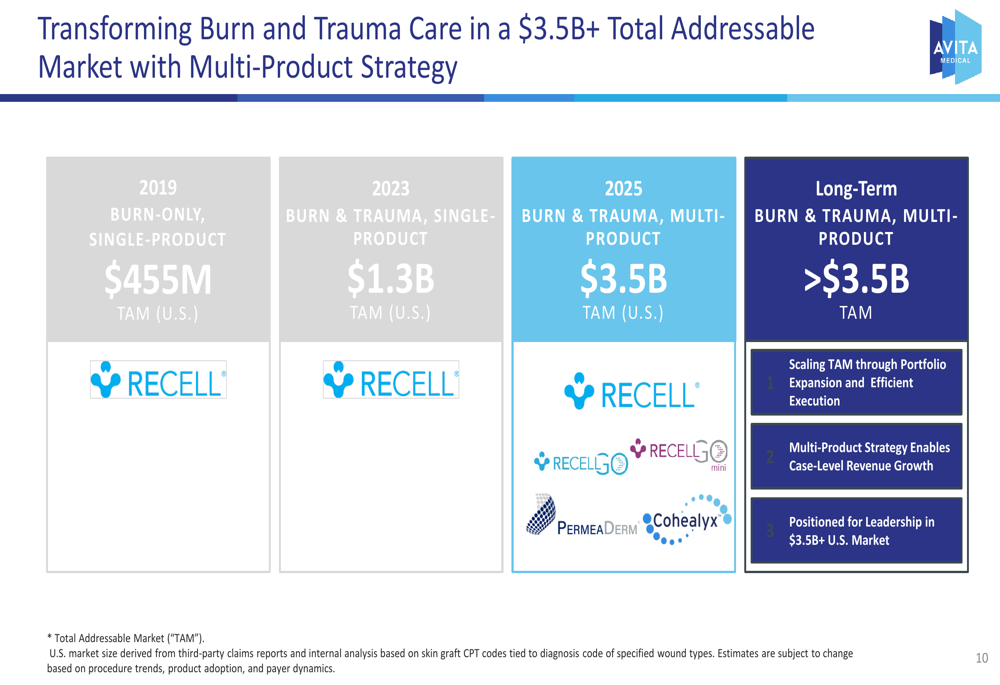

Avita Medical emphasized its transformation from a single-product, burn-focused company to a multi-product platform addressing a significantly larger market opportunity. The company’s presentation illustrated this expansion:

The company has grown its total addressable market from $455 million in 2019 to over $3.5 billion in 2025 through product and indication expansion. Key developments include RECELL’s expansion into trauma wounds, with CMS approving New Technology Add-on Payment (NTAP) for this indication, and international expansion with CE Mark approval expected in Q4 2025.

Additionally, Avita secured a strategic amendment to its OrbiMed agreement, revising trailing 12-month covenants to align with the updated growth outlook and provide financial flexibility.

Forward-Looking Statements

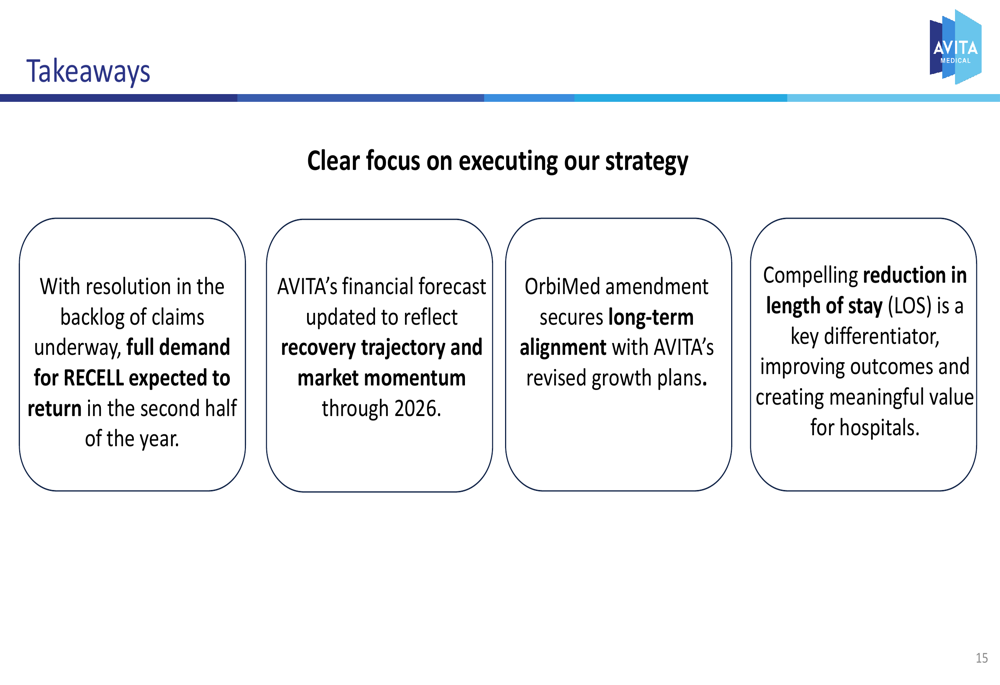

Management expressed confidence that the CMS reimbursement issues are transitory, with CEO Jim Corbett stating, "With resolution in the backlog of claims underway, full demand for RECELL expected to return in the second half of the year." The company highlighted several key takeaways that frame its recovery strategy:

The company’s portfolio developments across multiple products suggest potential for renewed growth once the reimbursement challenges are fully resolved. Management emphasized that the value assigned by MACs for RECELL plus split-thickness skin grafts is higher than skin grafts alone, which they believe will support adoption once the payment process is normalized.

While Avita has revised its near-term financial targets, the company maintains its long-term vision of establishing leadership in the $3.5 billion+ burn and trauma care market through its expanded multi-product strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.