Palantir shares slip by 7% despite posting record revenue in third quarter

Introduction & Market Context

Avolta AG (SIX:AVOL) shares gained nearly 2% following the release of its nine-month 2025 trading update on October 30, as the global travel retailer reported solid organic growth and margin expansion despite regional variations in performance.

The company’s stock closed at CHF 41.68, up 1.97% for the day, sitting comfortably within its 52-week range of CHF 27.50 to CHF 47.30, reflecting positive investor sentiment toward the company’s operational performance and strategic initiatives.

Avolta’s presentation highlighted its ability to maintain growth momentum while expanding margins and generating record cash flow, even as regional performance showed significant variations, with Europe leading growth while North America displayed early signs of recovery.

Quarterly Performance Highlights

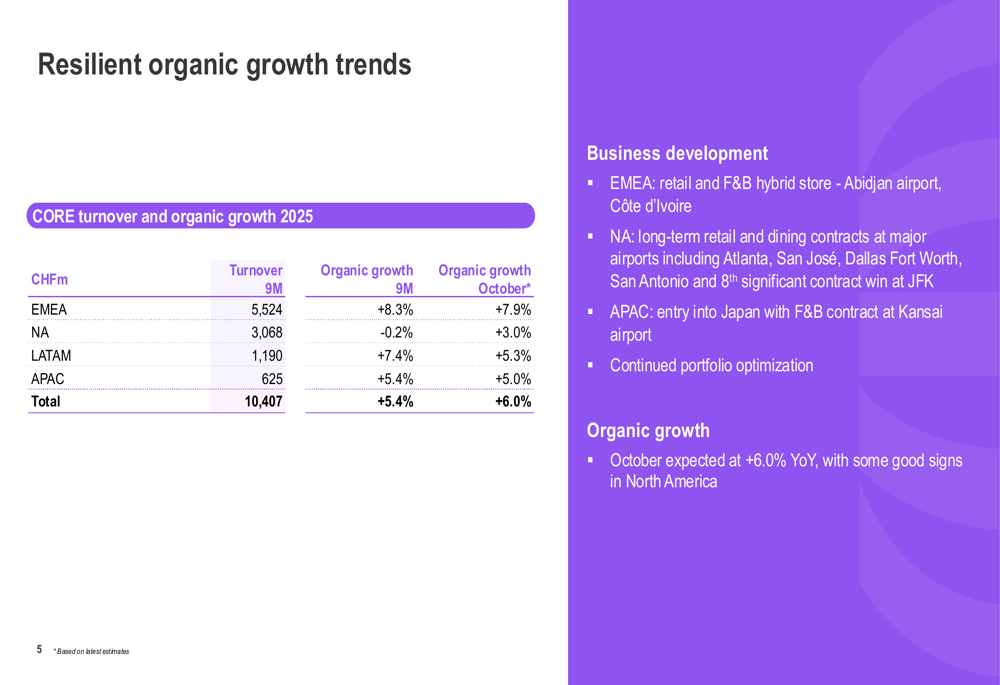

Avolta reported a total turnover of CHF 10,609 million for the first nine months of 2025, with core turnover reaching CHF 10,407 million. The company achieved core revenue growth of 5.8% at constant exchange rates, with organic growth of 5.4% year-over-year.

As shown in the following summary of key financial metrics:

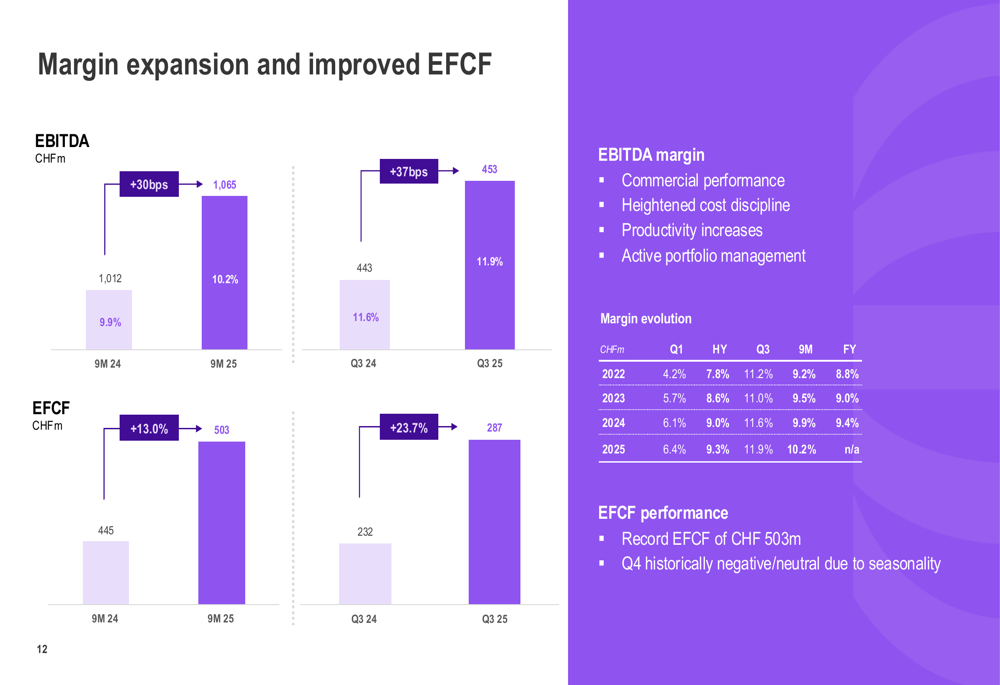

Core EBITDA increased by 5.3% year-over-year to CHF 1,065 million, with the EBITDA margin expanding by 30 basis points to 10.2%. This improvement was primarily driven by cost discipline and productivity enhancements. The company also reported record equity free cash flow (EFCF) of CHF 503 million, representing a 13.0% increase compared to the same period last year.

Regional performance varied significantly across Avolta’s global operations. EMEA (Europe, Middle East, and Africa) led growth with an impressive 8.3% organic increase, while North America remained essentially flat at -0.2%. However, the company noted encouraging signs in October with North American organic growth estimated at 3.0%.

The following table illustrates the regional breakdown of turnover and growth rates:

Detailed Financial Analysis

Avolta’s financial performance showed consistent improvement across key metrics. The company’s EBITDA margin continued its upward trajectory, reaching 10.2% for the nine-month period compared to 9.9% in 2024 and 9.5% in 2023 for the same period.

The margin expansion was attributed to commercial performance improvements, heightened cost discipline, productivity increases, and active portfolio management. This trend is clearly illustrated in the following chart showing margin evolution:

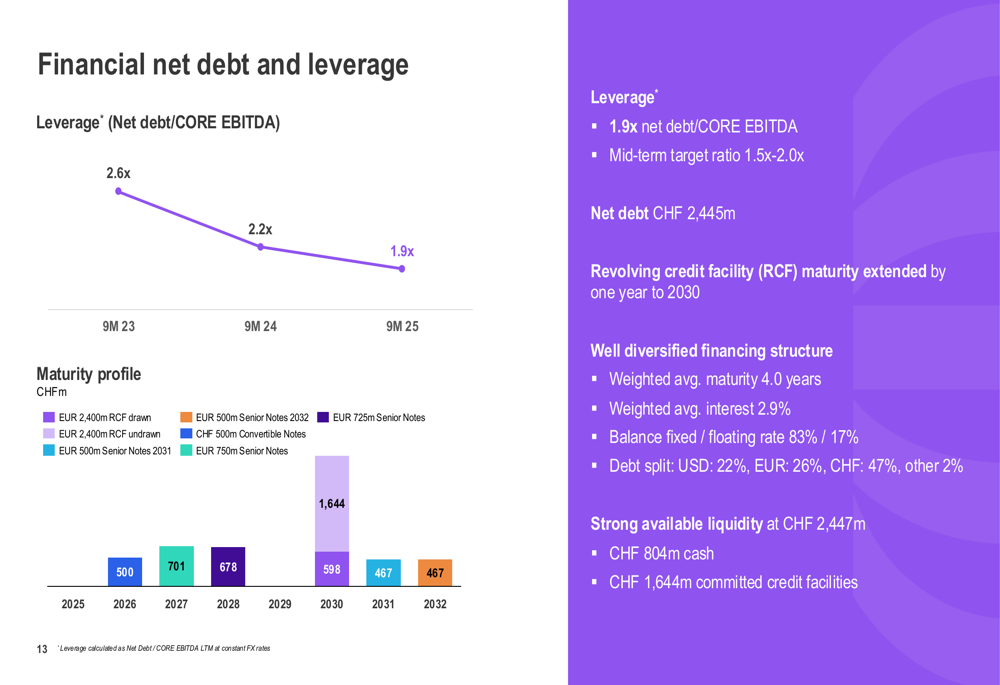

The company generated a record EFCF of CHF 503 million, representing a 13.0% increase year-over-year and a conversion rate of 47.3%. This strong cash flow generation allowed Avolta to reduce its leverage ratio to 1.9x net debt to CORE EBITDA, down from 2.2x in September 2024.

The following chart illustrates Avolta’s financial net debt and leverage position:

The company has maintained a well-diversified financing structure with a weighted average maturity of 4.0 years and a weighted average interest rate of 2.9%. Avolta also reported strong available liquidity of CHF 2,447 million, including CHF 804 million in cash and CHF 1,644 million in committed credit facilities.

Strategic Initiatives

Avolta continues to focus on strategic growth initiatives, including new concession wins and digital transformation. The company secured several long-term retail and dining contracts at major airports including Atlanta, San José, Dallas Fort Worth, San Antonio, and its eighth significant contract win at JFK. Additionally, Avolta entered the Japanese market with a food and beverage contract at Kansai airport.

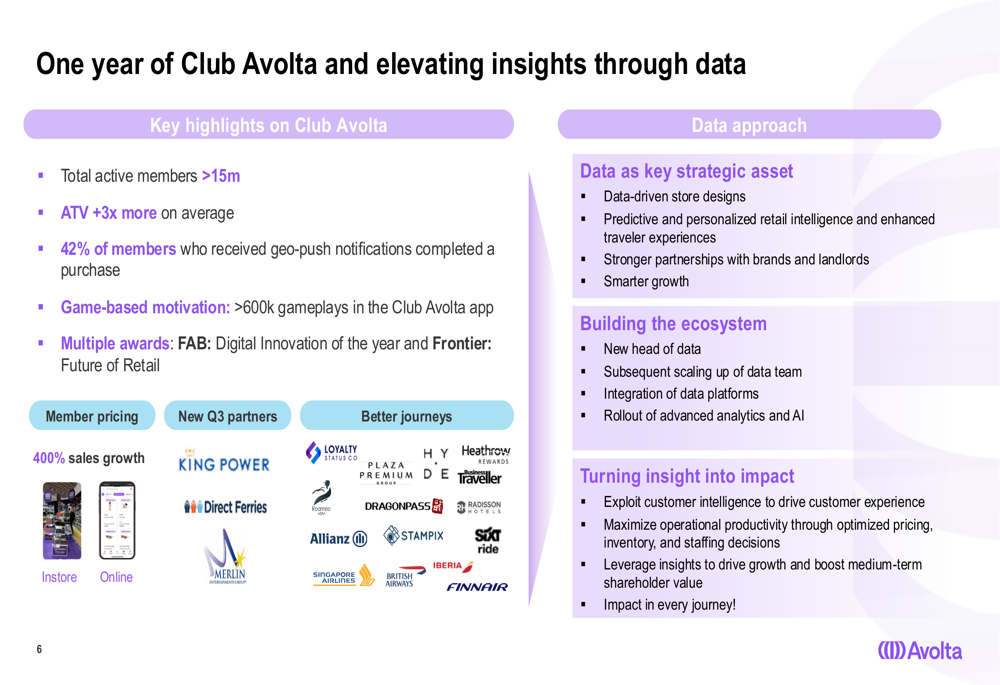

A key strategic focus has been the development of Club Avolta, the company’s loyalty program, which has reached over 15 million active members. The program has shown impressive results, with average transaction values three times higher among members compared to non-members.

The following slide highlights the success of Club Avolta and the company’s data-driven approach:

Avolta is leveraging data as a strategic asset to drive customer experience, maximize operational productivity, and boost medium-term shareholder value. The company has appointed a new head of data and is scaling up its data team to enhance analytics capabilities and artificial intelligence integration.

Forward-Looking Statements

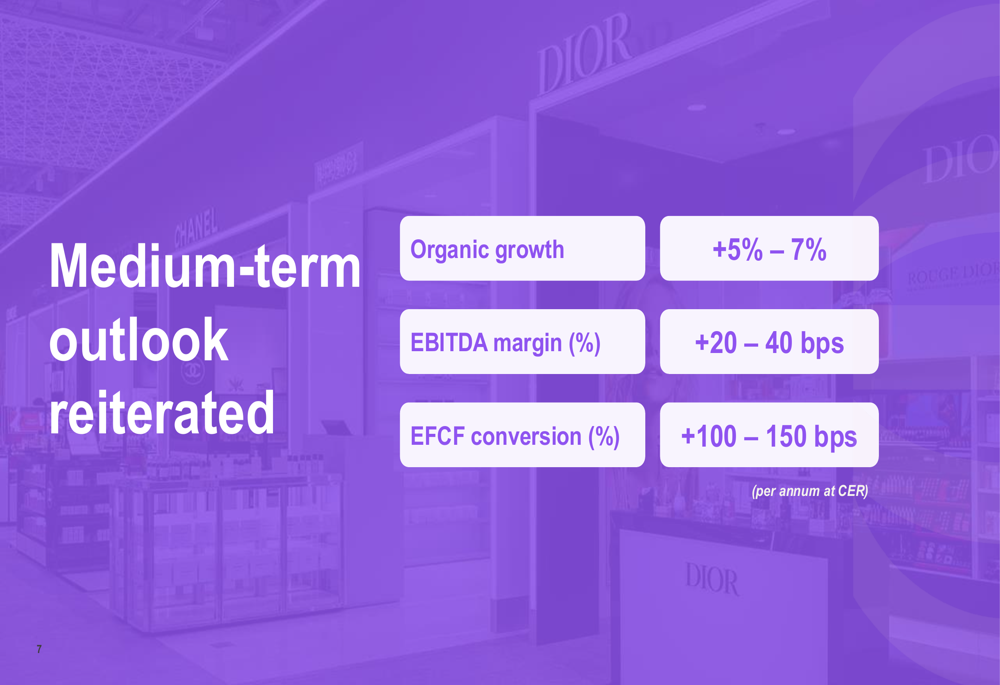

Avolta reiterated its medium-term outlook, targeting organic growth of 5-7%, annual EBITDA margin expansion of 20-40 basis points, and EFCF conversion improvement of 100-150 basis points per annum at constant exchange rates.

The following slide summarizes Avolta’s medium-term targets:

For the full year 2025, the company expressed confidence based on October’s estimated organic growth of 6.0%, which reflects an encouraging inflection in North America. Avolta also confirmed its capital allocation policy, which prioritizes investment in growth, maintaining balance sheet efficiency with a target leverage ratio of 1.5x-2.0x, and returning capital to shareholders through progressive dividends and share buybacks.

The company has already repurchased 3.2 million shares totaling CHF 129 million through the end of September under its CHF 200 million buyback program, demonstrating its commitment to shareholder returns while maintaining financial flexibility for growth investments.

As summarized in the conclusion slide, Avolta continues to deliver on all key performance indicators while creating shareholder value through deleveraging and share repurchases:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.