TSX runs higher on rate cut expectations

Introduction & Market Context

A&W Food Services of Canada Inc. (TSX:AW) presented its Q2 2025 results on July 24, 2025, highlighting improved performance with system sales growth of 3.4% and same-store sales growth of 1.6%. The company, which became publicly traded on the Toronto Stock Exchange in October 2024, continues to maintain its position as Canada’s second-largest burger chain in a competitive quick-service restaurant (QSR) market.

The Canadian QSR market represents a $42.9 billion opportunity with approximately 5.8% year-over-year growth, while the burger segment specifically accounts for $13.0 billion with 2.6% year-over-year growth. A&W’s trailing four-quarter system sales reached $1.89 billion through Q2 2025, demonstrating the company’s significant market presence.

Quarterly Performance Highlights

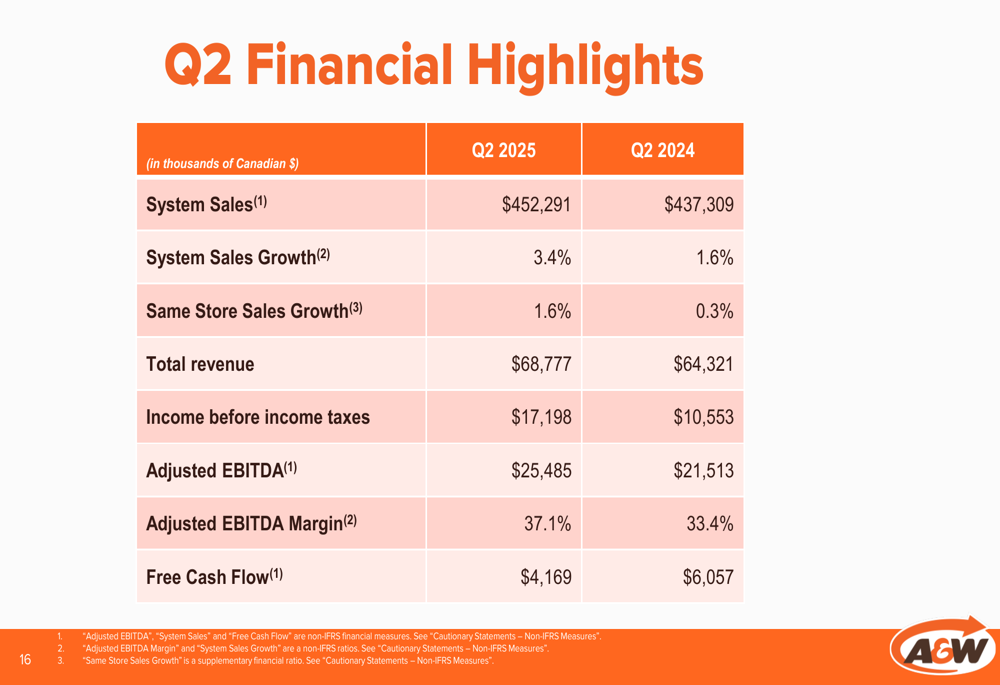

A&W reported solid financial results for Q2 2025, showing improvements across key metrics compared to the same period last year. System sales increased to $452,291 in Q2 2025, up 3.4% from $437,309 in Q2 2024. Same-store sales growth accelerated to 1.6% in Q2 2025 compared to just 0.3% in Q2 2024.

As shown in the following quarterly financial highlights:

Total (EPA:TTEF) revenue reached $68,777 in Q2 2025, up from $64,321 in Q2 2024. Income before income taxes saw a significant jump to $17,198 in Q2 2025 from $10,553 in Q2 2024. Notably, adjusted EBITDA increased to $25,485 in Q2 2025 from $21,513 in Q2 2024, with adjusted EBITDA margin expanding to 37.1% from 33.4% in the prior year period.

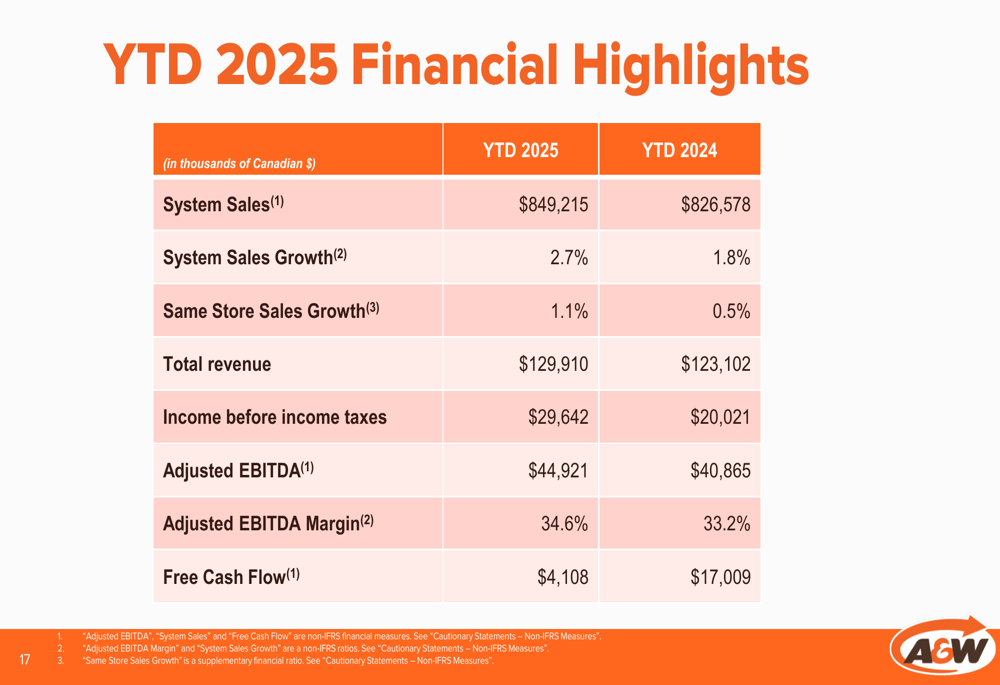

For the first half of 2025, A&W’s year-to-date performance also showed positive momentum:

System sales for YTD 2025 reached $849,215, representing a 2.7% increase from $826,578 in YTD 2024. Same-store sales growth for the first half of 2025 was 1.1%, compared to 0.5% in the same period of 2024. However, free cash flow declined to $4,108 in YTD 2025 from $17,009 in YTD 2024.

Competitive Industry Position

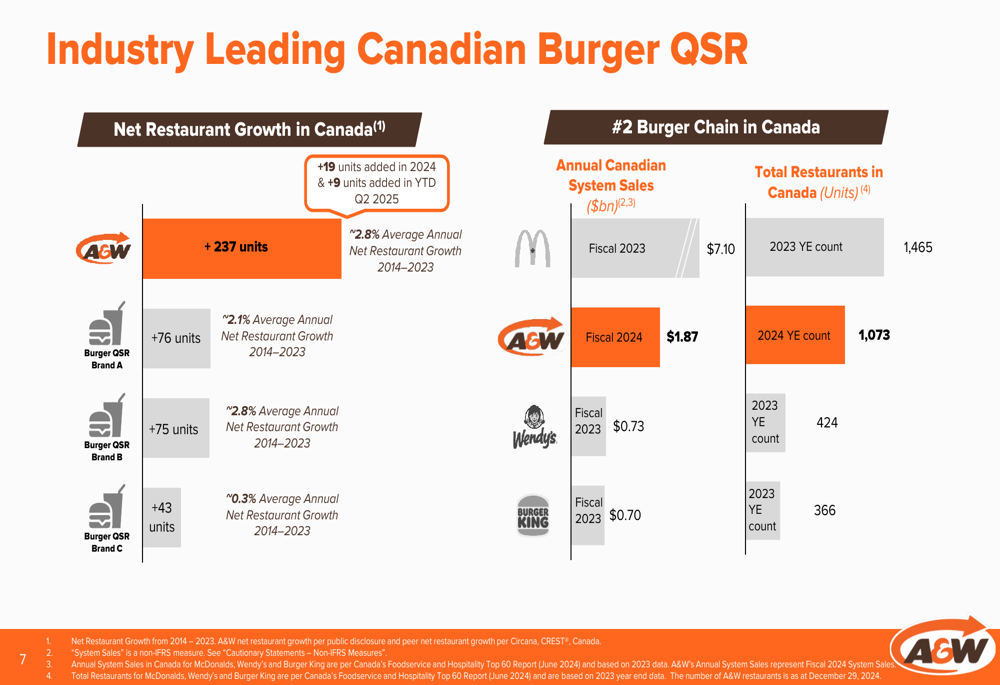

A&W has established itself as a formidable competitor in the Canadian burger QSR market, maintaining the #2 position behind McDonald’s (NYSE:MCD). The company has demonstrated superior growth compared to its main competitors over the past decade.

The following chart illustrates A&W’s industry-leading position in the Canadian burger QSR market:

A&W added 19 new units in 2024 and 9 units in YTD Q2 2025, bringing its total to 1,082 franchised locations, 10 corporate restaurants, and one Pret A Manger location. This represents a net addition of 237 units from 2014 to 2024, reflecting an average annual net restaurant growth of 2.1% during this period.

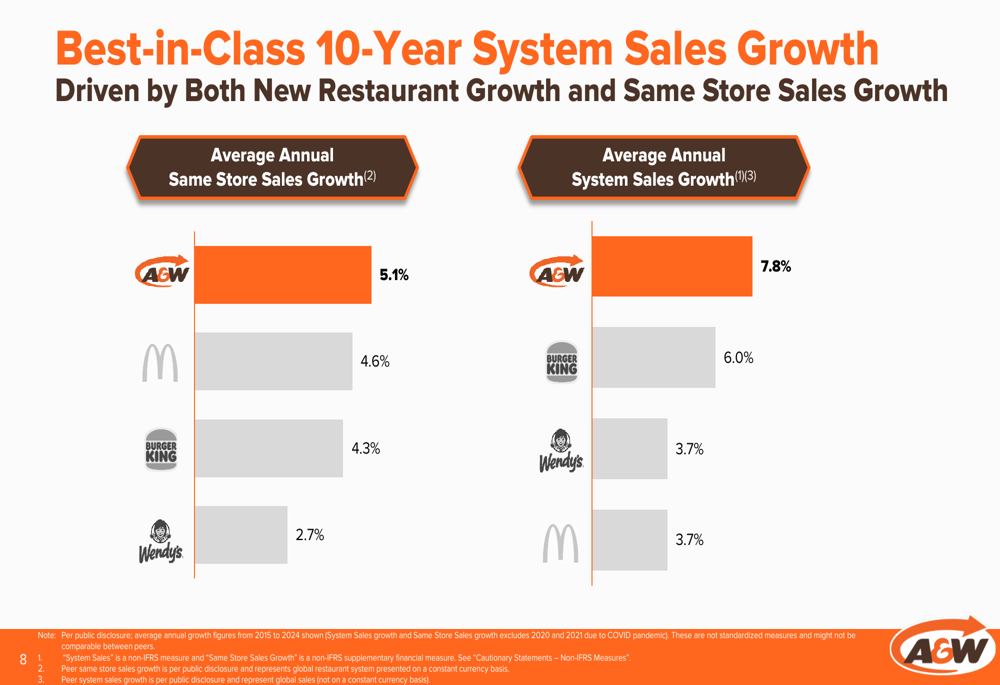

A&W’s growth metrics outperform major competitors in the Canadian market as shown in this comparative analysis:

From 2015 to 2024, A&W achieved an average annual system sales growth of 7.8% and same-store sales growth of 5.1%, surpassing McDonald’s, Burger King, and Wendy’s (NASDAQ:WEN) in these key metrics.

Strategic Initiatives

A&W outlined several strategic initiatives aimed at driving continued growth and enhancing profitability. The company is pursuing a two-pronged approach focused on new restaurant growth and same-store sales growth.

The growth strategy is illustrated in the following slide:

For new restaurant growth, A&W is leveraging its partnership with Petro-Canada (Suncor) and expanding its Pret A Manger concept. The company also launched A&W Rewards on April 22, 2025, to enhance customer loyalty and drive same-store sales growth.

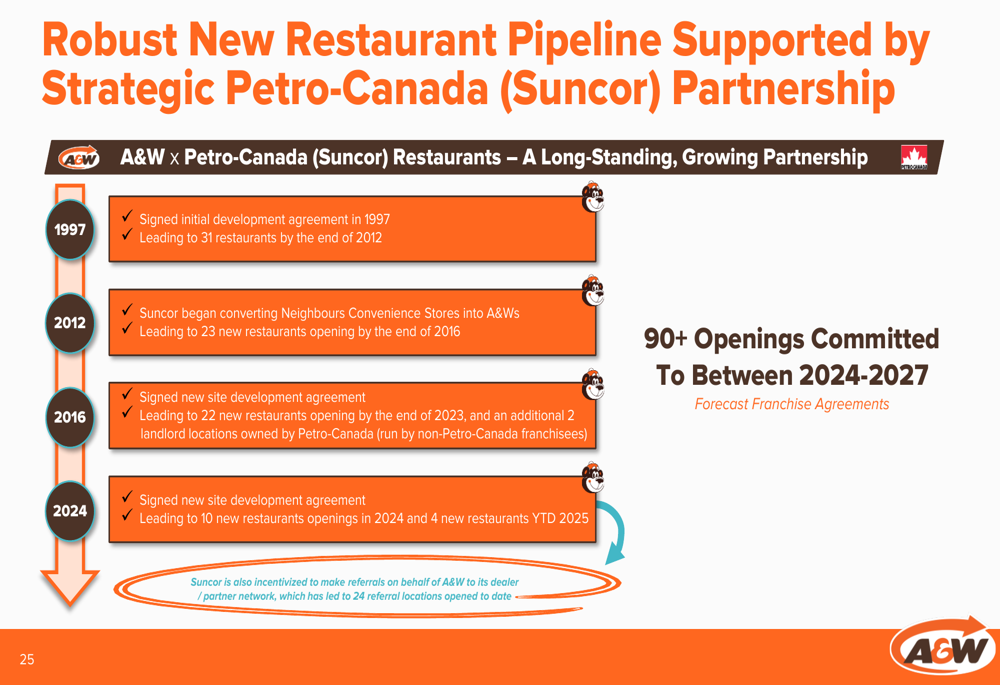

A&W’s partnership with Petro-Canada has been a significant driver of expansion:

This strategic relationship has evolved since 1997 and is expected to yield 90+ new restaurant openings between 2024-2027, with 10 new locations already opened in 2024 and 4 in YTD 2025.

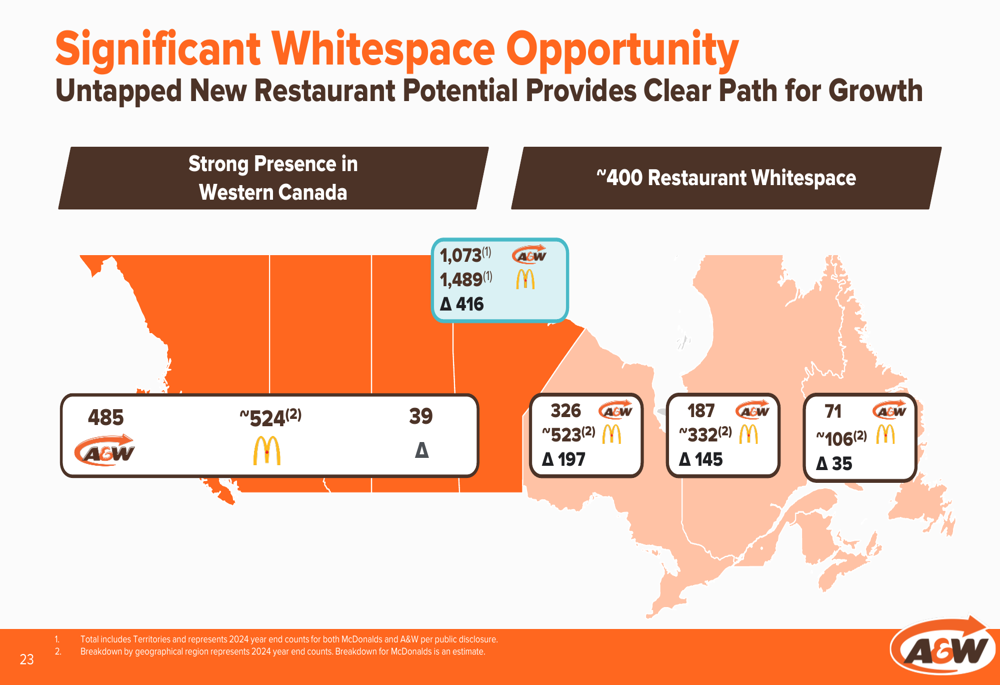

The company has identified substantial growth potential across Canada, particularly in Ontario and Quebec:

Compared to McDonald’s, A&W has 416 fewer locations across Canada, with the largest gaps in Ontario (197 fewer) and Quebec (145 fewer), representing significant whitespace opportunity for expansion.

Forward-Looking Statements

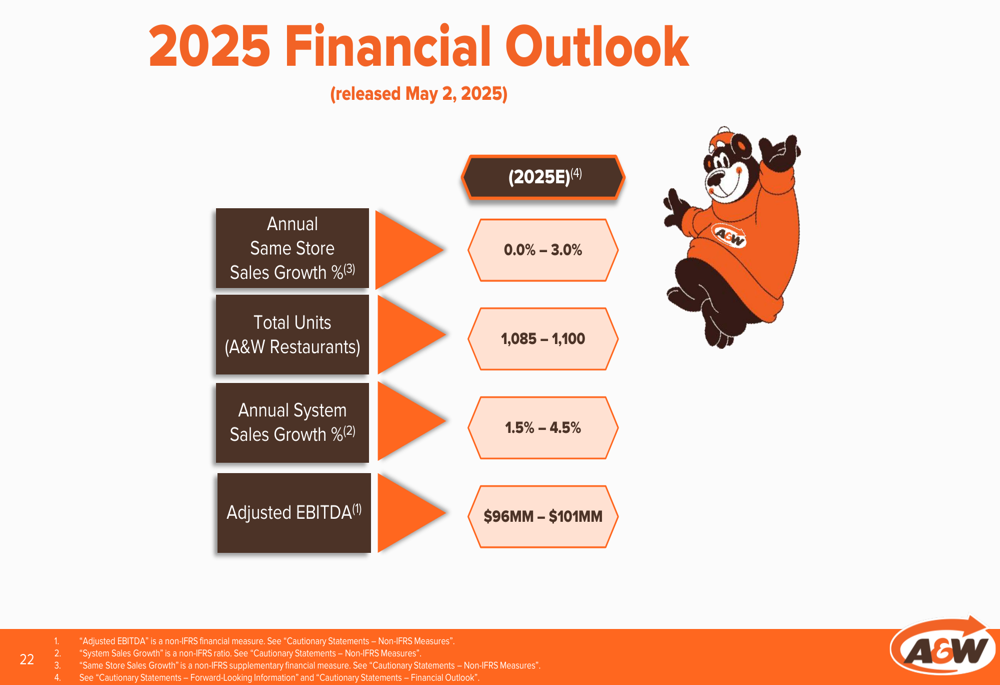

A&W provided a positive outlook for 2025, projecting continued growth across key metrics:

The company expects annual same-store sales growth of 0.0% to 3.0%, with total A&W restaurant units reaching 1,085 to 1,100 by year-end. Annual system sales growth is projected at 1.5% to 4.5%, with adjusted EBITDA forecasted between $96 million and $101 million.

Beyond 2025, A&W is targeting a 30% improvement in restaurant-level profitability for franchisees from 2023 to 2028, with 5% already achieved in 2024. The company is also working to reduce the cost of new freestanding restaurants by $500,000 through redesign, with the first such location to be built in 2025.

Capital Allocation Strategy

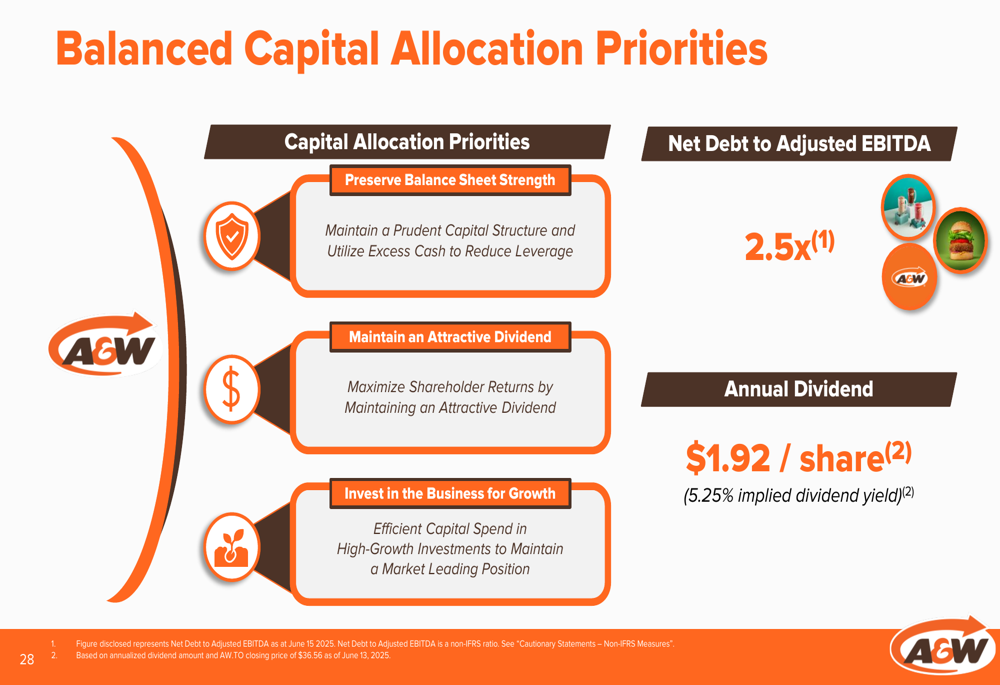

A&W outlined a balanced approach to capital allocation, focusing on three key priorities:

The company aims to maintain balance sheet strength with a prudent capital structure, currently reporting a net debt to adjusted EBITDA ratio of 2.5x. A&W is committed to providing an attractive dividend, currently set at $1.92 per share annually, representing an implied dividend yield of 5.25%. Additionally, the company plans to invest in high-growth opportunities to maintain its market-leading position.

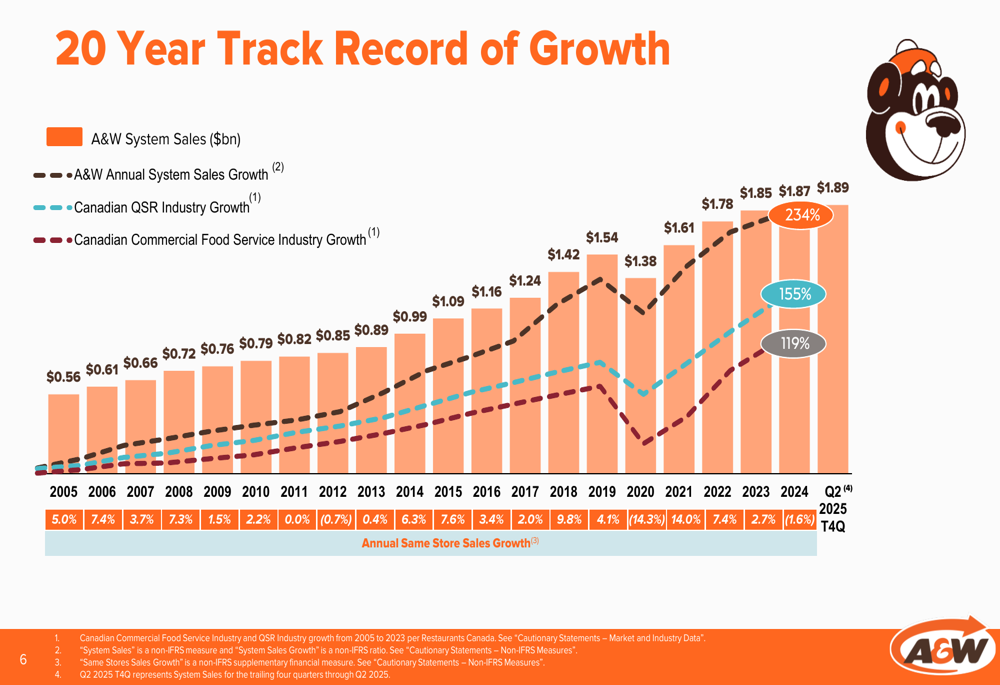

A&W’s 20-year track record of growth demonstrates the effectiveness of its long-term strategy:

System sales have grown from $0.56 billion in 2005 to $1.89 billion in Q2 2025, positioning A&W for continued success in the competitive Canadian QSR market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.