Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Axalta Coating Systems Ltd (NYSE:AXTA) reported its third quarter 2025 financial results on October 28, showcasing resilience amid challenging market conditions. The coatings manufacturer delivered record adjusted EBITDA and EPS figures despite a slight revenue decline, as the company continues to navigate macroeconomic headwinds in North America. Following the earnings announcement, Axalta’s stock rose 4.68% in pre-market trading to $30.42, reflecting positive investor sentiment.

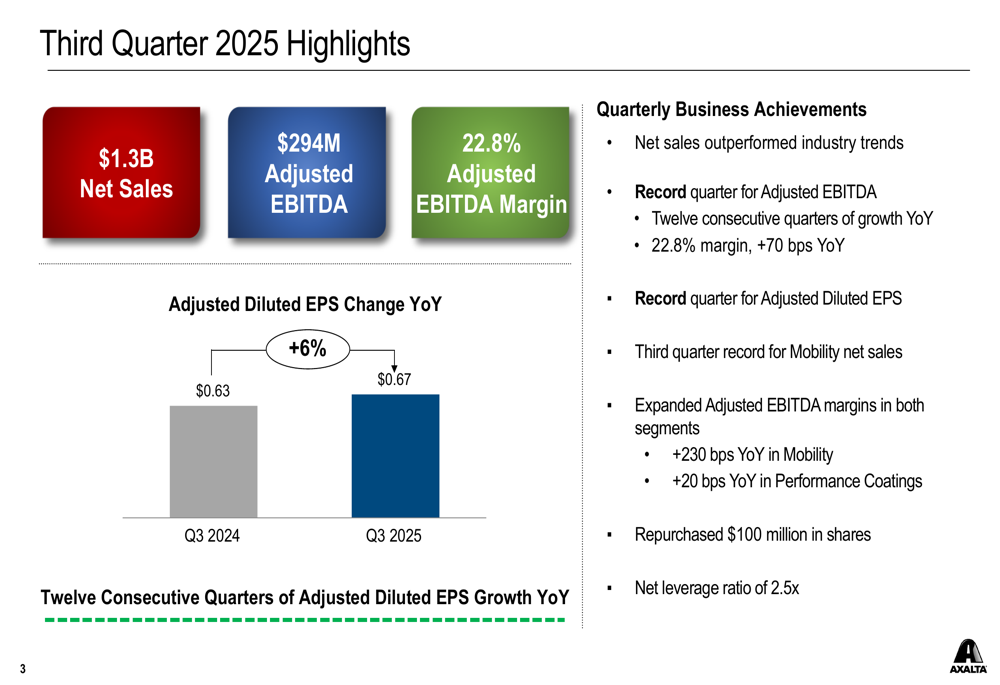

The company’s presentation highlighted its ability to maintain profitability through operational efficiency and strategic cost management, even as volume pressures persisted in certain segments. This performance comes as Axalta marks its twelfth consecutive quarter of year-over-year adjusted diluted EPS growth.

Quarterly Performance Highlights

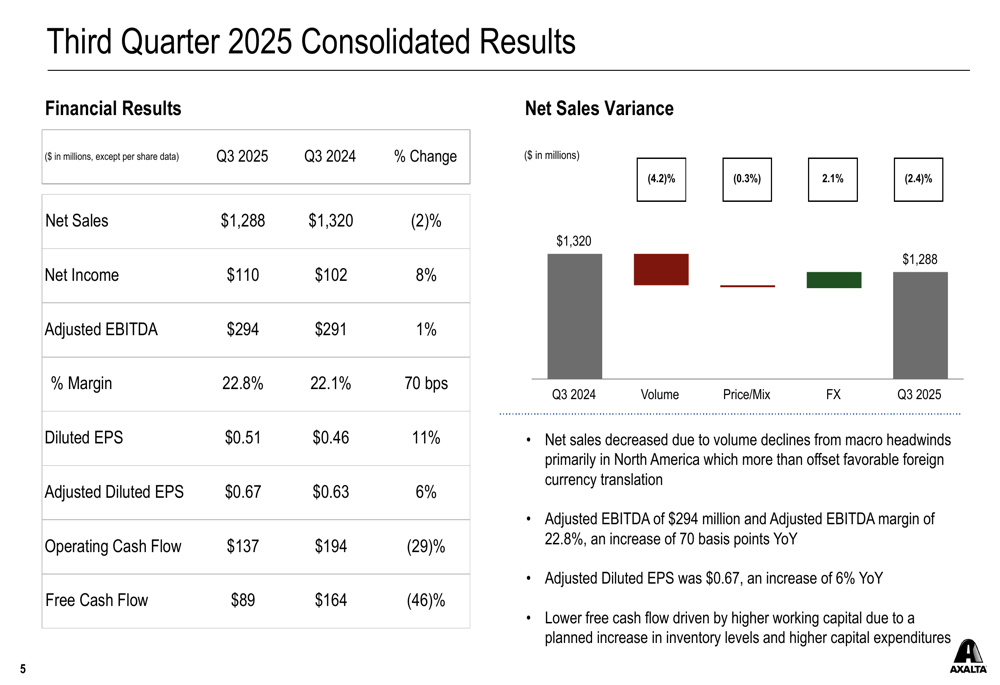

Axalta reported net sales of $1.3 billion for Q3 2025, representing a 2% year-over-year decrease. Despite this top-line challenge, the company achieved record adjusted EBITDA of $294 million, a 1% increase from the prior year, while expanding its adjusted EBITDA margin by 70 basis points to 22.8%.

As shown in the following quarterly highlights:

Adjusted diluted EPS reached $0.67, up 6% from $0.63 in the same quarter last year, exceeding analyst expectations of $0.64. Net income increased 8% to $110 million, while diluted EPS rose 11% to $0.51.

The company’s consolidated results demonstrate how Axalta managed to improve profitability metrics despite volume challenges:

The net sales decrease of 2.4% was primarily driven by volume declines (-4.2%) due to macro headwinds in North America, partially offset by favorable foreign currency translation. Free cash flow decreased to $89 million from $164 million in Q3 2024, primarily due to planned inventory increases and higher capital expenditures.

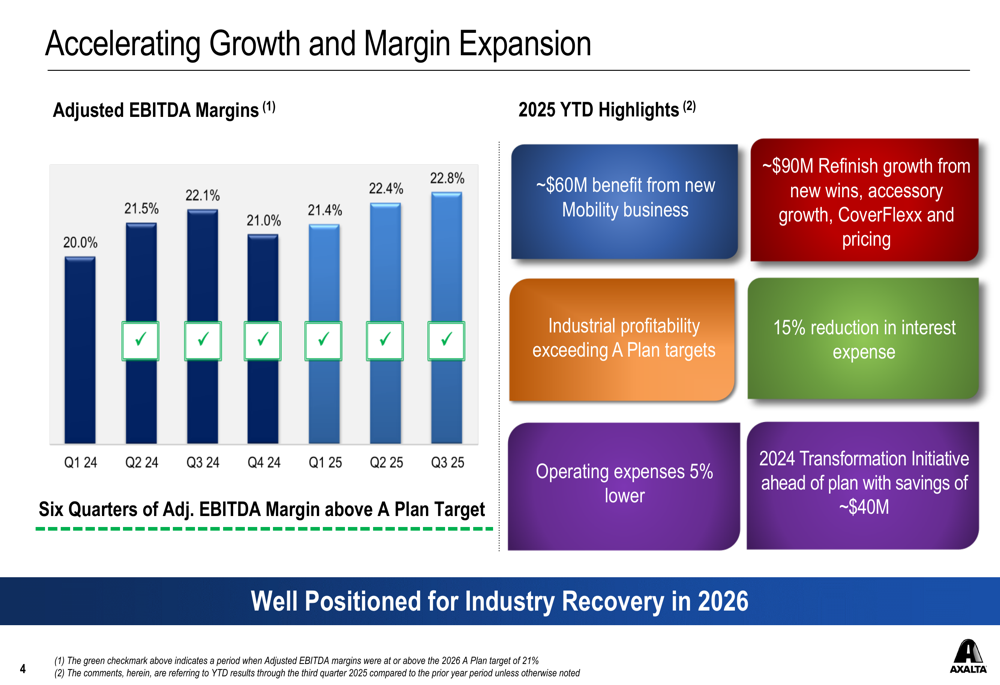

Axalta’s adjusted EBITDA margins have shown consistent improvement over the past seven quarters, exceeding the company’s 2026 targets ahead of schedule:

The margin expansion has been supported by approximately $60 million in benefits from new Mobility business, Industrial profitability exceeding targets, 5% lower operating expenses, and approximately $90 million in Refinish growth from new wins, accessory growth, and pricing initiatives.

Segment Analysis

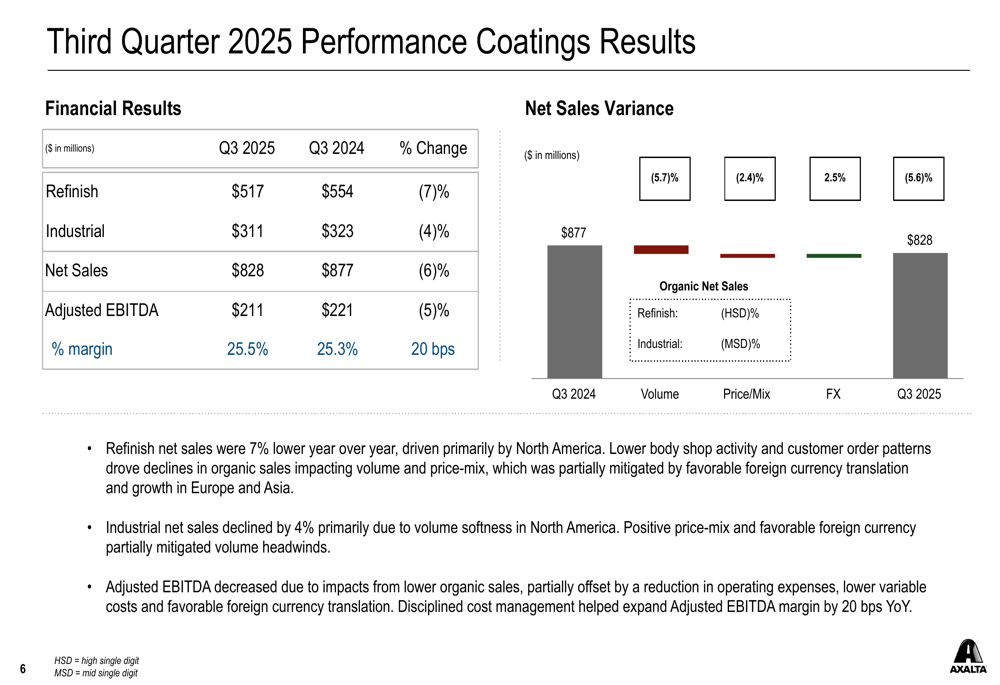

Axalta’s performance showed divergent trends across its two main segments. The Performance Coatings segment, which includes Refinish and Industrial businesses, reported net sales of $828 million, down 6% year-over-year. Adjusted EBITDA for this segment decreased 5% to $211 million, though margin improved slightly to 25.5%.

The decline in Performance Coatings was primarily driven by lower volumes in both Refinish and Industrial businesses, with North American destocking trends continuing to impact results.

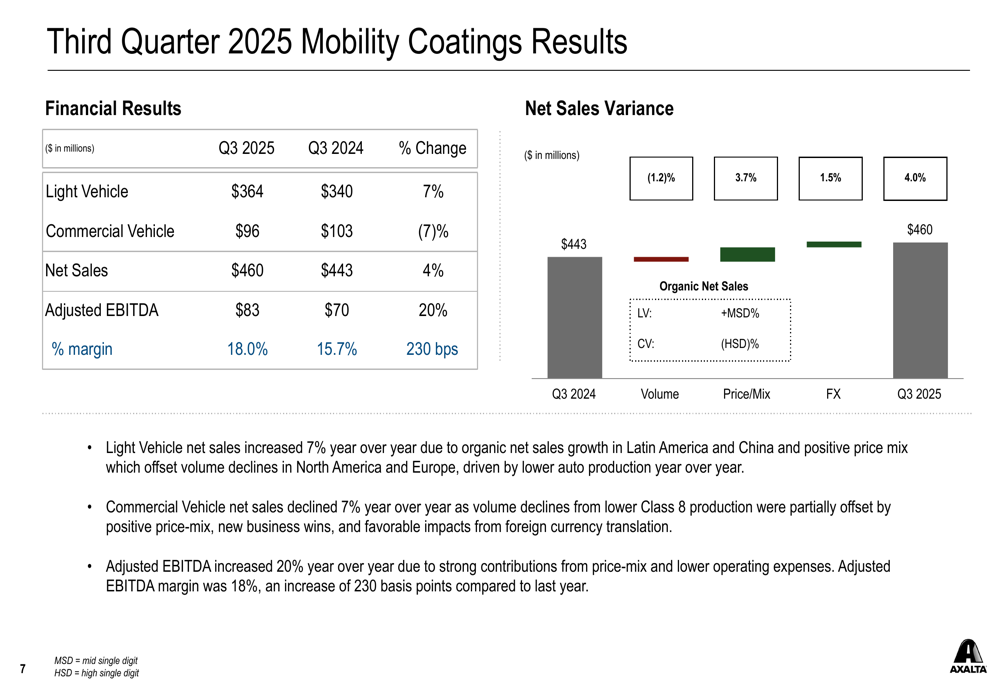

In contrast, the Mobility Coatings segment delivered strong results, with net sales increasing 4% to $460 million and adjusted EBITDA surging 20% to $83 million. The segment’s adjusted EBITDA margin expanded by 230 basis points to 18.0%.

The Light Vehicle subsegment was particularly strong, with net sales up 7% to $364 million, driven by favorable price-mix and new business wins. This growth helped offset a 7% decline in Commercial Vehicle sales, which were impacted by lower global production.

Capital Allocation Strategy

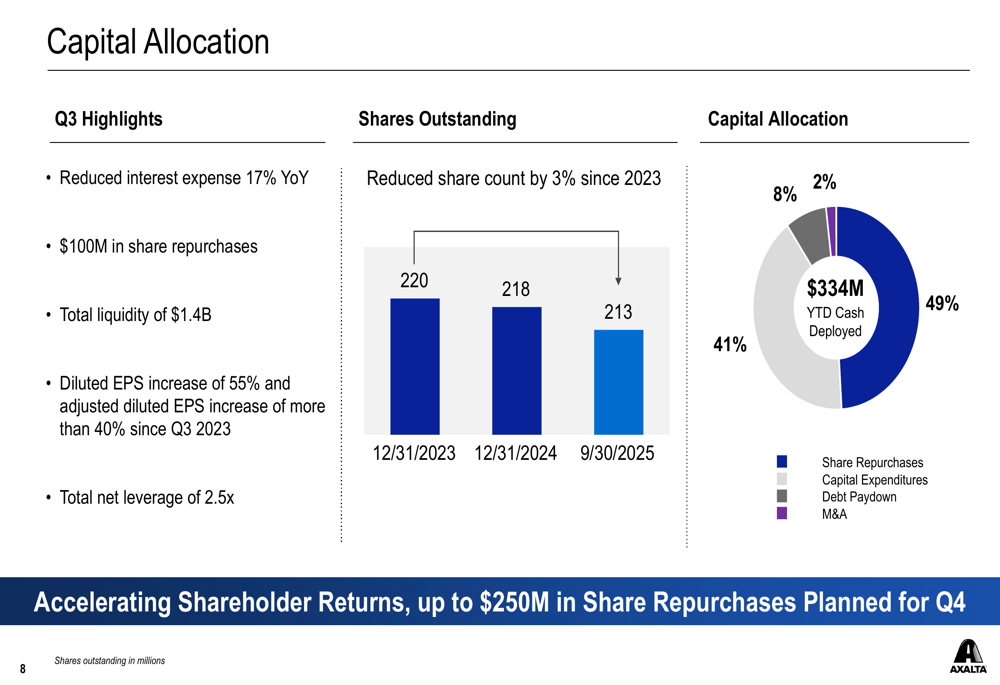

Axalta has maintained an aggressive capital allocation strategy, with a particular focus on share repurchases. During Q3 2025, the company repurchased $100 million in shares and announced plans for up to $250 million in additional share repurchases in Q4.

The company’s capital deployment strategy is illustrated in the following breakdown:

Since the end of 2023, Axalta has reduced its share count by 3%, from 220 million to 213 million shares outstanding. Year-to-date, the company has deployed $334 million in cash, with nearly half (49%) allocated to share repurchases, 41% to capital expenditures, 8% to debt reduction, and 2% to acquisitions.

The company has maintained a strong balance sheet with total liquidity of $1.4 billion and a net leverage ratio of 2.5x. Interest expense has been reduced by 17% year-over-year, contributing to the improved bottom-line performance.

Forward Guidance

Axalta provided updated guidance for the remainder of 2025 and offered preliminary insights into 2026 expectations:

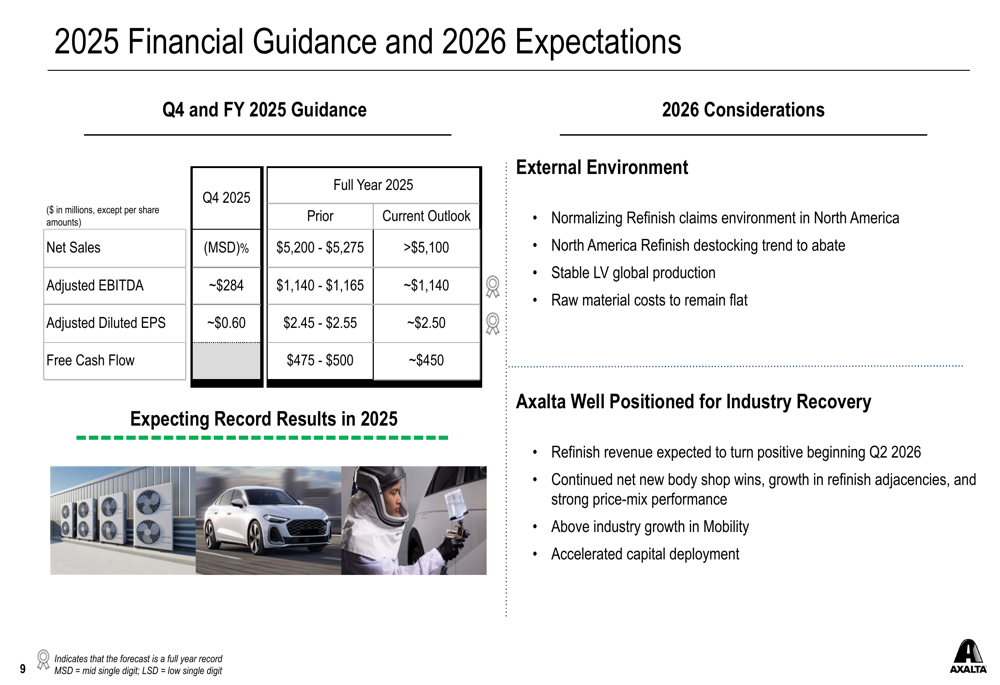

For the full year 2025, the company now expects net sales to exceed $5.1 billion, slightly below its prior guidance of $5.2-5.275 billion. Adjusted EBITDA is projected at approximately $1.14 billion, at the lower end of the previous range, while adjusted diluted EPS is expected to be around $2.50, in the middle of the prior guidance range.

For Q4 2025 specifically, Axalta anticipates a mid-single-digit percentage decline in net sales, adjusted EBITDA of approximately $284 million, and adjusted diluted EPS of around $0.60.

Looking ahead to 2026, the company expects the Refinish claims environment in North America to normalize and destocking trends to abate. Axalta anticipates Refinish revenue to turn positive beginning in Q2 2026, supported by continued body shop wins and growth in refinish adjacencies. The company also expects to maintain above-industry growth in its Mobility segment.

CEO Chris Villavarayan expressed confidence in the company’s trajectory during the earnings call, stating, "We’re well underway to deliver another record earnings year here in 2025." CFO Carl Anderson highlighted the strategic focus on share repurchases, noting, "At these trading multiples, it makes all the sense in the world to deploy almost all of our capital at this point to buying back shares."

With consistent margin expansion, strategic capital allocation, and expectations for market normalization in 2026, Axalta appears well-positioned to navigate current challenges while continuing to deliver shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.