Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Balco Group AB (STO:BALCO), the Nordic market leader in glazed balcony solutions, presented its third quarter 2025 results on October 27, revealing significant challenges in maintaining revenue and profitability. Following the announcement, the company’s stock plummeted 18.91% to 22.3 SEK, approaching its 52-week low of 22.1 SEK, as investors reacted to disappointing financial metrics.

The Sweden-based company, founded in 1987 and employing approximately 550 people, continues to navigate a mixed market environment across its European footprint, with particular strength in Swedish and Norwegian renovation markets contrasting with ongoing challenges in Denmark and slower recovery in Finland.

Quarterly Performance Highlights

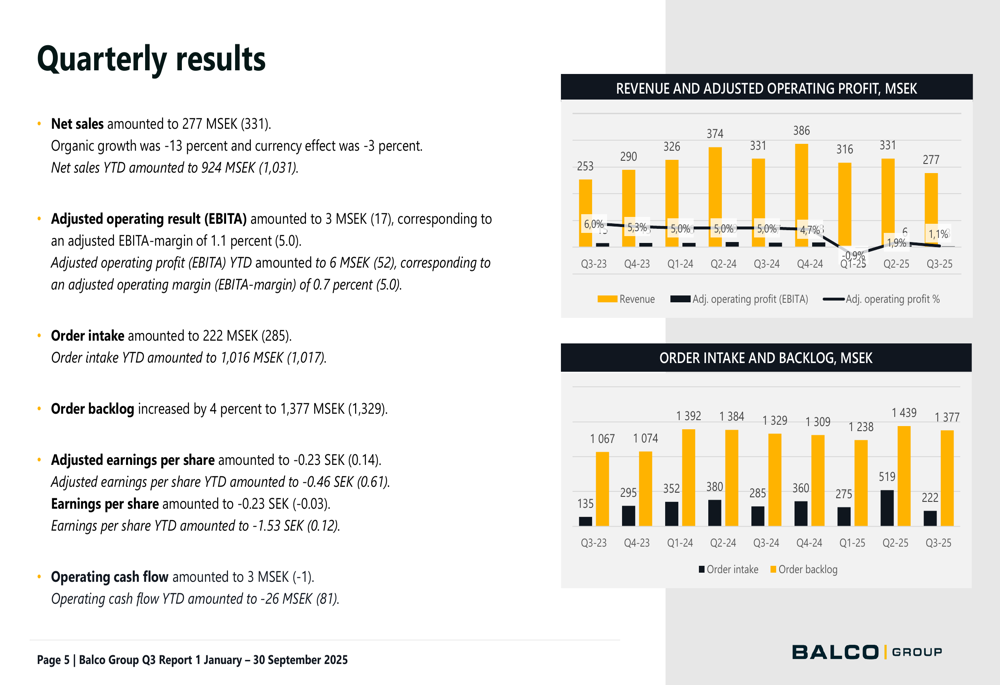

Balco reported net sales of 277 MSEK for Q3 2025, representing a 16.3% decline compared to the same period last year. The company’s organic growth was negative at -13%, while adjusted operating profit (EBITA) fell sharply to 3 MSEK, corresponding to a margin of just 1.1% - down from 5.0% in the previous year.

Order intake also declined significantly to 222 MSEK, down 22.1% from 285 MSEK in Q3 2024. Despite this drop, management highlighted that the last two quarters showed an 11% increase in orders, suggesting some stabilization. The company’s order backlog increased by 4% to 1,377 MSEK, providing some visibility for future revenues.

As shown in the following chart of quarterly financial performance:

Adjusted earnings per share turned negative at -0.23 SEK, reflecting the substantial profitability challenges facing the company. The financial results fell significantly short of market expectations, as evidenced by the sharp stock price reaction.

Segment Performance

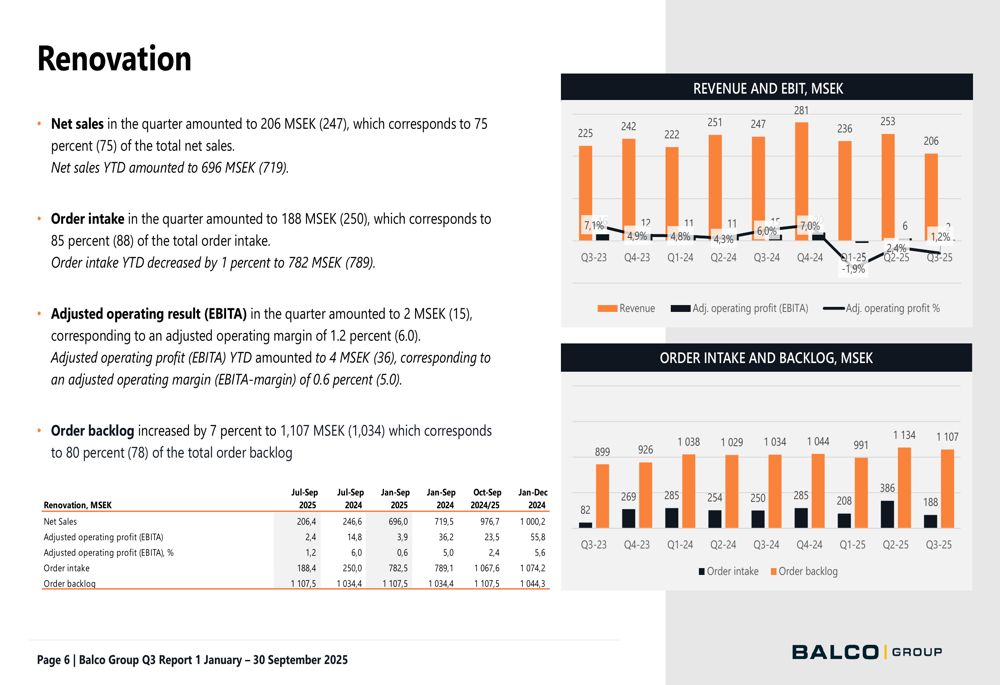

Balco’s business is divided into two main segments: renovation and new build. The renovation segment, which constitutes the company’s core business, generated 206 MSEK in net sales during Q3, representing 75% of total revenue. This segment received 188 MSEK in new orders (85% of total order intake) and maintained an order backlog of 1,107 MSEK, up 7% year-over-year.

The segment performance is illustrated in the following chart:

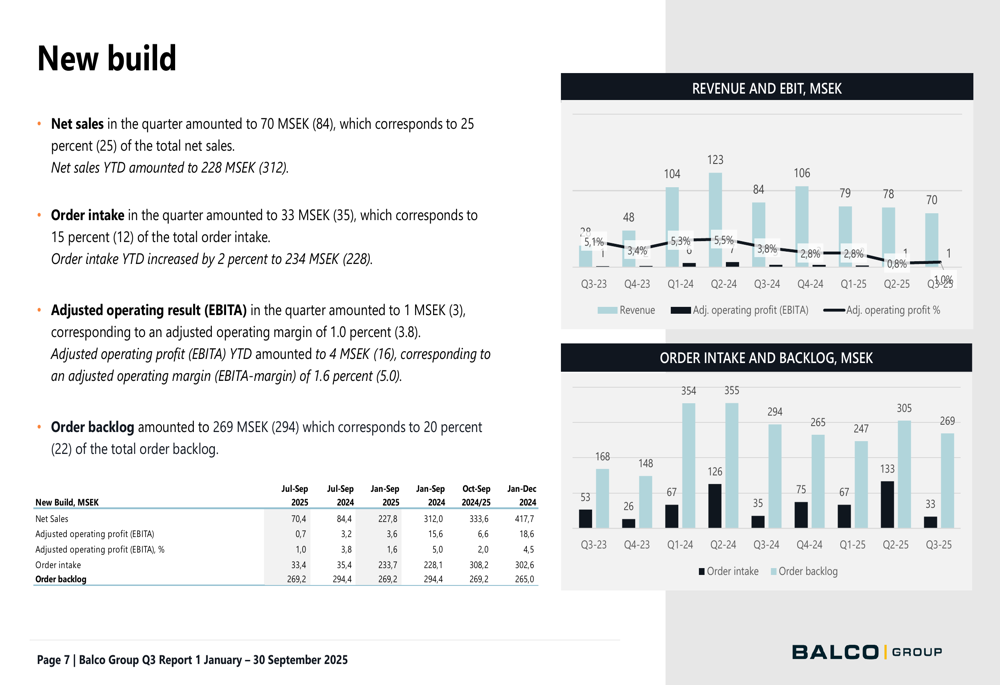

The new build segment contributed 70 MSEK (25% of total sales) with an order intake of 33 MSEK (15% of total). This segment’s adjusted operating result was 1 MSEK, corresponding to a 1.0% margin. Management noted that recovery in the new build segment, particularly in Nordic countries, is expected to take longer than in renovation.

The new build segment performance is shown here:

Market Expansion & Outlook

Despite current financial challenges, Balco continues to pursue geographic expansion. The company secured its first orders in Germany using glazing systems from its Riikku brand and won a contract for balconies for a social housing project in the Netherlands. Management sees substantial potential in the UK balcony market and strong demand in the German renovation sector.

The company’s market diversification strategy is illustrated in this overview:

CEO Camilla Ekdahl expressed cautious optimism for the remainder of the year regarding renovation project order intake, while acknowledging that recovery in the new build segment will take longer. The company continues to implement profitability-improving measures and cost savings initiatives launched earlier in the year.

The market update shows varying conditions across regions:

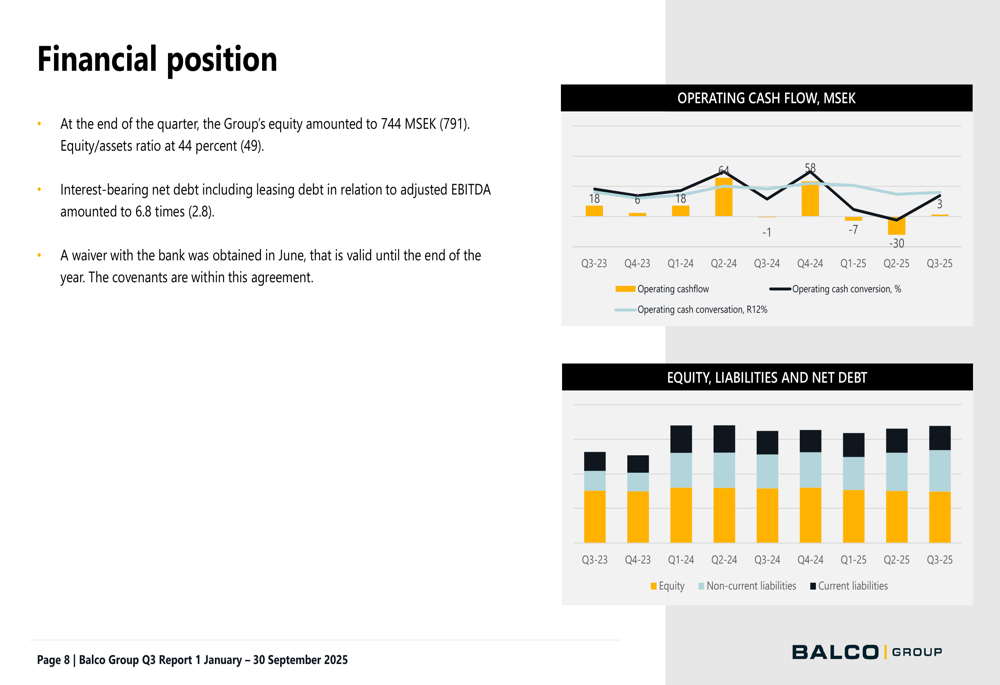

Financial Position & Challenges

Balco’s financial position shows signs of stress, with interest-bearing net debt including leasing debt at 6.8 times adjusted EBITDA - a concerning level that prompted the company to obtain a waiver from its bank in June, valid until the end of 2025. The Group’s equity amounted to 744 MSEK at quarter-end, with an equity/assets ratio of 44%.

This financial position is illustrated in the following chart:

The high debt-to-EBITDA ratio and need for a banking covenant waiver underscore the severity of the company’s financial challenges, despite management’s relatively measured tone in the presentation. The company’s structural measures and cost-saving initiatives will be crucial to improving its financial health.

Forward-Looking Statements

Looking ahead, Balco management remains "cautiously optimistic" about order intake for renovation projects for the rest of the year, while acknowledging that the new build segment in Nordic countries faces a longer recovery timeline. The company continues to focus on profitability-improving measures and cost savings.

As shown in the company’s concluding remarks:

However, investors appear less convinced of the near-term outlook, as evidenced by the significant stock price decline following the earnings release. With shares now trading near 52-week lows, market participants are seeking more concrete evidence of a sustainable turnaround in both revenue growth and profitability before regaining confidence in Balco’s prospects.

The company’s ability to improve margins, manage its debt load, and capitalize on its order backlog will be critical factors for investors to monitor in upcoming quarters. While Balco maintains market leadership in the Nordic region and continues its geographic expansion efforts, the financial results suggest significant work remains to restore the company to a healthier growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.