Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Baldwin Insurance Group Inc (NYSE:BWIN) released its first quarter 2025 earnings presentation on May 6, 2025, revealing a mixed financial picture characterized by strong organic revenue growth but declining GAAP earnings. The insurance broker reported 10% organic revenue growth, while GAAP net income fell 36% compared to the same period last year.

The company’s stock has experienced significant volatility since the end of Q1, trading at $39.37 as of May 12, 2025, down from $44.69 at the end of the first quarter. This represents a decline of approximately 12% since quarter-end, despite the company’s reported revenue growth.

Quarterly Performance Highlights

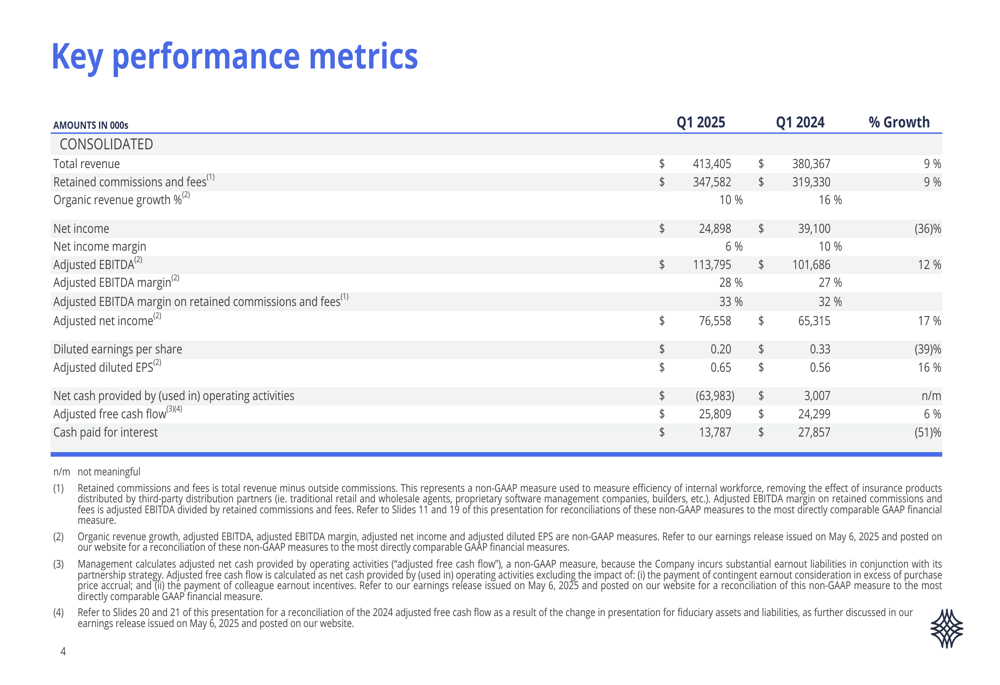

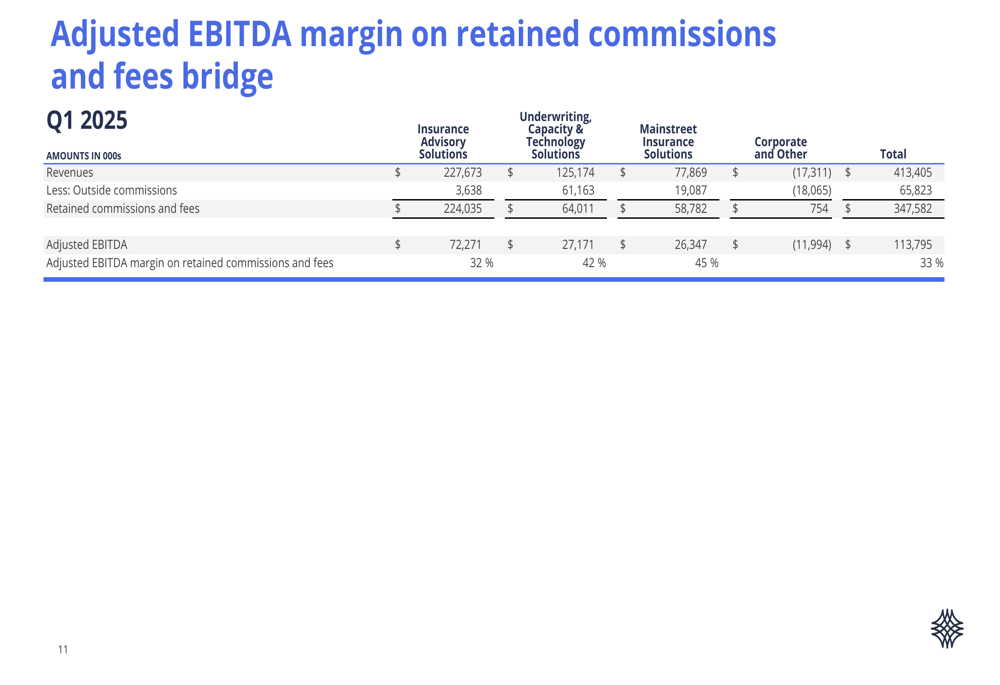

Baldwin Insurance reported total revenue of $413.4 million for Q1 2025, representing a 9% increase compared to $380.4 million in Q1 2024. Retained commissions and fees, a key metric for the company, grew by 9% to $347.6 million.

As shown in the following comprehensive performance metrics table:

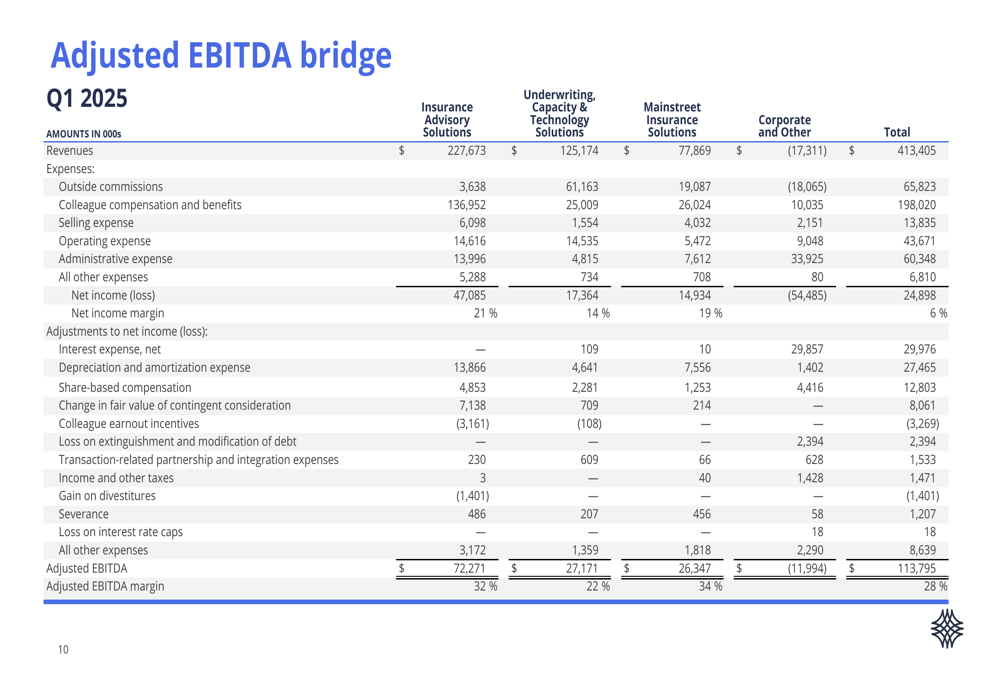

While top-line growth remained robust, GAAP earnings metrics showed significant pressure. Net income declined 36% year-over-year to $24.9 million, and diluted earnings per share fell 39% to $0.20. However, adjusted metrics painted a more positive picture, with adjusted EBITDA increasing 12% to $113.8 million and adjusted diluted EPS rising 16% to $0.65.

Segment Performance Analysis

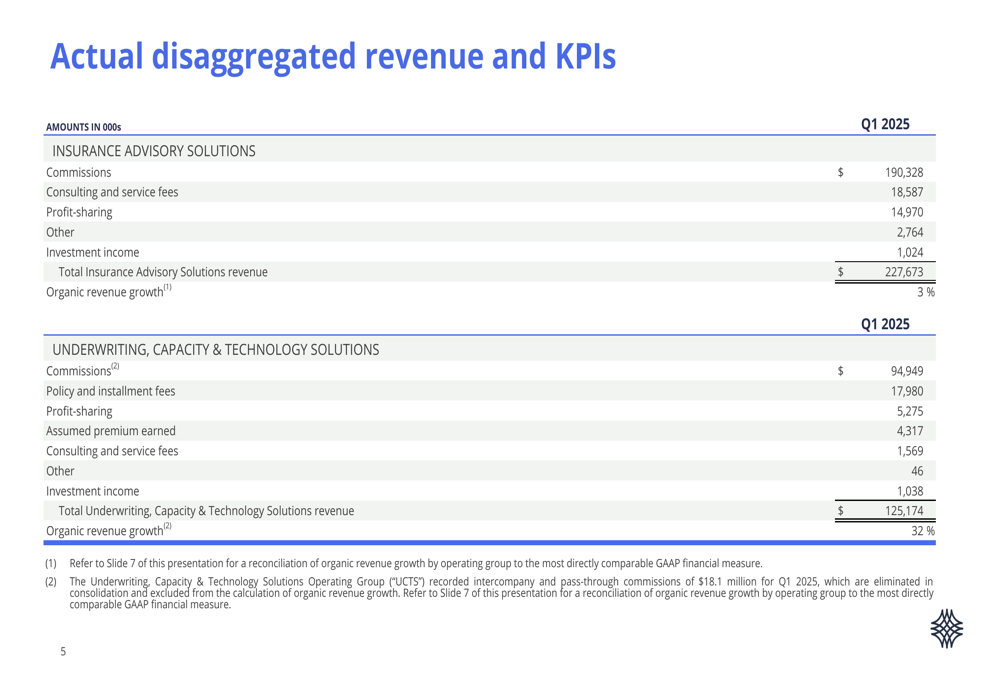

Baldwin’s performance varied significantly across its three business segments, with the Underwriting, Capacity & Technology Solutions segment delivering exceptional results.

The company’s segment breakdown reveals the following:

The Underwriting, Capacity & Technology Solutions segment was the standout performer, generating $125.2 million in revenue with impressive 32% organic growth. This segment’s strong performance helped offset more modest growth in the Insurance Advisory Solutions segment, which posted 3% organic growth on $227.7 million in revenue.

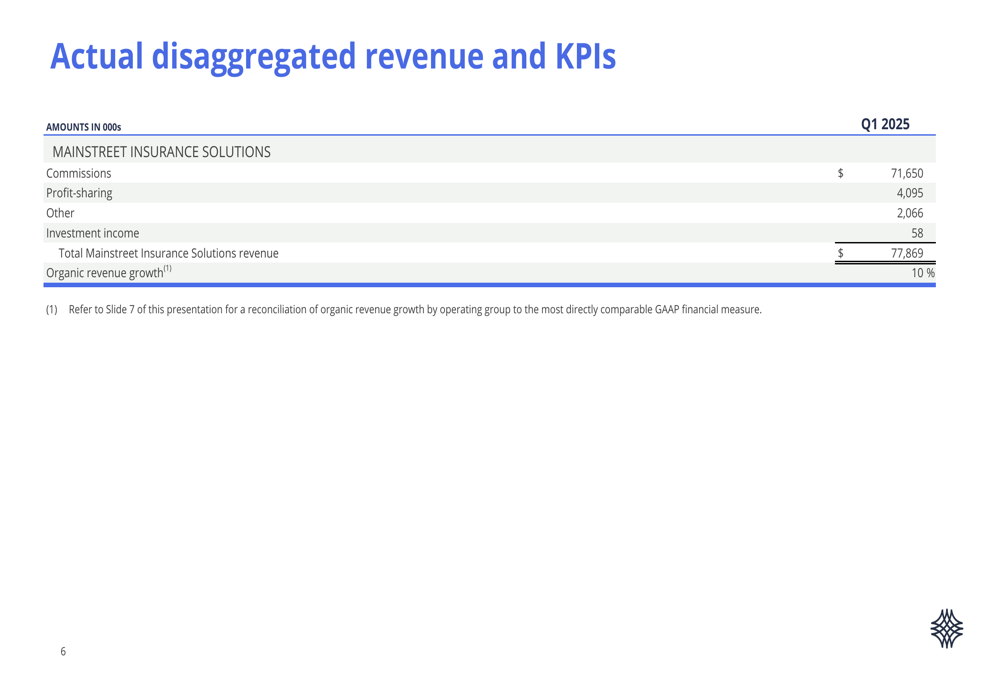

The Mainstreet Insurance Solutions segment delivered solid results with $77.9 million in revenue and 10% organic growth:

Detailed Financial Analysis

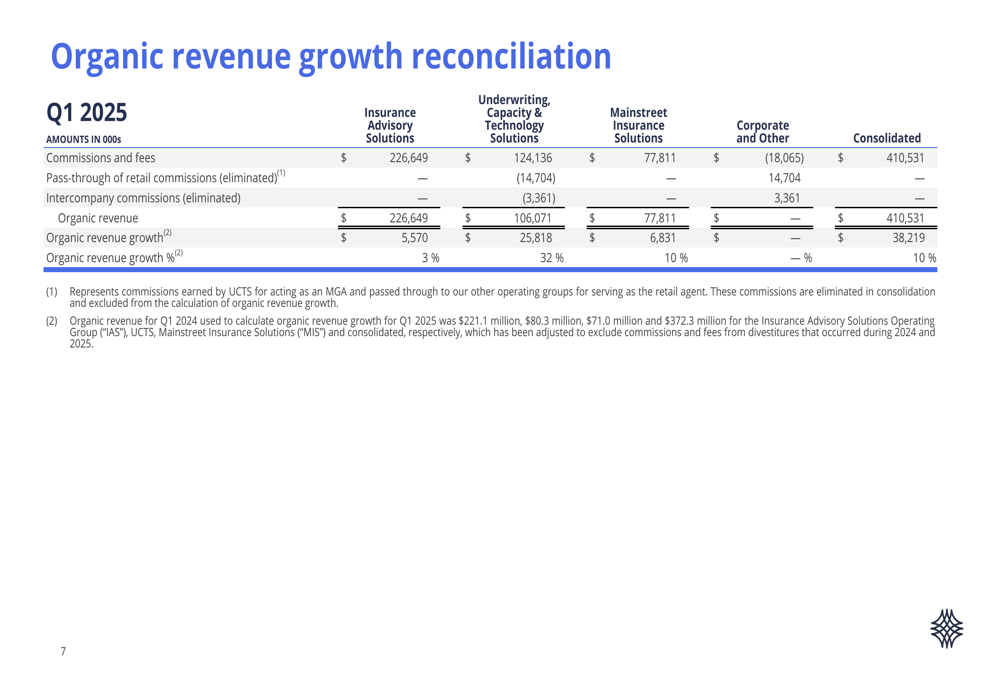

Baldwin’s organic revenue growth of 10% represents a deceleration from the 17% growth reported for full-year 2024, but remains at the lower end of the company’s previously guided range of 10-15% for 2025.

The reconciliation of organic revenue growth across segments provides further insight into the company’s performance:

The company’s adjusted EBITDA bridge demonstrates how Baldwin arrived at its $113.8 million figure, representing a 28% margin compared to 27% in the prior-year period:

When measured against retained commissions and fees, the adjusted EBITDA margin improved to 33% from 32% in Q1 2024:

Capital Structure and Treasury

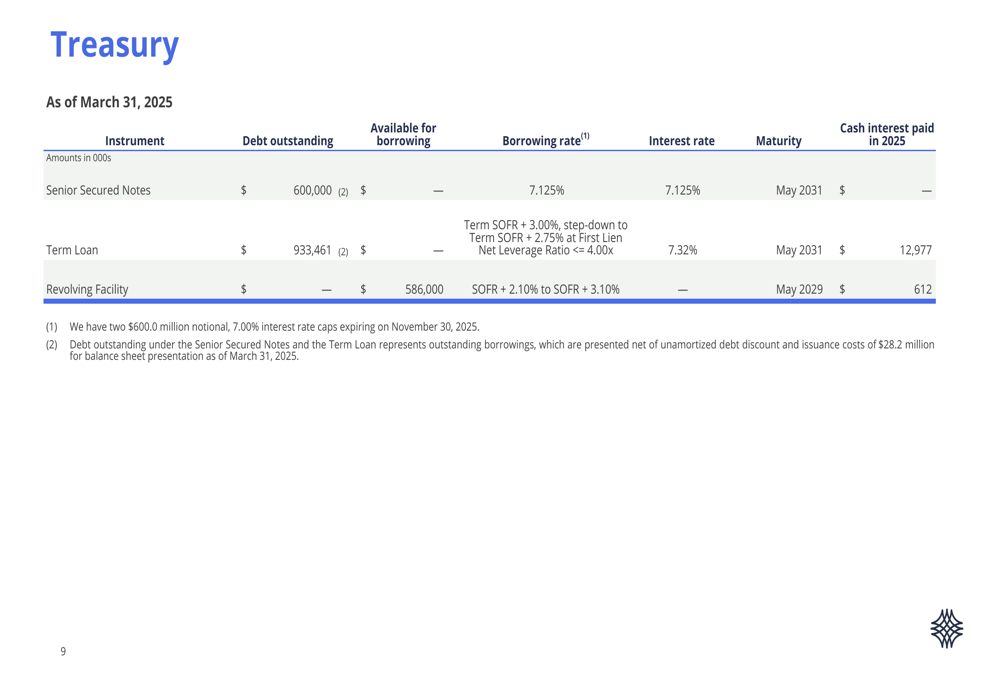

Baldwin’s treasury information reveals a substantial debt load, with $1.53 billion in total debt outstanding as of March 31, 2025. The company maintains $586 million available for borrowing under its revolving facility.

The following table details the company’s debt structure:

The company paid $13.6 million in cash interest during Q1 2025, with its debt carrying interest rates between 7.125% and 7.32%. All major debt facilities mature in 2029 or later, providing Baldwin with long-term financing stability despite the relatively high interest rates in the current environment.

Shareholder Value and Stock Performance

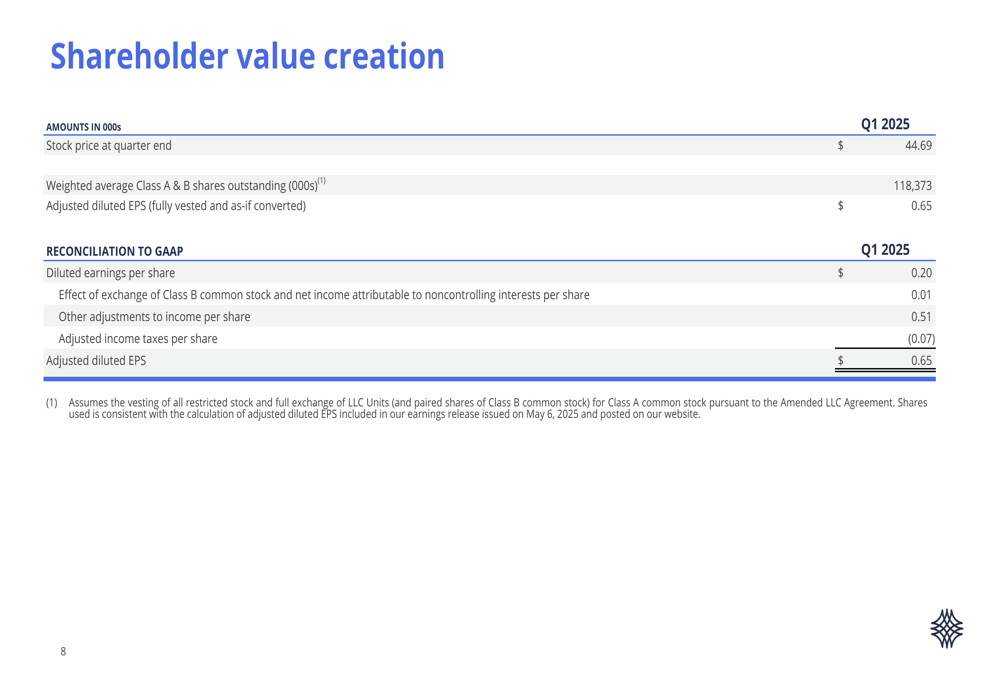

Baldwin’s stock price of $44.69 at quarter-end represented a premium to its current trading price of $39.37. The company’s adjusted diluted EPS of $0.65 for the quarter represents significant growth over the GAAP figure of $0.20 per share.

The following reconciliation explains the adjustments made to arrive at the adjusted EPS figure:

Forward Outlook

While the Q1 2025 presentation does not provide explicit forward guidance, the 10% organic revenue growth achieved in the first quarter aligns with the company’s previous guidance of growth in the "lower half of the 10-15% range" for 2025.

The significant gap between GAAP and adjusted metrics bears watching in future quarters, particularly the 36% decline in net income despite strong revenue growth. This disparity suggests underlying challenges that may impact future performance, potentially including integration costs from acquisitions or other one-time expenses that the company excludes from its adjusted figures.

Baldwin’s ability to maintain its organic growth rate while improving GAAP profitability will be crucial for investor confidence in the coming quarters, especially given the recent stock price decline from its Q1 ending level.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.