Street Calls of the Week

Introduction & Market Context

Bank of Hawaii Corporation (NYSE:BOH) presented its third quarter 2020 financial results on October 26, 2020, highlighting the bank’s performance amid significant economic challenges in Hawaii due to the COVID-19 pandemic. The presentation provided insights into both the state’s economic conditions and the bank’s financial resilience during this difficult period.

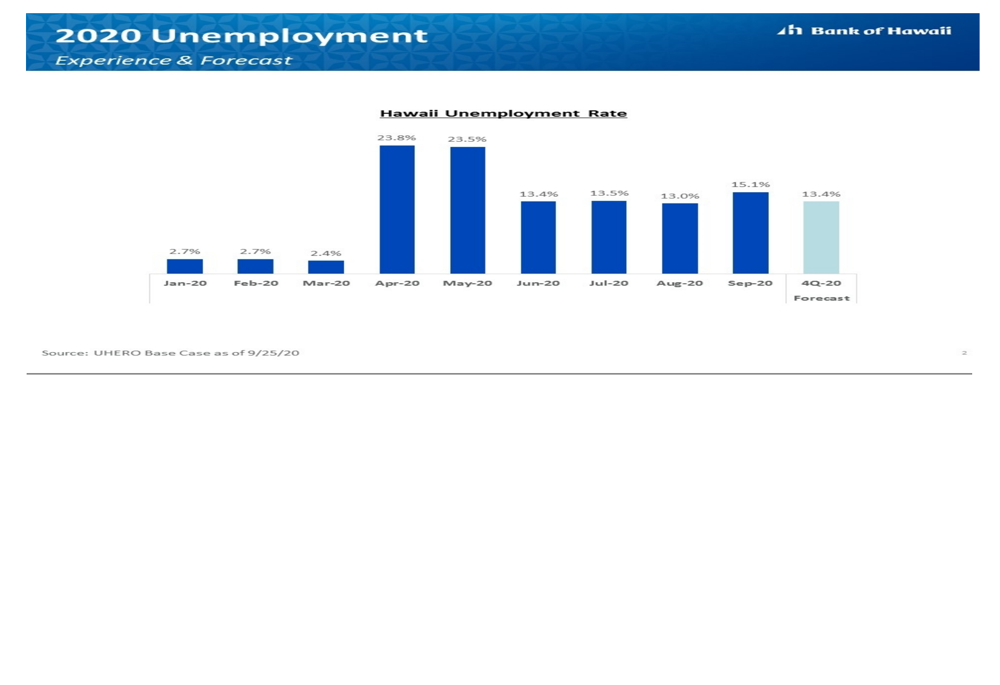

Hawaii’s unemployment rate reached 15.1% in September 2020, reflecting the severe impact of travel restrictions on the tourism-dependent economy. However, forecasts showed improvement with unemployment expected to decline to 13.4% by Q4 2020, and continue decreasing to 9.7% in 2021 and 5.0% by 2022.

As shown in the following chart of Hawaii’s unemployment experience and forecast for 2020:

The economic outlook for Hawaii, while challenging, showed signs of improvement compared to earlier projections. The real GDP forecast for 2020 was revised to -11.8%, a significant improvement from the earlier forecast of -18.2% made in May 2020.

Quarterly Performance Highlights

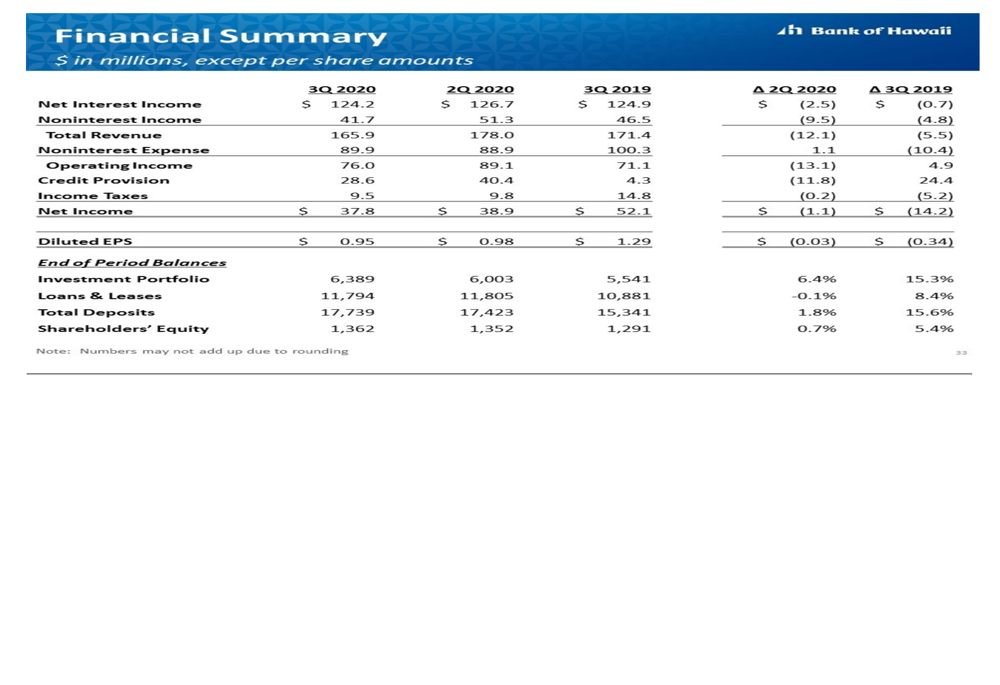

Despite the challenging economic environment, Bank of Hawaii reported net income of $37.8 million for Q3 2020. The bank’s net interest income remained relatively stable at $124.2 million, though net interest margin faced pressure, declining to approximately 2.7% from 3.12% a year earlier.

The bank’s financial summary showed the following key metrics for Q3 2020:

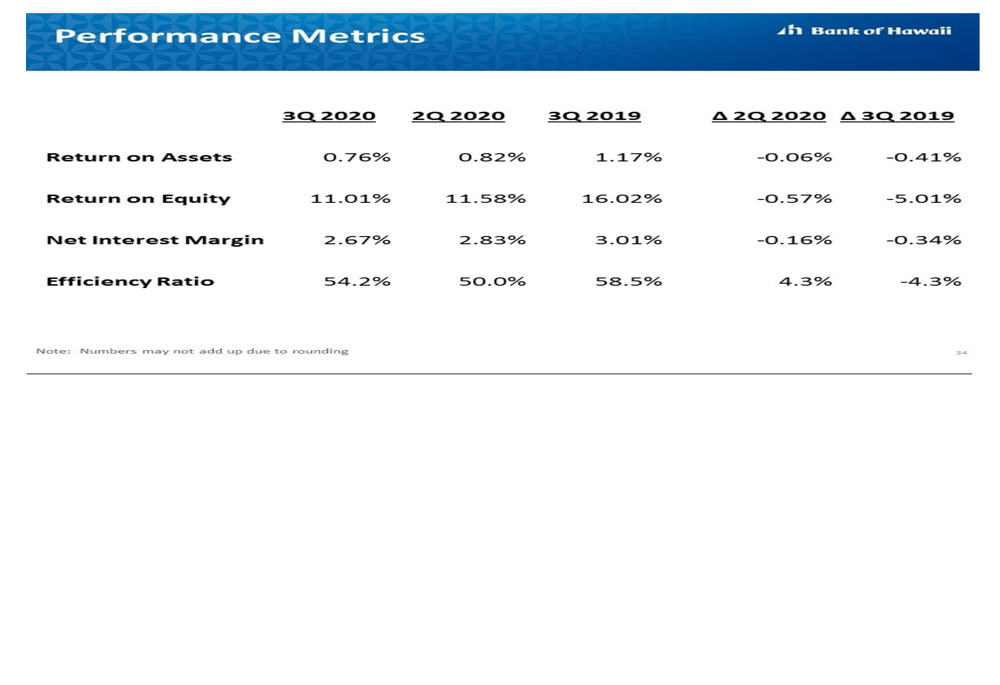

Performance metrics revealed the impact of the pandemic on returns, with the bank maintaining positive but reduced profitability:

The bank demonstrated disciplined expense management, with a noninterest expense CAGR of 0.8% compared to average inflation of 1.9%, reflecting long-term cost control measures:

Credit Quality & Risk Management

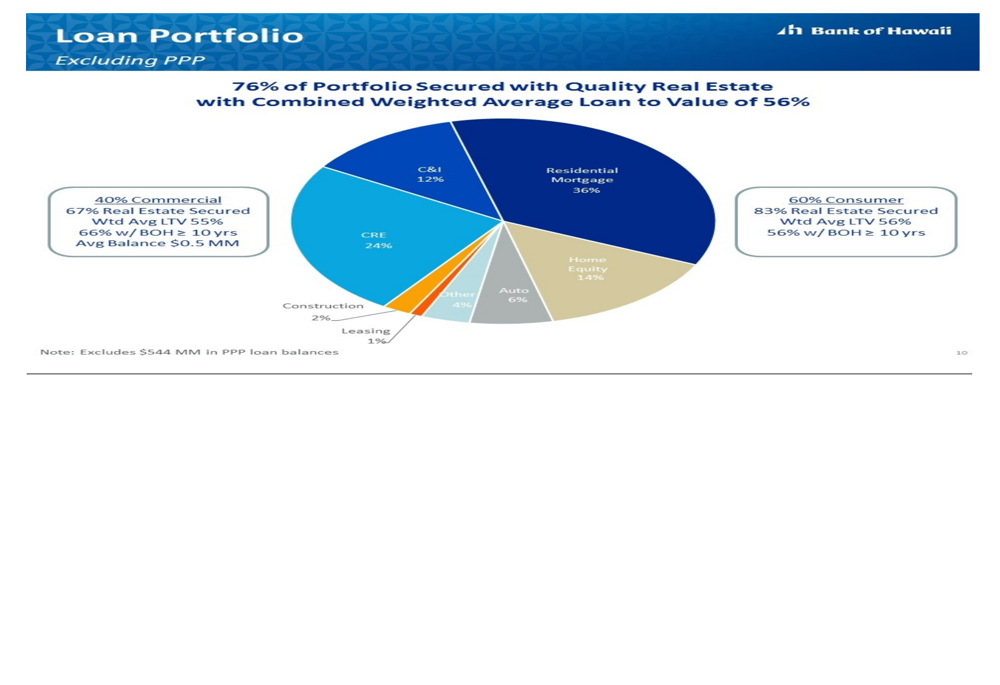

A key focus of the presentation was the bank’s credit quality and risk management during the pandemic. The loan portfolio showed 76% secured with quality real estate, with a weighted average loan-to-value (LTV) ratio of 56%, providing significant protection against potential defaults.

The composition of the loan portfolio (excluding PPP loans) demonstrated the bank’s focus on secured lending:

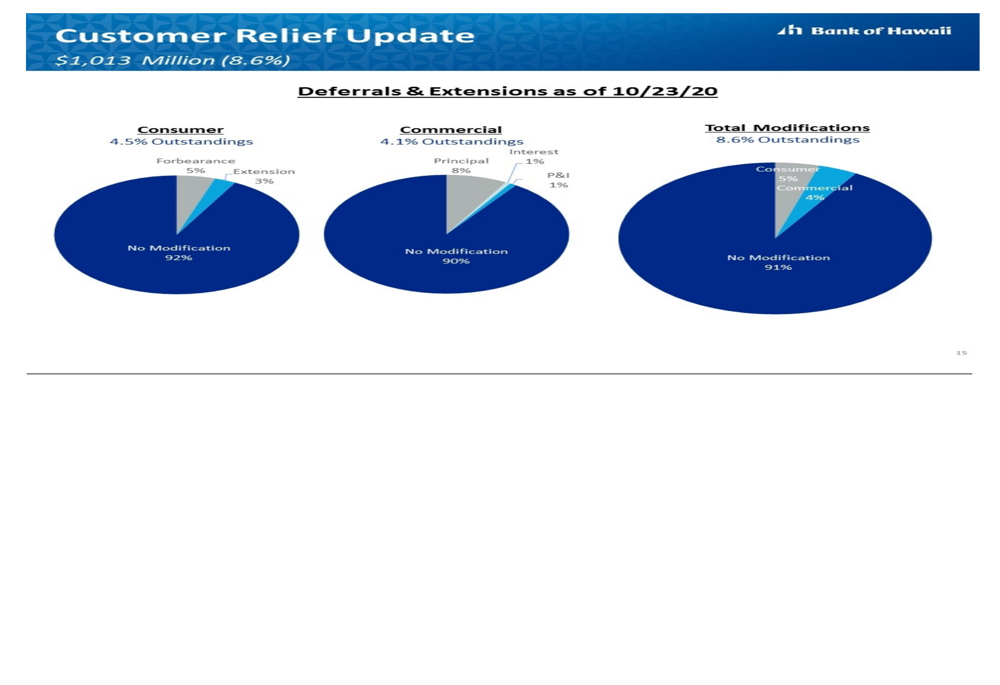

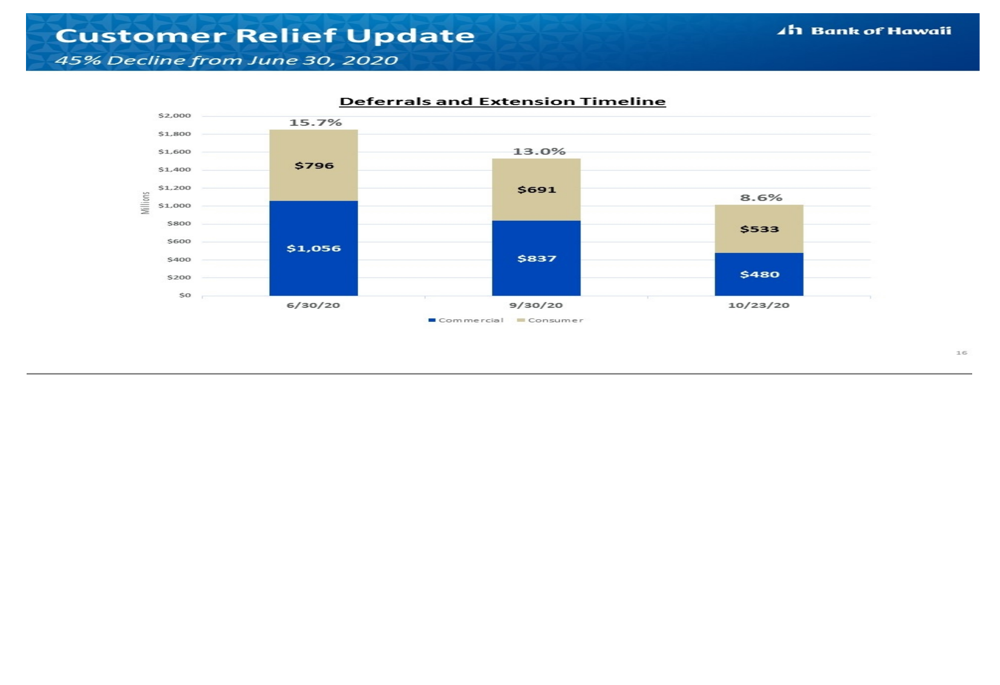

The bank highlighted its customer relief efforts, showing significant progress in reducing payment deferrals. Total modifications decreased from 13.0% of outstandings on September 30, 2020, to 8.6% by October 23, 2020, indicating improving conditions for borrowers:

This positive trend was further illustrated in the timeline of deferrals and extensions, showing a steady decline from June to October:

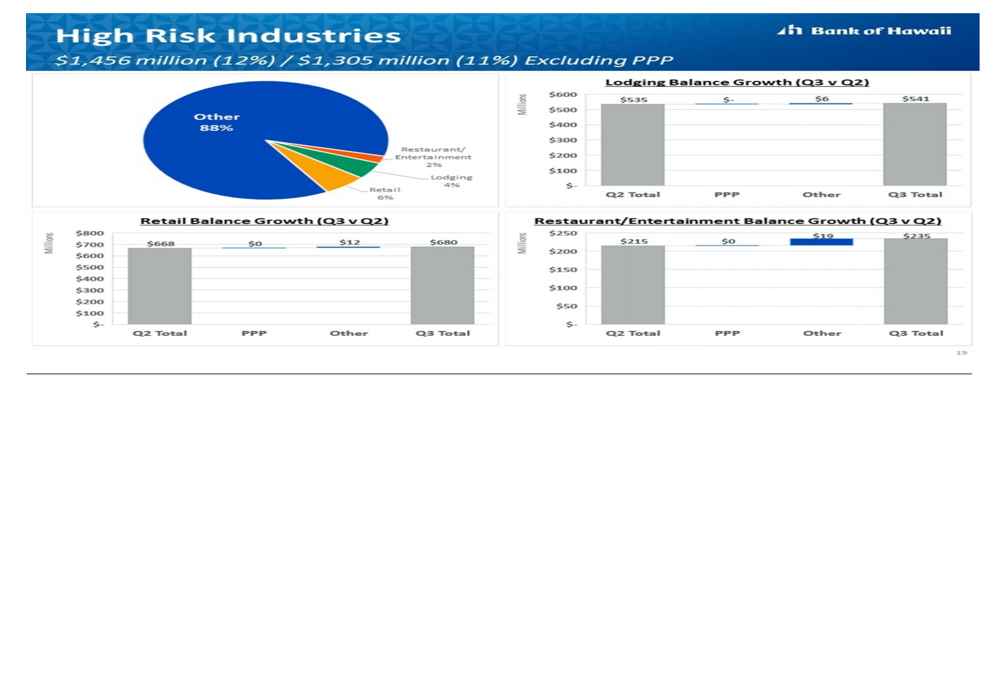

The presentation addressed exposure to high-risk industries affected by the pandemic, including lodging, retail, and restaurant/entertainment sectors, which collectively represented 12% of total loans or $1,456 million:

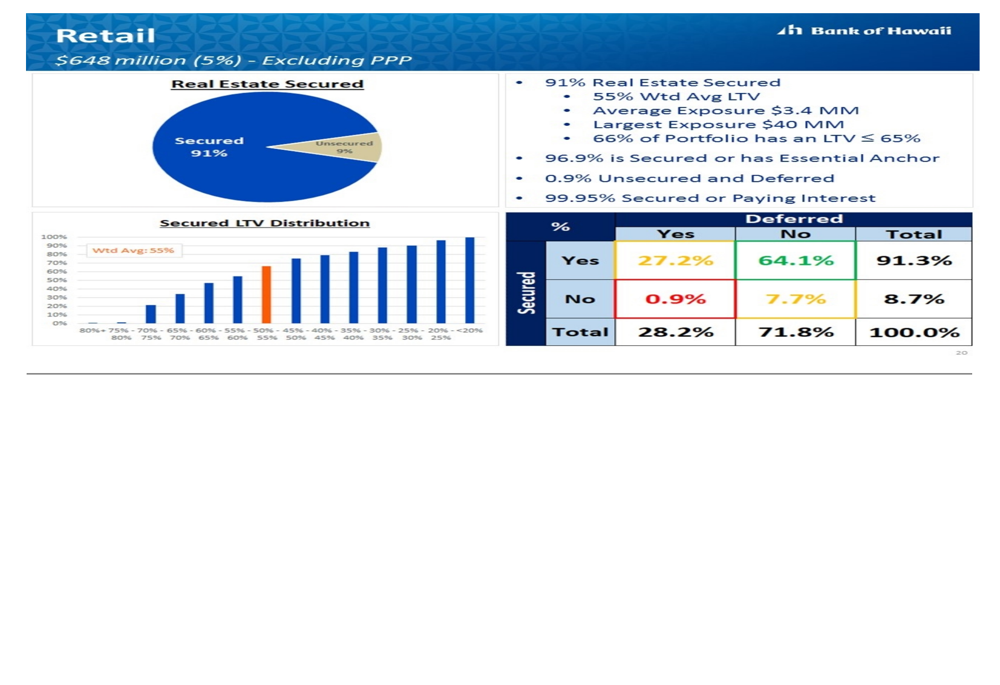

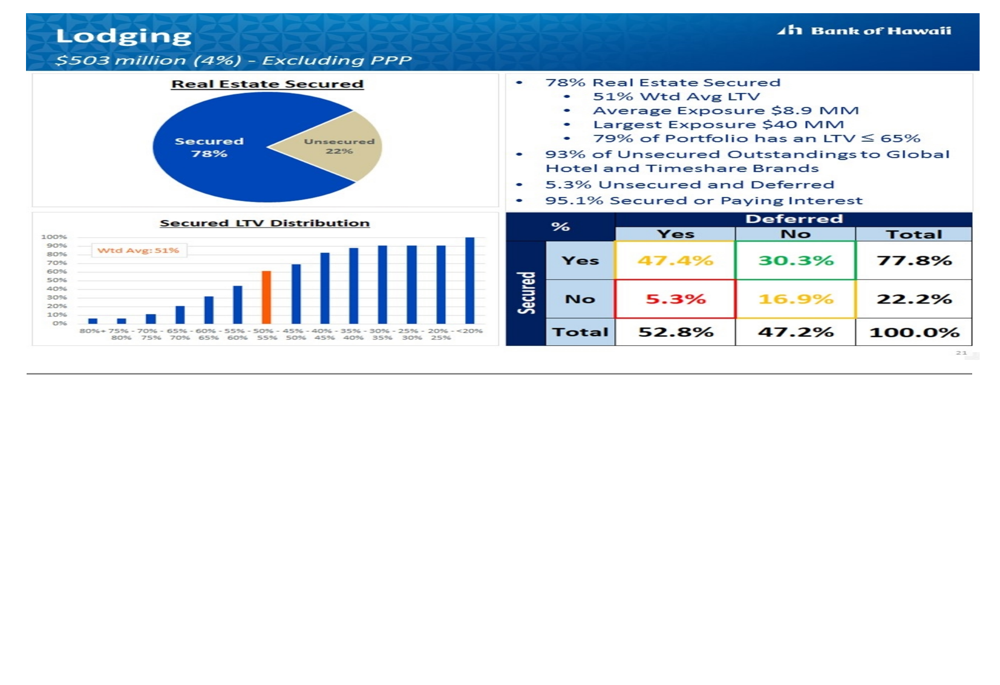

For the retail sector specifically, the bank emphasized that 91% of these loans were secured by real estate with a weighted average LTV of 55%, providing significant protection:

Similarly, in the lodging sector, 78% of loans were secured by real estate with a weighted average LTV of 51%:

Capital & Liquidity Position

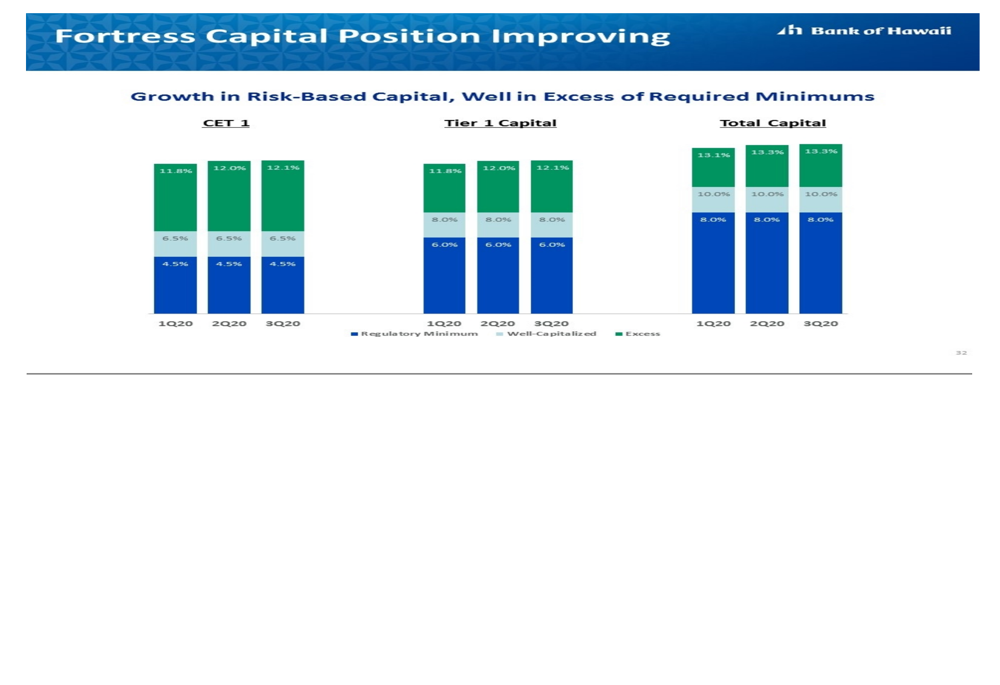

Bank of Hawaii maintained a strong capital position throughout the pandemic, with capital ratios well above regulatory requirements. The CET1 ratio improved from 11.8% in Q1 2020 to 12.1% in Q3 2020, demonstrating the bank’s financial strength:

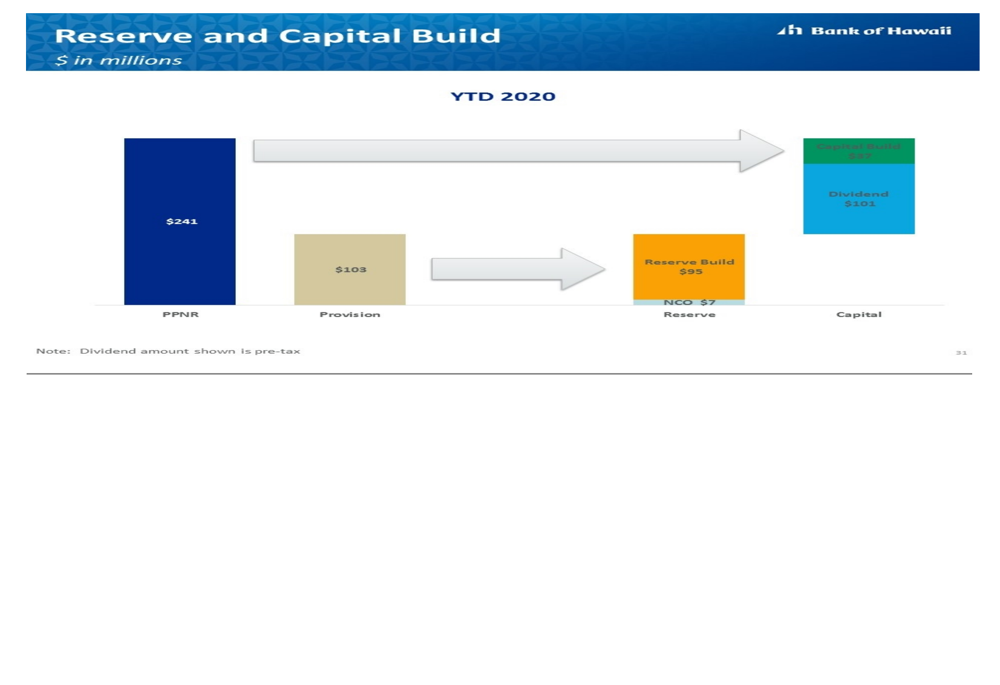

The bank’s reserve and capital build for 2020 showed pre-provision net revenue (PPNR) of $241 million, with $103 million allocated to provisions and $37 million to capital build, while maintaining dividend payments of $101 million:

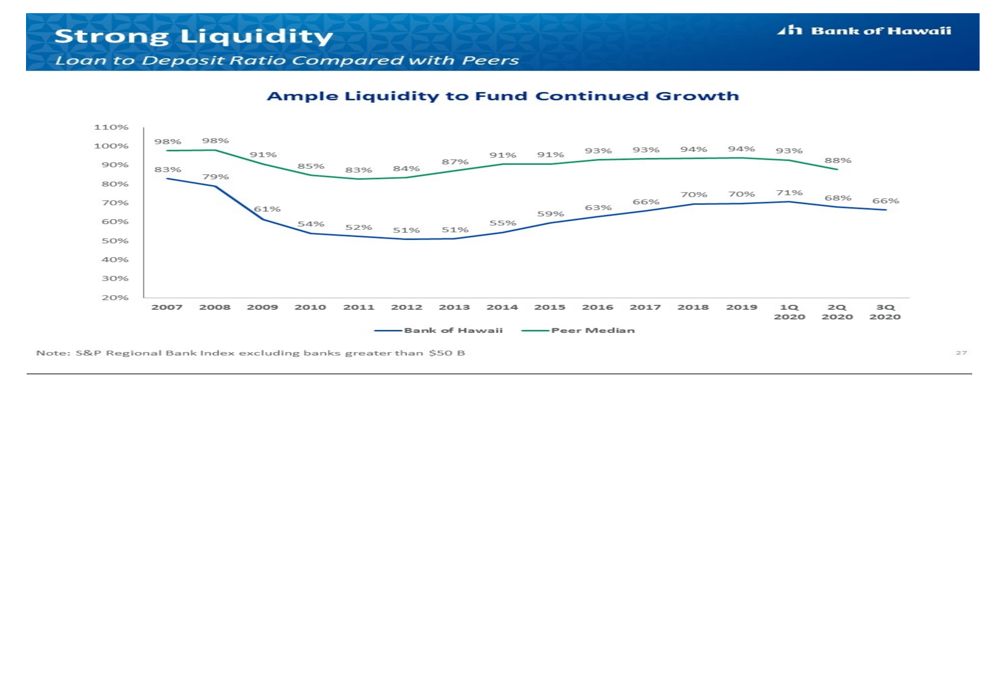

Liquidity remained strong, with a loan-to-deposit ratio of 66%, significantly lower than the peer average of 88%, providing ample funding capacity for continued growth:

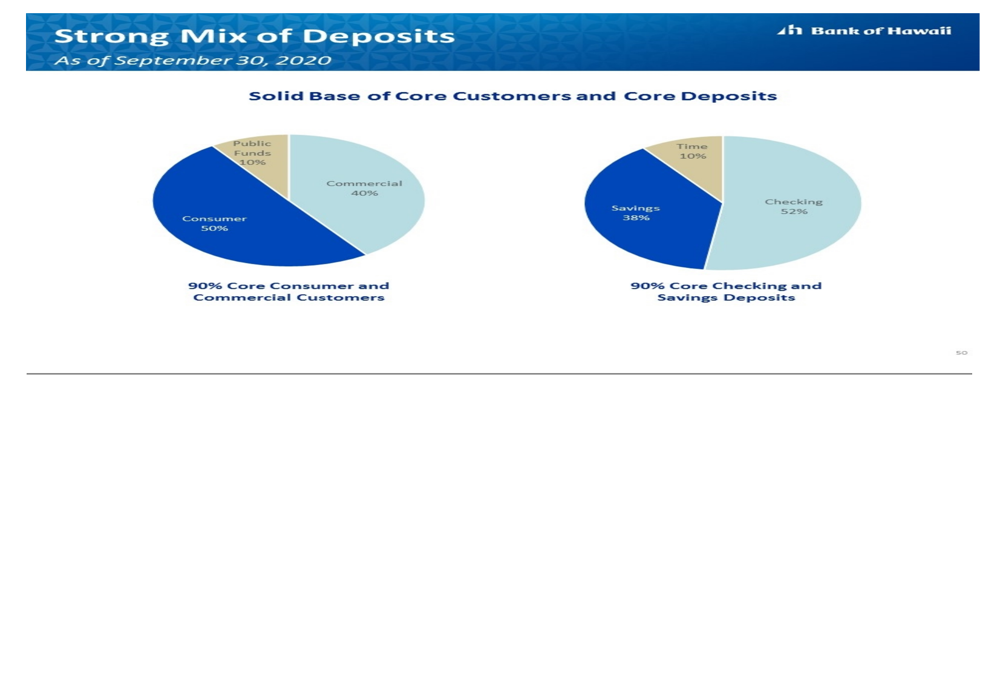

The bank maintained a strong mix of core deposits, with 50% from consumer accounts, 40% from commercial accounts, and 10% from public funds:

Forward-Looking Statements

Looking ahead, Bank of Hawaii positioned itself for continued stability through the economic recovery. The presentation highlighted improving economic forecasts for Hawaii, with unemployment expected to gradually decrease and GDP to return to growth in 2021.

The bank emphasized its "well positioned" status based on several strengths:

- Strong credit metrics

- Continued stable loan growth

- Strong deposit growth

- Well-managed funding costs

- Strong liquidity

- Solid capital levels

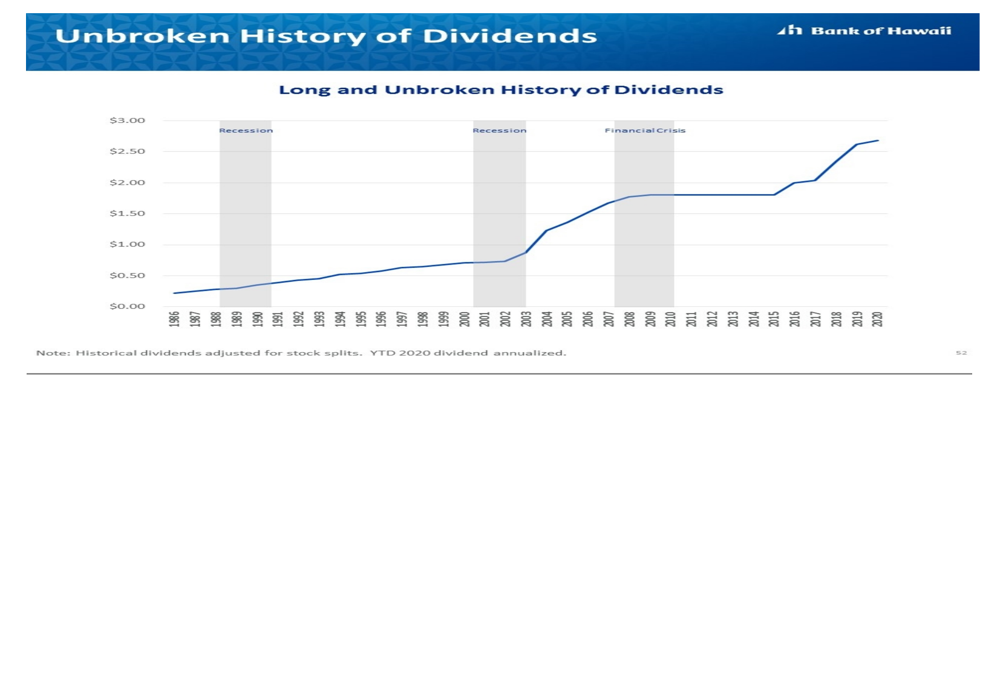

The presentation also noted the bank’s unbroken history of dividends since 1986, demonstrating its long-term financial stability and commitment to shareholder returns:

While the pandemic created significant challenges for Hawaii’s economy and the banking sector, Bank of Hawaii’s Q3 2020 presentation demonstrated resilience through strong capital management, secured lending practices, and improving credit metrics as customer deferrals declined. The bank appeared well-positioned to navigate the ongoing economic recovery in Hawaii as tourism gradually resumed.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.