Gold prices just lower; monthly gains on track

Introduction & Market Context

Bank of Marin Bancorp (NASDAQ:BMRC) presented its first quarter 2025 financial results on April 28, 2025, highlighting improved margins and deposit growth despite a slight earnings miss. The California-based community bank reported earnings per share of $0.30, just below analyst expectations of $0.31, while its stock traded at $20.82, showing minimal movement following the announcement. With $3.8 billion in total assets and a market capitalization of $357.6 million, the bank continues to maintain its strong position in Northern California’s competitive banking landscape.

Quarterly Performance Highlights

Bank of Marin delivered solid first quarter results driven by strategic deposit management and improved interest margins. The bank’s net interest margin increased to 2.86% from 2.80% in the previous quarter, reflecting successful efforts to reduce deposit costs while maintaining asset yields.

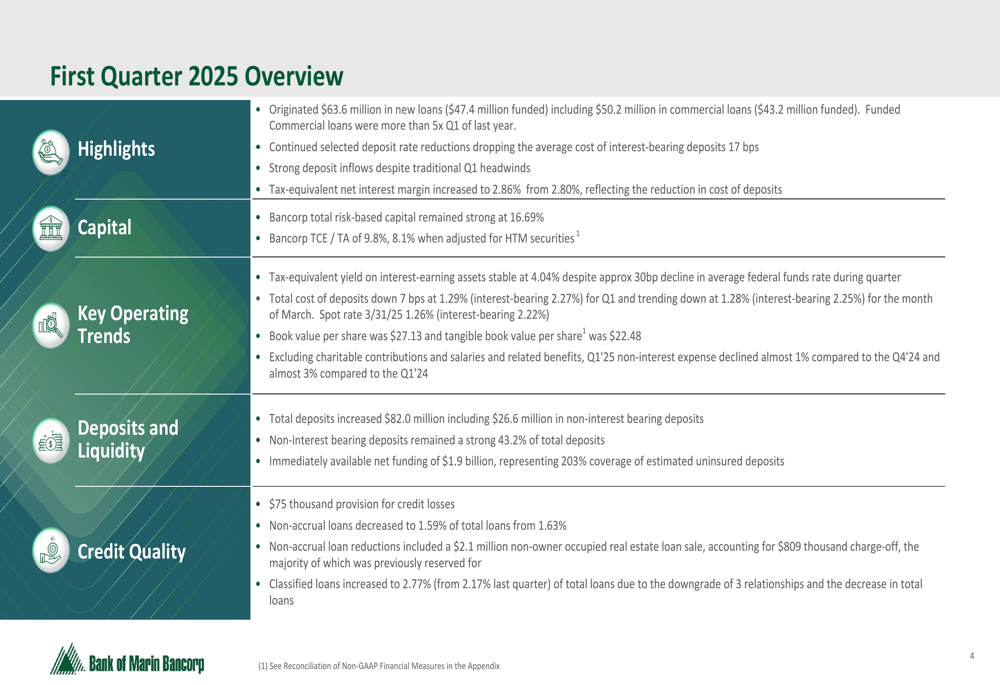

As shown in the following comprehensive overview of the bank’s first quarter performance:

Loan origination reached $63.6 million in Q1 2025, with $47.4 million funded during the quarter. Notably, commercial loans grew more than five times compared to the same period last year, demonstrating the bank’s successful business development efforts. Total (EPA:TTEF) deposits increased by $82.0 million, with non-interest bearing deposits comprising 43.2% of the total deposit base, providing a cost advantage in the current rate environment.

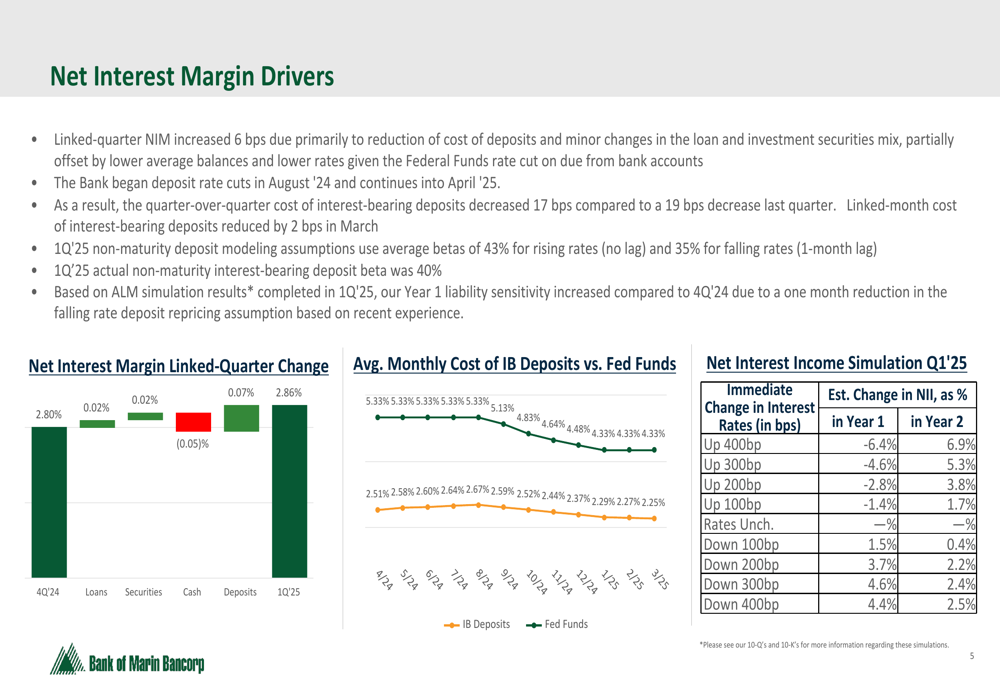

The bank’s net interest margin improvement was driven primarily by strategic deposit pricing adjustments, as illustrated in this analysis of margin drivers:

The chart shows how the bank’s net interest margin increased from 2.80% to 2.86% quarter-over-quarter, with deposit costs being the primary contributor to this improvement. Management initiated deposit rate reductions beginning in August 2024 and has continued this strategy, resulting in a 17 basis point decrease in the cost of interest-bearing deposits compared to the previous quarter.

Detailed Financial Analysis

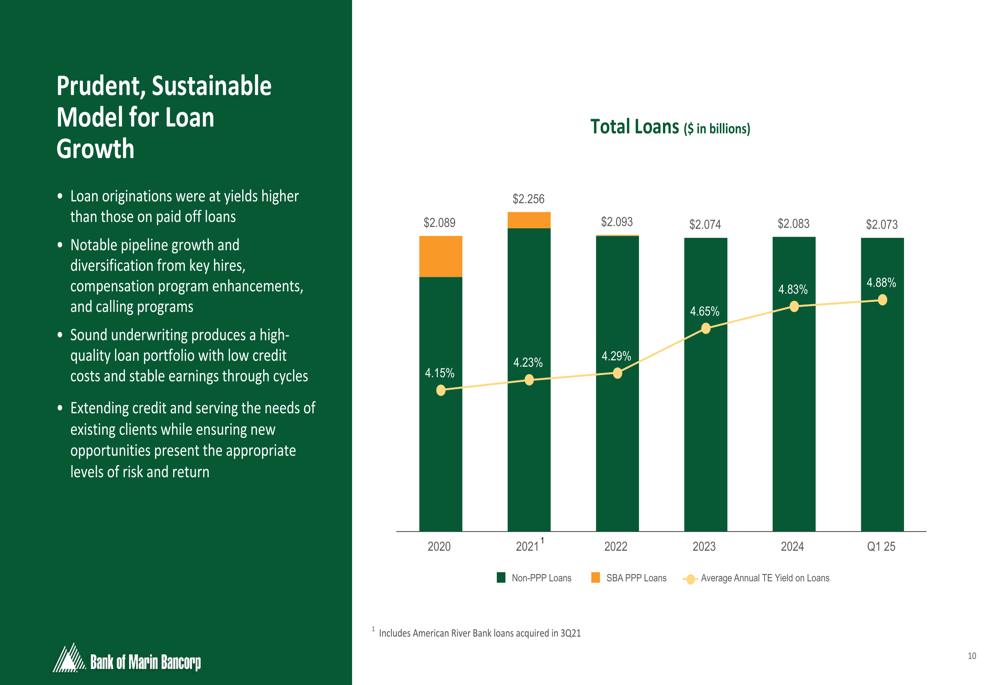

Bank of Marin maintains a well-diversified loan portfolio, with a strategic focus on commercial real estate lending. The bank’s disciplined approach to loan growth has resulted in new originations at yields higher than those on paid-off loans, contributing to margin stability.

The following chart illustrates the bank’s prudent approach to loan growth:

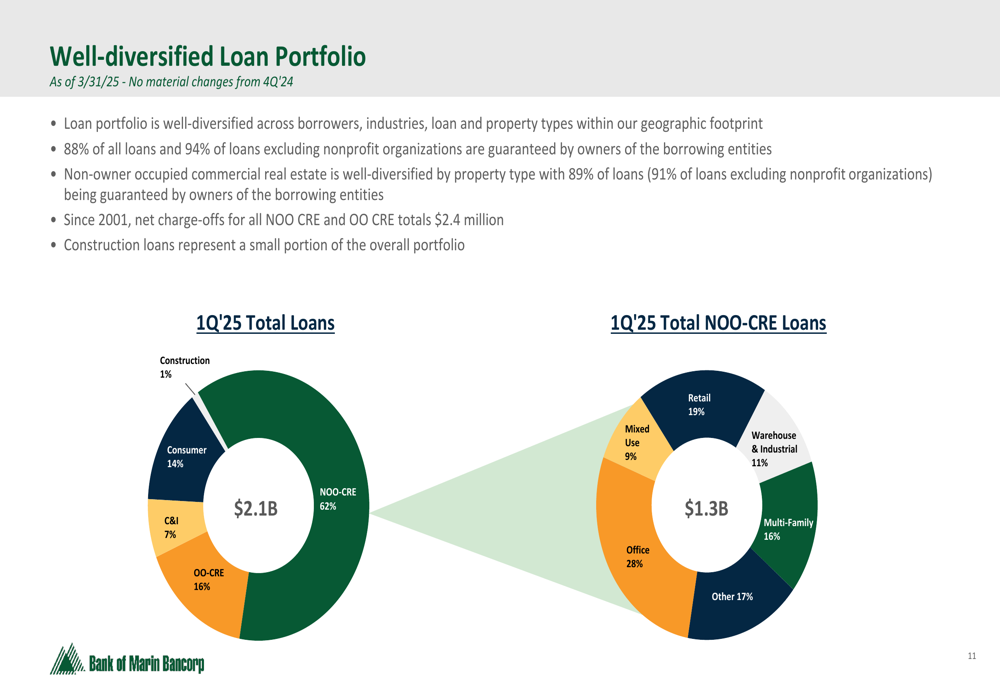

The bank’s loan portfolio remains well-diversified across property types and geographies, providing protection against sector-specific downturns. Non-owner occupied commercial real estate represents the largest segment at 62% of the total portfolio, followed by owner-occupied commercial real estate at 16%.

The composition of the loan portfolio is detailed in the following breakdown:

Asset quality metrics remain strong, with the allowance for credit losses to total loans holding steady at 1.44%. While non-accrual loans increased to 1.59% of total loans from 0.31% a year earlier, the bank proactively sold one non-accrual commercial real estate loan to minimize potential losses. Historically, Bank of Marin has maintained negligible net charge-offs, reflecting its conservative underwriting standards.

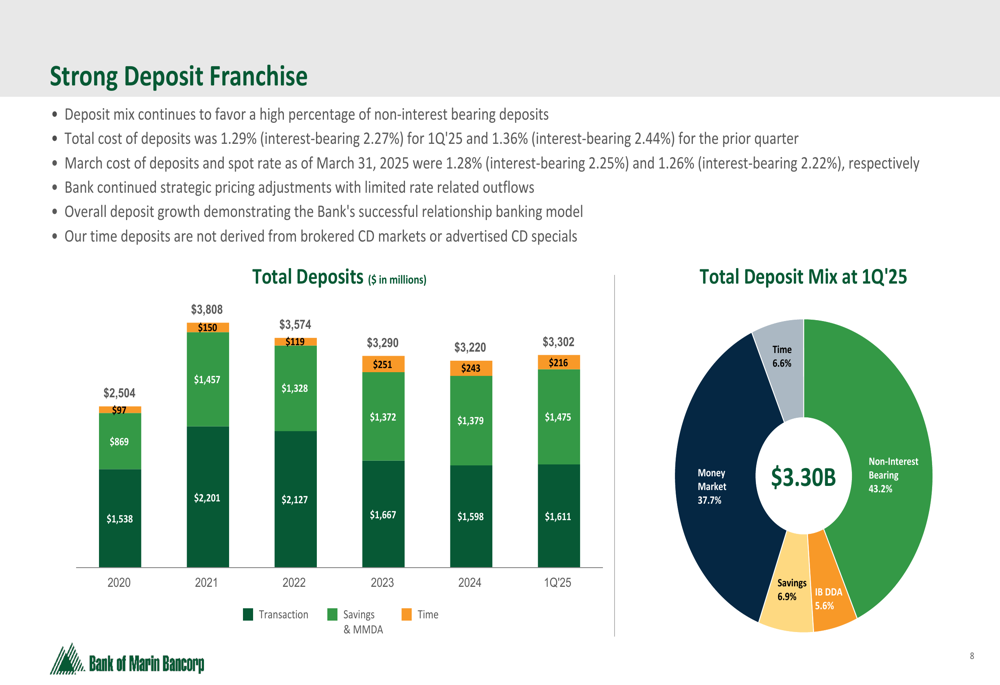

The bank’s deposit franchise continues to show strength, with a favorable mix of account types that helps control funding costs:

The deposit base grew to $3.30 billion, with non-interest bearing deposits comprising 43.2% of the total. This favorable deposit mix has helped the bank maintain a competitive total cost of deposits at 1.29% for the quarter, with interest-bearing deposits costing 2.27%.

Strategic Initiatives

Bank of Marin’s strategic focus centers on relationship banking, disciplined fundamentals, and community commitment. This approach has enabled the bank to maintain a strong deposit franchise while carefully managing its loan portfolio risk.

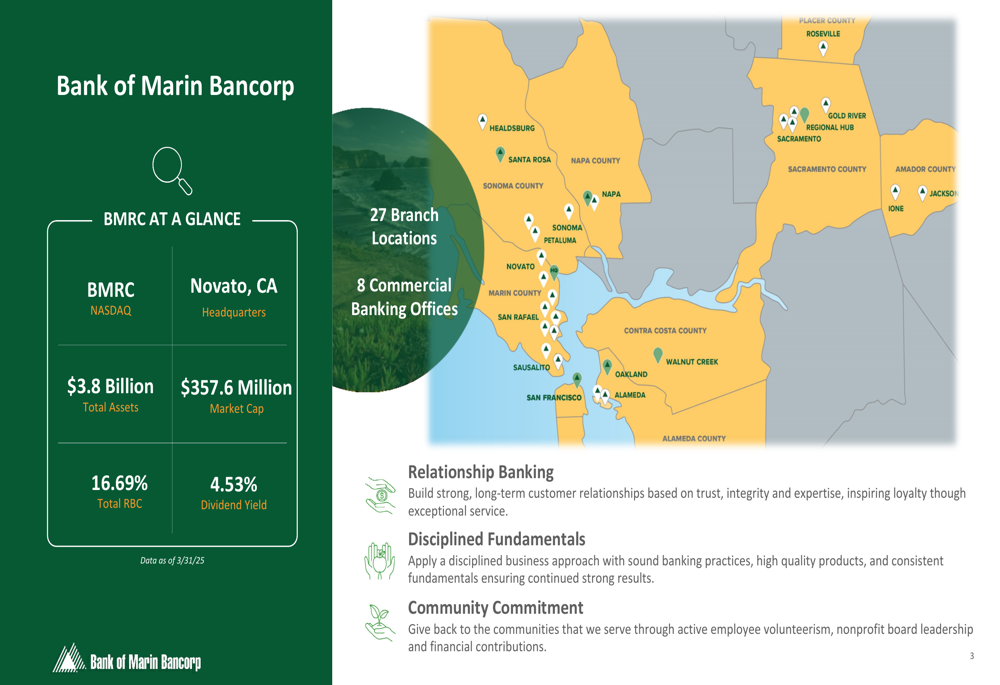

The bank’s branch network spans multiple Northern California counties, providing a solid foundation for relationship-based banking:

The bank’s liquidity position remains exceptionally strong, with $1.9 billion in immediately available net funding, representing 203% of estimated uninsured and uncollateralized deposits. This robust liquidity buffer provides significant protection against potential deposit outflows and enhances the bank’s ability to fund new loans.

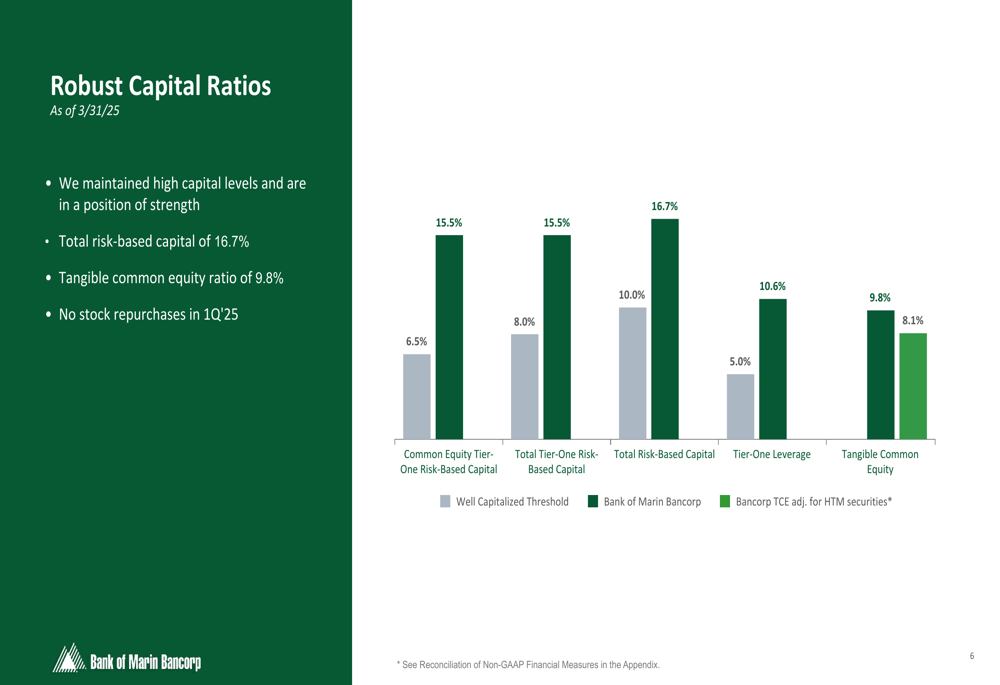

Bank of Marin’s capital position continues to exceed regulatory requirements by a substantial margin:

With a total risk-based capital ratio of 16.7% and a tangible common equity ratio of 9.8%, the bank maintains significant capacity to absorb potential losses and support future growth. No stock repurchases were conducted during the first quarter of 2025.

Forward-Looking Statements

Looking ahead, Bank of Marin is well-positioned for continued growth despite challenges in the banking sector. The bank’s loan portfolio shows low refinance risk through 2026, with maturing loans well-structured to absorb higher rates at maturity or repricing dates.

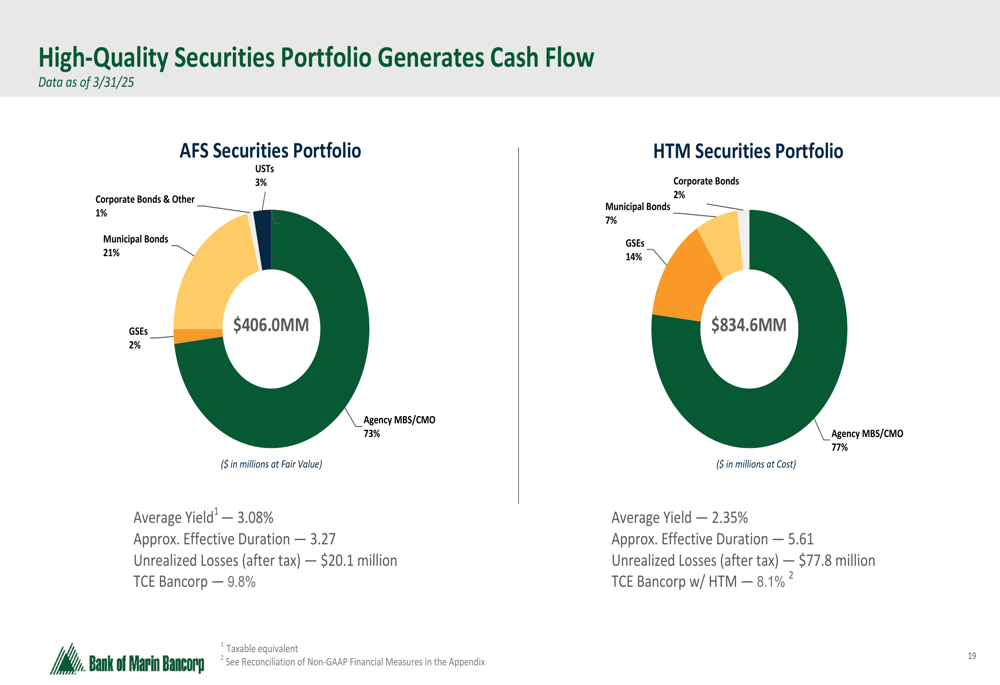

The bank’s securities portfolio is designed to generate consistent cash flow while maintaining high credit quality:

During the earnings call, CEO Tim Myers expressed confidence in the bank’s growth trajectory, noting, "We delivered a solid first quarter driven primarily by positive trends in our net interest margin and deposit growth." He emphasized that these positive trends appear sustainable, supporting the bank’s optimistic outlook.

Management anticipates improved loan growth driven by strategic hiring and maintains a healthy loan pipeline that is 50% higher than the previous year. The bank plans to continue focusing on expense management while maintaining its disciplined approach to lending and deposit gathering.

While economic uncertainty could impact loan demand and growth, Bank of Marin’s strong capital position, robust liquidity, and diversified loan portfolio provide a solid foundation for navigating potential challenges in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.