U.S. stocks mixed ahead of Fed decision; General Mills retreatseyed

Introduction & Market Context

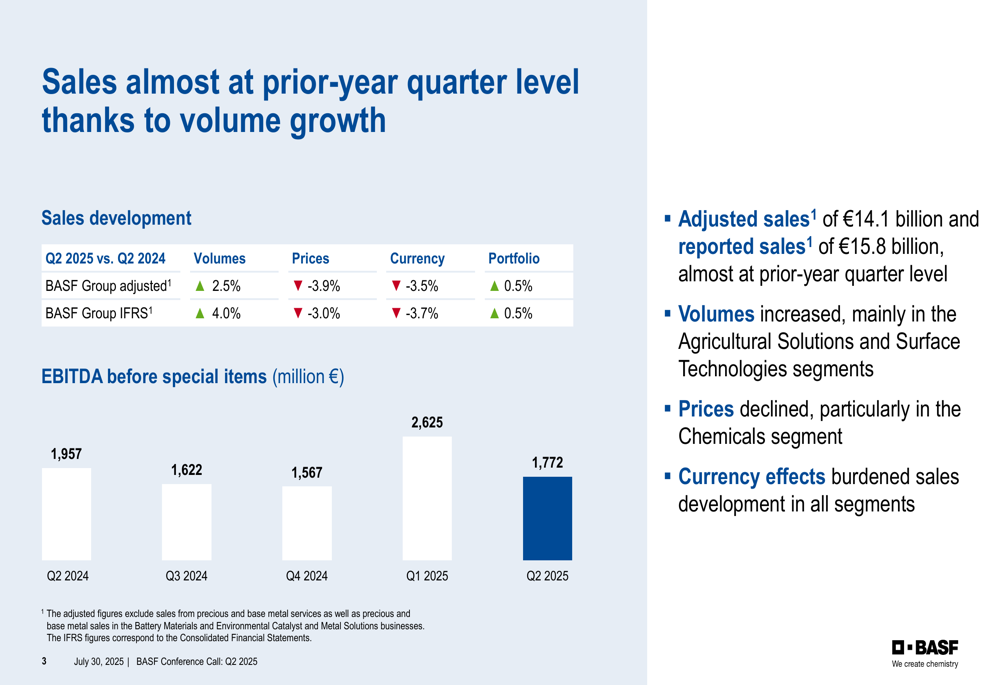

BASF SE (OTC:BASFY) (ETR:BAS) presented its second quarter 2025 results on July 30, revealing a mixed performance across its business segments and a downward revision of its full-year outlook. The German chemical giant reported Q2 sales of €15.8 billion, nearly matching prior-year levels, while EBITDA before special items declined by 9.4% year-over-year to €1.8 billion.

The results show some recovery from the challenging first quarter, when net income plummeted to just €8 million. However, the overall first-half performance remains significantly below 2024 levels, prompting the company to lower its full-year guidance amid persistent headwinds in the chemical industry.

As shown in the following chart, BASF’s quarterly EBITDA before special items has fluctuated significantly over the past year, with Q2 2025 showing a sequential improvement from Q1 but remaining below the prior-year quarter:

Quarterly Performance Highlights

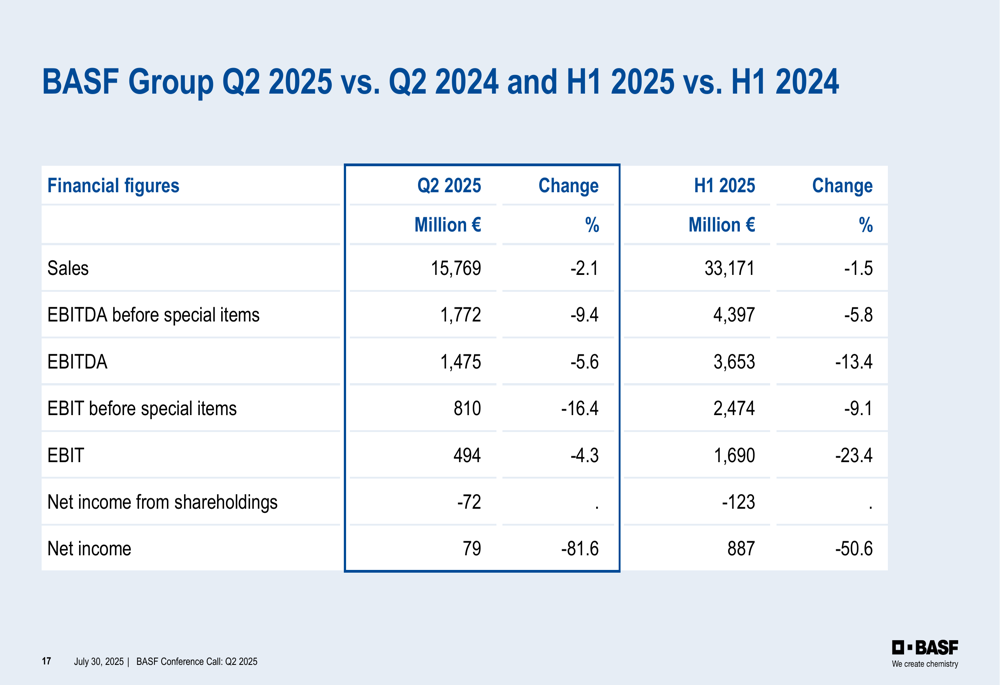

BASF reported Q2 2025 sales of €15.8 billion, representing a slight decrease of 2.1% compared to Q2 2024. While volumes increased by 2.5% (adjusted basis), this was offset by price declines of 3.9% and negative currency effects of 3.5%. Net income fell dramatically by 81.6% to €79 million, reflecting ongoing profitability challenges.

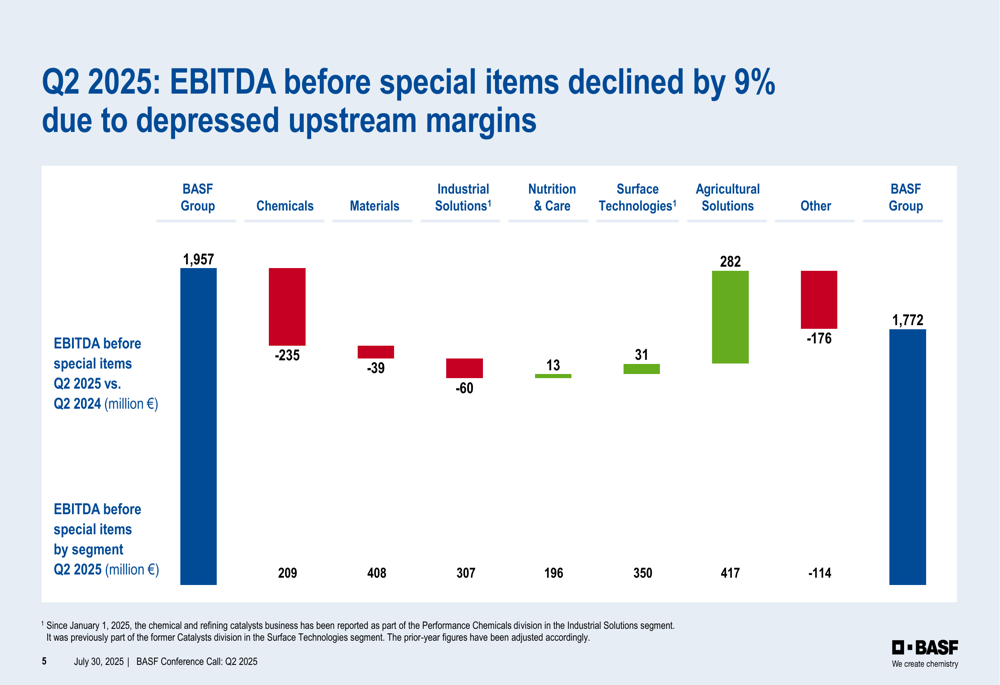

The company’s EBITDA bridge reveals significant divergence across segments, with Agricultural Solutions and Surface Technologies delivering strong year-over-year improvements, while the Chemicals segment experienced a substantial decline:

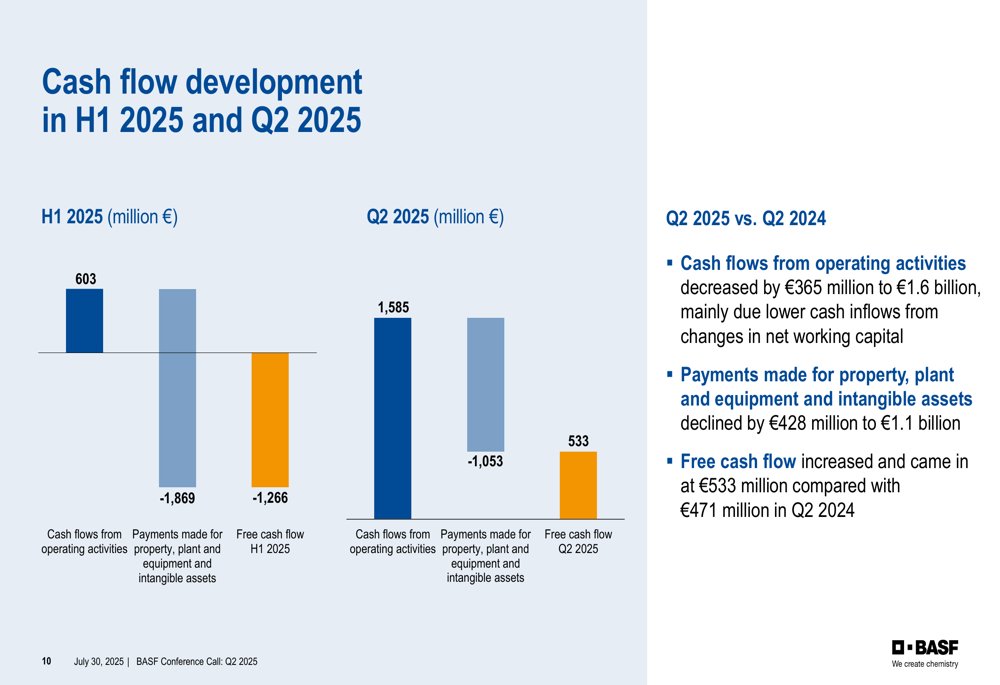

Free cash flow showed improvement in Q2 2025, reaching €533 million compared to €471 million in the same period last year. This positive development came despite lower cash flows from operating activities, as the company reduced its capital expenditures.

The following table provides a comprehensive overview of BASF’s financial performance for Q2 and H1 2025 compared to the prior year:

Segment Performance Analysis

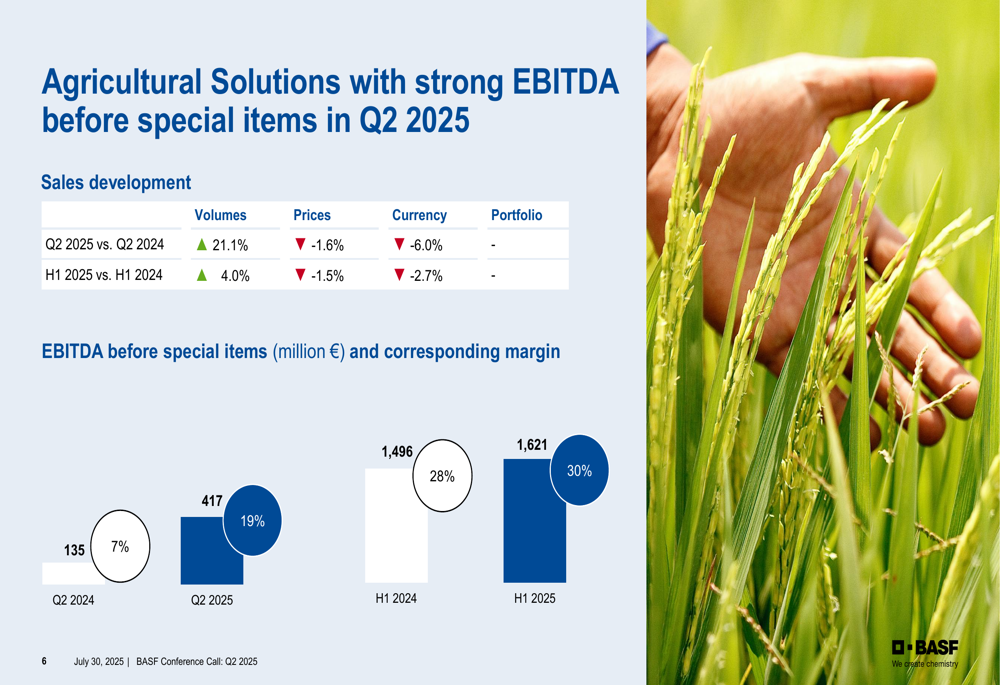

The Agricultural Solutions segment emerged as a standout performer in Q2 2025, with EBITDA before special items surging to €417 million from €135 million in Q2 2024. This impressive 209% increase was driven by strong volume growth of 21.1%, which more than offset price declines and negative currency effects.

As shown in the following chart, the segment’s EBITDA margin improved significantly to 19% in Q2 2025, up from 7% in the prior-year quarter:

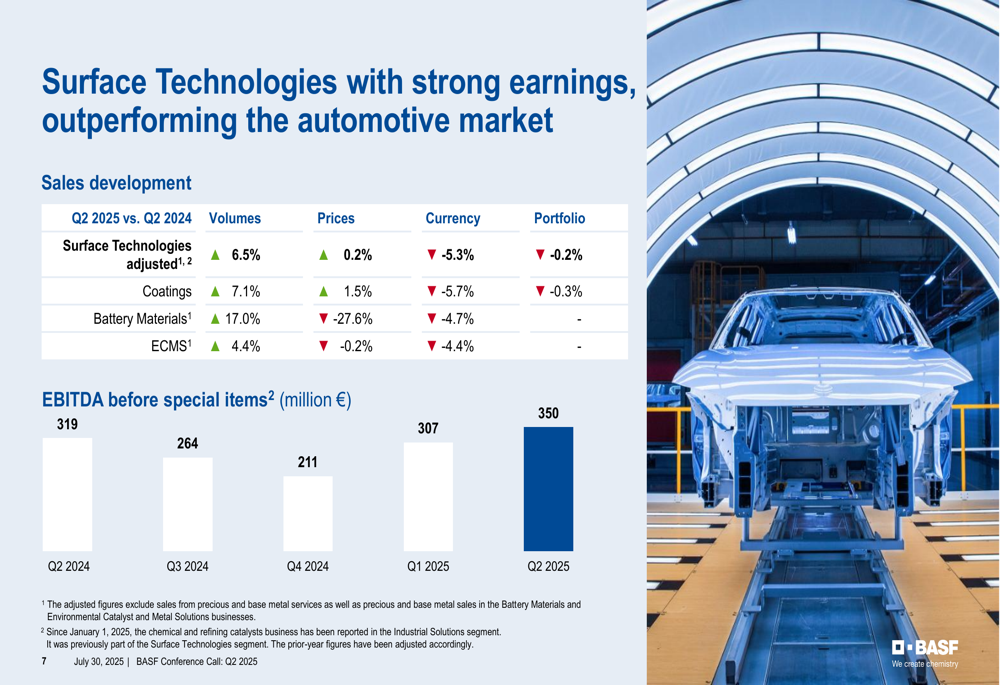

The Surface Technologies segment also delivered solid results, with EBITDA before special items increasing to €350 million from €319 million in Q2 2024. Volume growth of 6.5% was the primary driver, particularly in the Battery Materials business which saw volumes rise by 17.0%.

In contrast, the Chemicals segment faced significant headwinds, with EBITDA before special items declining to €209 million from €444 million in Q2 2024. This 53% decrease was primarily due to price pressure, with prices falling by 12.4% year-over-year amid challenging market conditions.

Strategic Initiatives & Portfolio Management

BASF outlined several strategic initiatives aimed at strengthening its financial position and optimizing its business portfolio. The company is accelerating its cost savings programs to generate €1.6 billion in annual savings by year-end 2025 (previously €1.5 billion) and is on track to reach €2.1 billion by year-end 2026.

Capital expenditure is being reduced, with 2025 payments for property, plant and equipment expected to be €200 million lower than forecasted in February. From 2026 onward, capex is expected to fall below depreciation levels.

The company’s active portfolio management includes:

Additionally, BASF has secured its natural gas supply in Europe through long-term contracts with Equinor and Cheniere, ensuring competitive terms and supply security while diversifying its energy sources.

The following slide highlights the company’s cash flow development in H1 2025, reflecting the ongoing balance between operational needs and strategic investments:

Revised Outlook & Forward-Looking Statements

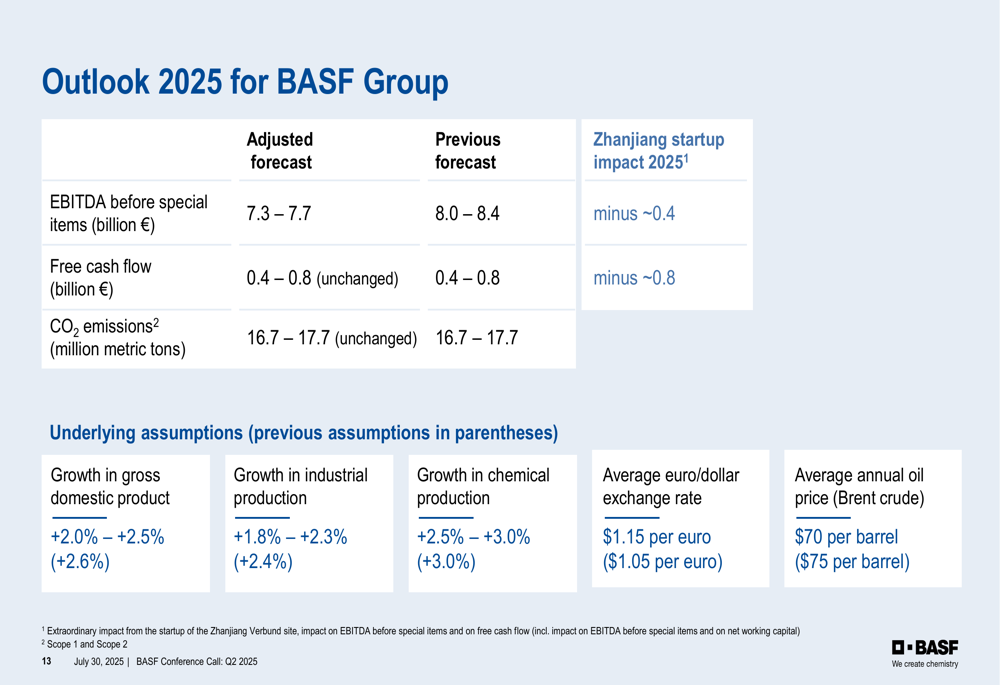

BASF has revised its full-year 2025 outlook, lowering its EBITDA before special items guidance to €7.3-7.7 billion from the previous forecast of €8.0-8.4 billion. This reduction primarily reflects the impact of the Zhanjiang Verbund (VIE:VERB) site startup, which is expected to reduce EBITDA by approximately €0.4 billion in 2025.

The company maintained its free cash flow guidance of €0.4-0.8 billion for 2025, despite the Zhanjiang startup impact of approximately €0.8 billion. BASF also adjusted its underlying economic assumptions, including lower GDP and industrial production growth forecasts:

BASF’s management emphasized its commitment to maintaining the company’s single A credit rating, described as "best in class in the chemical industry," through debt reduction and lowering its leverage ratio. The company is focusing on its "Winning Ways" strategy, which combines portfolio optimization, structural cost reduction, and cultural transformation to enhance long-term value creation.

Despite the challenging environment, BASF’s Q2 results show some signs of stabilization compared to Q1 2025, with improvements in free cash flow and strong performance in key segments like Agricultural Solutions and Surface Technologies. However, the downward revision of full-year guidance underscores the persistent challenges facing the chemical industry and the company’s ongoing transformation efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.