Palantir shares slip premarket despite posting record revenue in third quarter

Introduction & Market Context

Banco Bilbao Viscaya Argentaria SA (NYSE:BBVA) released its third-quarter 2025 earnings presentation on October 30, revealing mixed results that fell short of analyst expectations despite showing strong underlying business growth. The Spanish banking giant reported earnings per share of €0.42, missing forecasts of $0.53, which contributed to a 2.56% decline in pre-market trading with shares priced at $19.78.

The earnings miss comes despite BBVA maintaining solid growth in core revenues and improving efficiency metrics, highlighting the gap between the company’s operational achievements and market expectations. The bank’s stock had performed exceptionally well prior to this report, with year-to-date returns exceeding 115% according to available data.

Quarterly Performance Highlights

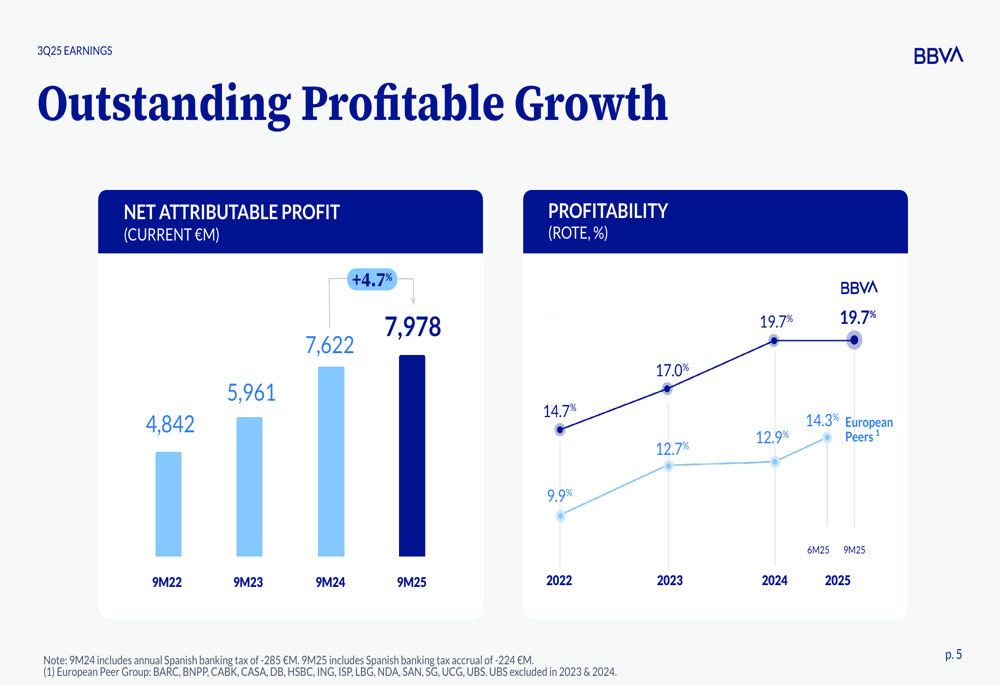

BBVA reported a net attributable profit of €2,531 million for Q3 2025, representing a 3.7% decrease from the previous quarter and an 8.0% decline year-over-year. This contributed to a cumulative profit of €7,978 million for the first nine months of 2025, still showing a 4.7% increase compared to the same period in 2024.

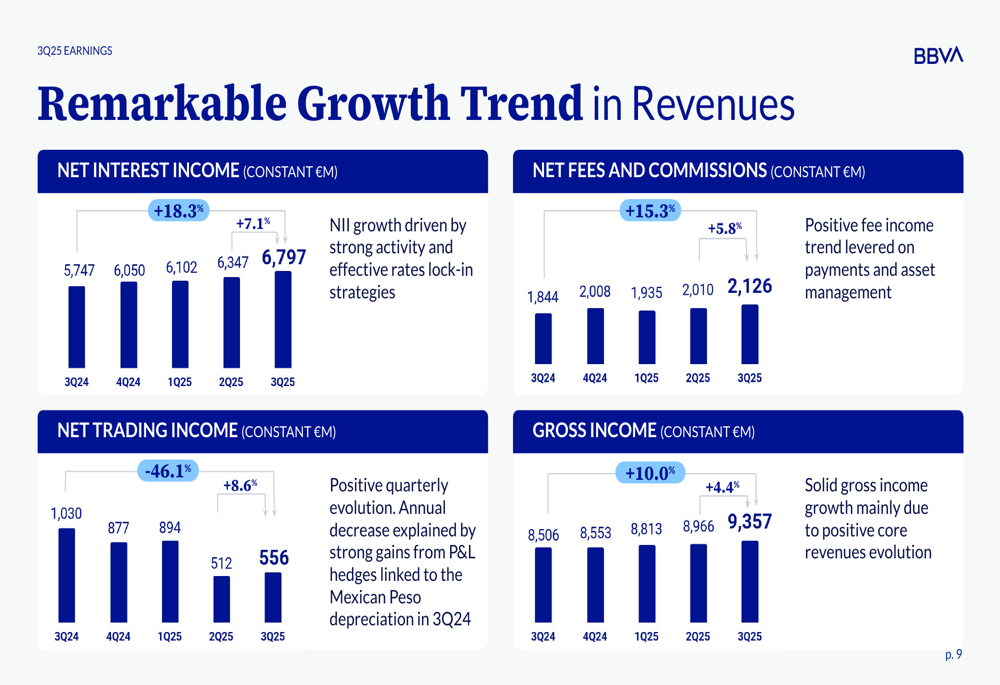

The bank’s core revenues showed remarkable growth, with net interest income reaching €6,640 million, up 18.3% year-over-year in constant currency terms. Net fees and commissions also performed strongly at €2,060 million, representing a 15.3% increase compared to Q3 2024.

As shown in the following chart of revenue growth trends, BBVA has maintained consistent growth across its key revenue streams:

The bank’s profitability metrics remained strong despite the quarterly decline, with Return on Tangible Equity (ROTE) at 19.7% for the first nine months of 2025, significantly outperforming European peers who averaged 14.3%. Return on Equity (ROE) stood at 18.8%, slightly down from 19.2% in the same period of 2024.

The following slide illustrates BBVA’s value creation and profitability compared to peers:

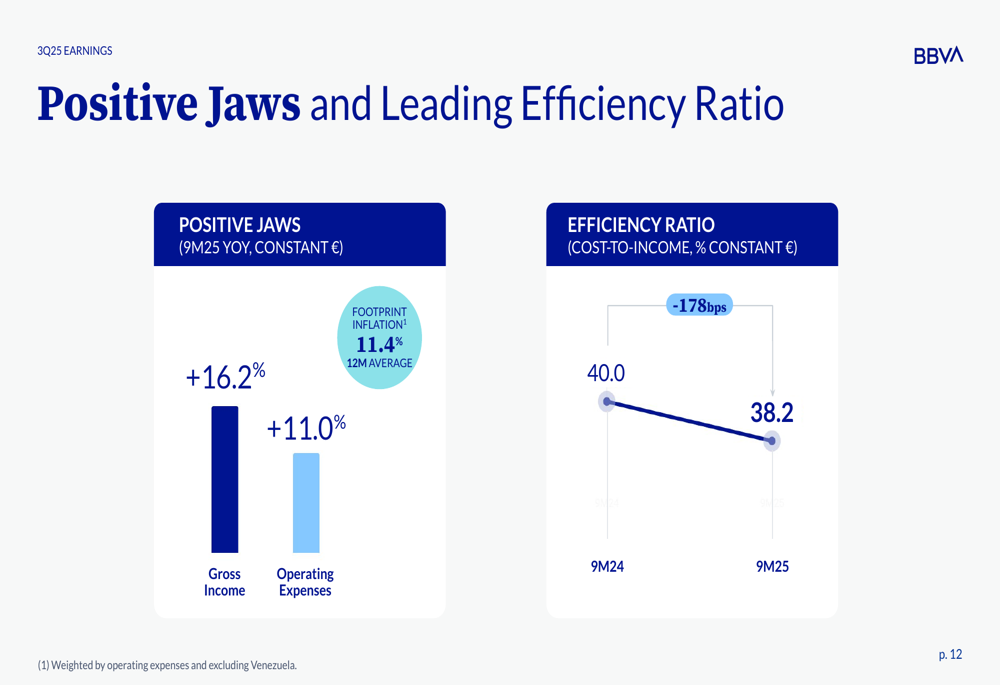

BBVA’s efficiency ratio improved to 38.2% for 9M25 from 40.0% in 9M24, demonstrating the bank’s ability to grow revenues faster than expenses. This "positive jaws" effect is illustrated in the following chart:

Asset Quality and Capital Position

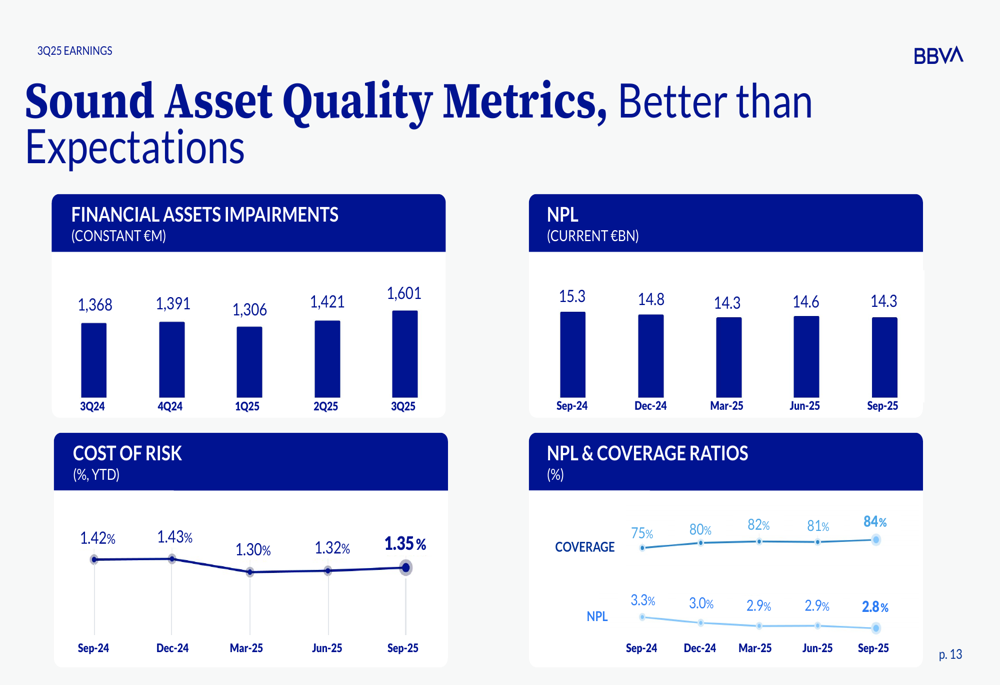

The bank maintained sound asset quality metrics with a cost of risk of 1.35% for 9M25, which management noted was better than expectations. The non-performing loan (NPL) ratio improved to 2.8% as of September 2025, down from 3.3% a year earlier, while the coverage ratio strengthened to 84% from 75%.

The following slide details these asset quality improvements:

BBVA’s capital position remained solid with a CET1 ratio of 13.42% as of September 2025, an 8 basis point improvement from June 2025. This capital level comfortably exceeds the bank’s target range of 11.5%-12.0% and the regulatory requirement of 9.13%.

The strong capital position has enabled BBVA to announce significant shareholder returns, including a share buyback program of approximately €1 billion starting October 31, and a record interim dividend of 32 euro cents per share payable on November 7. The bank also indicated plans for an additional significant share buyback program pending approval.

As illustrated in the following slide, BBVA’s capital position supports its shareholder remuneration strategy:

Strategic Initiatives

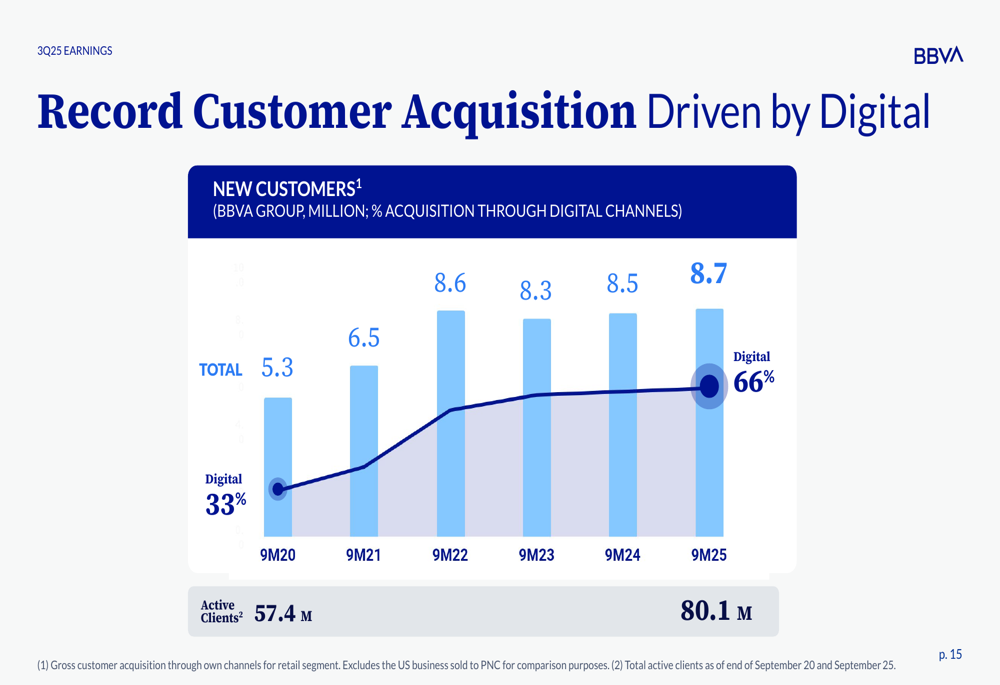

BBVA continues to focus on digital transformation, with 66% of new customer acquisition now coming through digital channels, up from 33% in 9M20. The bank added 8.7 million new customers in the first nine months of 2025, bringing its total active client base to 80.1 million, up from 57.4 million in 9M20.

The following chart demonstrates this digital-driven customer acquisition trend:

Sustainability remains another strategic priority, with sustainable finance volumes reaching €97 billion in 9M25, up from €66 billion in 9M24. The bank has set an ambitious target of €700 billion in sustainable business for 2025-2029.

This sustainability focus is illustrated in the following slide:

Regional Performance

BBVA’s performance varied significantly across its geographic footprint. Turkey emerged as the standout performer with net attributable profit up 187.7% year-over-year to €236 million, driven by net interest income growth of 159.4%. However, this comes against a backdrop of high inflation and interest rates in the country.

Mexico, BBVA’s largest market outside Spain, delivered a modest 1.0% increase in net attributable profit to €1,296 million, with lending up 9.8% and customer funds up 13.7%.

Spain, the bank’s home market, faced challenges with net attributable profit declining 7.2% year-over-year to €994 million, despite lending growth of 7.8% and customer funds growth of 6.7%.

South America and Rest of Business areas showed positive growth, with net attributable profits increasing 5.8% and 5.6% year-over-year, respectively.

Forward-Looking Statements

BBVA outlined ambitious financial goals for 2025-2028, including:

- ROTE of approximately 22% on average

- Tangible book value plus dividends per share growth at mid-teens CAGR

- Cost-to-income ratio of approximately 35%

- Cumulative net attributable profit of approximately €48 billion

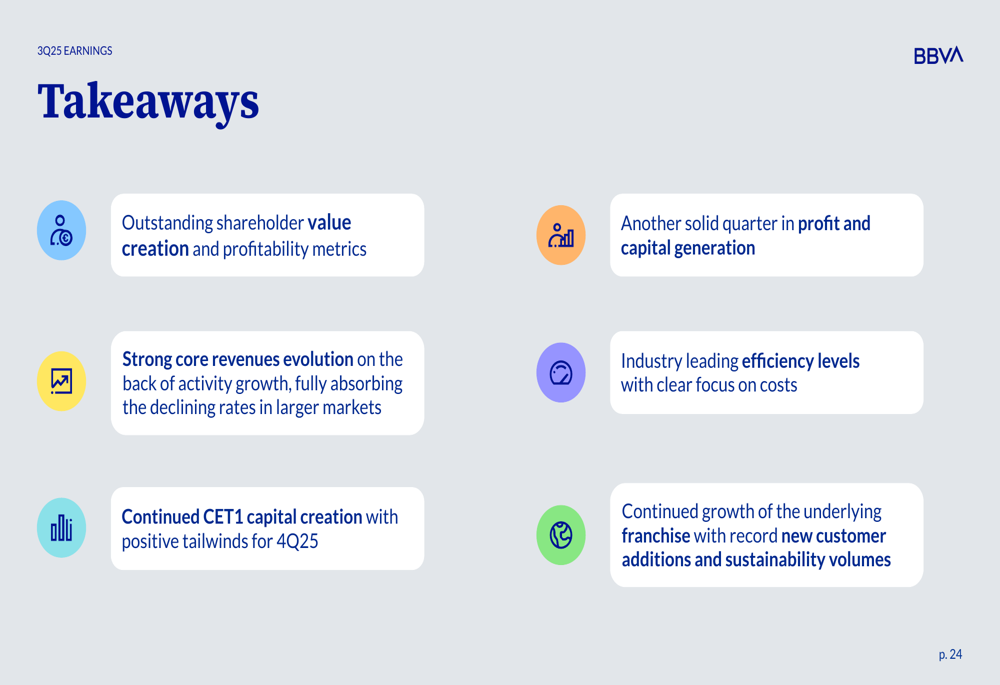

The bank’s key takeaways from the presentation are summarized in the following slide:

CEO Onur Genç expressed satisfaction with the company’s quarterly performance during the earnings call, stating, "We are once again very happy with the performance in the quarter, especially the quarterly core revenue evolution." He emphasized BBVA’s commitment to profitable growth and market share gains.

However, the bank faces several challenges, including macroeconomic pressures in key markets, competition from neobanks in the digital space, and potential regulatory hurdles regarding capital distribution strategies. Economic slowdowns in markets like Mexico, where GDP growth forecasts have been revised downward, could also impact future revenue growth.

Despite these challenges and the current earnings miss, BBVA’s strong capital position, improving efficiency, and strategic focus on digital transformation and sustainability position the bank to potentially overcome short-term market disappointments and deliver on its long-term financial goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.