Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Becton Dickinson and Company (NYSE:BDX) shares fell over 5% in premarket trading following the release of its Q2 FY25 earnings presentation on May 1, 2025, which revealed mixed results characterized by strong margin expansion but slowing organic growth, prompting the company to lower its full-year guidance.

Quarterly Performance Highlights

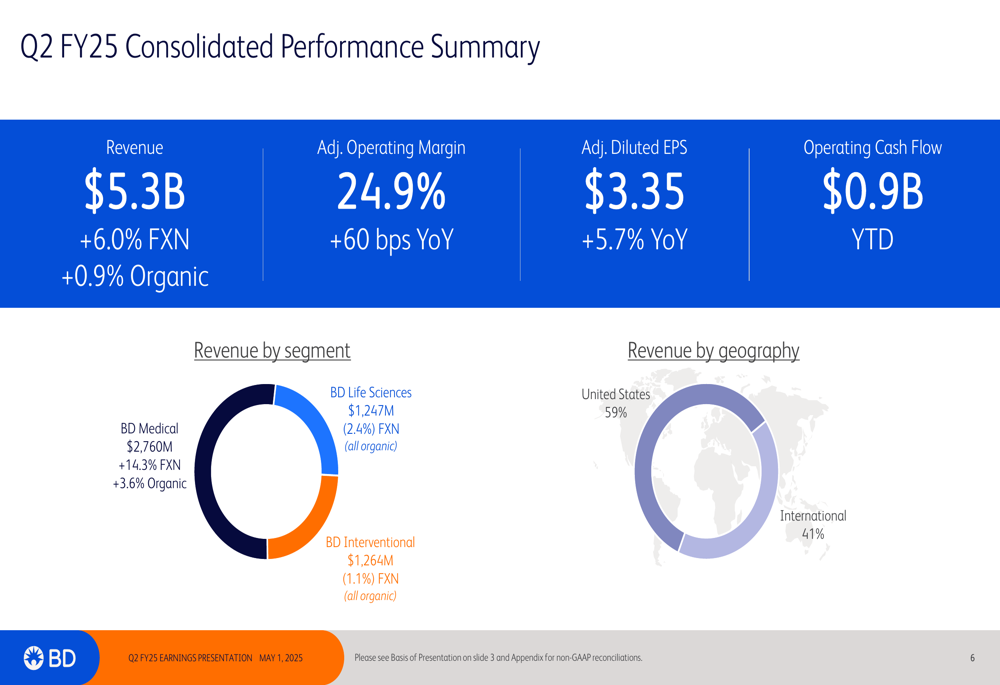

BD reported Q2 FY25 revenue of $5.3 billion, representing 6.0% growth on a foreign-exchange neutral (FXN) basis but only 0.9% organic growth. Despite the growth challenges, the company exceeded earnings expectations through significant margin improvement, with adjusted operating margin expanding 60 basis points year-over-year to 24.9% and adjusted diluted EPS increasing 5.7% to $3.35.

"Our BD Excellence operating system is driving continued margin expansion and increasing investment in our commercial organization and innovation, and we believe we are well positioned to accelerate growth as markets recover," said Tom Polen, BD Chairman, CEO, and President, in the earnings presentation.

The company’s performance varied significantly across its three main segments. BD Medical (TASE:BLWV) led with strong results, generating $2.76 billion in revenue (+14.3% FXN, +3.6% organic), while both BD Life Sciences and BD Interventional experienced declines of 2.4% and 1.1% FXN, respectively. Geographically, 59% of revenue came from the United States, with the remaining 41% from international markets.

Detailed Financial Analysis

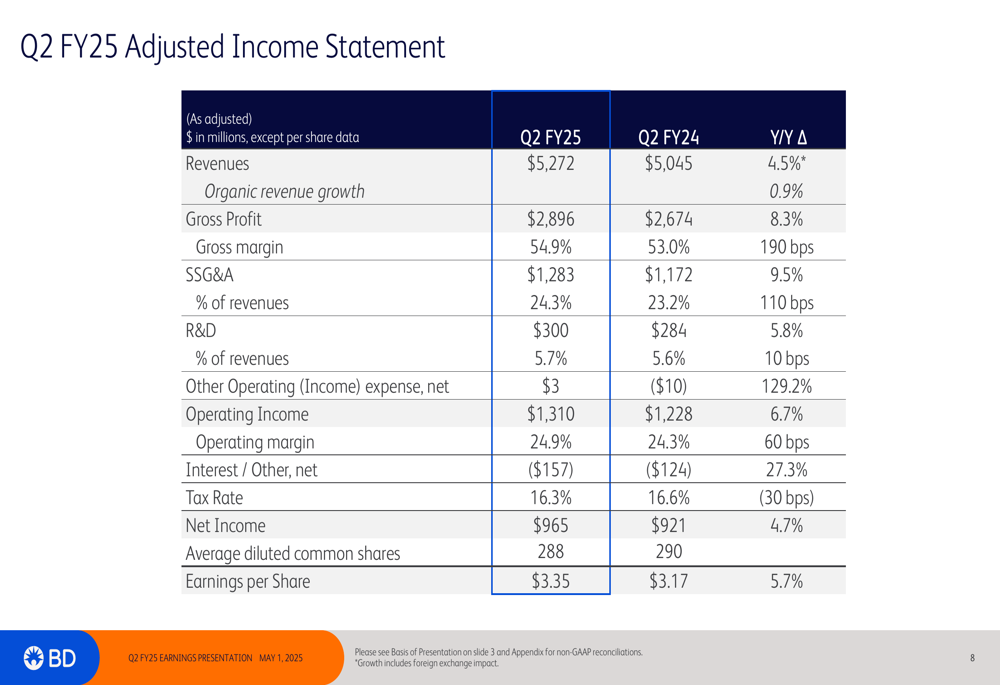

BD’s adjusted income statement for Q2 FY25 showed impressive margin expansion, with gross margin improving 190 basis points year-over-year to 54.9%. This improvement helped offset increased spending in selling, general and administrative expenses (SSG&A), which rose 9.5% compared to the prior year. Research and development expenses increased 5.8% to $300 million, reflecting the company’s continued investment in innovation.

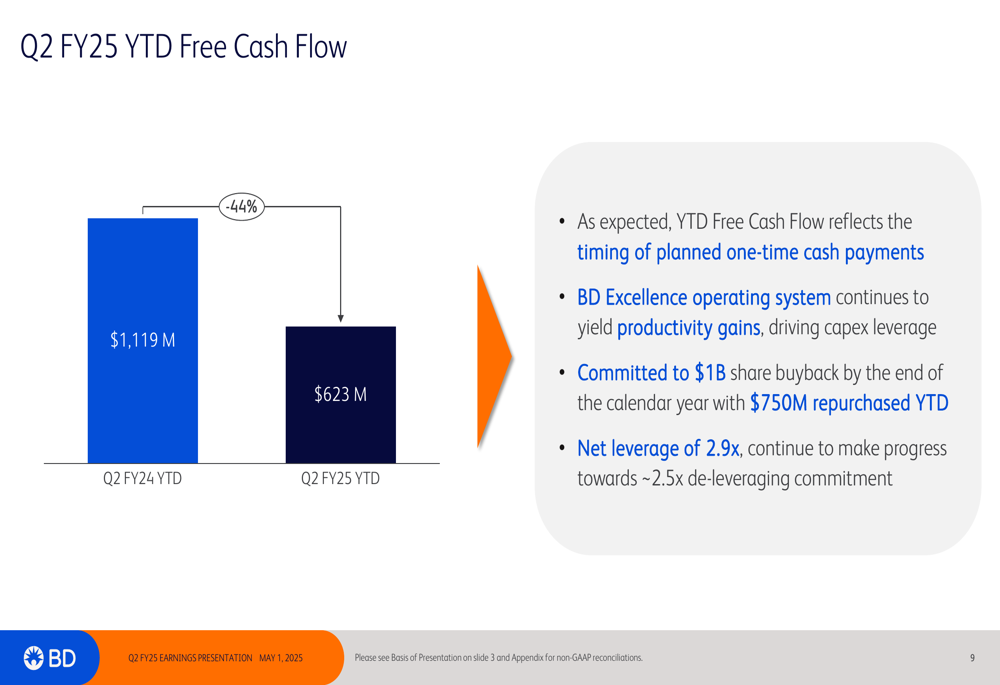

Free cash flow generation has been a challenge, with year-to-date free cash flow of $623 million representing a 44% decline compared to the same period in FY24. The company attributed this decline to "the timing of planned one-time cash payments." Despite this, BD has continued its share repurchase program, with $750 million repurchased year-to-date toward its commitment of $1 billion by the end of the calendar year. The company’s net leverage stands at 2.9x, as it progresses toward its de-leveraging target of approximately 2.5x.

Strategic Initiatives

BD highlighted several strategic initiatives in its presentation, including the advancement of its plan to separate the Biosciences and Diagnostics business, which the company expects will "unlock compelling value." The company is also navigating tariff impacts through advanced supply chain capabilities and regionalized manufacturing.

The presentation showcased BD’s strong pipeline progression, featuring key product launches across multiple areas. These include the Phasix™ ST Umbilical Hernia Patch in Advanced Tissue Regeneration, the BD Alaris™ Infusion System (which received 510(k) clearance) and the BD Alaris™ neXus Infusion System (launched in EMEA) in infusion pump technologies, and the BD FACSDiscover™ A8 Cell Analyzer (on track for Q3 FY25 launch) in lab productivity.

The company’s innovation pipeline aims to deliver over 100 new product launches by FY25, with recent innovations driving growth including the BD Alaris™ Infusion System, HemoSphere Alta™ Swan IQ™ and ForeSight IQ™ Smart Sensors, and Site-Rite™ 9 Ultrasound. Near and mid-term catalysts include the BD Alaris™ neXus Infusion System, BD Libertas™ 5mL, and CentroVena One™.

Forward-Looking Statements

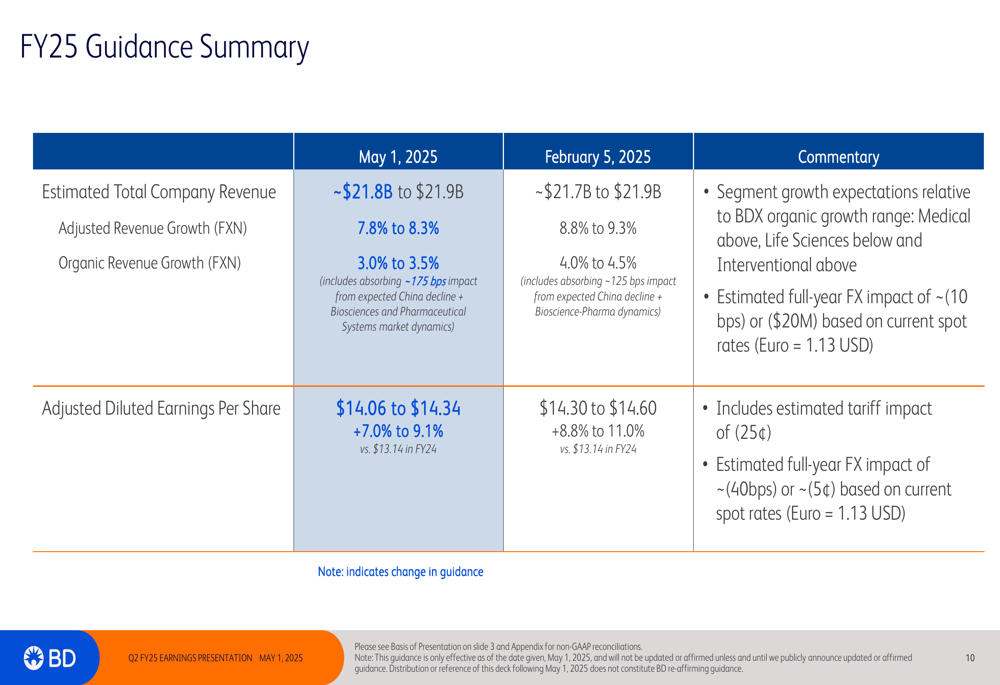

In response to the challenging operating environment, BD revised its FY25 guidance downward. The company now expects organic revenue growth of 3.0% to 3.5%, down from the previous guidance of 4.0% to 4.5%. Adjusted diluted EPS is now projected to be between $14.06 and $14.34, compared to the previous range of $14.30 to $14.60.

The lowered guidance reflects several factors, including the impact of tariffs and a difficult operating environment. However, the adjusted EPS guidance still represents approximately 8% growth at the mid-point, inclusive of tariff impact, highlighting the company’s ability to drive earnings growth through margin expansion despite top-line challenges.

This guidance revision marks a shift from the company’s previous outlook. In its Q3 FY24 earnings call, BD had expressed confidence in achieving 10% EPS growth in fiscal year 2025, but the current guidance suggests more modest growth.

Despite the near-term challenges, BD remains committed to its long-term strategic initiatives, including its BD Excellence operating system, which continues to drive productivity gains and capital expenditure leverage. The company also highlighted its sustainability efforts, noting its inclusion on Newsweek’s Most Trustworthy Company list and recognition as one of America’s Climate Leaders by USA TODAY in 2025.

As BD navigates the current challenging environment, investors will be watching closely to see if the company can maintain its margin expansion while returning to stronger organic growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.