Trump to appeal tariff ruling, warns of economic consequences

Introduction & Market Context

Bentley Systems (NASDAQ:BSY) presented its second quarter 2025 results on August 6, 2025, highlighting continued growth in its infrastructure engineering software business. The company reported total revenue of $364 million, representing a 9% year-over-year increase (10% in constant currency), driven primarily by strong subscription revenue.

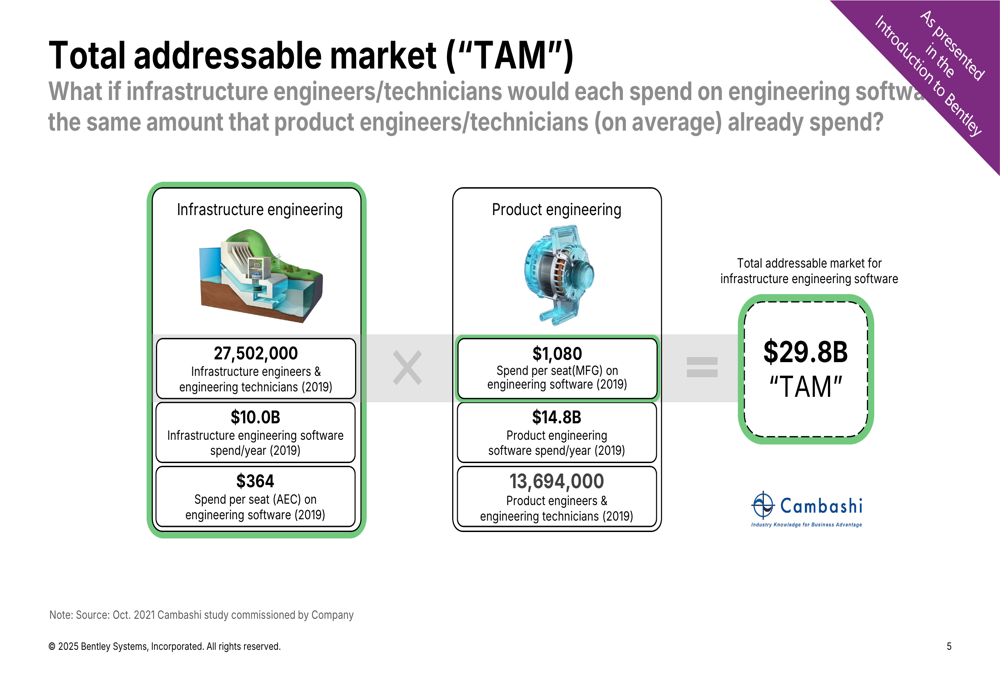

The infrastructure engineering software market continues to expand, with Bentley estimating a Total (EPA:TTEF) Addressable Market (TAM) of $29.8 billion. According to data presented, infrastructure engineering software spending has grown at a 10% CAGR from 2019 to 2023, with spending per engineer increasing at a 9% CAGR during the same period.

As shown in the following chart, the infrastructure engineering market represents a significant opportunity with 27.5 million engineers/technicians compared to 13.7 million in product engineering, though spending per seat remains lower at $364 versus $1,080:

Quarterly Performance Highlights

Bentley’s Q2 2025 performance was anchored by subscription revenue of $333 million, which increased 11% year-over-year (12% in constant currency) and accounted for approximately 91% of total revenue. This represents a slight sequential decline from the $371 million in total revenue reported in Q1 2025.

For the first half of 2025, the company reported:

- Total revenue of $735 million, up 10% year-over-year

- Subscription revenue of $676 million, up 12% year-over-year

- License revenue of $38 million, down 12% year-over-year

- Services revenue of $21 million, up 3% year-over-year

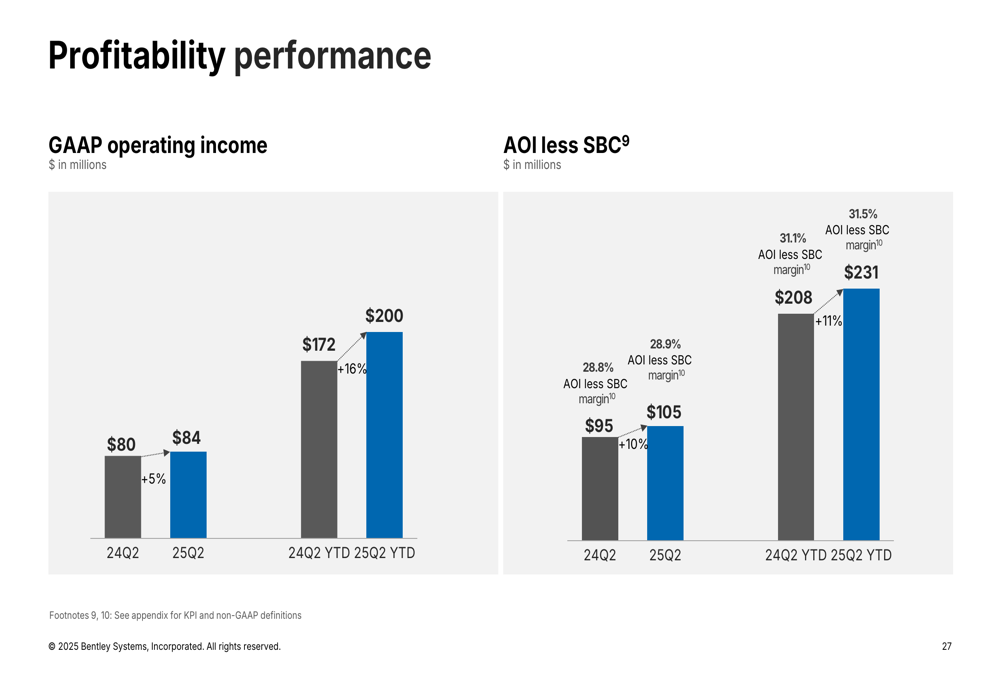

The company’s profitability metrics remained solid, with GAAP operating income of $84 million (up 5% year-over-year) and Adjusted Operating Income less Stock-Based Compensation (AOI less SBC) of $105 million (up 10% year-over-year) for Q2 2025.

The following chart illustrates Bentley’s profitability performance for both Q2 and the first half of 2025:

Recurring Revenue and ARR Growth

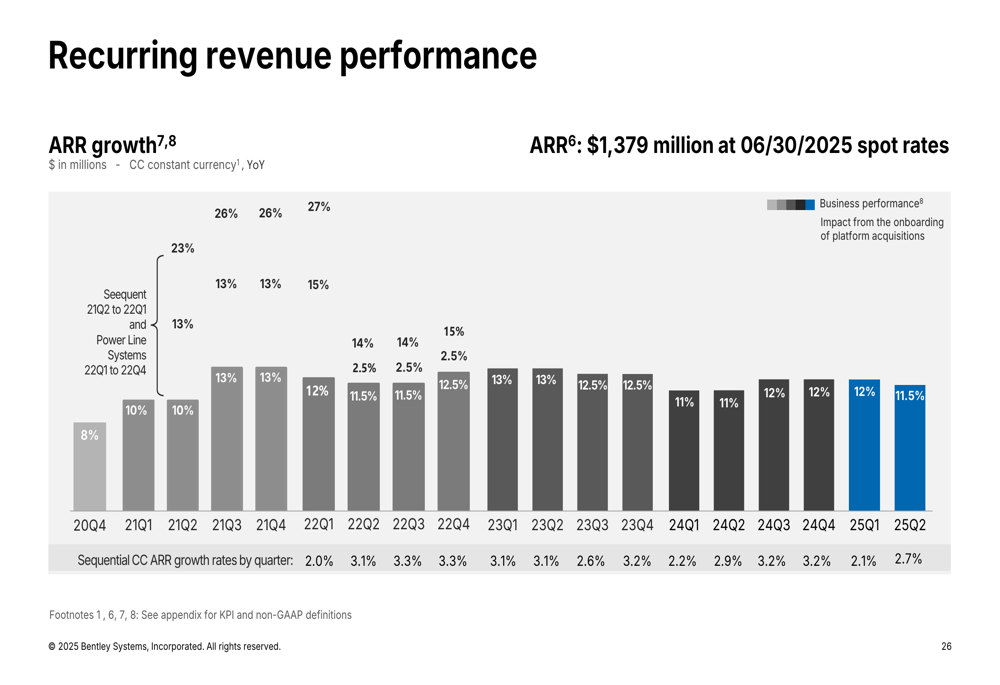

Annual Recurring Revenue (ARR) reached $1,379 million as of June 30, 2025, with the company maintaining double-digit ARR growth. However, the growth rate has moderated slightly compared to previous quarters, with the 2025 outlook projected at 10.5%-12.5%.

Bentley continues to demonstrate strong recurring revenue retention, with a rate of 109% for Q2 2025 and an account retention rate (dollar-weighted) of 99%, reflecting the company’s stable customer base.

The following chart shows Bentley’s ARR growth trend over time, highlighting both business performance and the impact of platform acquisitions:

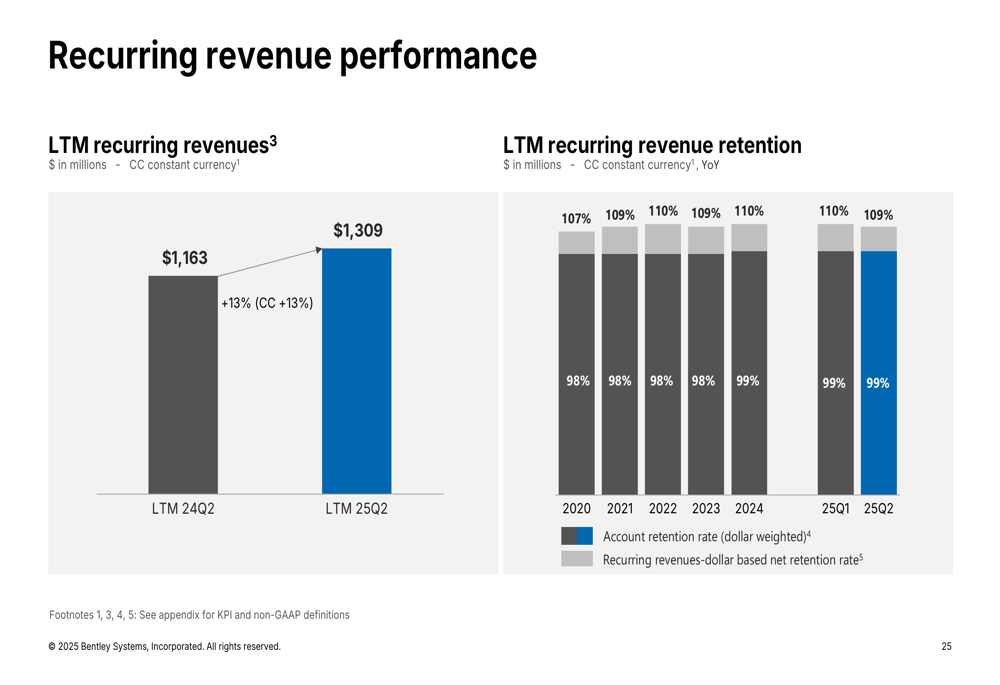

Last twelve months (LTM) recurring revenue increased to $1,309 million, representing a 13% growth year-over-year both on a reported and constant currency basis:

Business Segment Analysis

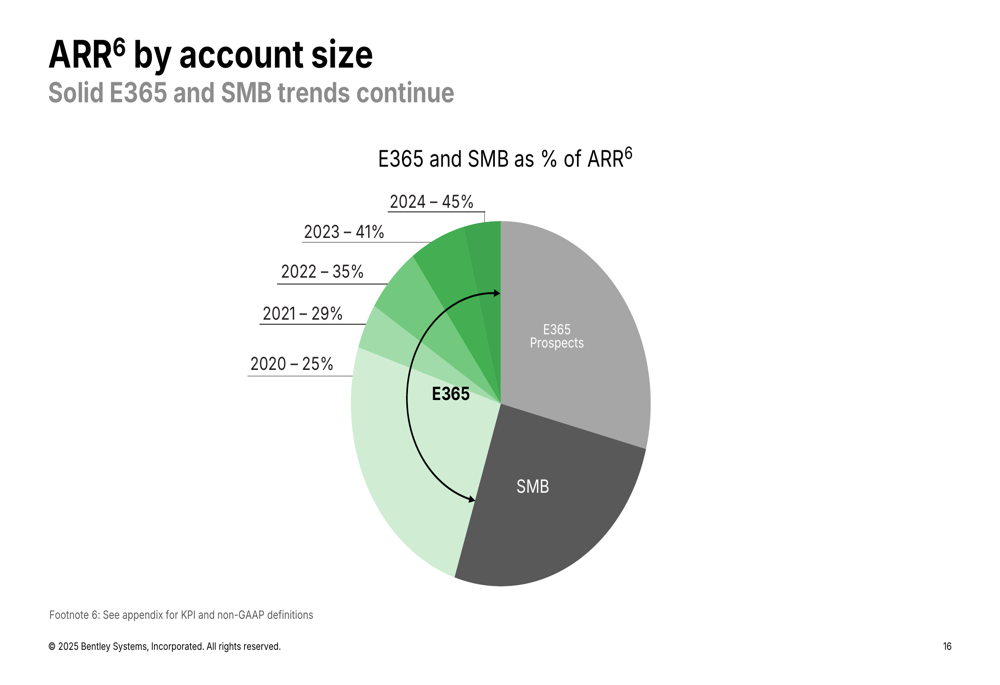

Bentley is seeing increasing contributions from Enterprise 365 (E365) and Small and Medium Business (SMB) accounts, which now constitute 45% of ARR, up from 41% in 2023 and 25% in 2020. This trend indicates the company’s successful expansion beyond its traditional large enterprise customer base.

As illustrated in the following chart, E365 and SMB accounts are becoming increasingly important to Bentley’s revenue mix:

From a sector perspective, Resources emerged as the fastest-growing infrastructure sector, while Public Works/Utilities showed solid performance in Q2. Geographically, the company reported favorable signals for longer-term U.S. infrastructure spending, continued strength in Latin America, a favorable EU budget proposal, growth in the Middle East, and standout performance in India.

Competitive Industry Position

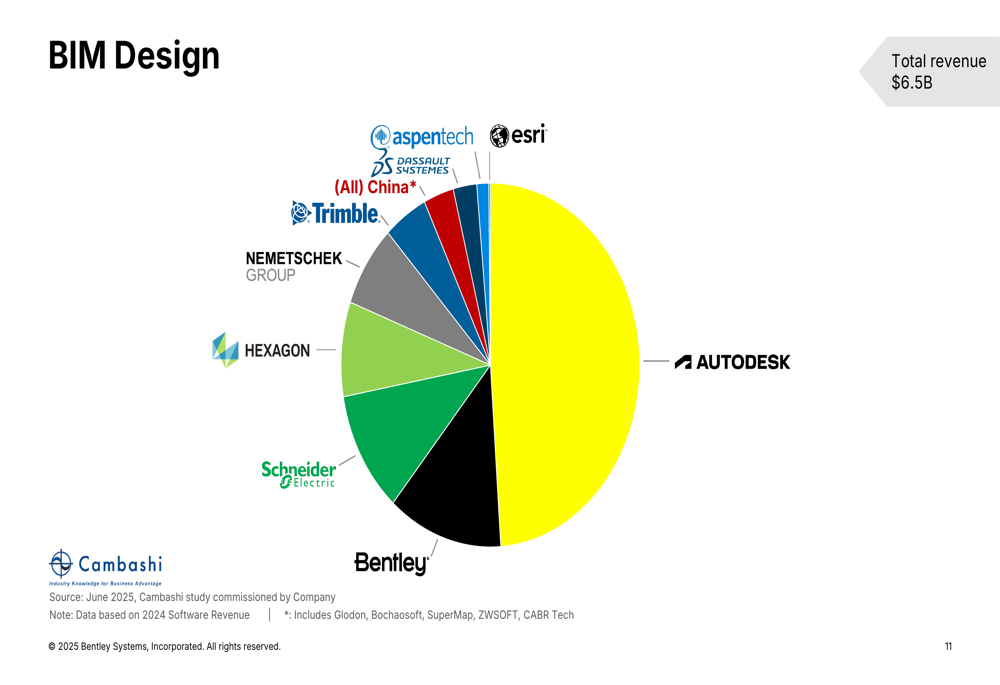

In the infrastructure engineering software market, Bentley maintains a strong competitive position alongside Autodesk (NASDAQ:ADSK). The BIM (Building Information Modeling) Design market, valued at $6.5 billion, shows Autodesk as the market leader, with Bentley holding a significant share particularly in civil, structural, and plant disciplines.

The following chart illustrates Bentley’s position in the BIM Design market:

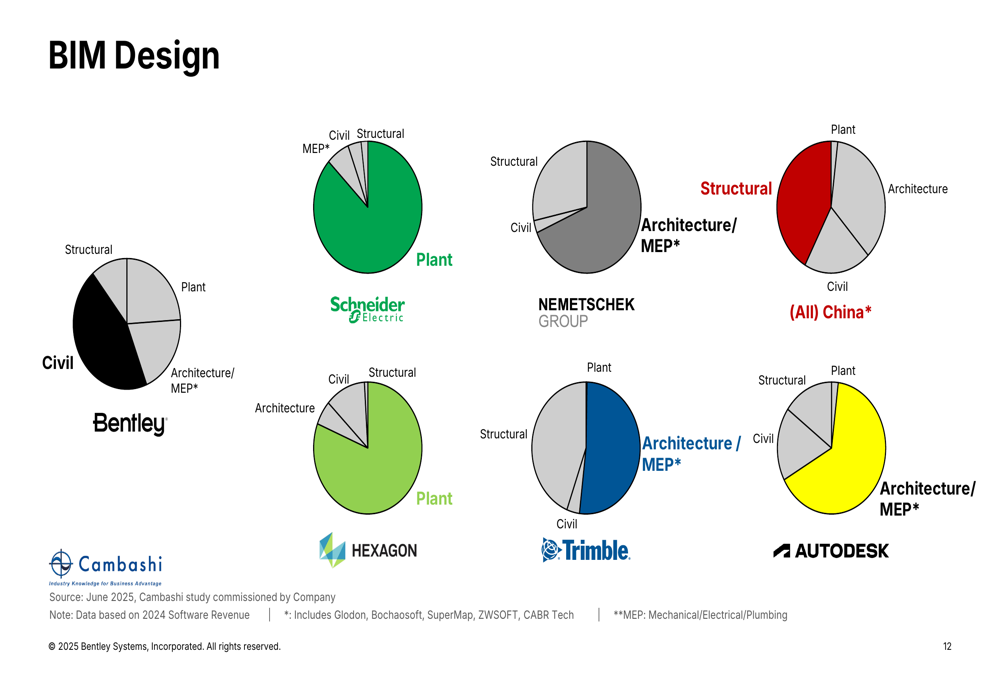

Bentley’s competitive advantage lies in its specialized focus on infrastructure engineering, with particular strength in certain disciplines compared to competitors:

Strategic Initiatives

Bentley continues to focus on 3D geospatial technology and digital twins, with its Cesium platform playing a key role in this strategy. The company is promoting the Cesium Developer Conference taking place in Philadelphia on June 23-25, 2025, focusing on 3D geospatial tech, digital twins, and open data innovation.

The company highlighted how 3D geospatial context, powered by Cesium, improves infrastructure decision-making, with HNTB (an architecture, engineering, and construction management firm) leveraging Cesium to vertically align long linear infrastructure models with the Earth’s curvature.

Additionally, Bentley is preparing for its Going Digital Awards event, scheduled for October 15-16 in Amsterdam, Netherlands, which will celebrate innovative infrastructure projects.

Financial Position and Capital Allocation

Bentley maintains a strong financial position with $90 million in cash and $1,300 million in available revolver credit capacity as of Q2 2025. The company has no net senior debt, with a net senior debt leverage of 0.0x.

Year-to-date capital allocation for 2025 includes:

- $135 million in net bank debt reduction

- $75 million in share repurchases (including $25 million of de-facto share repurchases)

- $42 million in dividends

- $10 million in convertible senior notes repurchase

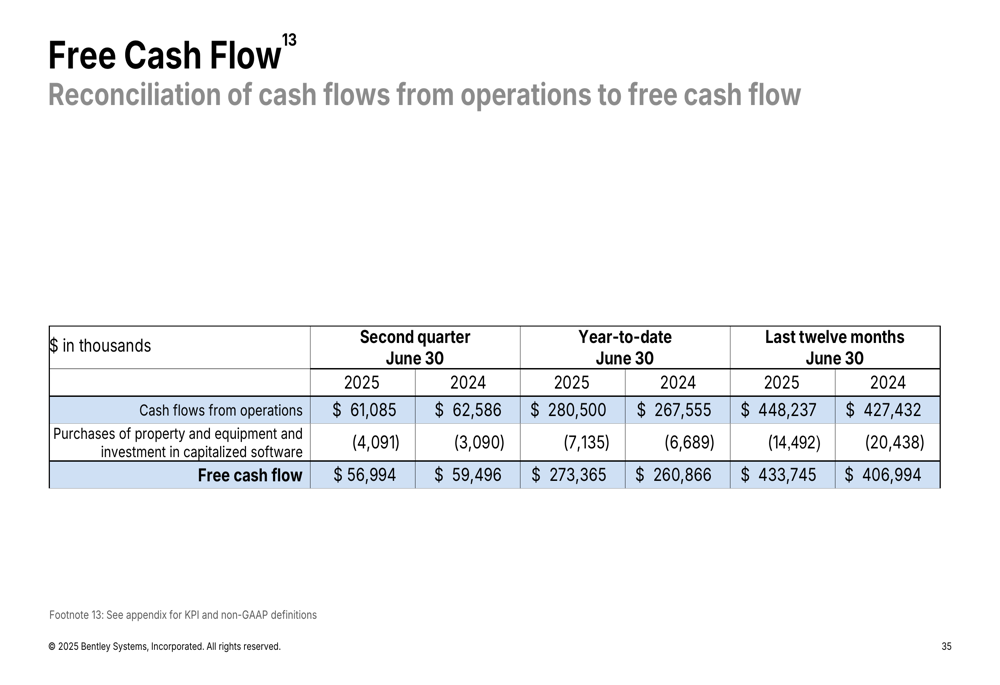

The following chart details Bentley’s free cash flow reconciliation:

Forward-Looking Statements

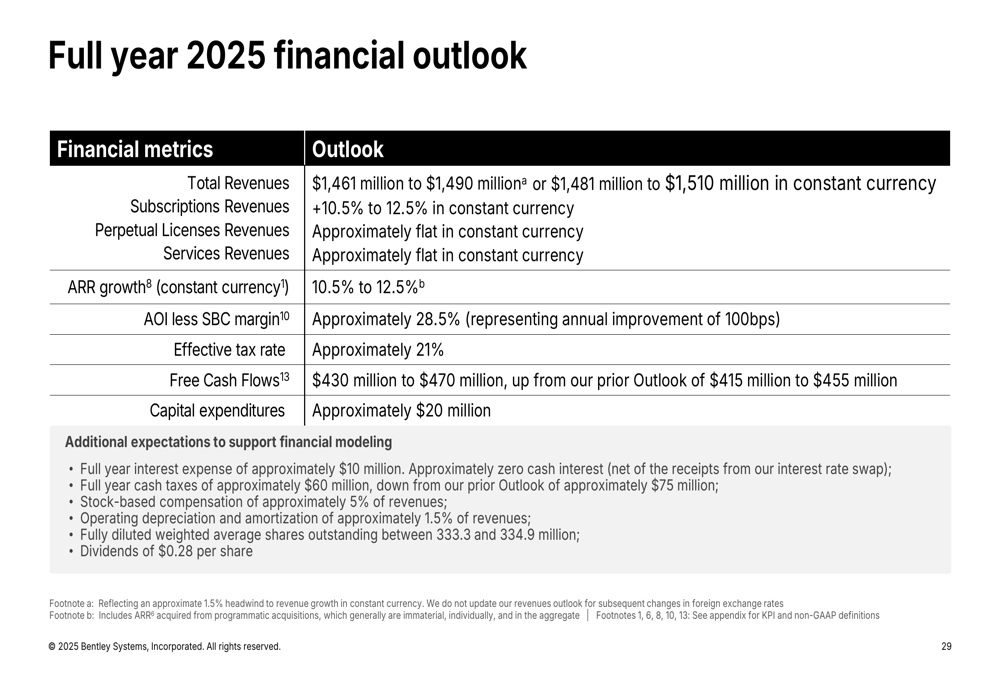

For the full year 2025, Bentley provided the following financial outlook:

- Total Revenues: $1,461 million to $1,490 million ($1,481 million to $1,510 million in constant currency)

- Subscription Revenues: +10.5% to 12.5% growth in constant currency

- Perpetual Licenses Revenues: Approximately flat in constant currency

- Services Revenues: Approximately flat in constant currency

- ARR growth: 10.5% to 12.5%

- AOI less SBC margin: Approximately 28.5%

- Effective tax rate: Approximately 21%

- Free Cash Flows: $430 million to $470 million

- Capital expenditures: Approximately $20 million

This guidance suggests that Bentley expects to maintain its growth trajectory through the remainder of 2025, albeit at a slightly moderated pace compared to previous years.

The company’s outlook is supported by favorable trends in infrastructure spending globally, particularly in the U.S., Latin America, Middle East, and India, though challenges remain in certain regions such as slower transportation spending in Australia.

Bentley’s stock closed at $57.05 on August 5, 2025, and was slightly down in pre-market trading on August 6, 2025, with a minor decrease of 0.09% to $57.00.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.