Hyperscale Data shifts to bitcoin-only treasury strategy

Introduction & Market Context

Beyond Inc. (NYSE:BYON) presented its second quarter 2025 earnings results on July 29, 2025, revealing a company in transition as it continues to prioritize profitability over growth. The company’s stock closed at $10.09 on July 28, up 2.08% ahead of the earnings release, trading significantly above its 52-week low of $3.54 but still well below its 52-week high of $15.44.

The presentation highlighted Beyond’s ongoing efforts to improve operational efficiency and financial discipline while navigating a challenging retail environment. This follows the company’s Q1 2025 results, which saw Beyond beat earnings expectations despite missing revenue forecasts.

Quarterly Performance Highlights

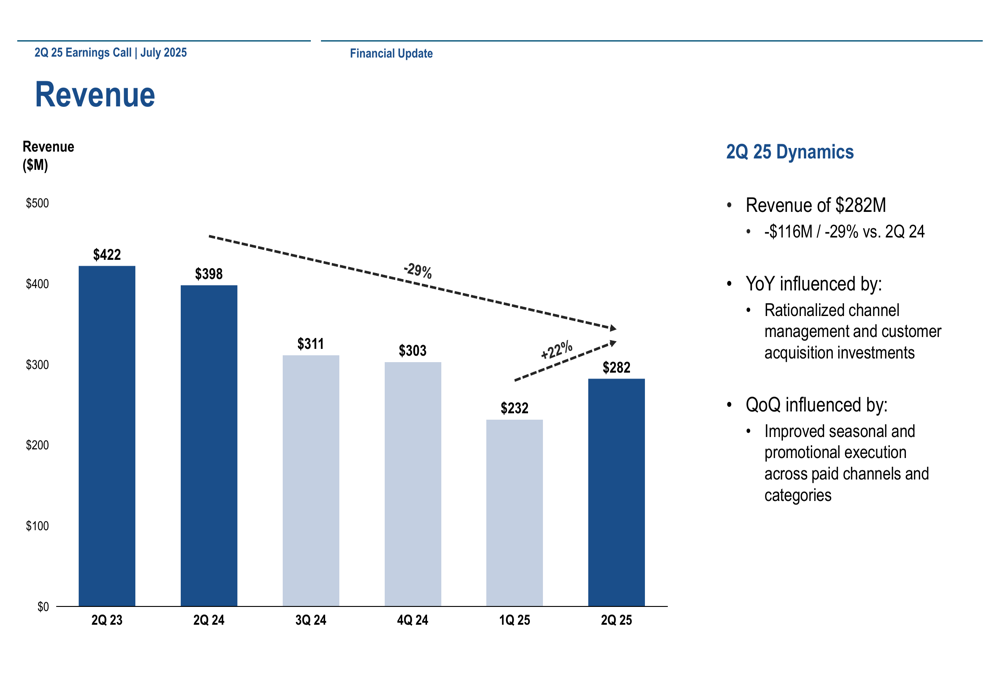

Beyond reported Q2 2025 revenue of $282.3 million, representing a 29.1% decline compared to the same period last year. However, the company showed sequential improvement from Q1 2025’s $232 million, suggesting potential stabilization after several quarters of decline.

As shown in the following chart of quarterly revenue performance:

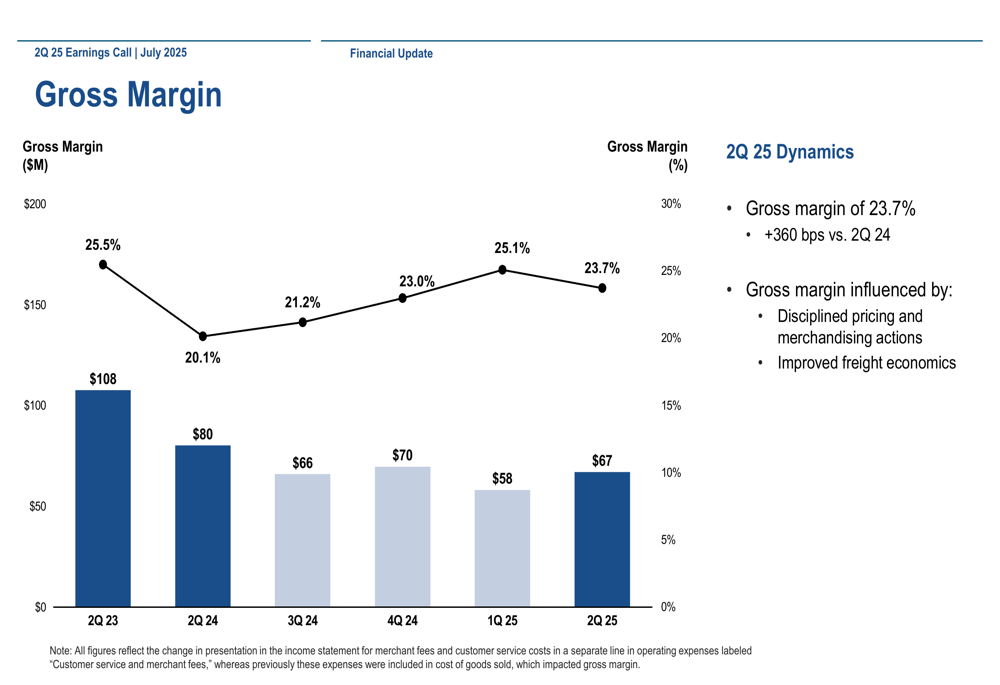

Despite the revenue decline, Beyond made significant progress on profitability metrics. Gross margin improved to 23.7%, a 360 basis point increase compared to Q2 2024. The company attributed this improvement to disciplined pricing and merchandising actions, along with improved freight economics.

The following chart illustrates the gross margin trend over recent quarters:

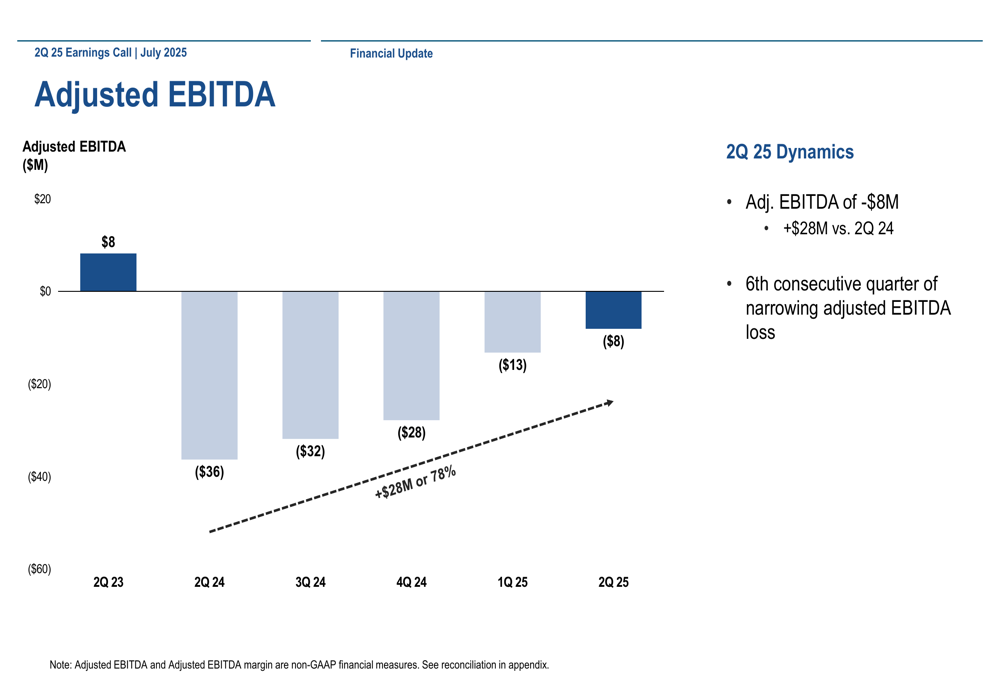

Perhaps most notably, Beyond reported its sixth consecutive quarter of narrowing adjusted EBITDA loss, with Q2 2025 adjusted EBITDA at -$8.1 million, representing a $28.3 million improvement compared to Q2 2024.

The company’s progress in reducing losses is clearly demonstrated in this chart:

Detailed Financial Analysis

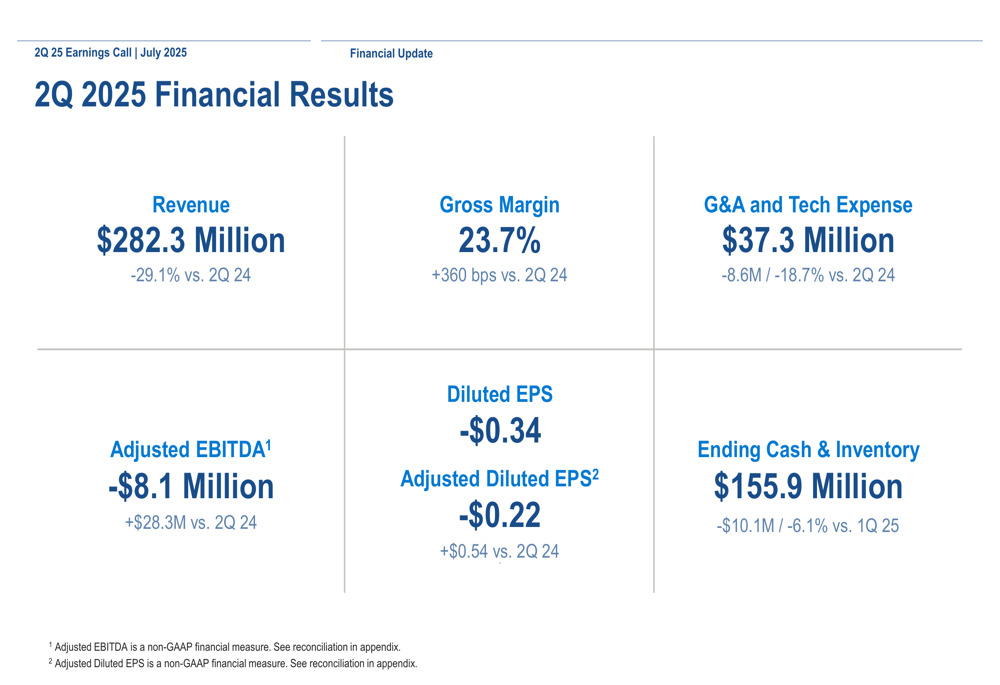

Beyond’s financial results reflect its strategic shift toward operational efficiency and profitability. The company reported adjusted diluted EPS of -$0.22, a $0.54 improvement compared to Q2 2024, while ending the quarter with $155.9 million in cash and inventory, a 6.1% decrease from Q1 2025.

The comprehensive financial results are summarized in this slide:

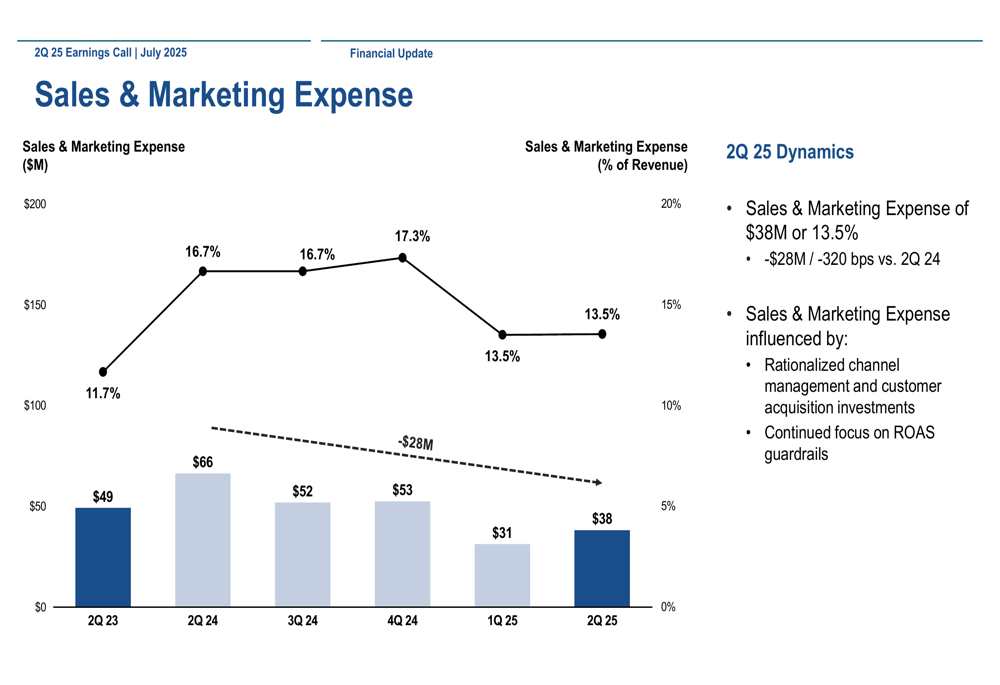

A key component of Beyond’s cost-cutting strategy has been reducing sales and marketing expenses, which decreased to 13.5% of revenue in Q2 2025 compared to 16.7% in Q2 2024. This represents a $28 million reduction year-over-year, driven by what the company describes as "rationalized channel management and customer acquisition investments" and "continued focus on ROAS guardrails."

The following chart shows the trend in sales and marketing expenses:

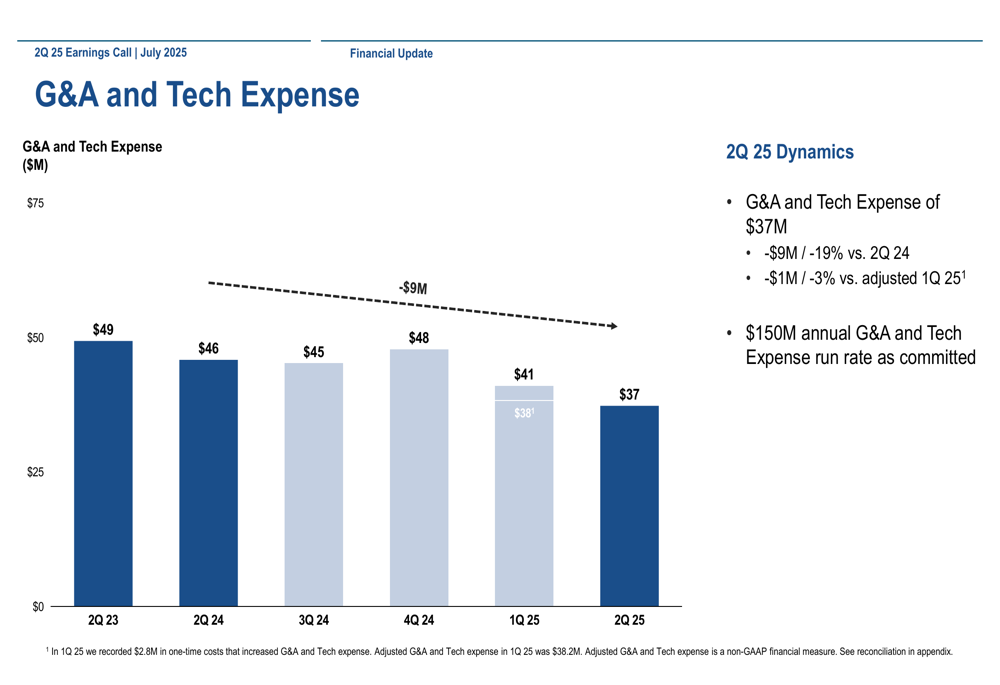

Similarly, Beyond has made significant progress in reducing G&A and technology expenses, which totaled $37.3 million in Q2 2025, a 18.7% decrease compared to Q2 2024. The company noted it has achieved its target of a $150 million annual G&A and Tech expense run rate.

This expense reduction is illustrated in the following chart:

Strategic Initiatives

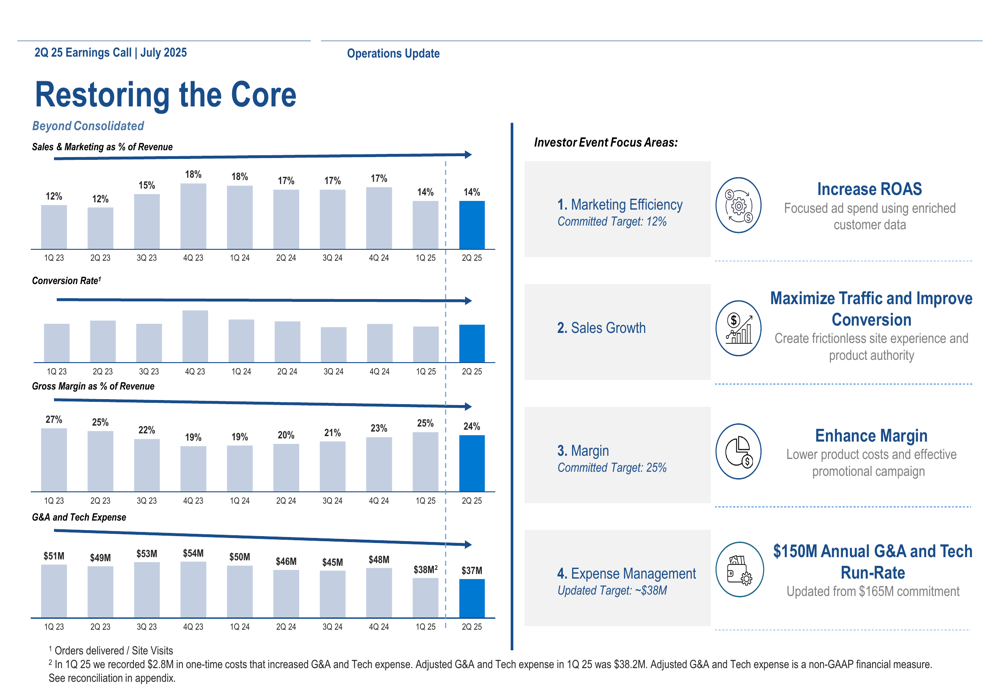

Beyond’s presentation revealed a strategic focus on what it calls "Restoring the Core," with emphasis on four key areas: marketing efficiency, sales growth, margin improvement, and expense management. The company has committed to specific targets in these areas, including a 12% target for marketing as a percentage of revenue and a 25% gross margin target.

The company’s strategic roadmap is outlined in this slide:

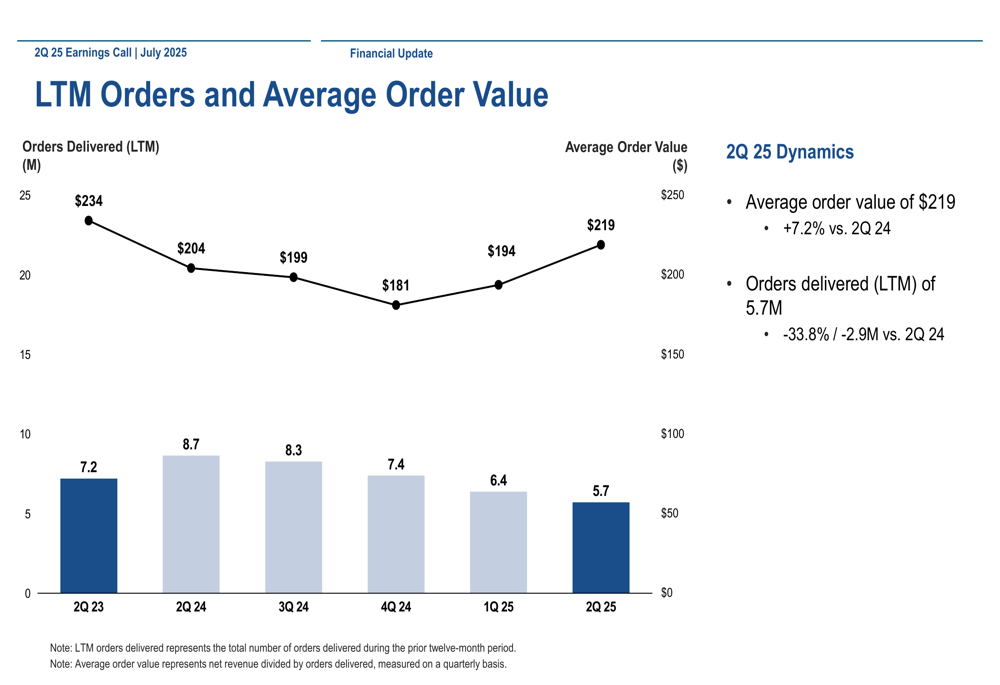

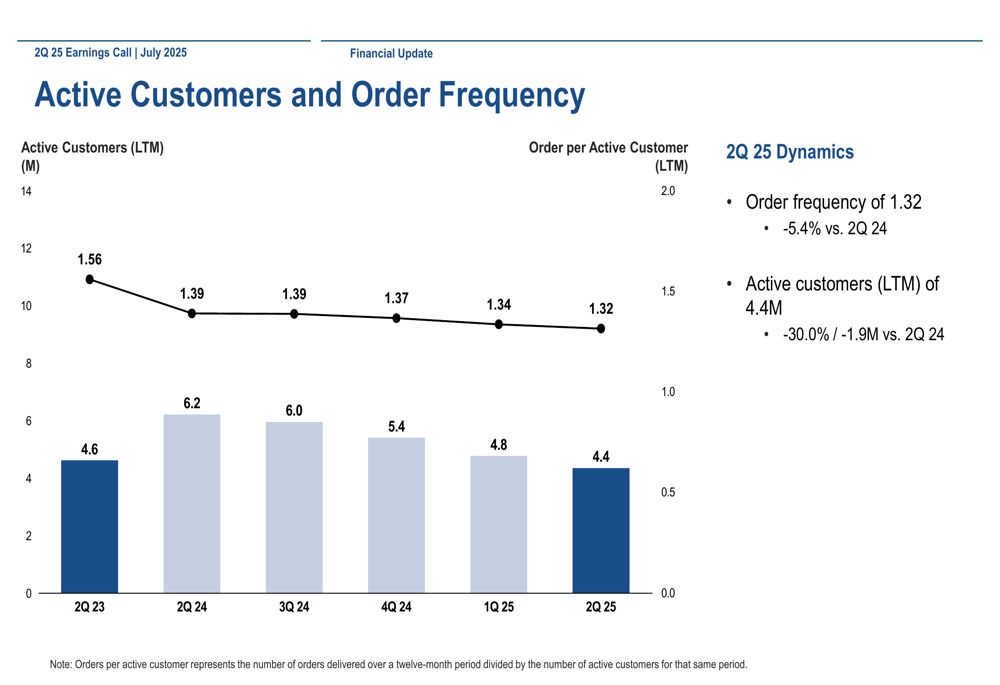

While Beyond has successfully improved its average order value to $219 in Q2 2025 (a 7.2% increase year-over-year), the company continues to face challenges with customer retention and order frequency. Active customers declined to 4.4 million, a 30% decrease compared to Q2 2024, while order frequency decreased to 1.32 orders per active customer, down 5.4% year-over-year.

The following charts illustrate these customer metrics:

Forward-Looking Statements

Looking ahead, Beyond appears to be maintaining its focus on operational efficiency while working to stabilize and eventually grow revenue. The sequential improvement in revenue from Q1 to Q2 2025 suggests the company may be making progress toward its previously stated goal of transitioning from restructuring to growth.

The company’s cash position of $155.9 million represents a decline from the $166 million reported at the end of Q1 2025, indicating that Beyond continues to use cash resources as it works toward profitability. However, the narrowing adjusted EBITDA loss suggests the company is moving in the right direction.

Beyond’s commitment to specific targets, including a 25% gross margin and a $150 million annual G&A and Tech expense run rate, provides clear benchmarks against which investors can measure the company’s progress in coming quarters. The company’s ability to meet these targets while reversing the trend of declining active customers will likely be key factors in determining its long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.