Oil prices extend losses as traders downplay Russia sanction risks

Introduction & Market Context

Biogen Inc (NASDAQ:BIIB) presented its second quarter 2025 financial results on July 31, 2025, showcasing solid performance that exceeded market expectations and prompted management to raise full-year guidance. The company’s stock jumped 4.3% in premarket trading to $132.08, reflecting investor optimism about the results and outlook.

The biotechnology company reported revenue growth of 7% year-over-year, continuing its recovery trajectory after facing headwinds in its multiple sclerosis franchise. This performance represents an acceleration from the 6% growth reported in Q1 2025, with new product launches increasingly offsetting declines in mature products.

Quarterly Performance Highlights

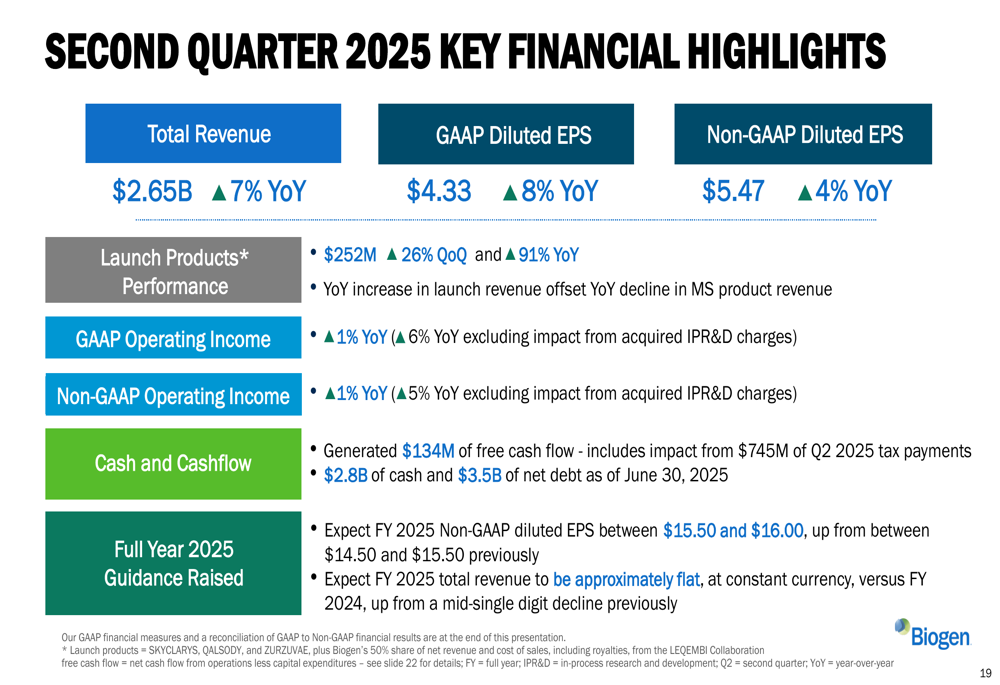

Biogen reported total revenue of $2.65 billion for Q2 2025, a 7% increase compared to the same period last year. The company’s newer products showed particularly strong momentum, with launch products generating $252 million, up 26% quarter-over-quarter and 91% year-over-year.

As shown in the following financial highlights slide, Biogen delivered GAAP diluted earnings per share of $4.33, up 8% year-over-year, while non-GAAP diluted EPS reached $5.47, representing a 4% increase:

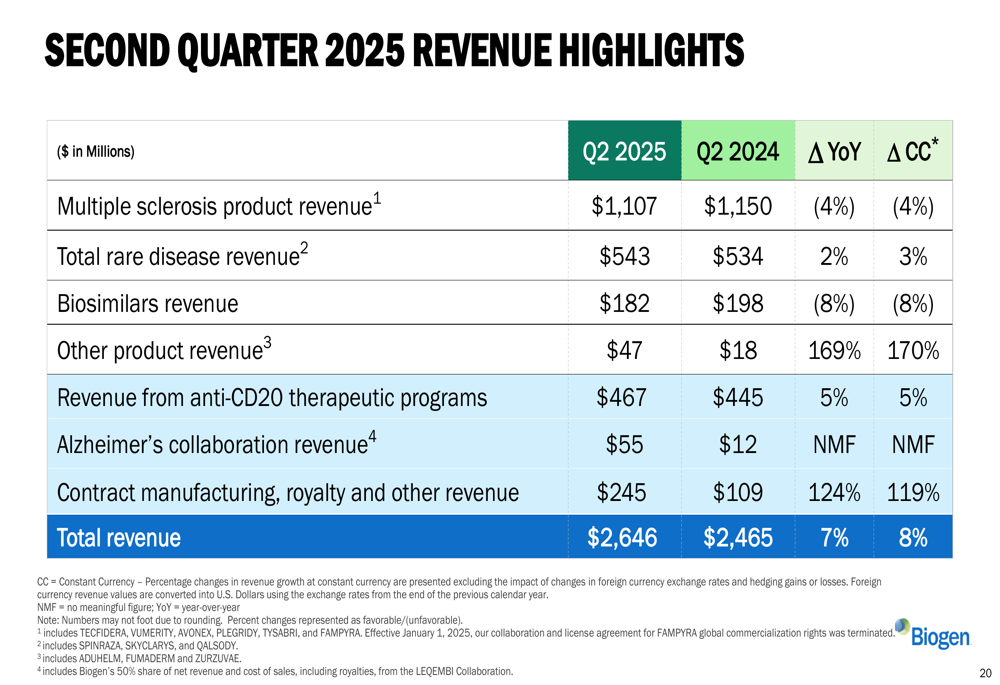

The revenue breakdown reveals a mixed performance across Biogen’s portfolio. While multiple sclerosis products declined 4% to $1.1 billion, this was more than offset by growth in other areas, particularly rare disease products and contract manufacturing revenue:

The company’s financial position remains solid with $134 million in free cash flow generated during the quarter. As of June 30, 2025, Biogen reported $2.8 billion in cash and cash equivalents against $6.3 billion in debt, resulting in a net debt position of $3.5 billion.

Product Performance & Commercial Strategy

Biogen’s newer products continue to gain traction in the market, helping to diversify revenue streams beyond the company’s traditional multiple sclerosis franchise. SKYCLARYS, a treatment for Friedreich’s ataxia, has expanded its global footprint significantly:

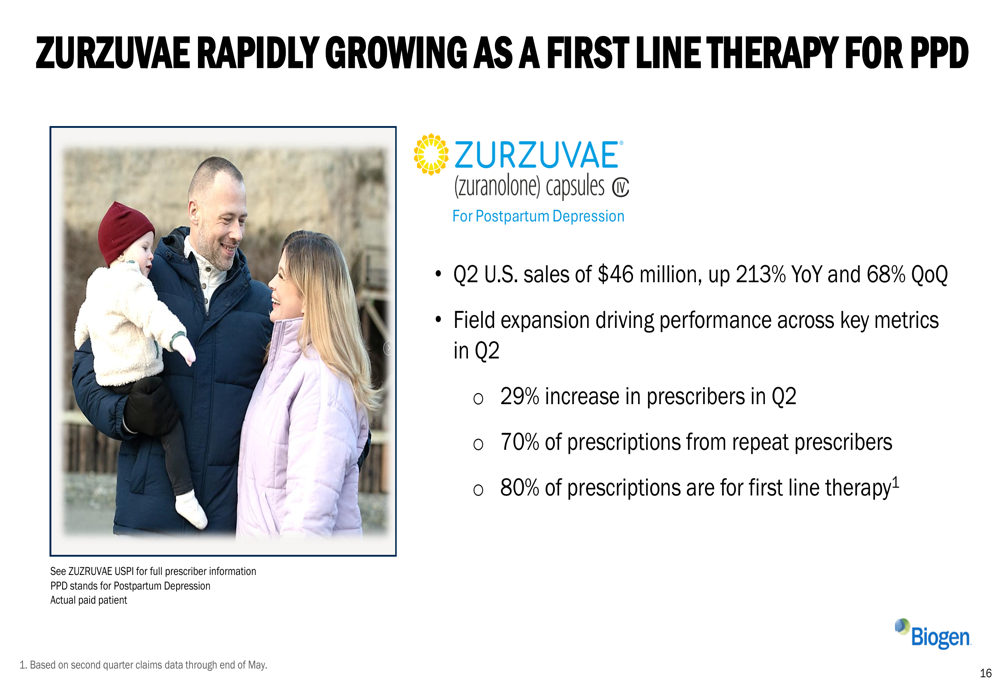

ZURZUVAE, Biogen’s treatment for postpartum depression, demonstrated exceptional growth with Q2 U.S. sales of $46 million, representing a 213% year-over-year increase and 68% quarter-over-quarter growth. The company noted that 80% of prescriptions are for first-line therapy, indicating strong physician adoption:

In the Alzheimer’s disease space, LEQEMBI continues to gain momentum with worldwide sales of $160 million. The company is making strategic investments to accelerate growth, including expanding the prescriber base and increasing diagnostic capabilities:

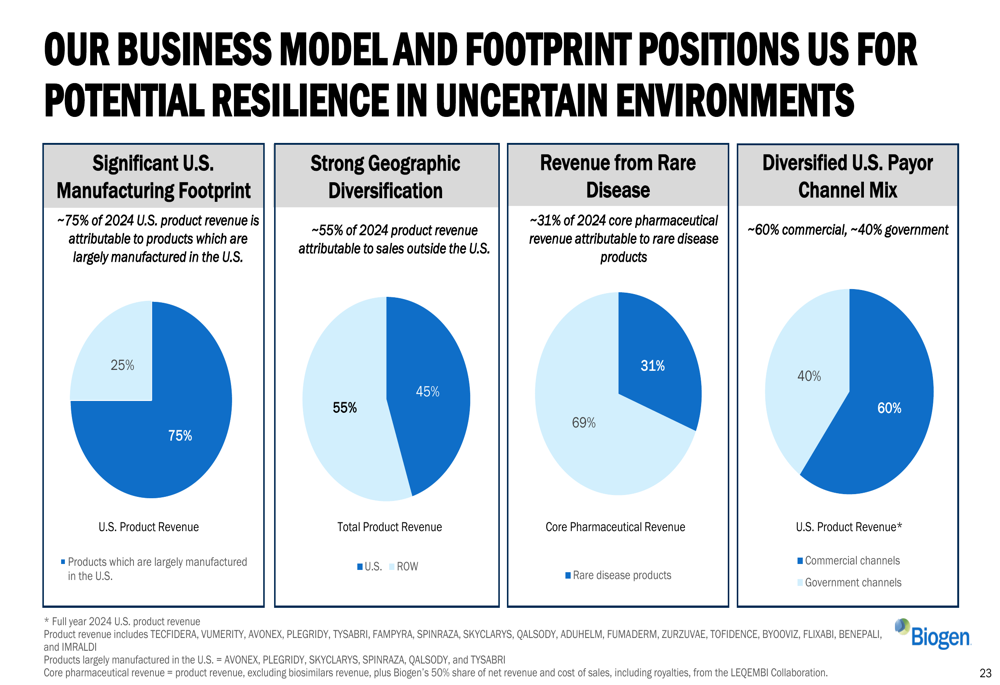

Biogen emphasized the resilience of its business model through geographic diversification, with approximately 55% of 2024 product revenue coming from outside the U.S. The company also highlighted its strong U.S. manufacturing footprint and significant presence in rare diseases:

Pipeline Advancements

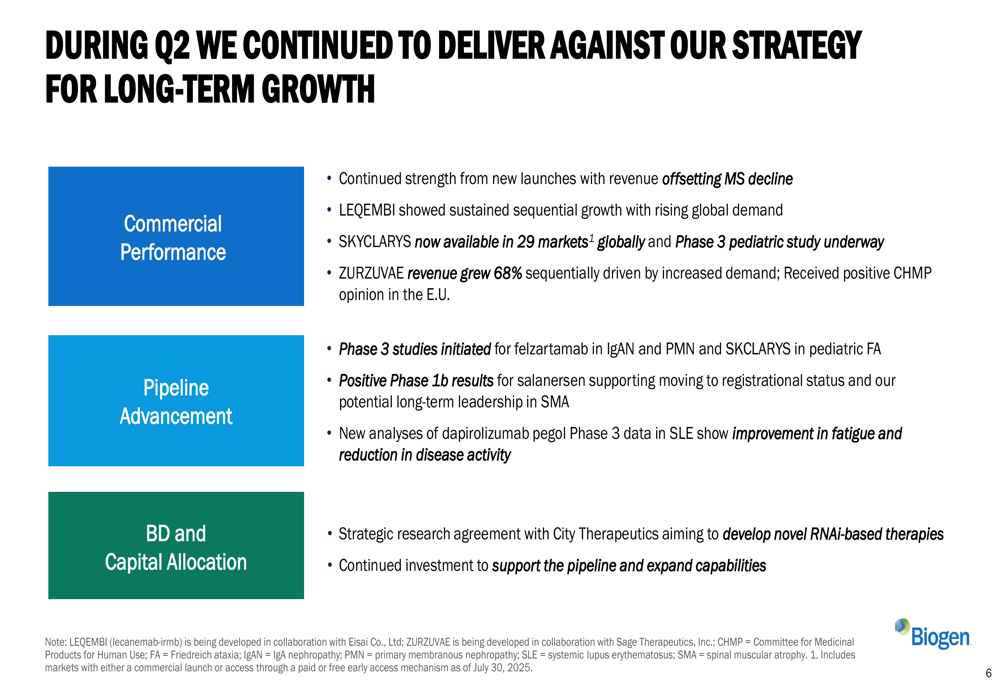

Biogen’s pipeline saw significant advancement during Q2 2025, with progress across multiple therapeutic areas. The company’s strategy delivery slide highlights key achievements in commercial performance and pipeline advancement:

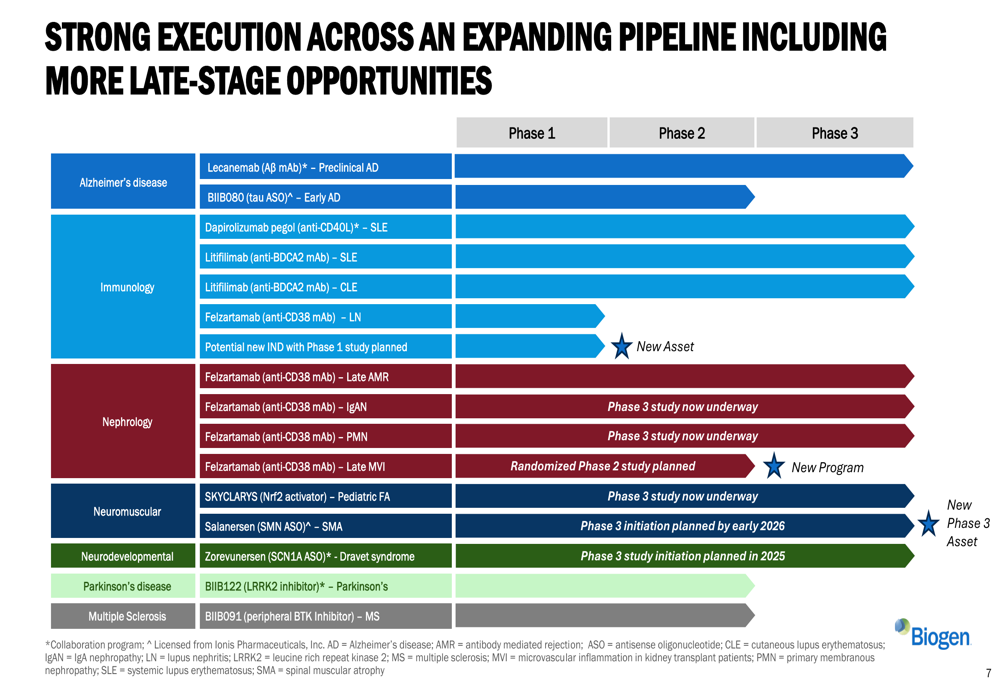

The expanding pipeline provides multiple opportunities for future growth across various disease areas and development stages:

Among the notable pipeline developments, Biogen reported positive Phase 1b interim results for salanersen in spinal muscular atrophy (SMA) patients who previously received gene therapy. The company also presented new data showing that dapirolizumab pegol improved fatigue, reduced disease activity, and enhanced quality of life in lupus patients.

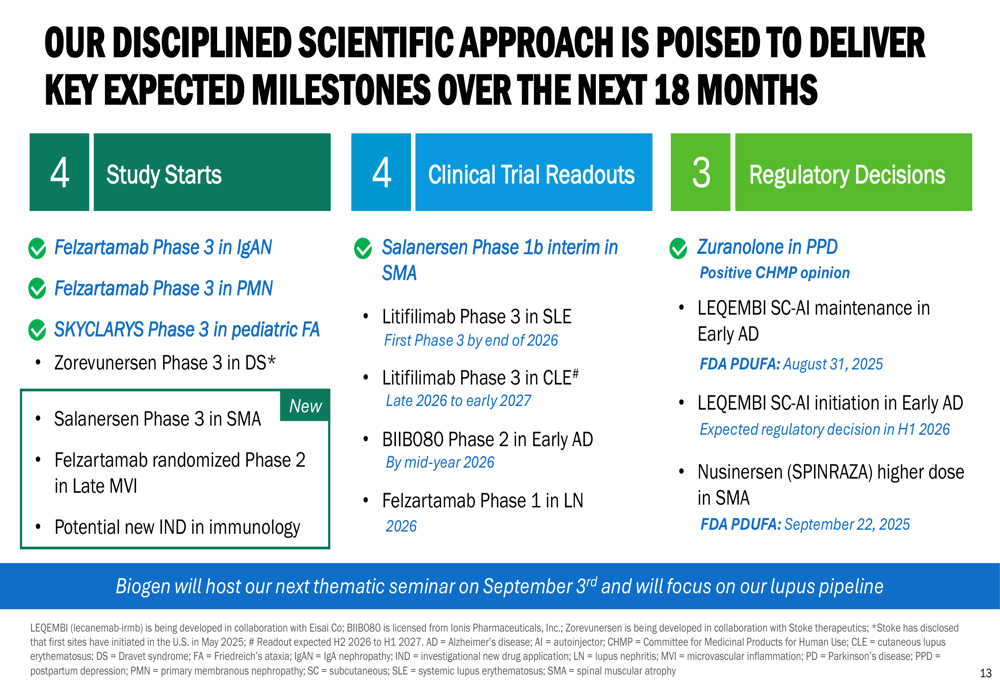

Looking ahead, Biogen outlined several key milestones expected over the next 18 months, including multiple study initiations, clinical trial readouts, and regulatory decisions:

Financial Outlook & Guidance

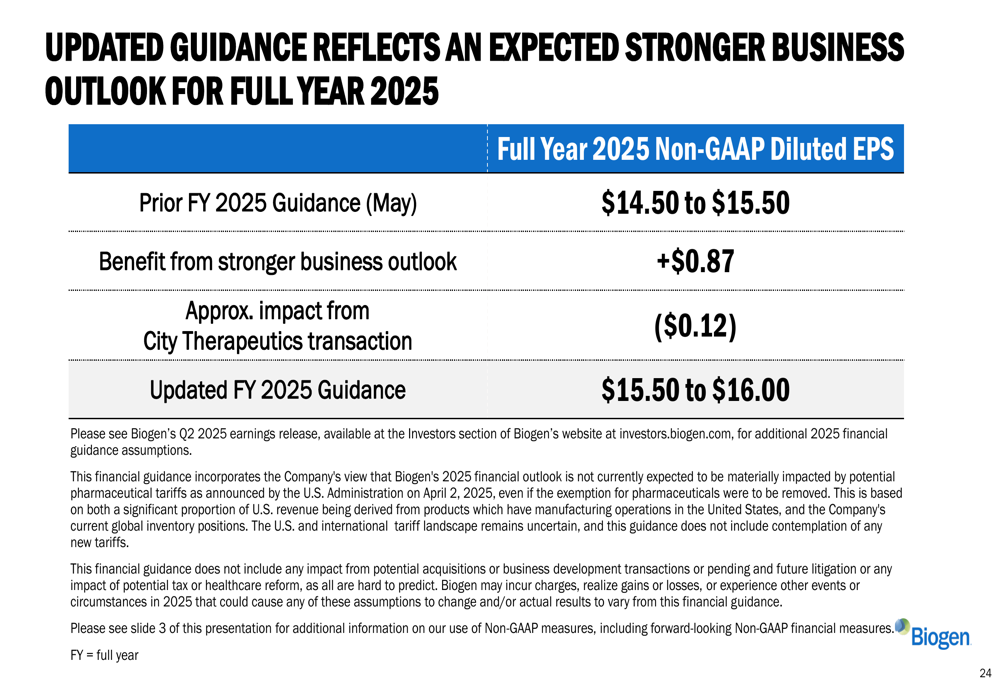

Based on the strong Q2 performance and positive business outlook, Biogen raised its full-year 2025 guidance. The company now expects non-GAAP diluted EPS of $15.50 to $16.00, up from the previous guidance of $14.50 to $15.50:

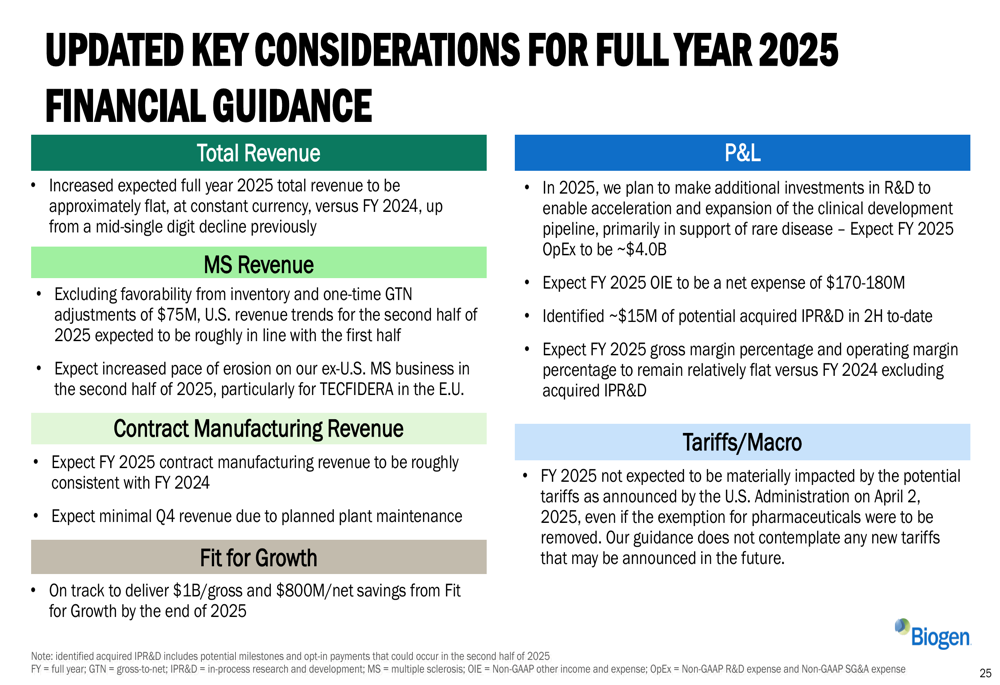

For the full year 2025, Biogen expects total revenue to be approximately flat at constant currency, an improvement from the mid-single-digit decline projected earlier in the year. The company remains on track to deliver $1 billion in gross savings and $800 million in net savings by the end of 2025 through its "Fit for Growth" initiative.

The guidance update represents a significant improvement from Biogen’s outlook following Q1 results, when the company anticipated a mid-single-digit revenue decline for the year. This positive revision suggests that Biogen’s strategy of focusing on newer products while managing the decline of mature franchises is yielding better-than-expected results.

With multiple potential catalysts on the horizon, including regulatory decisions for LEQEMBI’s subcutaneous formulation and higher-dose SPINRAZA, along with several Phase 3 study initiations, Biogen appears well-positioned to maintain its growth momentum through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.