US stock futures steady with China trade talks, Q3 earnings in focus

Introduction & Market Context

Björn Borg AB (STO:BORG) presented its Q2 2025 results on August 15, 2025, revealing continued channel transformation with strong e-commerce growth offsetting physical retail challenges. The Swedish sportswear company’s stock closed at 57.5 SEK on August 14, down 1.54% ahead of the presentation, continuing a downward trend that began after its Q1 earnings release despite strong financial results.

The presentation highlighted the company’s ongoing strategic shift toward digital channels and sports apparel, with mixed performance across geographic markets. Following a record-breaking Q1 with sales of SEK 280 million, Q2 showed more moderate growth of 6% year-over-year.

Executive Summary

CEO Henrik Bunge emphasized the quarter’s standout performances: "We see strong growth in e-commerce, up 26%, and sports apparel, up 45%, during the second quarter of 2025. This confirms the power of our brand, the relevance of our product offering, and the strength of our digital strategies."

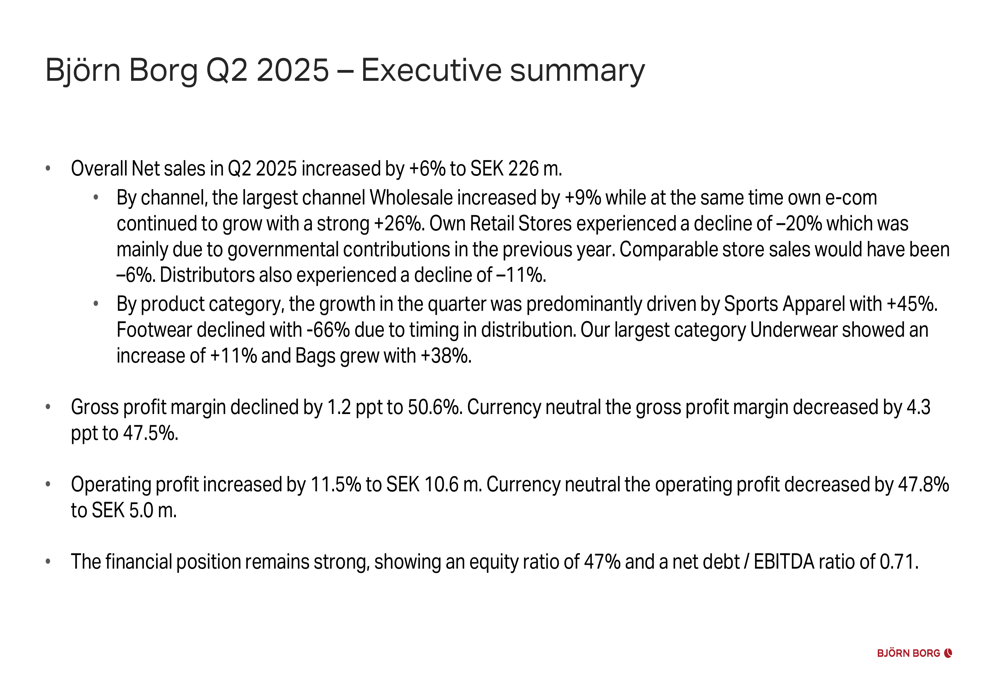

The company reported net sales of SEK 226 million, a 6% increase compared to Q2 2024. Operating profit rose 11.5% to SEK 10.6 million, though on a currency-neutral basis, operating profit decreased by 47.8% to SEK 5.0 million, indicating significant currency tailwinds during the quarter.

As shown in the following financial summary:

Quarterly Performance Highlights

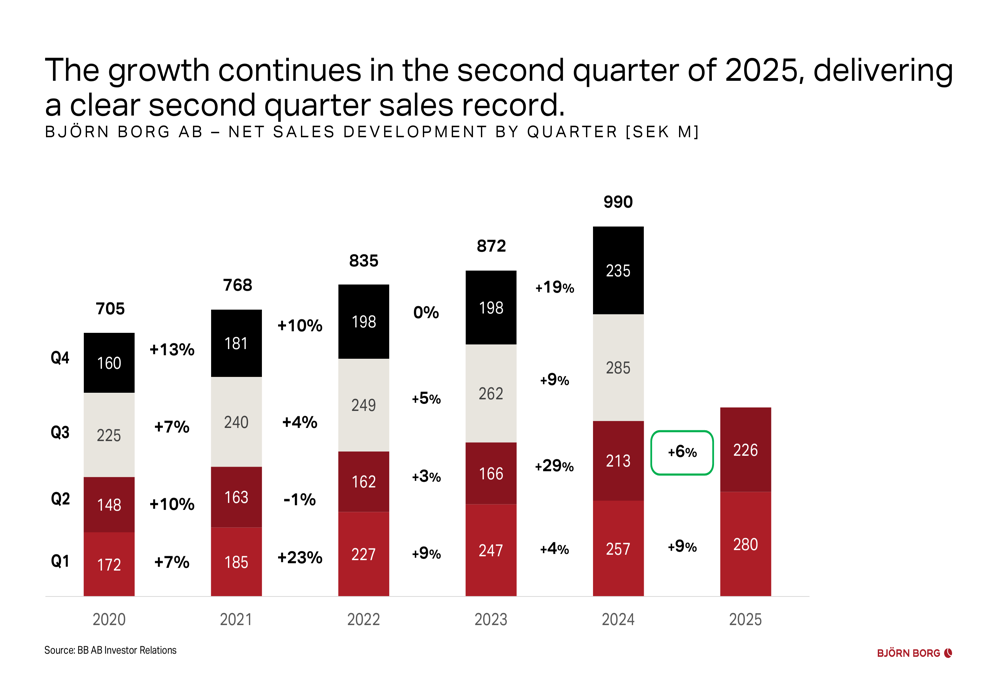

Björn Borg’s quarterly sales have shown consistent growth since 2020, with Q2 2025 continuing this upward trajectory. The company achieved sales of SEK 226 million in Q2 2025, compared to SEK 213 million in Q3 2024 and SEK 257 million in Q4 2024. This performance aligns with the company’s long-term financial objective of achieving minimum 10% annual sales growth.

The quarterly sales development demonstrates the company’s recovery and growth:

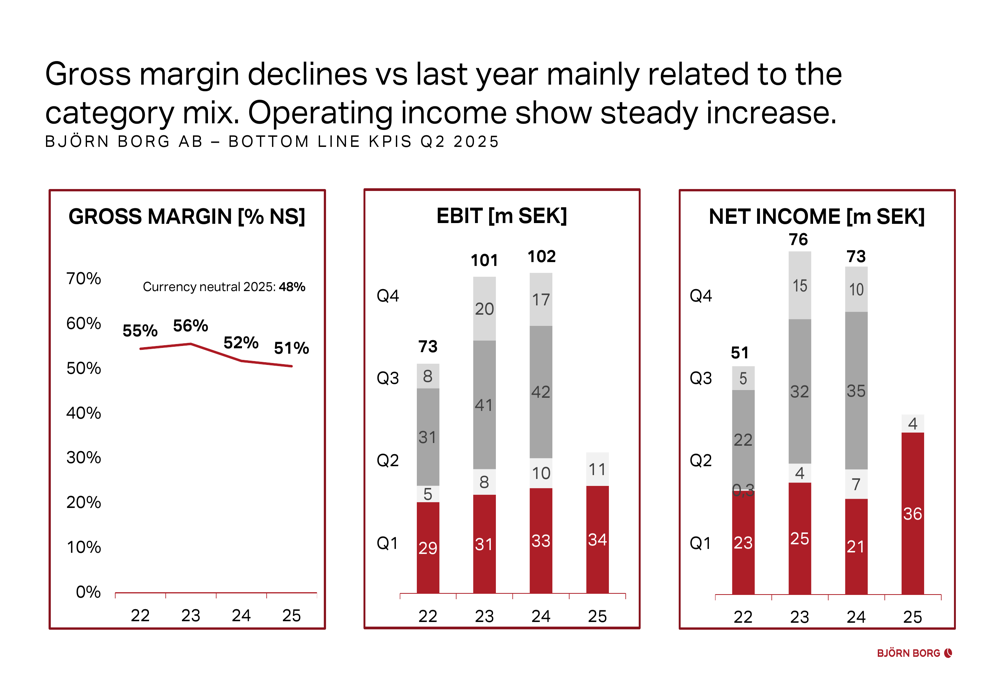

However, profitability metrics showed mixed results. While operating profit increased in absolute terms, the gross profit margin declined by 1.2 percentage points to 50.6%. On a currency-neutral basis, the margin decrease was more pronounced at 4.3 percentage points, falling to 47.5%. This continues a trend seen in Q1, where the company reported a gross margin of 50%.

The following chart illustrates the company’s profitability trends:

Channel & Category Analysis

Björn Borg’s channel performance revealed a clear shift toward digital sales. Wholesale grew by 9% and own e-commerce surged by 26% compared to Q2 2024, while retail stores declined by 20% and distributor sales fell by 11%.

The channel development breakdown shows this divergence:

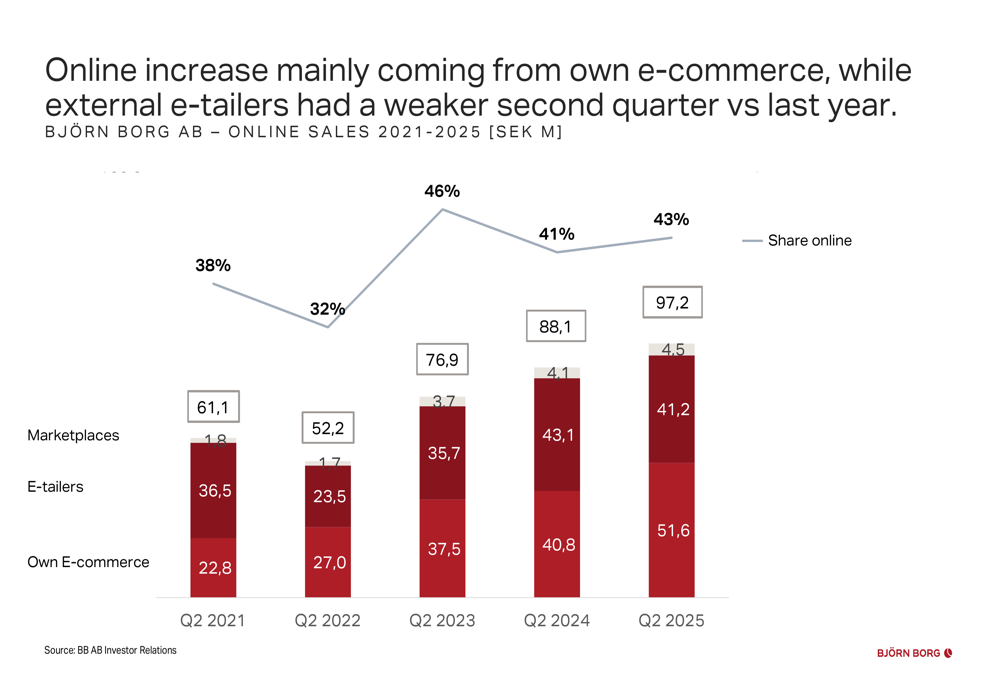

The company’s online presence has strengthened considerably, with total online sales reaching 43% of revenue in Q2 2025, up from 38% in 2021. Own e-commerce sales have more than doubled from SEK 22.8 million in Q2 2021 to SEK 51.6 million in Q2 2025.

This digital transformation is illustrated in the following chart:

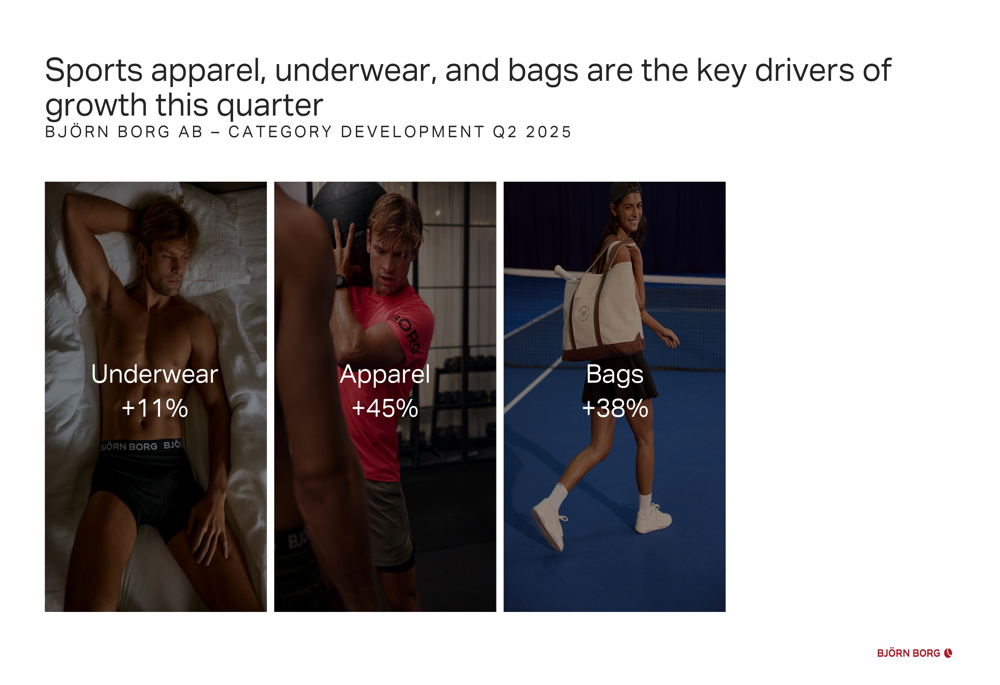

Product category performance was led by sports apparel, which grew by an impressive 45%, reinforcing the company’s strategic focus on this segment. Underwear, traditionally Björn Borg’s core product, increased by 11%, while bags grew by 38%. Notably, footwear declined by 66%, a significant reversal from the strong footwear performance reported in Q1 2025.

The category growth rates demonstrate this shift:

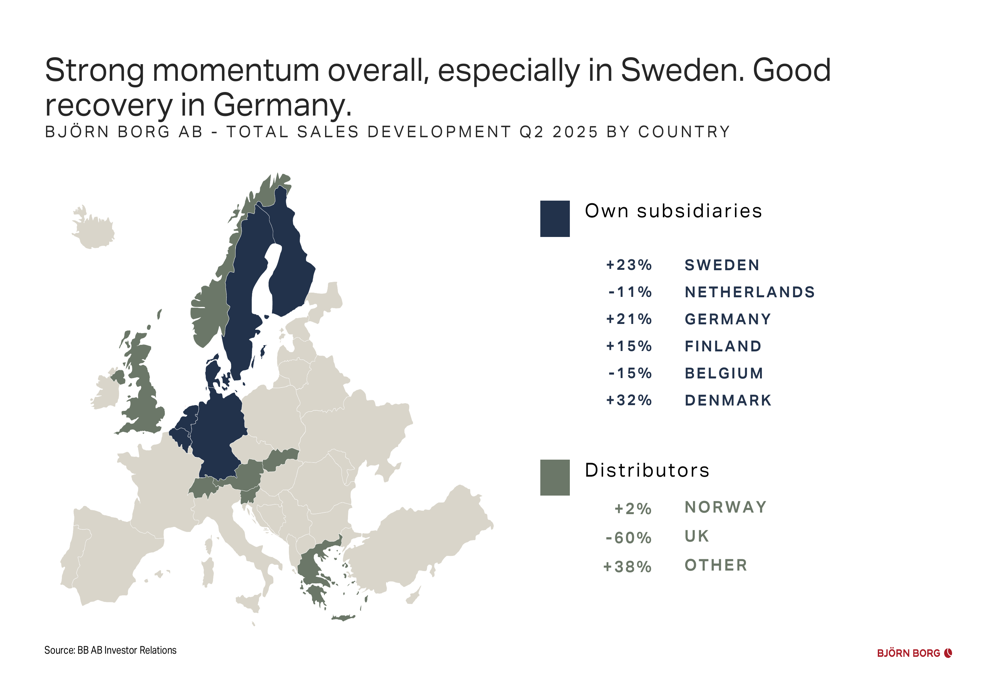

Geographic Performance

Björn Borg reported varied performance across markets, with strongest growth in Denmark (+32%), Sweden (+23%), and Germany (+21%). Finland also performed well with 15% growth. However, the company faced challenges in Belgium (-15%), Netherlands (-11%), and particularly in the UK, where sales plummeted by 60%.

The geographic sales breakdown is visualized here:

The company highlighted significant brand momentum in Germany, with consideration among women increasing by 39% (18.9% vs 13.6% in Q2 2024) and purchase intention among men rising by 46% (34.5% vs 23.6% in Q2 2024). Sweden also showed positive brand development, with consideration among men increasing by 10% (84.6% vs 76.9% in Q2 2024).

This brand strength is captured in the following metrics:

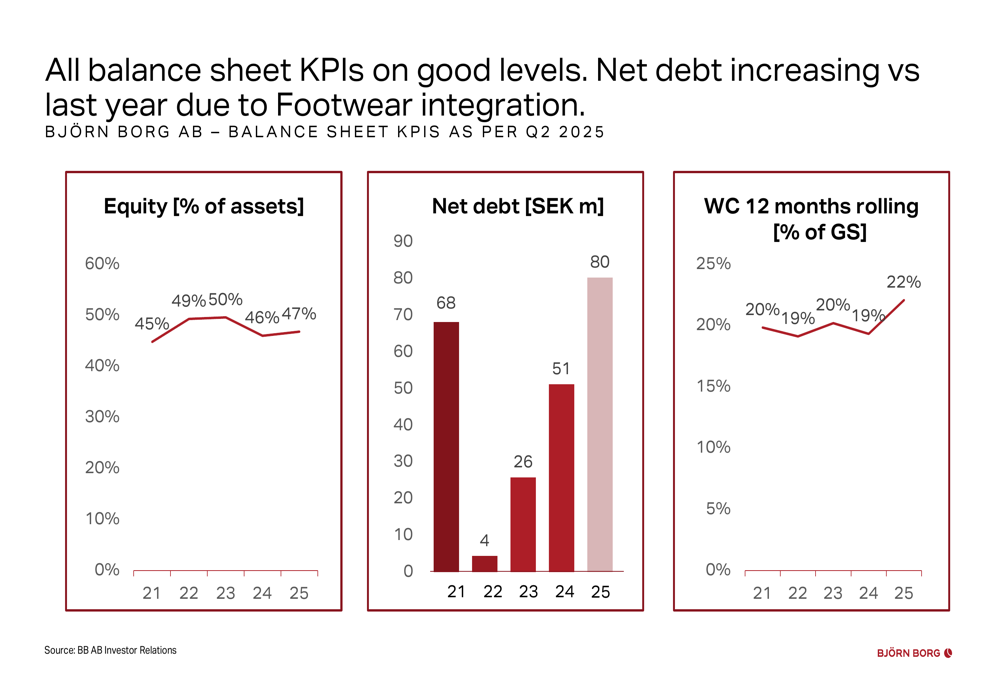

Balance Sheet & Profitability

Björn Borg maintained an equity ratio of 47%, above its minimum target of 35% but down from the 52% reported in Q1 2025. The company’s net debt to EBITDA ratio stood at 0.71, indicating relatively low leverage. However, the presentation showed an increasing trend in net debt, which warrants monitoring.

The balance sheet metrics are shown here:

Strategic Outlook

Björn Borg reiterated its mission to "Inspire people to be more through sports" and outlined its business strategy focused on three pillars: increasing share of online and business with e-tailers, growing business share and preference in sports apparel, and expanding geographically with a focus on Europe.

The company’s strategic framework is outlined below:

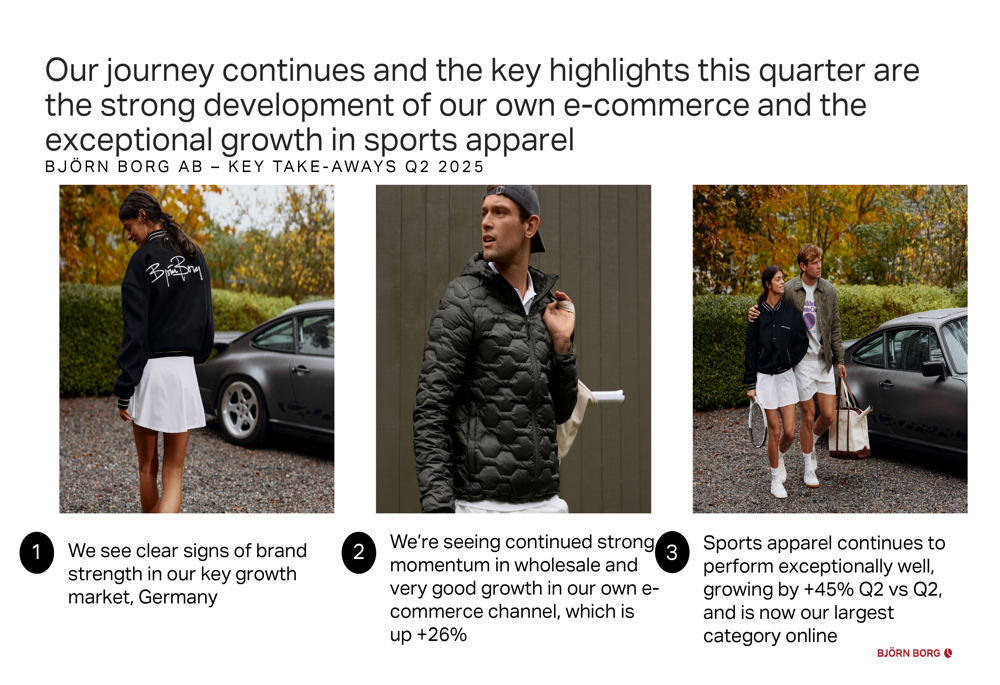

The presentation concluded with three key takeaways: clear signs of brand strength in Germany, strong momentum in wholesale and growth in own e-commerce, and continued strong performance in sports apparel, which is now the largest category online.

While Q2 2025 showed continued growth, the declining gross margin and mixed geographic performance present challenges that the company will need to address to achieve its long-term financial objectives of minimum 10% annual sales growth and minimum 10% operating margin. The strong performance in e-commerce and sports apparel, however, indicates that Björn Borg’s strategic transformation is progressing successfully.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.