TSX gains after CPI shows US inflation rose 3%

Introduction & Market Context

BlackRock TCP Capital Corp . (NASDAQ:TCPC) released its first quarter 2025 investor presentation on May 8, showcasing steady performance in a challenging middle market lending environment. The business development company (BDC) continues to focus on senior secured lending to middle market companies, which represent approximately one-third of private sector GDP and employ around 48 million people in the United States.

According to the presentation, 85% of middle market companies reported year-over-year revenue growth of 12.1%, highlighting the resilience of this segment despite broader economic uncertainties. This growth environment provides TCPC with continued lending opportunities, though the company’s stock has faced pressure, currently trading at $6.61, well below its 52-week high of $11.39.

Quarterly Performance Highlights

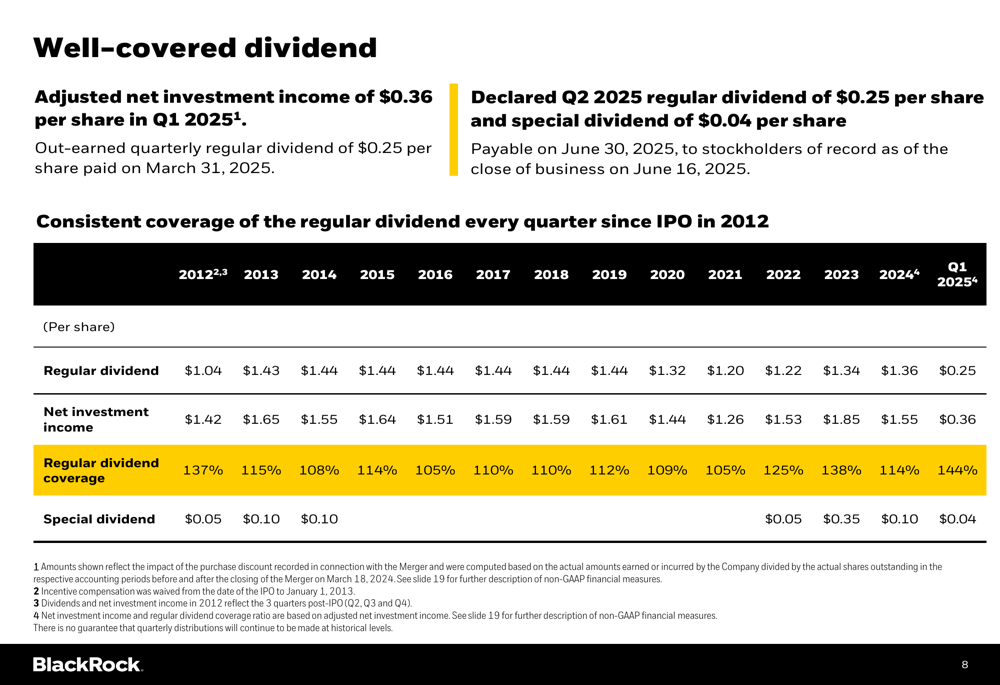

BlackRock (NYSE:BLK) TCP reported adjusted net investment income (NII) of $0.36 per share for Q1 2025, translating to an annualized adjusted NII return on equity of 15.4%. This performance exceeded the regular quarterly dividend of $0.25 per share, resulting in a dividend coverage ratio of 144% for the quarter.

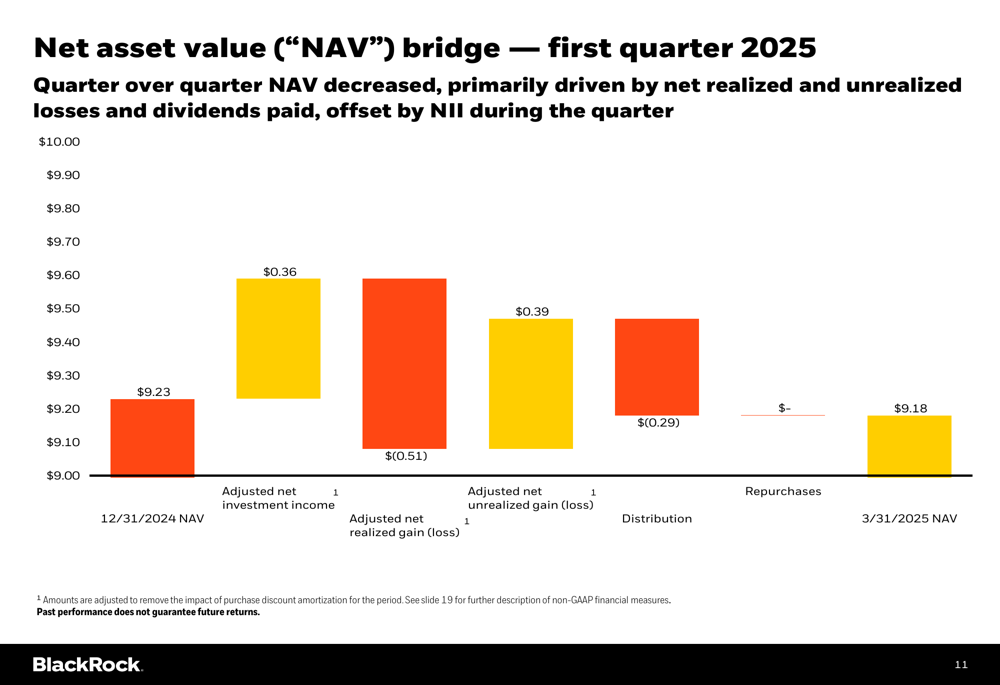

The company’s net asset value (NAV) per share decreased slightly from $9.23 at the end of 2024 to $9.18 as of March 31, 2025. This decline continues a downward trend, as NAV stood at $10.11 before Q4 2024, according to previous earnings reports.

As shown in the following NAV bridge chart, the decrease was primarily driven by net realized losses of $0.51 per share, partially offset by net unrealized gains of $0.39 per share and the strong NII performance:

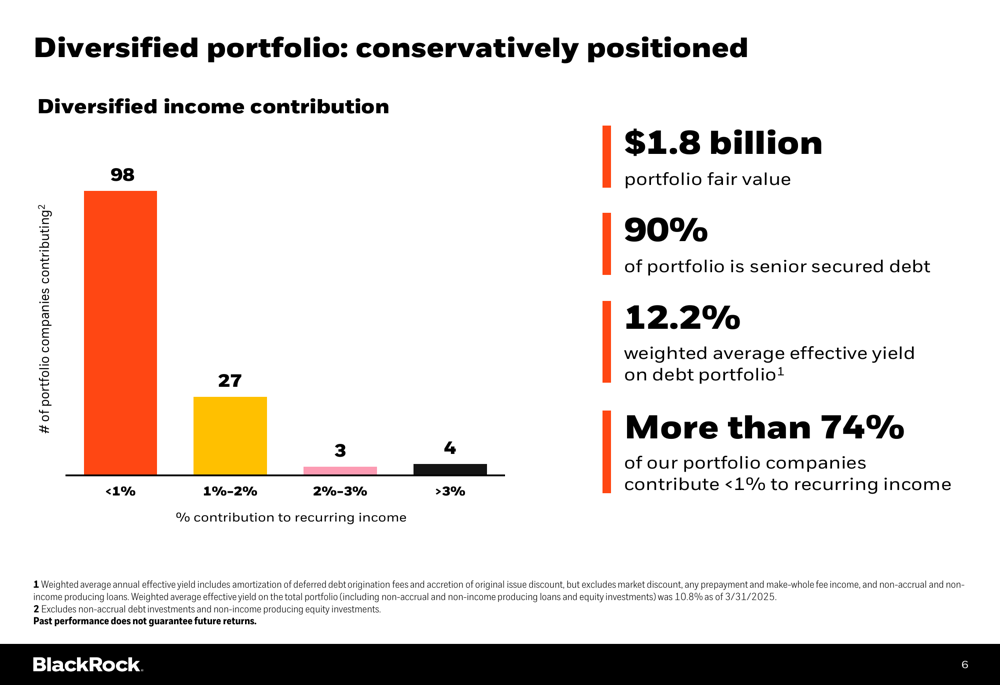

The company’s total portfolio fair value stood at $1.8 billion, diversified across 146 portfolio companies. During the quarter, TCPC completed $66 million in new acquisitions while disposing of $85 million in investments, indicating a slight net reduction in portfolio size.

Portfolio Composition and Quality

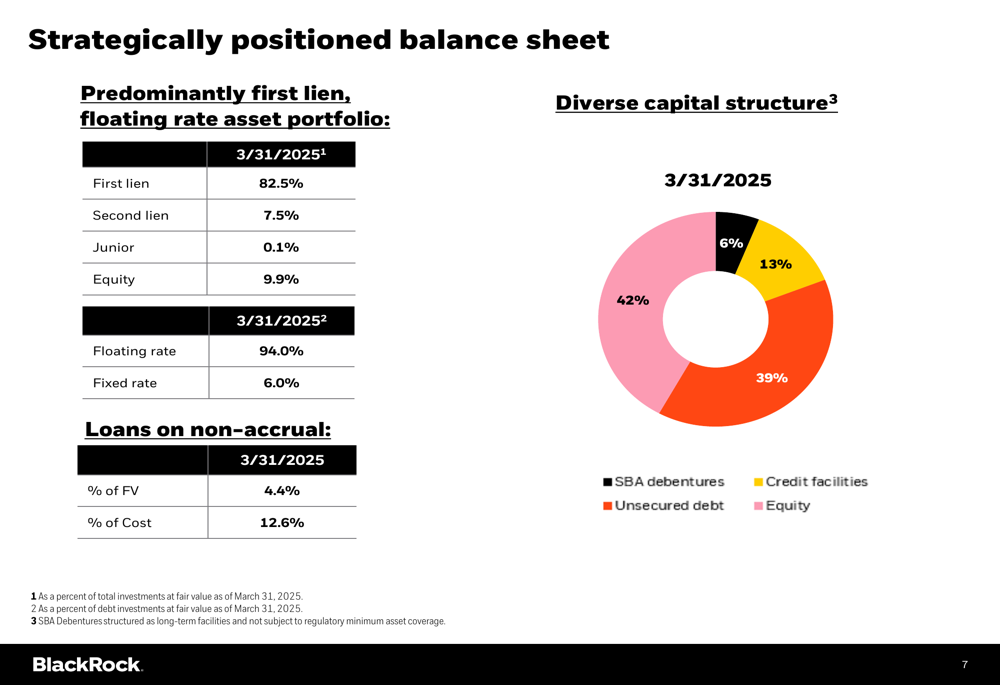

BlackRock TCP maintains a diversified portfolio with a strong emphasis on senior secured debt, which comprises 90% of investments, with 83% in first-lien positions. This conservative positioning reflects the company’s focus on capital preservation and consistent income generation.

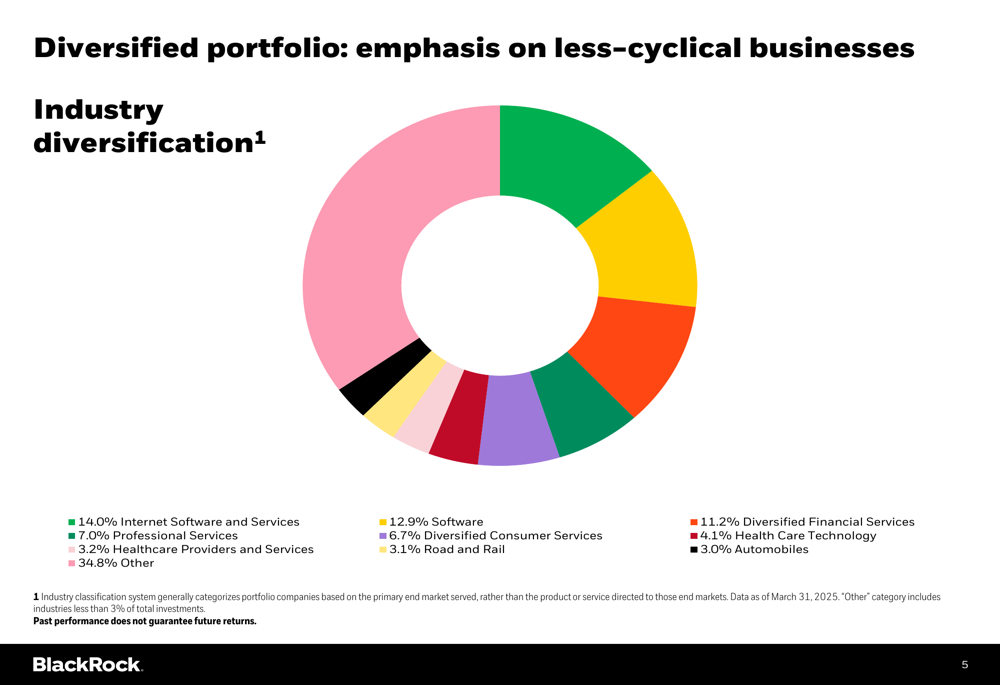

The portfolio’s industry diversification shows a significant allocation to technology sectors, with Internet Software (ETR:SOWGn) and Services (14.0%) and Software (12.9%) representing the largest exposures, followed by Diversified Financial Services at 11.2%:

The weighted average yield on the performing debt portfolio was 12.2% as of Q1 2025, representing a slight decrease from the 12.4% reported in Q4 2024. This yield compression reflects the broader interest rate environment as markets anticipate potential rate cuts.

The company’s portfolio quality metrics show some stress, with loans on non-accrual representing 4.4% of the portfolio by fair value and 12.6% by cost. The weighted average internal portfolio risk rating stands at 1.51x on a scale of 1-4, where 1 represents the lowest risk.

TCPC emphasizes its focus on less-cyclical businesses and robust downside analysis in its underwriting process:

Dividend Strategy and History

One of the most compelling aspects of BlackRock TCP’s investment case is its consistent dividend coverage history. The company has maintained dividend coverage with net investment income every quarter since its IPO in 2012, as illustrated in the following chart:

For Q2 2025, TCPC declared a regular dividend of $0.25 per share and a special dividend of $0.04 per share, both payable on June 30, 2025. This follows a special dividend of $0.10 per share paid in Q1 2025, continuing the company’s practice of returning excess earnings to shareholders.

The presentation highlights that 2024 saw total dividends of $1.71 per share ($1.36 regular + $0.35 special), representing a substantial yield based on current share prices. The company’s ability to maintain and supplement its regular dividend reflects the strength of its core earnings despite market challenges.

Balance Sheet and Liquidity

BlackRock TCP maintains a strategically positioned balance sheet with a diverse capital structure. As of March 31, 2025, the company’s capital structure consisted of 42% equity, 39% unsecured debt, 13% credit facilities, and 6% SBA (LON:SBA) debentures:

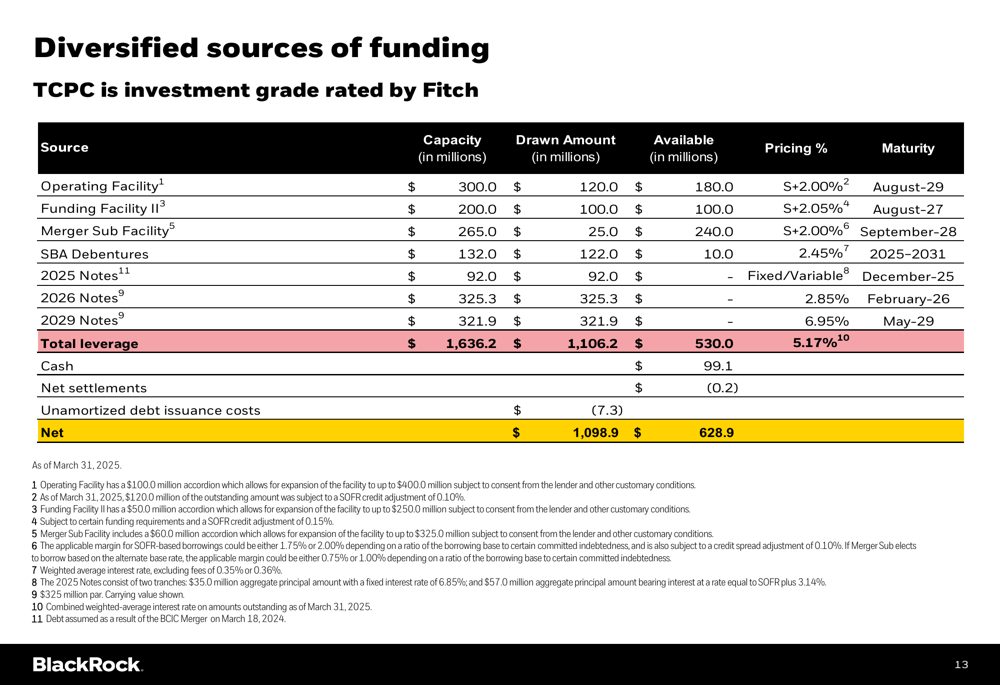

The company’s leverage program totals $1.6 billion, with 67% of outstanding leverage being unsecured. The net regulatory leverage ratio stands at 1.13x, providing room under regulatory limits while maintaining an investment-grade rating from Fitch.

TCPC reported $629 million of available liquidity, providing significant dry powder for new investments as opportunities arise. The company’s funding sources are well-diversified across multiple facilities with staggered maturities:

Forward-Looking Statements

Looking ahead, BlackRock TCP is leveraging its position within the broader BlackRock platform, which includes $63 billion in assets under management across private debt classes globally and over 170 private debt professionals. This scale provides TCPC with significant competitive advantages in sourcing, due diligence, and risk management.

The company’s management has emphasized its cycle-tested approach and focus on maintaining a diversified portfolio of senior secured loans to less-cyclical businesses. With its strong dividend coverage, substantial liquidity, and conservative portfolio positioning, TCPC appears well-positioned to navigate the current economic environment while continuing to deliver shareholder value through regular and special dividends.

However, investors should note the ongoing NAV erosion and the elevated level of non-accrual loans, which represent potential headwinds to future performance. The stock’s current trading level, well below its 52-week high, suggests market concerns about these challenges despite the company’s consistent income generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.