United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Boliden AB (STO:BOL) presented its Q2 2025 interim results on July 18, highlighting strong operational performance despite significant currency challenges. The Swedish mining and smelting company reported a robust free cash flow of SEK 2,035 million (excluding acquisition costs), up significantly from SEK 401 million in the same period last year, even as operating profit declined.

The quarter was marked by a SEK 600 million negative currency impact compared to both the previous quarter and year-on-year, reflecting broader market challenges that have affected the metals sector. Metal prices showed mixed performance during the period, with weaker zinc prices offset by stronger precious metal prices, while copper treatment charges faced continued pressure.

Quarterly Performance Highlights

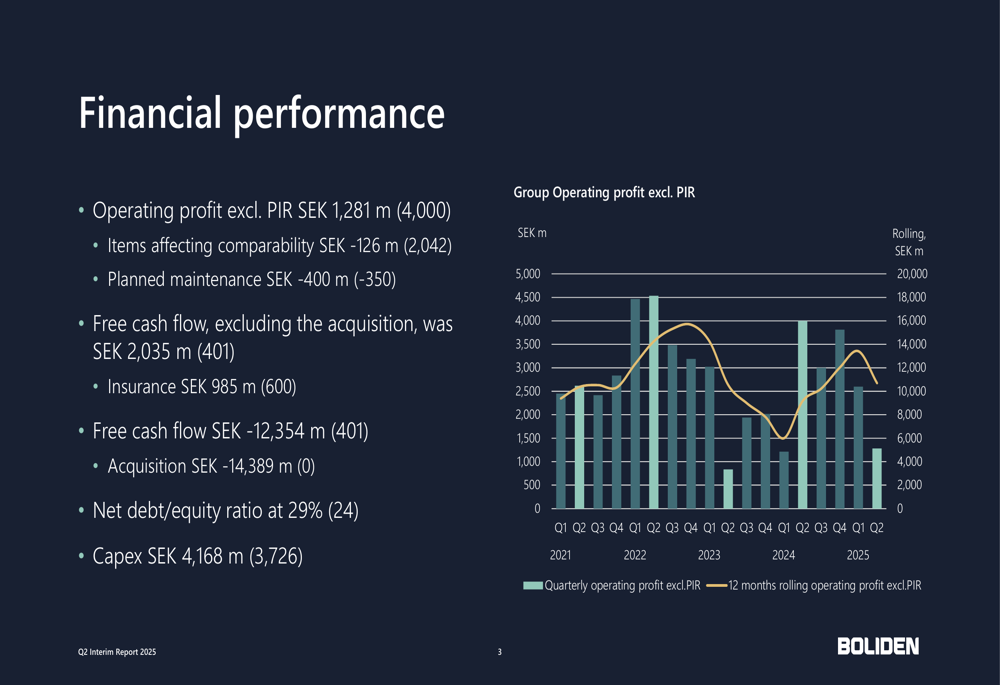

Boliden reported operating profit excluding process inventory revaluation (PIR) of SEK 1,281 million for Q2 2025, down significantly from SEK 4,000 million in Q2 2024. Despite this decline, the company achieved record mine production at its Aitik operation and maintained stable production across its portfolio.

The mining segment contributed SEK 1,035 million to operating profit, while the smelters segment added SEK 585 million. These figures represent a substantial year-on-year decline for smelters (from SEK 3,084 million) while mining remained relatively stable compared to Q2 2024 (SEK 1,118 million).

The company completed the acquisition of Somincor and Zinkgruvan mines during the quarter, with both operations included in financial results since April 16. This strategic expansion contributed to the company’s production volumes but also increased net debt, with the acquisition cost amounting to SEK 14,389 million.

Detailed Financial Analysis

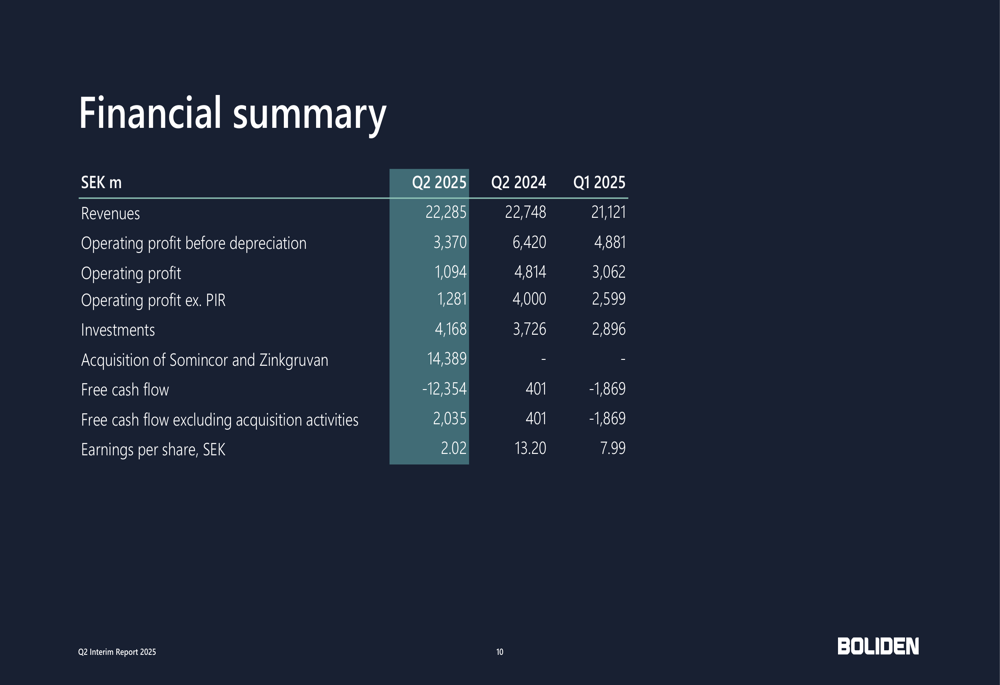

Boliden’s financial performance in Q2 2025 reflects both operational strengths and market challenges. The company’s revenue reached SEK 22,285 million, slightly down from SEK 22,748 million in Q2 2024. Operating profit before depreciation was SEK 3,370 million, compared to SEK 6,420 million in the same period last year.

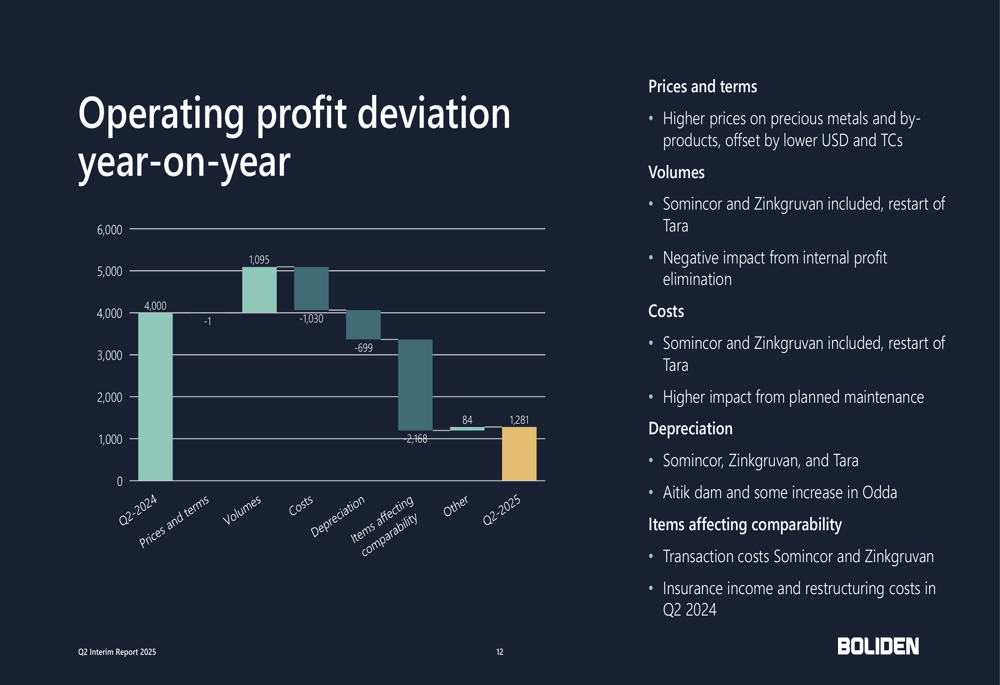

The year-on-year profit decline was primarily driven by lower metal prices and terms (SEK -4,000 million impact), increased costs (SEK -1,030 million), higher depreciation (SEK -699 million), and items affecting comparability (SEK -2,168 million). These negative factors were partially offset by improved volumes, which contributed SEK 1,095 million to operating profit.

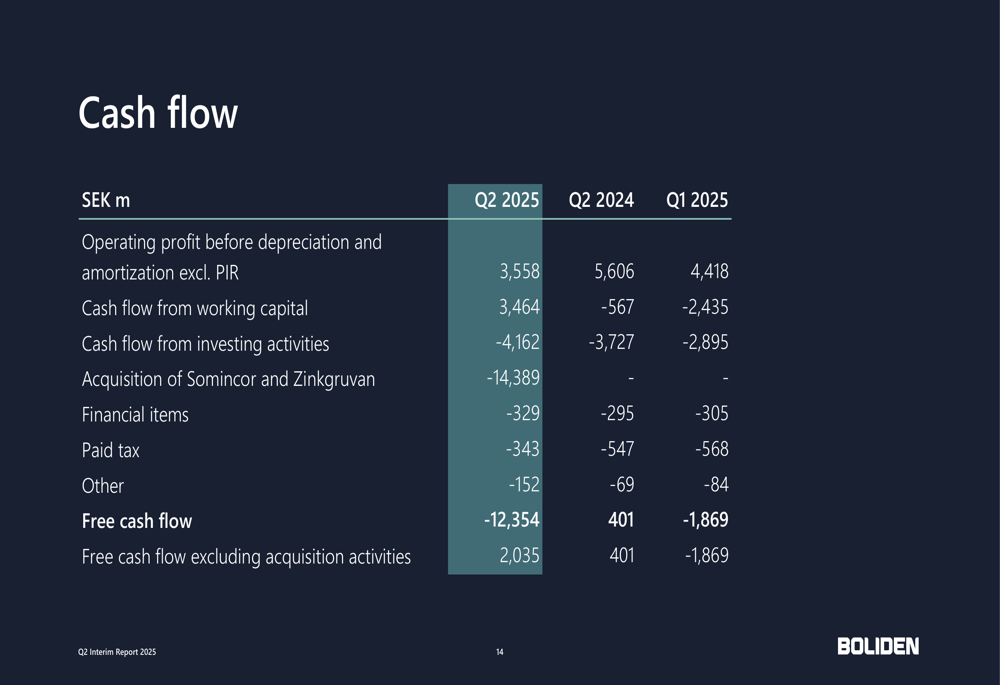

Cash flow performance was particularly strong, with cash flow from working capital contributing SEK 3,464 million, a significant improvement from SEK -567 million in Q2 2024. This helped offset the impact of acquisition activities and resulted in a free cash flow (excluding acquisitions) of SEK 2,035 million.

Strategic Initiatives & Acquisitions

The quarter saw significant strategic developments for Boliden, most notably the acquisition of Somincor and Zinkgruvan mines. This expansion has increased the company’s production capacity while maintaining a manageable net debt to equity ratio of 29%, up from 24% in Q2 2024.

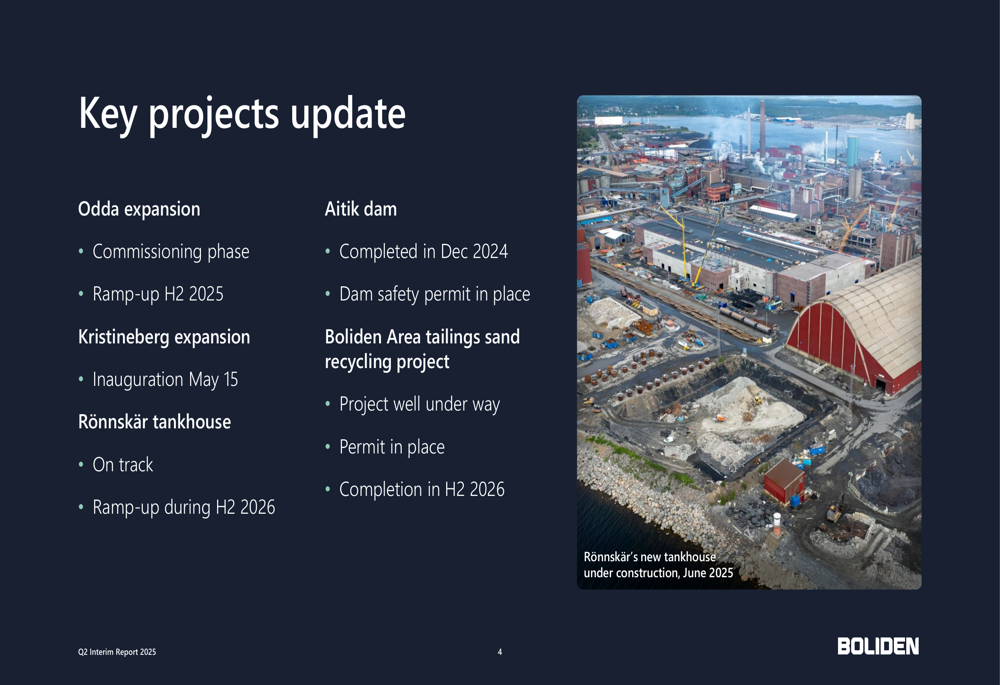

Several key projects continued to progress during the quarter. The Odda expansion has entered its commissioning phase, with ramp-up expected in H2 2025. The Kristineberg expansion was inaugurated on May 15, while the Rönnskär tankhouse project remains on track, with ramp-up scheduled for H2 2026. The Aitik dam project was completed in December 2024, with necessary permits now in place.

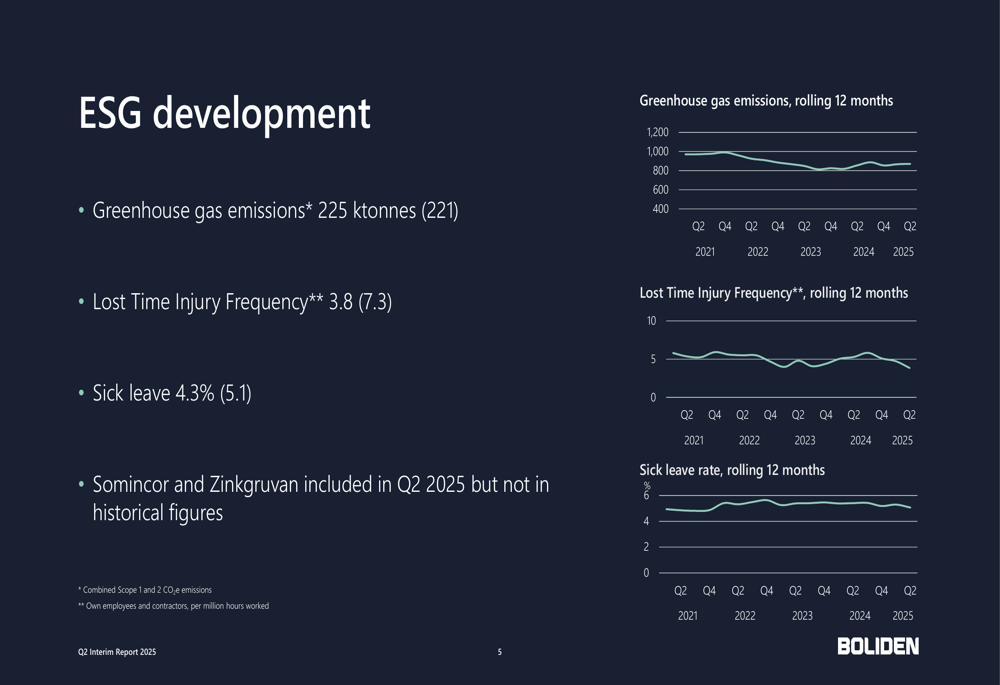

On the ESG front, Boliden reported greenhouse gas emissions of 225 ktonnes, slightly up from 221 ktonnes in the comparative period. However, the company made significant improvements in safety metrics, with Lost Time Injury Frequency decreasing to 3.8 from 7.3, and sick leave declining to 4.3% from 5.1%.

Forward-Looking Statements

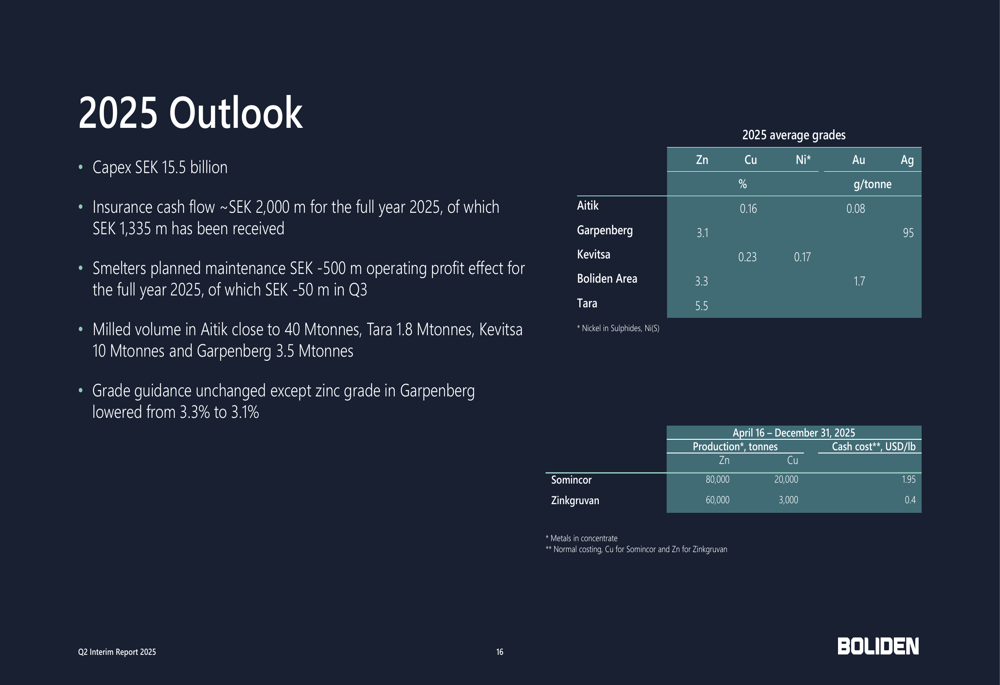

Looking ahead, Boliden provided guidance for the remainder of 2025, including capital expenditure of SEK 15.5 billion and expected insurance cash flow of approximately SEK 2,000 million for the full year. The company anticipates planned maintenance at its smelters to have a SEK -500 million impact on operating profit.

For the Aitik mine, Boliden expects milled volume to approach 40 million tonnes for the year. The company also provided detailed information on expected average grades across its mining operations, reflecting its confidence in operational performance despite market uncertainties.

CEO Mikael Staffas expressed confidence in the company’s position during the earnings call, stating, "We feel stronger than we’ve done in a long time." However, he also highlighted concerns about the sustainability of current copper treatment charges, suggesting potential industry adjustments may be necessary.

The market response to Boliden’s Q2 results was slightly negative, with the stock declining 1.34% following the announcement, closing at SEK 418.6, though this remains near the company’s 52-week high of SEK 418.6. The current price represents a significant recovery from the 52-week low of SEK 259.4, reflecting overall investor confidence in Boliden’s long-term strategy despite quarterly fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.