Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Bowhead Specialty Holdings Inc (NYSE:BOW) presented its Q1 2025 results on May 6, 2025, highlighting continued growth in the expanding Excess and Surplus (E&S) insurance market. The company, founded and led by industry veteran Stephen Sills, has positioned itself as a specialty Property & Casualty insurer with a focus on underwriting complex risks.

Trading at $41.30 as of May 5, 2025, Bowhead’s stock sits near its 52-week high of $42.29, reflecting investor confidence in the company’s growth trajectory. However, premarket trading on May 6 showed a 2.18% decline to $40.40, suggesting some caution ahead of the presentation.

Q1 2025 Performance Highlights

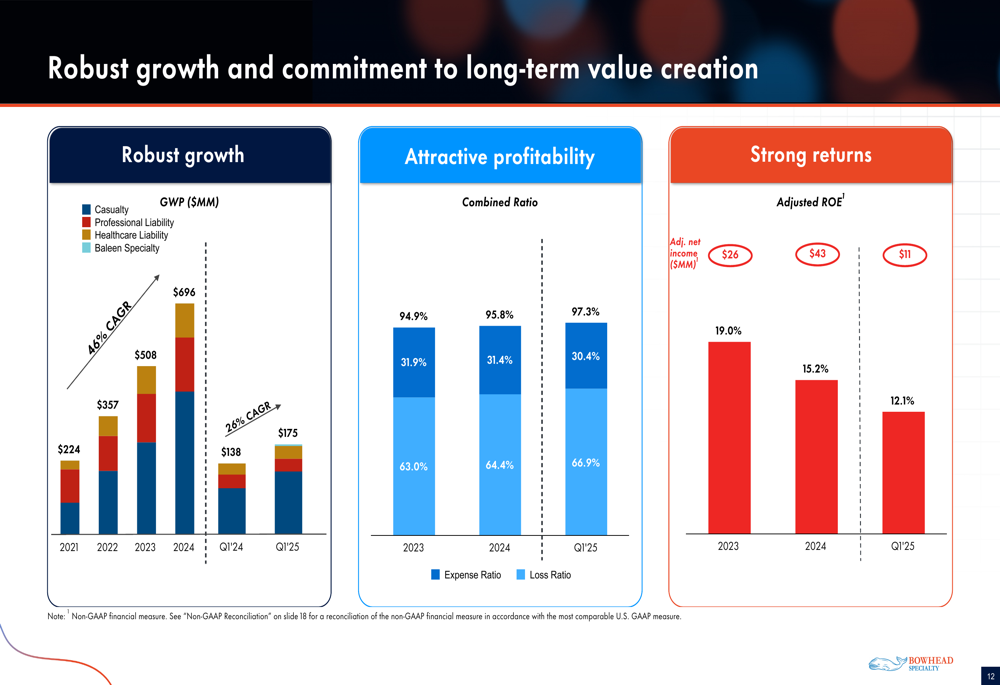

Bowhead reported strong premium growth in Q1 2025, with Gross Written Premiums (GWP) reaching $175 million, a 26% increase compared to Q1 2024’s $138 million. This continues the company’s impressive growth trajectory, with GWP expanding from $224 million in 2021 to $696 million in 2024, representing a 46% compound annual growth rate (CAGR).

As shown in the following financial performance chart, while top-line growth remains robust, profitability metrics show some signs of pressure:

The company’s combined ratio for Q1 2025 was 97.3%, showing deterioration from 95.8% for full-year 2024 and 94.9% for 2023. This was driven primarily by an increase in the loss ratio to 66.9% in Q1 2025 from 64.4% in 2024. On a positive note, the expense ratio improved to 30.4% in Q1 2025 from 31.4% in 2024.

Adjusted Return on Equity (ROE) has also shown a downward trend, declining from 19.0% in 2023 to 15.2% in 2024, and further to 12.1% for Q1 2025. Adjusted net income for Q1 2025 was $11 million, compared to $43 million for the full year 2024.

Strategic Positioning in E&S Market

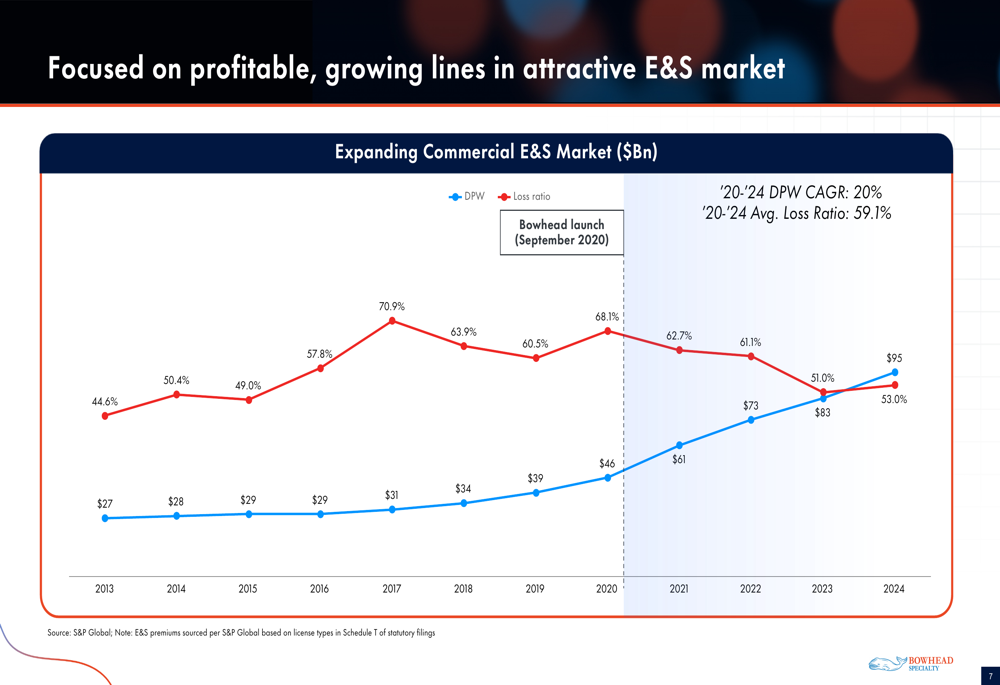

Bowhead has strategically positioned itself in the growing E&S insurance market, which has expanded significantly from $27 billion in 2013 to $95 billion in 2024, with a 20% CAGR from 2020 to 2024. The company’s presentation highlighted how this market expansion provides a favorable backdrop for continued growth.

The following chart illustrates the growth trajectory of the E&S market and loss ratio trends:

Bowhead’s business is heavily concentrated in the E&S segment, with 76% of its 2024 GWP written on an E&S basis. This positions the company among the leaders in E&S market exposure, second only to Kinsale Insurance (which writes 100% of its business in E&S) and well ahead of competitors like RLI (NYSE:RLI) and Palomar (both at 42%).

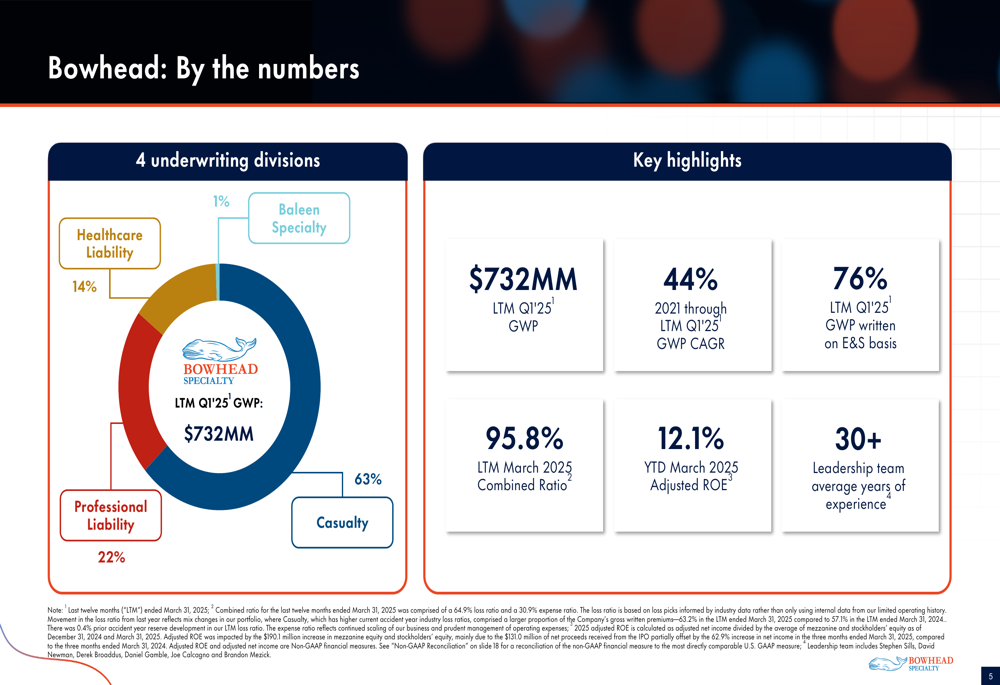

The company’s portfolio is diversified across four underwriting divisions, with Casualty representing the largest segment at 63% of premiums, followed by Professional Liability (22%), Healthcare Liability (14%), and the newly launched Baleen Specialty (1%).

As shown in the following breakdown of the company’s business segments and key metrics:

Business Model and Underwriting Approach

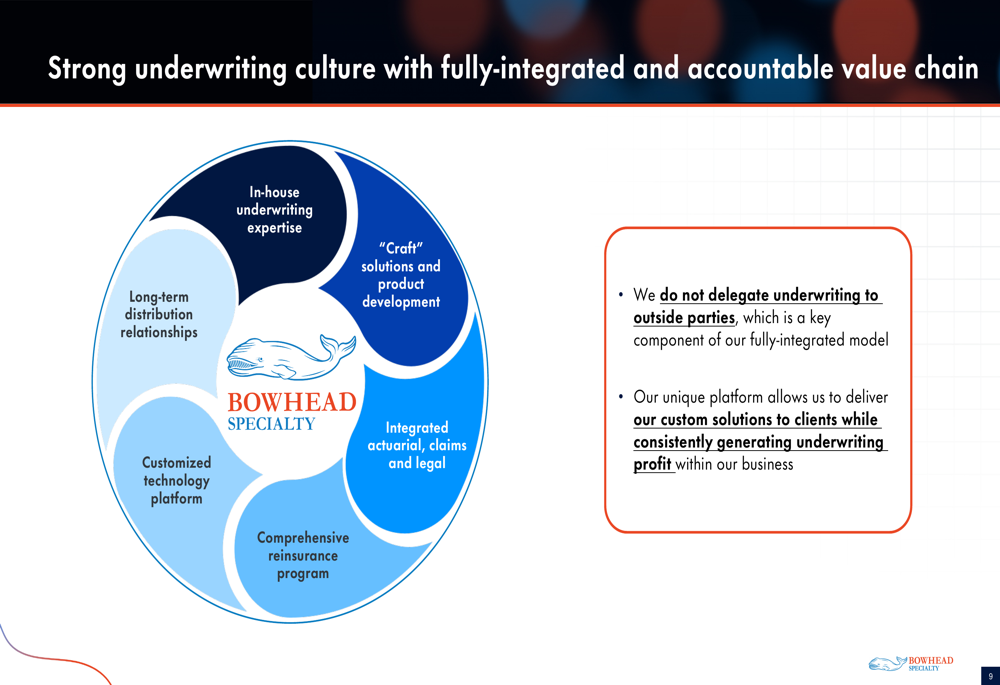

Bowhead emphasizes its "craft" underwriting approach, which focuses on individual, custom underwriting of large, complicated risks. This segment represents 99.4% of the company’s book as of March 2025. The company maintains a fully integrated underwriting model that does not delegate underwriting to outside parties.

The following diagram illustrates Bowhead’s integrated underwriting approach:

In Q2 2024, Bowhead launched "Baleen," a new "flow" business focused on streamlined, tech-enabled underwriting of small, hard-to-place E&S risks. While still a small portion of the overall business (1% of GWP), this initiative represents a strategic expansion beyond the company’s core specialty underwriting.

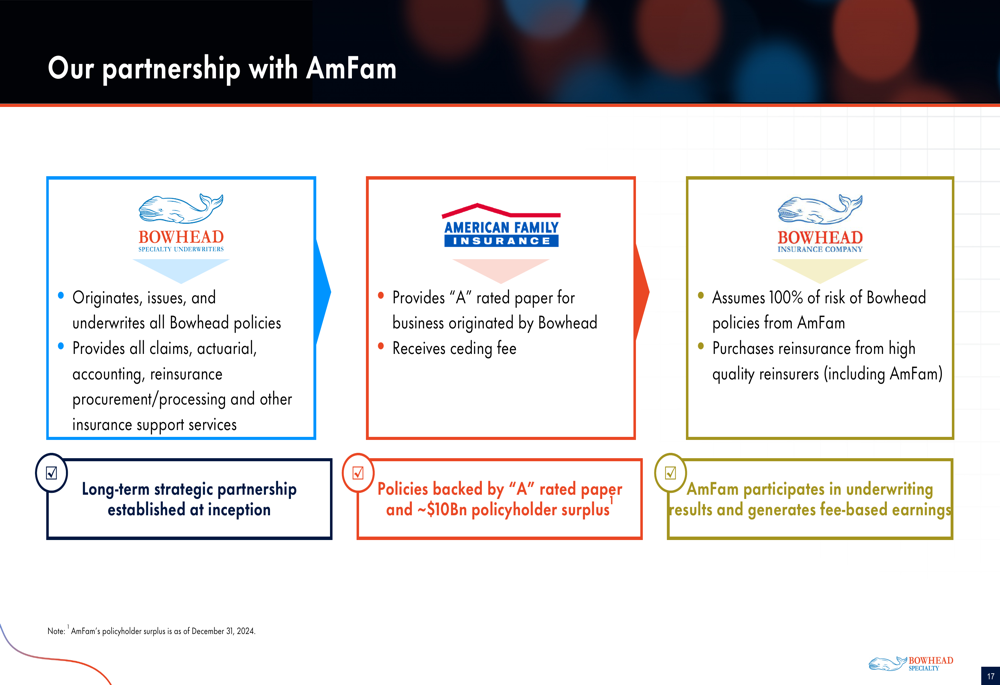

A key component of Bowhead’s business model is its strategic partnership with American Family Mutual Insurance Company (AmFam), which provides "A" rated paper for business originated by Bowhead. The structure of this relationship is illustrated below:

Financial Outlook and Challenges

Bowhead highlighted several strengths in its financial position, including a clean balance sheet with no reserves from accident years prior to 2020, no debt outstanding, and a conservative investment portfolio consisting entirely of cash, short-term investments, and investment-grade securities. The company reported a fixed income book yield of 4.7% and market yield of 4.8% as of March 31, 2025.

However, the presentation also revealed some challenges. The rising loss ratio (from 63.0% in 2023 to 66.9% in Q1 2025) and declining adjusted ROE (from 19.0% in 2023 to 12.1% in Q1 2025) suggest potential headwinds in maintaining profitability while pursuing aggressive growth.

Management, led by CEO Stephen Sills who has 48 years of industry experience, emphasized the company’s ability to deliver differentiated profitability across market cycles through its experienced team and disciplined underwriting culture. The leadership team averages over 30 years of experience, with executives previously holding senior positions at established insurers like Allied World, Markel (NYSE:MKL), and W.R. Berkley.

As Bowhead continues to expand in the growing E&S market, investors will be watching closely to see if the company can reverse the recent profitability trends while maintaining its impressive growth trajectory. The stock’s current trading level near its 52-week high suggests investor confidence in the company’s long-term prospects, despite the short-term profitability challenges highlighted in the Q1 2025 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.