IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Bowman Consulting Group Ltd (NASDAQ:BWMN) presented its first quarter 2025 earnings results on May 7, 2025, highlighting strong revenue growth and expanding backlog despite facing some profitability challenges. The infrastructure consulting firm reported significant year-over-year improvements across several key metrics while continuing to diversify its revenue streams across multiple sectors.

The company’s stock closed at $22.67 on May 6, 2025, showing a modest gain of 0.85% ahead of the earnings presentation, but remains well below its 52-week high of $36.65. Bowman’s Q1 results come after a strong Q4 2024 performance that had previously exceeded market expectations.

Quarterly Performance Highlights

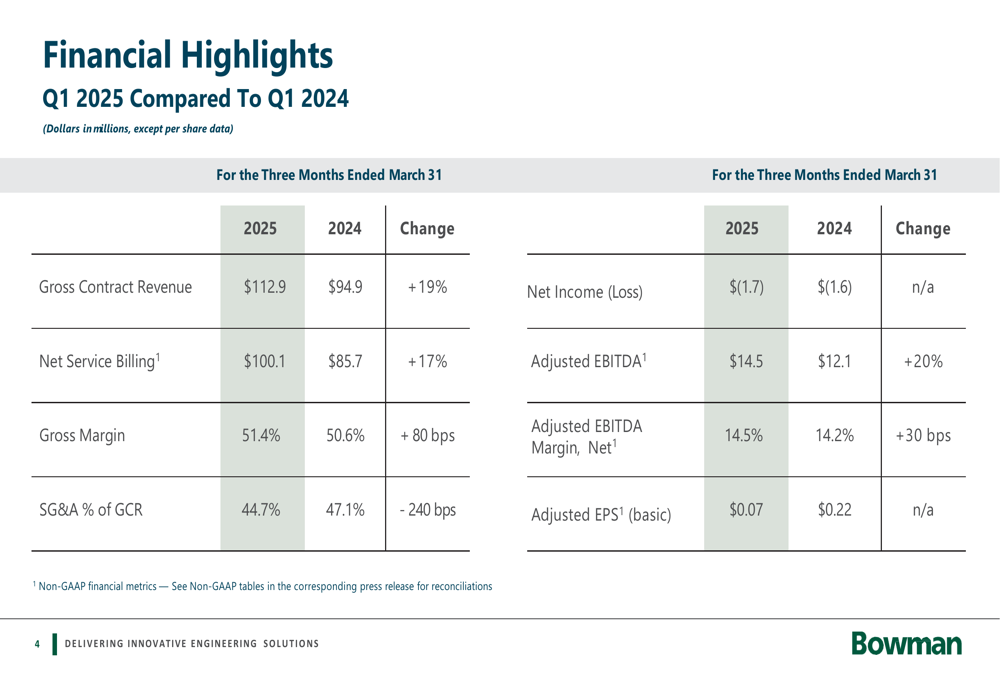

Bowman reported impressive top-line growth for the first quarter of 2025, with gross contract revenue increasing 19% year-over-year to $112.9 million, compared to $94.9 million in Q1 2024. Net service billing, a key non-GAAP metric that excludes sub-consultants and other direct expenses, grew 17% to $100.1 million.

As shown in the following financial highlights comparison:

The company improved its gross margin to 51.4%, up 80 basis points from 50.6% in the prior-year period. SG&A expenses as a percentage of gross contract revenue decreased significantly by 240 basis points to 44.7%. Adjusted EBITDA increased 20% to $14.5 million, with the adjusted EBITDA margin improving slightly to 14.5%.

Despite these positive trends, Bowman reported a net loss of $1.7 million for the quarter, slightly worse than the $1.6 million loss in Q1 2024. More concerning was the sharp decline in adjusted earnings per share, which fell to $0.07 from $0.22 in the prior-year period.

Revenue Diversification and Backlog Growth

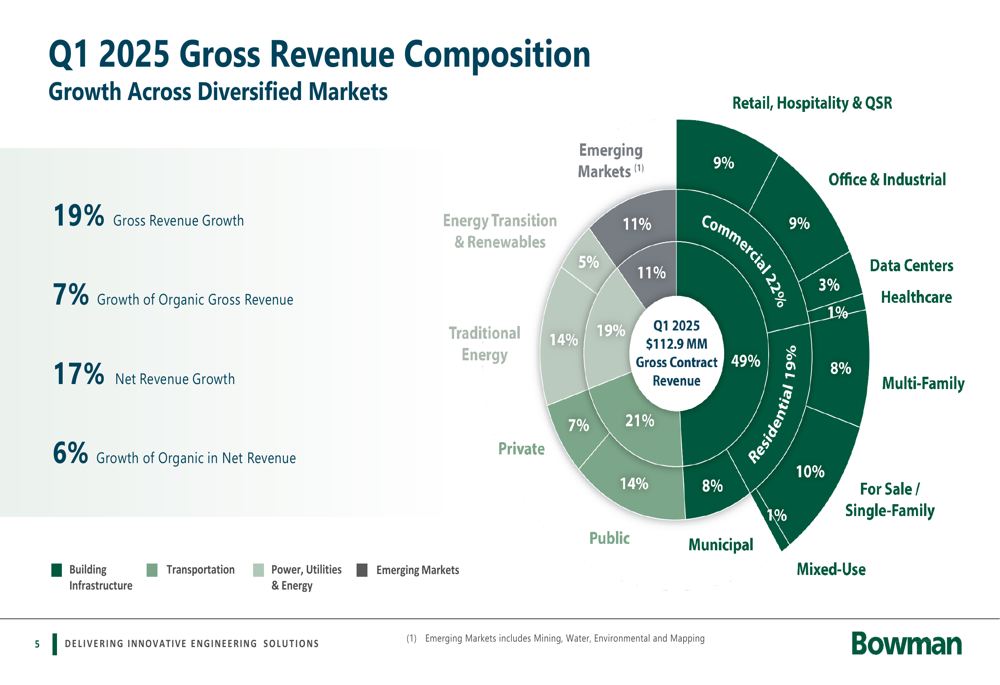

Bowman’s revenue composition demonstrates the company’s continued diversification across multiple sectors. Municipal projects represent the largest portion at 49% of gross contract revenue, followed by traditional energy (14%), energy transition and renewables (11%), and emerging markets (11%).

The company’s Q1 2025 revenue composition is illustrated in the following chart:

Organic growth was positive across all verticals, with transportation leading at 14.9%, followed by emerging markets at 9.6%, power and utilities at 5.8%, and building infrastructure at 2.3%. This diversification strategy appears to be providing resilience against sector-specific downturns.

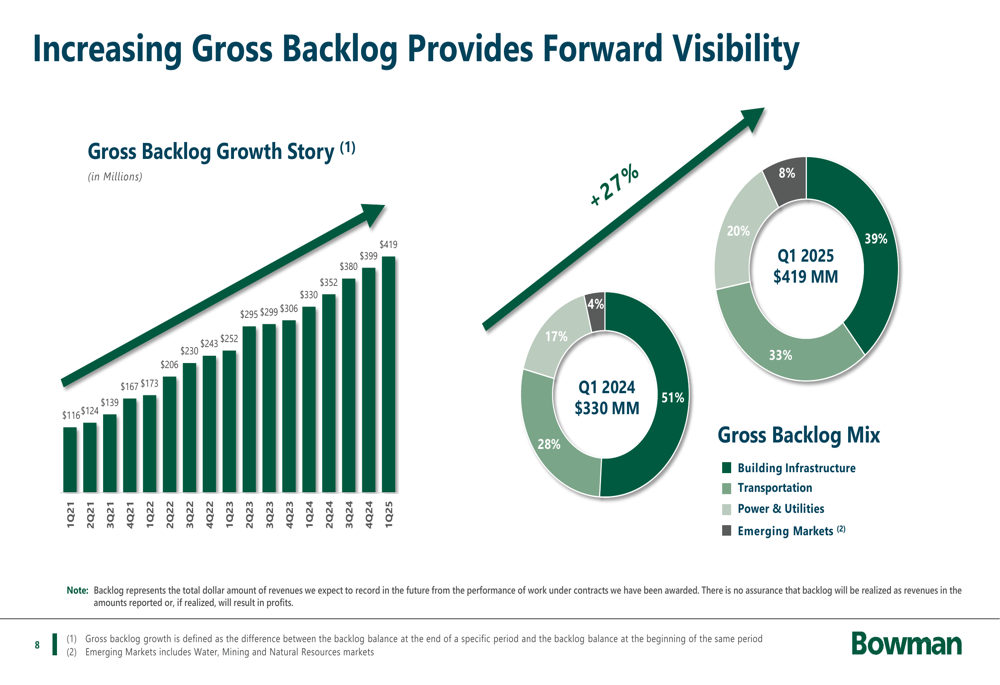

One of the most impressive aspects of Bowman’s Q1 results was the substantial growth in backlog, which provides strong forward visibility for future revenue. The company’s gross backlog reached $419 million in Q1 2025, representing a 30% increase from Q1 2024 and continuing a multi-year growth trend.

The backlog growth trajectory and composition are shown in the following chart:

The backlog mix is well-diversified, with building infrastructure representing 39%, emerging markets 33%, transportation 20%, and power and utilities 8%. This diverse backlog suggests continued revenue diversification in future quarters.

Balance Sheet and Capital Allocation

Bowman maintained a solid balance sheet position with $10.7 million in cash on hand and $97 million in net debt as of March 31, 2025. The company’s net leverage ratios stood at 1.6x trailing twelve months adjusted EBITDA and 1.3x based on forward midpoint adjusted EBITDA guidance.

Cash generation remained strong, with $12 million in cash from operating activities and $10.5 million in free cash flow during the quarter. The company achieved an impressive 83% cash conversion rate and 73% free cash flow conversion.

Bowman continued its share repurchase program, buying back $6.7 million of common stock during Q1 2025, with an additional $5.3 million repurchased by May 2, 2025. The company reported 17.3 million shares outstanding as of March 31, 2025, decreasing to 17.2 million by May 2, 2025.

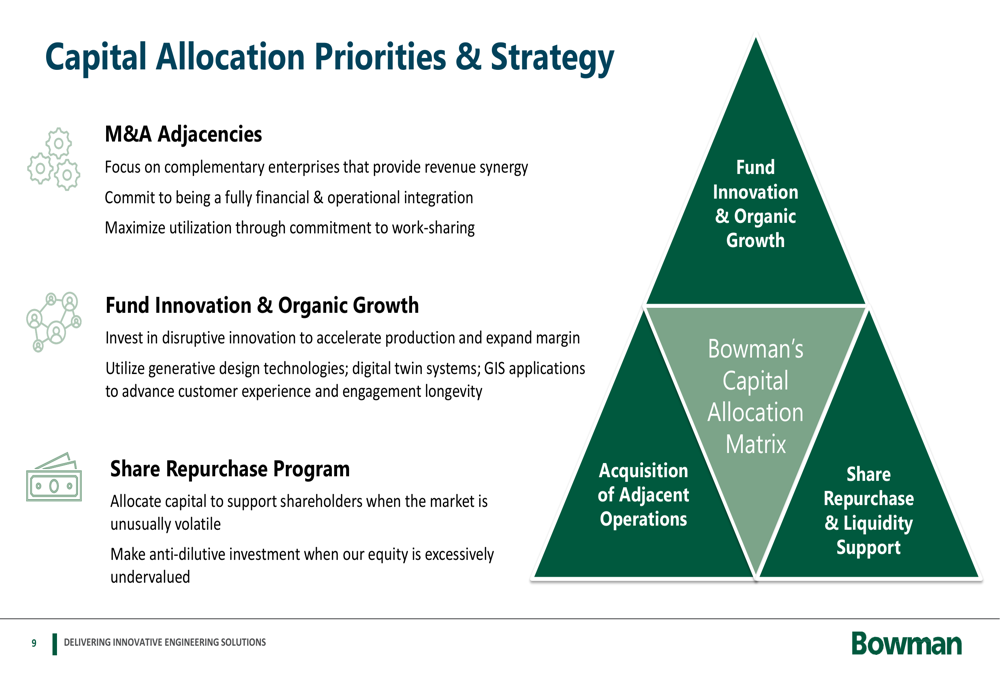

The company’s capital allocation strategy focuses on three key areas, as illustrated in the following slide:

End Market Performance

Bowman’s performance across different end markets showed significant variation in growth rates. The building infrastructure sector demonstrated the strongest growth at 117.9% year-over-year, albeit from a smaller base, now representing 11% of gross revenue. Transportation infrastructure grew 29.9% and accounts for 21% of revenue, while power, utilities and energy services increased 16.1%, making up 19% of revenue.

The company’s end market performance is detailed in the following slide:

Forward Guidance and Outlook

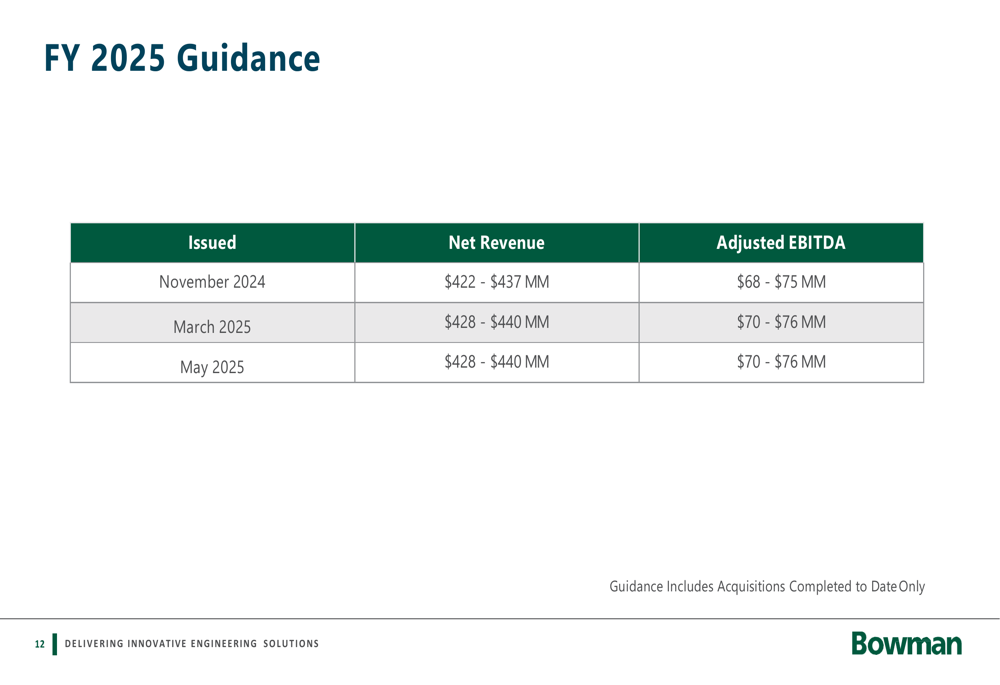

Bowman maintained its full-year 2025 guidance, projecting net revenue between $428 million and $440 million and adjusted EBITDA between $70 million and $76 million. This guidance includes only acquisitions completed to date and suggests continued confidence in the company’s growth trajectory.

The company’s guidance is summarized in the following table:

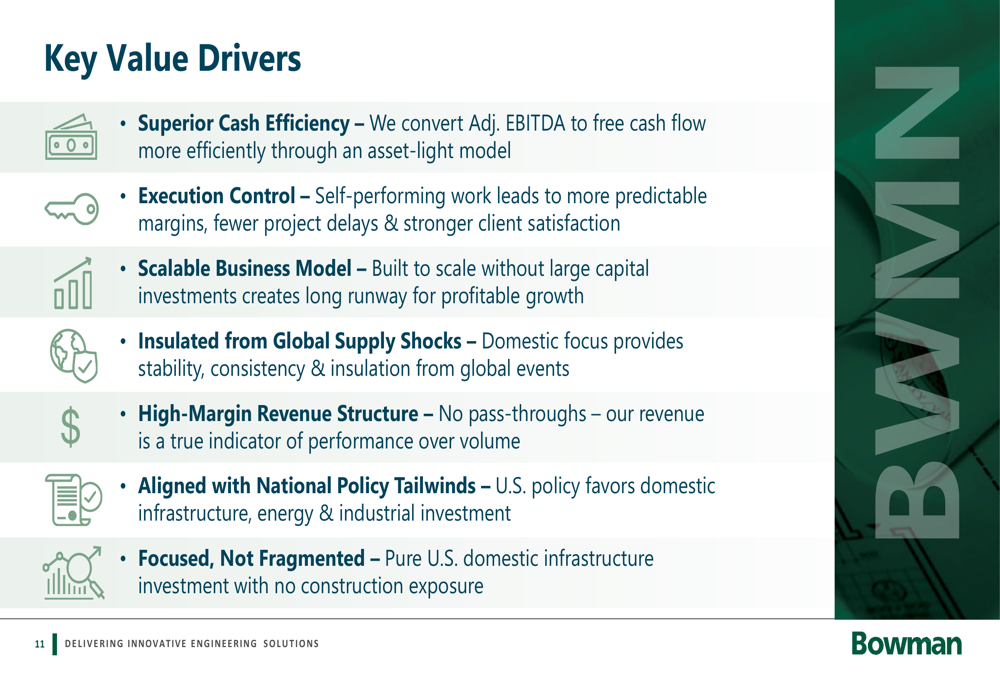

Bowman highlighted several key value drivers that position it for continued success, including superior cash efficiency through an asset-light model, execution control, a scalable business model, insulation from global supply shocks, a high-margin revenue structure, alignment with national policy tailwinds, and a focused approach to its markets.

These value drivers are illustrated in the following slide:

While Bowman’s Q1 2025 results demonstrated strong top-line growth and backlog expansion, the decline in adjusted EPS despite revenue and EBITDA growth raises questions about increasing costs or changes in the company’s capital structure. Investors will likely watch closely to see if this trend reverses in future quarters as the company continues to execute on its diversification and growth strategies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.