Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

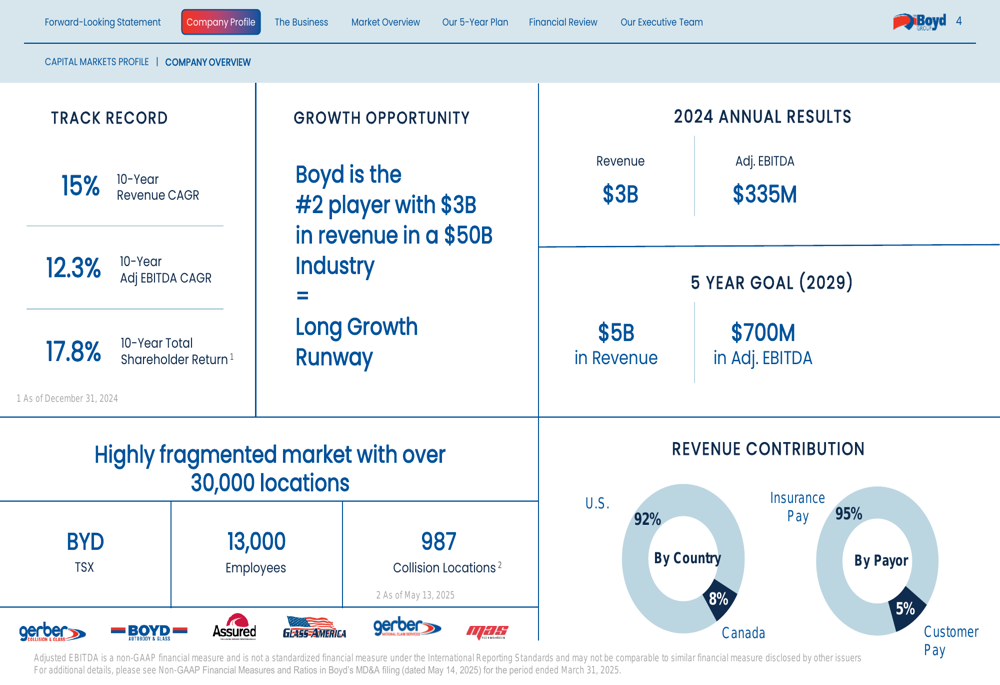

Boyd Group Services Inc (TSX:BYD) presented its investor update in May 2025, outlining ambitious growth targets amid challenging market conditions. As the second-largest player in the North American collision repair industry with approximately 7% market share, Boyd operates 987 collision locations across 34 U.S. states and 5 Canadian provinces. The company’s stock closed at C$211.78 on May 15, 2025, down 1.5% from the previous close, reflecting ongoing market volatility.

The presentation comes after Boyd reported modest Q1 2025 results, with sales growing just 1% year-over-year to $778.3 million while posting a net loss of CAD $2.6 million, compared to net earnings of CAD $8.4 million in the same quarter last year. Same-store sales declined by 2.8% in the quarter, continuing the negative trend from 2024.

Executive Summary

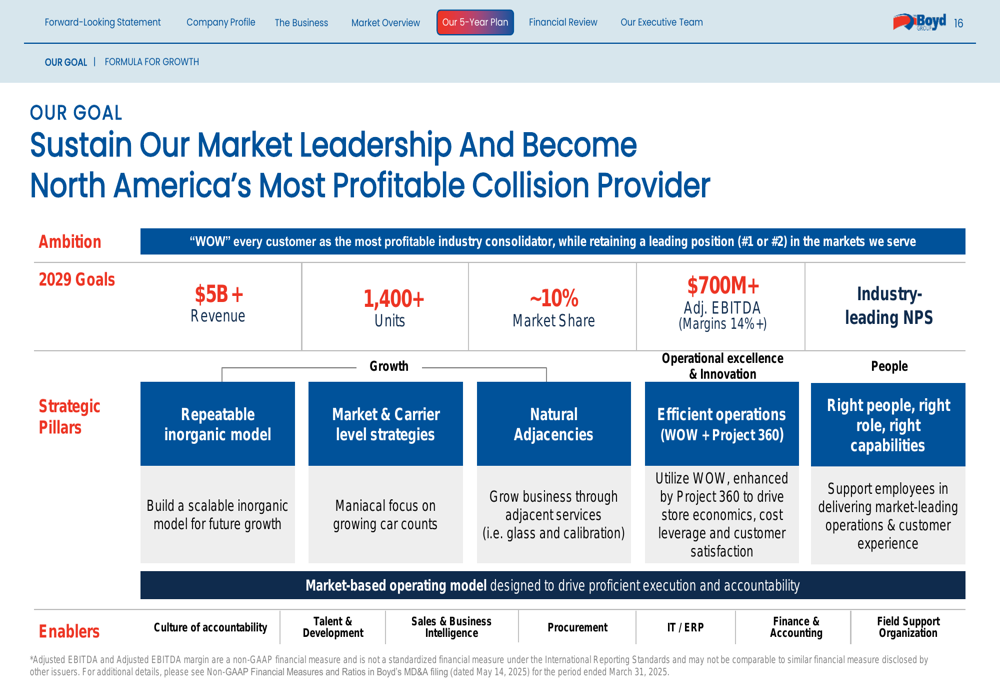

Boyd Group’s presentation highlighted its position in a highly fragmented $50 billion collision repair market, where the company currently generates approximately $3 billion in annual revenue. Management outlined a five-year goal to reach $5 billion in revenue and $700 million in adjusted EBITDA by 2029, nearly doubling current levels despite recent headwinds.

As shown in the following financial highlights chart, Boyd has maintained strong long-term growth metrics despite recent challenges:

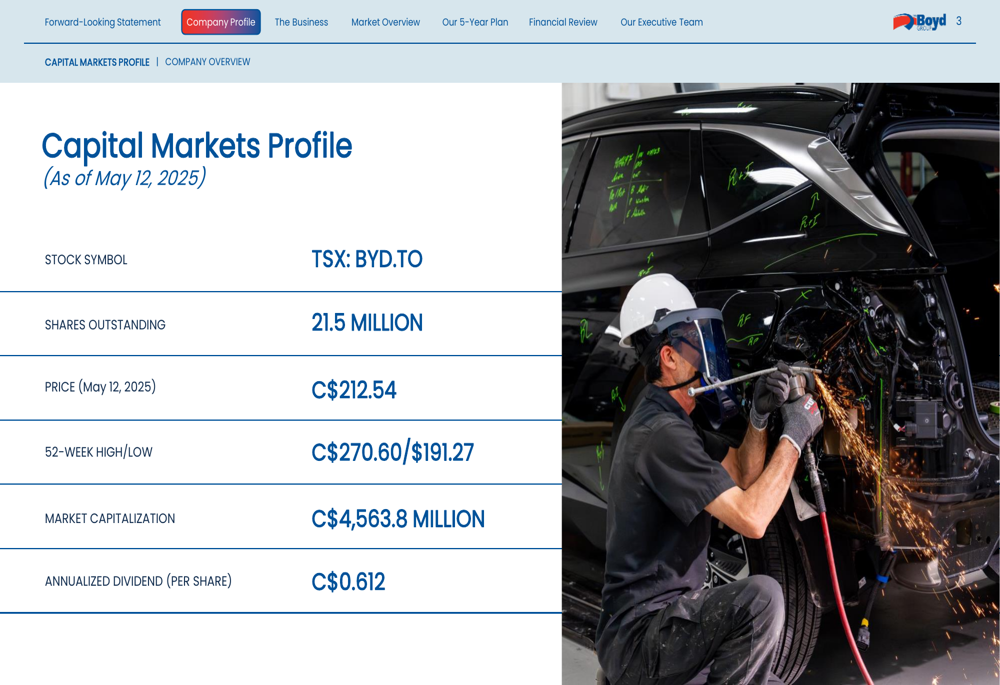

The company’s capital markets profile reveals a market capitalization of approximately C$4.56 billion as of mid-May 2025, with 21.5 million shares outstanding and an annualized dividend of C$0.612 per share:

Strategic Initiatives

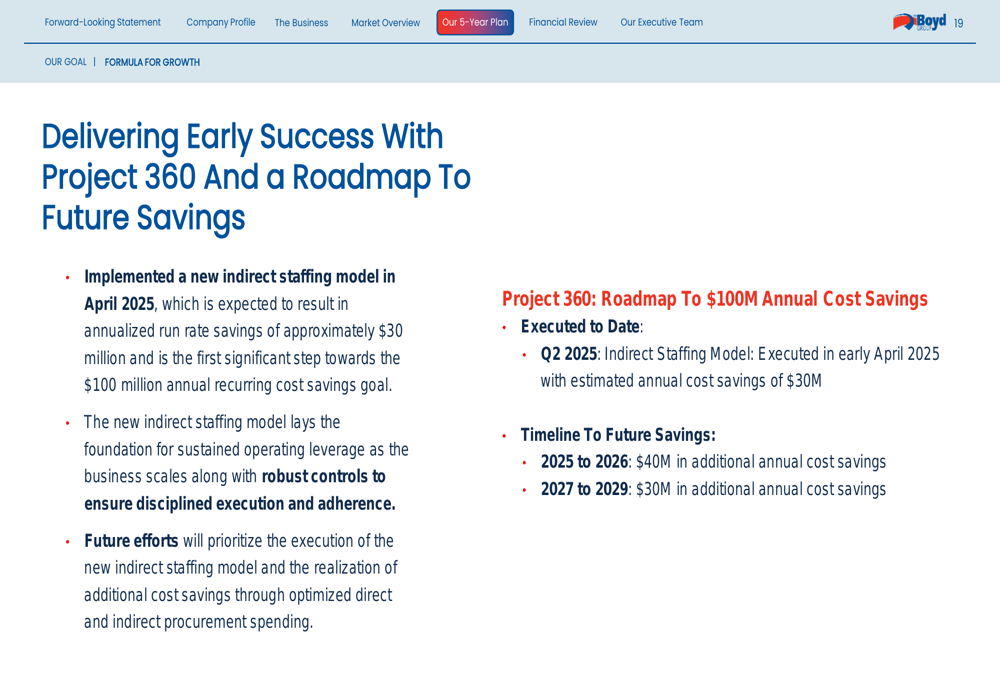

Central to Boyd’s growth strategy is "Project 360," a comprehensive cost-saving initiative launched in partnership with a leading global consulting firm. The program aims to deliver $100 million in annual cost savings by 2029, with the first phase already implemented in April 2025.

The company has provided a clear roadmap for achieving these savings, with $30 million in annualized run-rate savings already identified through a new indirect staffing model:

Boyd’s CEO Brian Kaner emphasized during the recent earnings call that despite market challenges, "We continue to outperform the market, consistently demonstrating market share gains." He noted that the broader market is expected to decline by approximately 2% in claims volume, driven by the increased penetration of Advanced Driver Assistance Systems (ADAS).

Detailed Financial Analysis

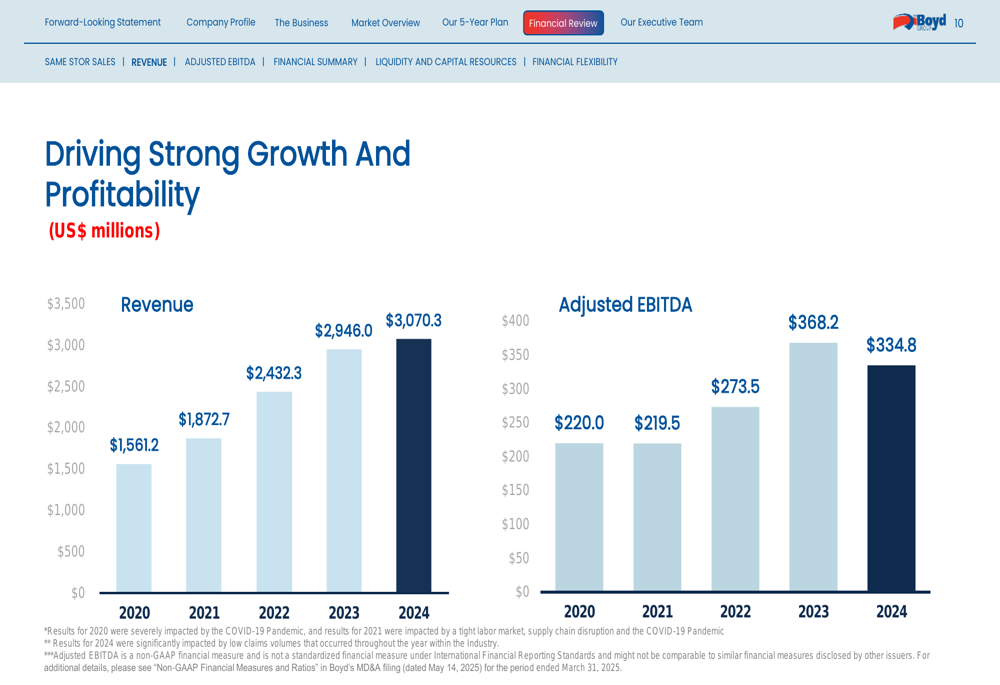

Boyd’s financial performance has shown strong long-term growth, with revenue increasing from $1.56 billion in 2020 to $3.07 billion in 2024, representing a compound annual growth rate of 15% over the past decade. However, adjusted EBITDA growth has been more modest in recent years, reaching $334.8 million in 2024:

Same-store sales growth has been volatile, with significant pandemic-related declines in 2020 (-15.6%), followed by strong recovery in 2022 (19.8%) and 2023 (15.8%), before turning negative again in 2024 (-1.8%) and continuing to decline in Q1 2025 (-2.8%):

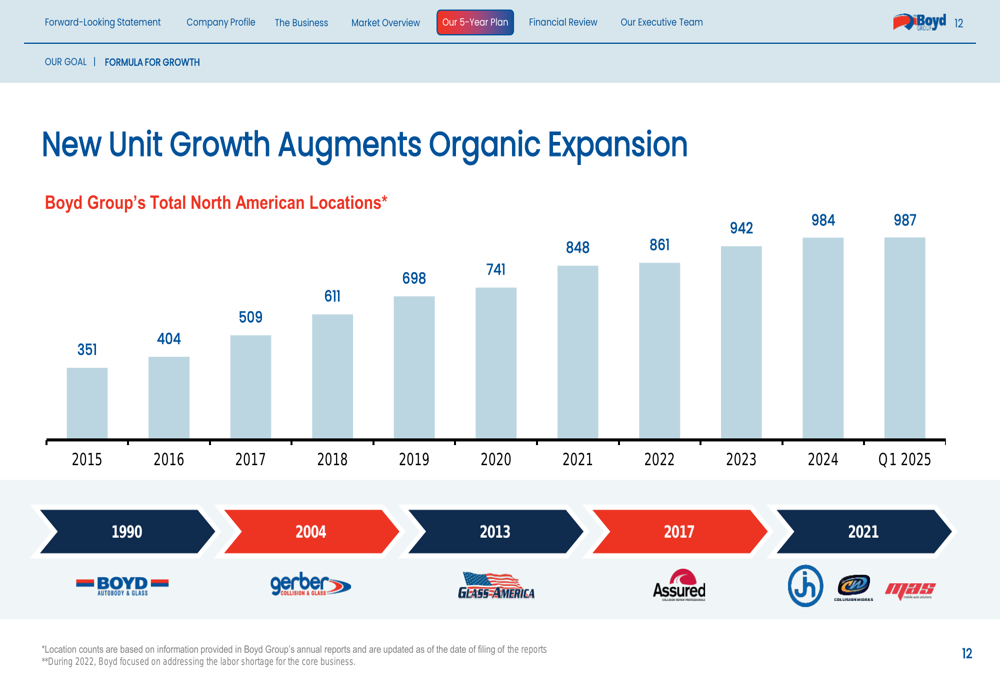

The company has steadily expanded its footprint, growing from 351 locations in 2015 to 987 in Q1 2025 through a combination of acquisitions and new store openings:

Competitive Industry Position

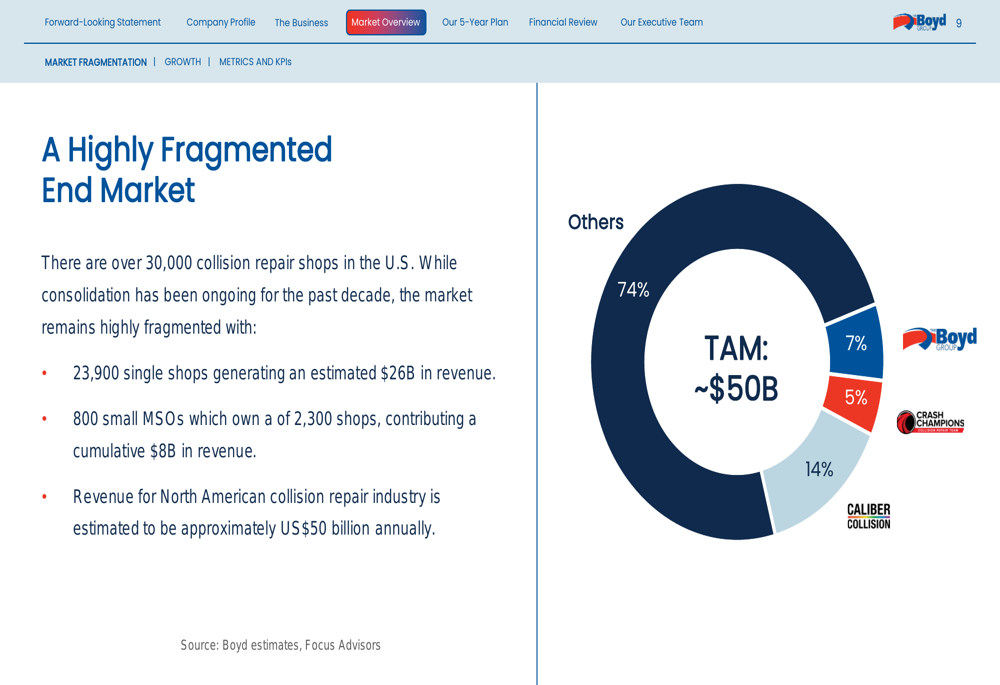

Boyd operates in a highly fragmented collision repair market with over 30,000 shops across North America. The company holds approximately 7% market share, positioning it as the second-largest player behind Caliber Collision (14%), with Crash Champions (5%) as the third major competitor:

This fragmentation presents significant consolidation opportunities, with nearly 24,000 single shops generating an estimated $26 billion in revenue. Boyd’s strategy leverages its strong relationships with insurance carriers, with its top five customers contributing 51% of revenue in 2024.

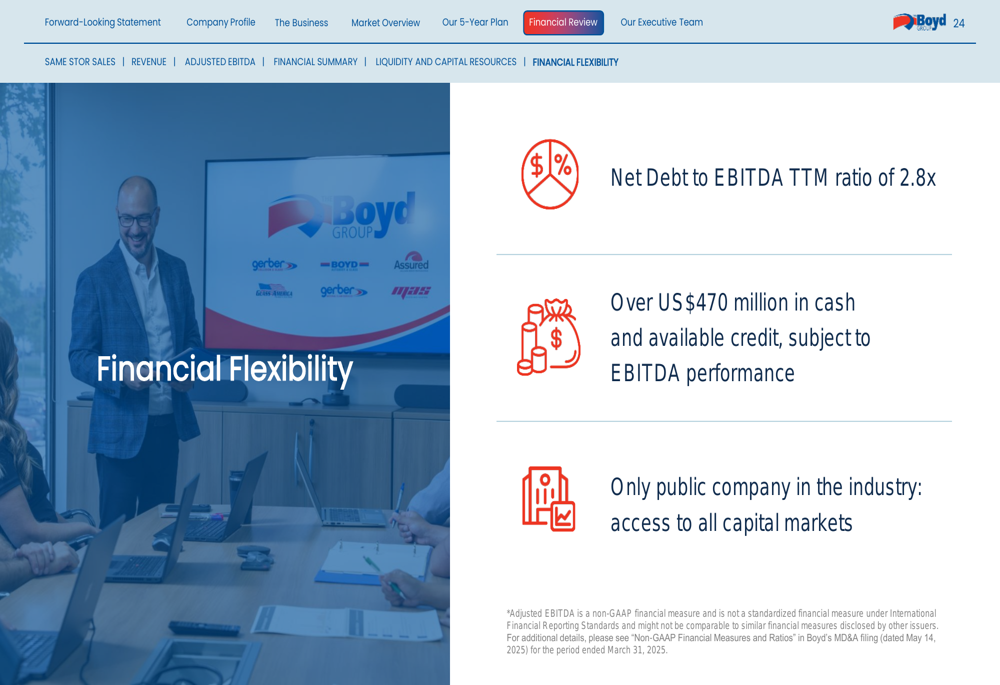

The company maintains a strong financial position to pursue growth opportunities, with a net debt to EBITDA ratio of 2.8x and over $470 million in cash and available credit:

Forward-Looking Statements

Boyd’s 2029 targets include reaching $5 billion in revenue, operating more than 1,400 locations, capturing approximately 10% market share, and generating over $700 million in adjusted EBITDA with margins exceeding 14%:

To achieve these goals, the company plans to allocate $150-200 million annually to acquisitions and growth capital expenditures, while maintaining 1.6-1.8% of revenue for maintenance capex and continuing modest dividend growth.

Management expects a gradual improvement in the claims environment and anticipates opening 80-100 new locations annually. However, these projections come amid current challenges, as evidenced by the Q1 2025 results showing minimal growth and margin pressure.

Conclusion

Boyd Group Services faces a challenging near-term environment with declining same-store sales and margin pressure, but maintains an ambitious long-term growth strategy focused on market consolidation and operational efficiency. The company’s Project 360 cost-saving initiatives will be critical to achieving its 2029 targets of $5 billion in revenue and $700 million in adjusted EBITDA.

As the second-largest player in a highly fragmented market, Boyd is well-positioned to capitalize on consolidation opportunities, supported by strong relationships with insurance carriers and a solid financial foundation. However, investors should monitor the execution of cost-saving measures and the recovery of same-store sales growth as key indicators of the company’s ability to achieve its ambitious five-year goals.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.