BofA update shows where active managers are putting money

Introduction & Market Context

Bravida Holding AB (STO:BRAV) presented its first quarter 2025 results on May 6, highlighting improved profitability despite challenging market conditions that led to a 5% decline in net sales. The Nordic technical installation and service provider saw its stock price drop 2.36% following the announcement, with shares trading at SEK 91.00, reflecting investor concerns about the continued weakness in the installation segment.

The company’s presentation emphasized its strategic focus on "margin over volume," which appears to be yielding results as EBITA margins improved across all countries despite the sales decline. Bravida’s diversified presence across Sweden, Norway, Denmark, and Finland has provided some insulation against regional market fluctuations.

Quarterly Performance Highlights

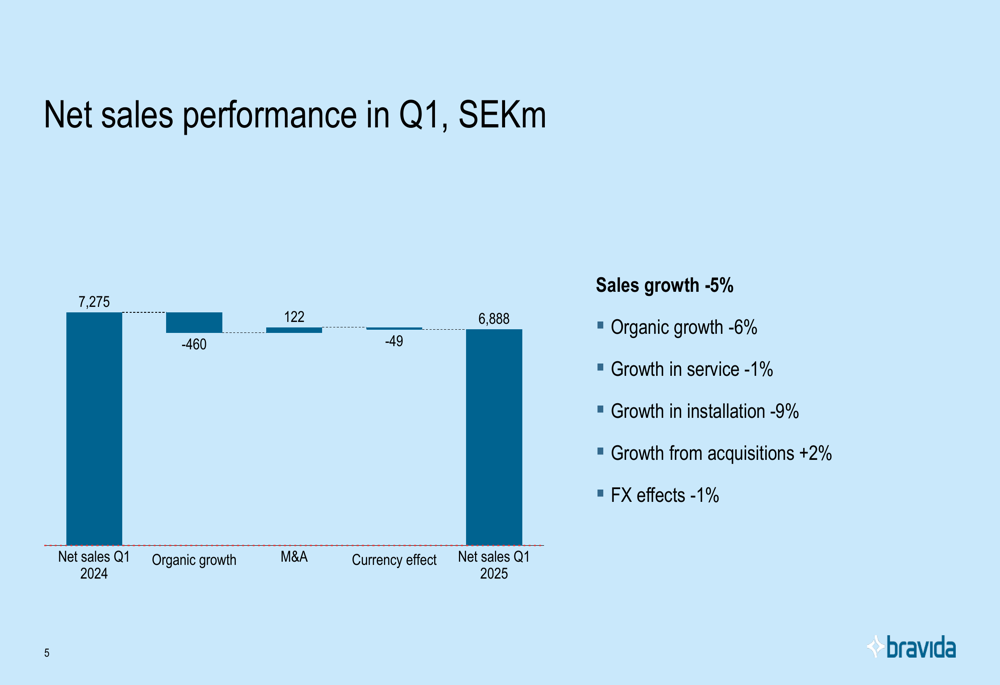

Bravida reported net sales of SEK 6,888 million for Q1 2025, down 5% from SEK 7,275 million in the same period last year. This decline was primarily driven by a 9% drop in installation sales, while service sales showed more resilience with only a 1% decrease. The company’s organic growth was -6%, partially offset by a 2% contribution from acquisitions, with currency effects accounting for a -1% impact.

As shown in the following chart of quarterly sales performance:

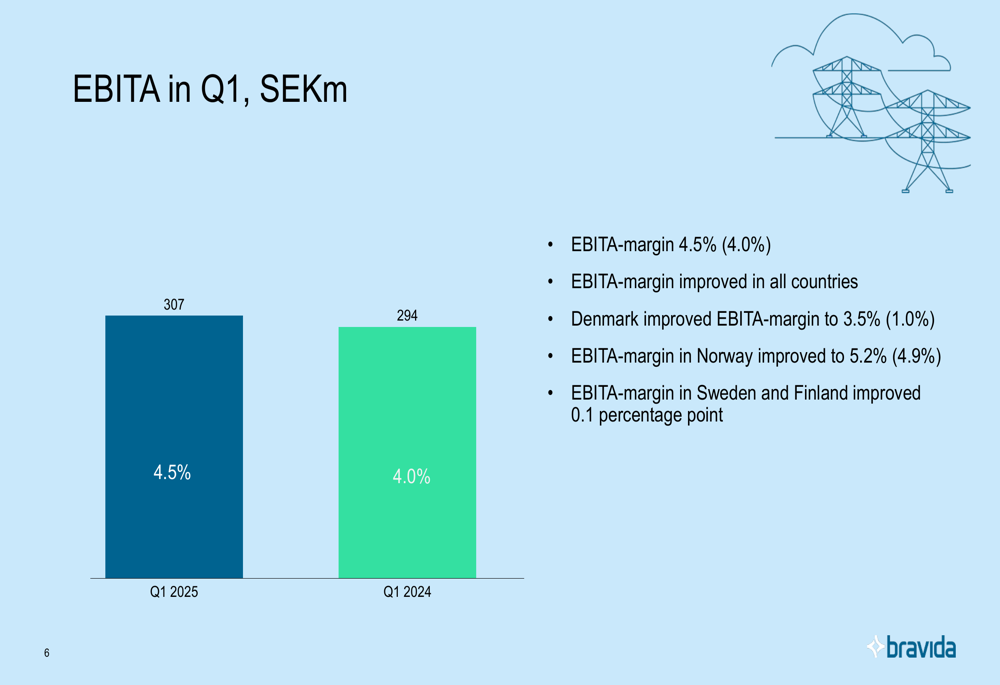

Despite the sales decline, Bravida improved its EBITA margin to 4.5% in Q1 2025, up from 4.0% in Q1 2024. This resulted in an EBITA of SEK 307 million, compared to SEK 294 million in the previous year. The margin improvement was particularly notable in Denmark, which saw its EBITA margin rise to 3.5% from just 1.0% a year earlier.

The following chart illustrates the EBITA performance:

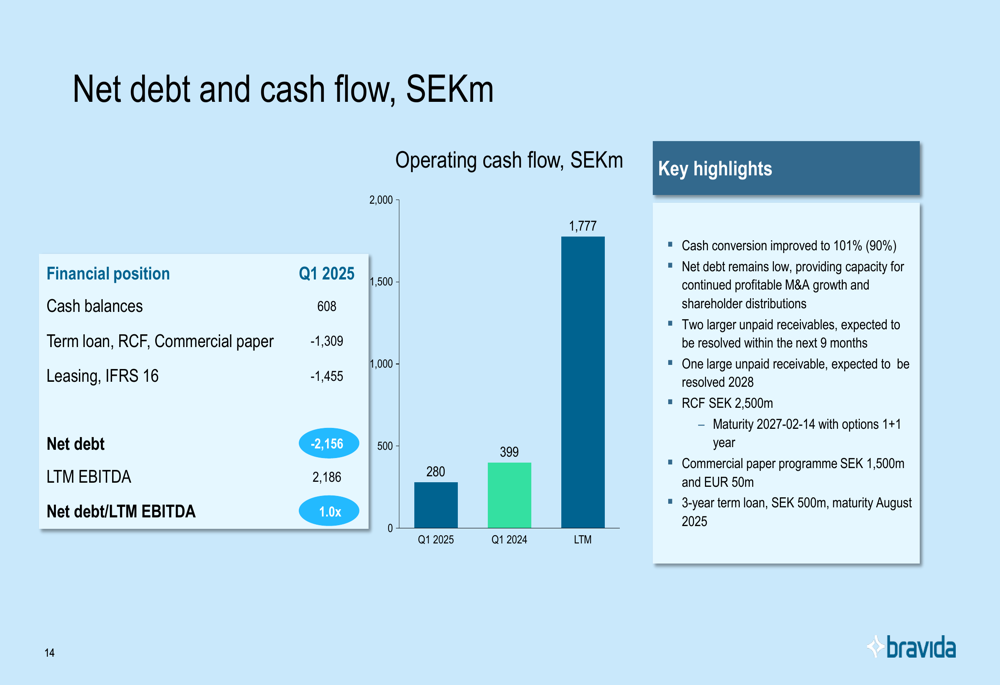

The company’s cash flow remained strong, with operating cash flow of SEK 280 million in Q1 2025. Cash conversion improved to 101% from 90% in the same period last year, while net debt remained low at 1.0x EBITDA, providing financial flexibility for future acquisitions and shareholder distributions.

Regional Performance Analysis

Bravida’s performance varied significantly across its four Nordic markets, with Denmark showing the strongest improvement while other countries faced more challenging conditions.

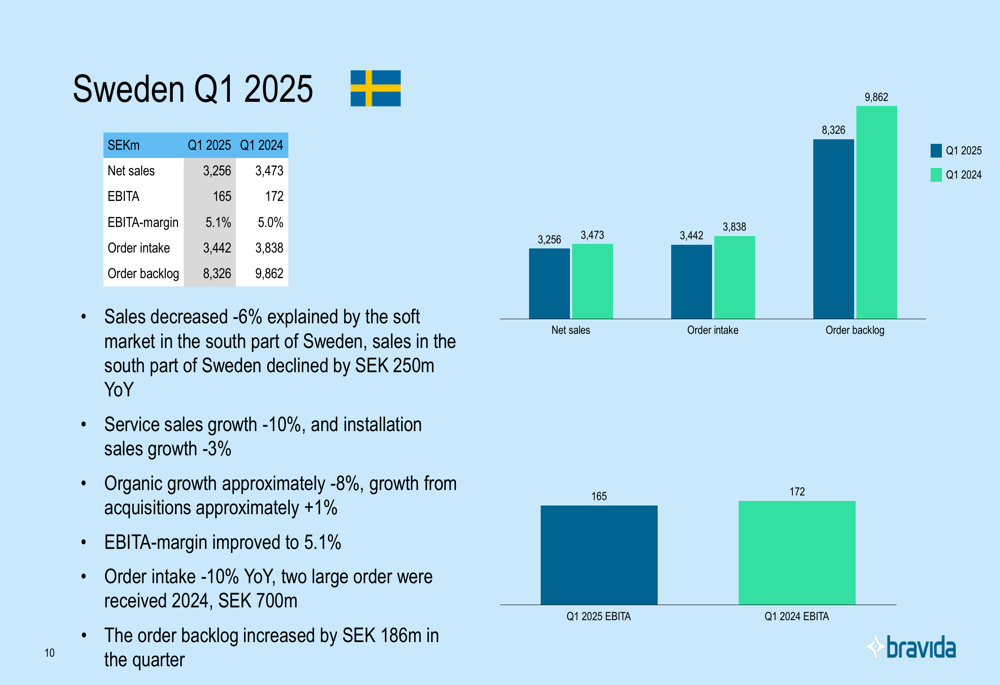

Sweden, the company’s largest market, saw sales decrease by 6% to SEK 3,256 million, primarily due to weakness in the southern part of the country, where sales declined by SEK 250 million year-over-year. Despite this, the EBITA margin improved slightly to 5.1% from 5.0%. Order intake decreased by 10% compared to Q1 2024, which had included two large orders worth SEK 700 million.

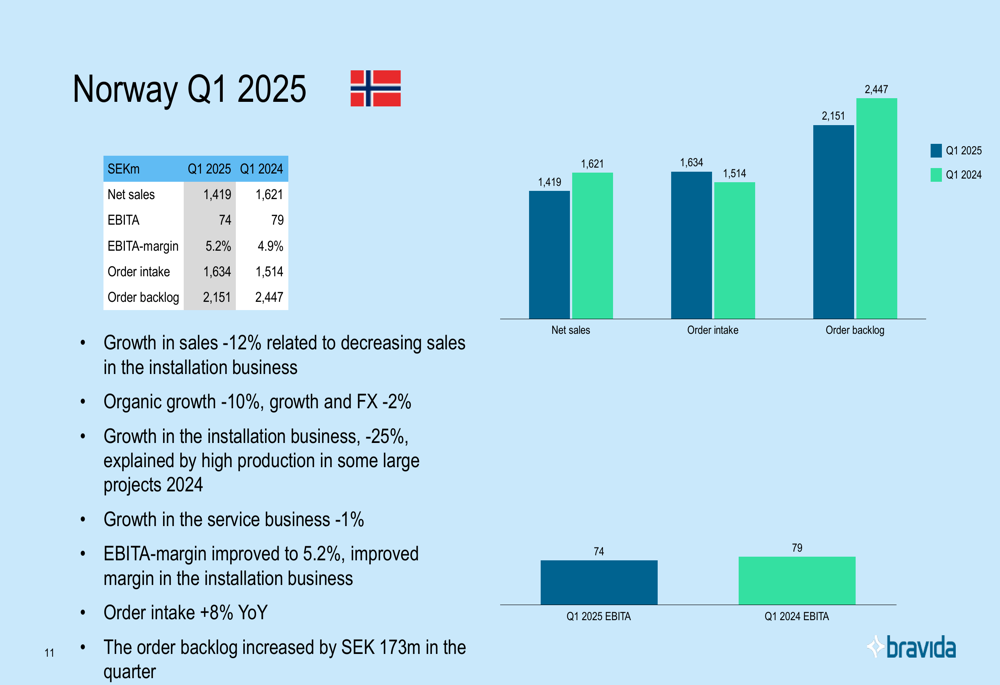

Norway experienced a 12% sales decline to SEK 1,419 million, largely due to a 25% drop in installation business as some large projects from 2024 were completed. Service sales were more stable with only a 1% decrease. Despite lower sales, Norway improved its EBITA margin to 5.2% from 4.9%, and order intake increased by 8% year-over-year.

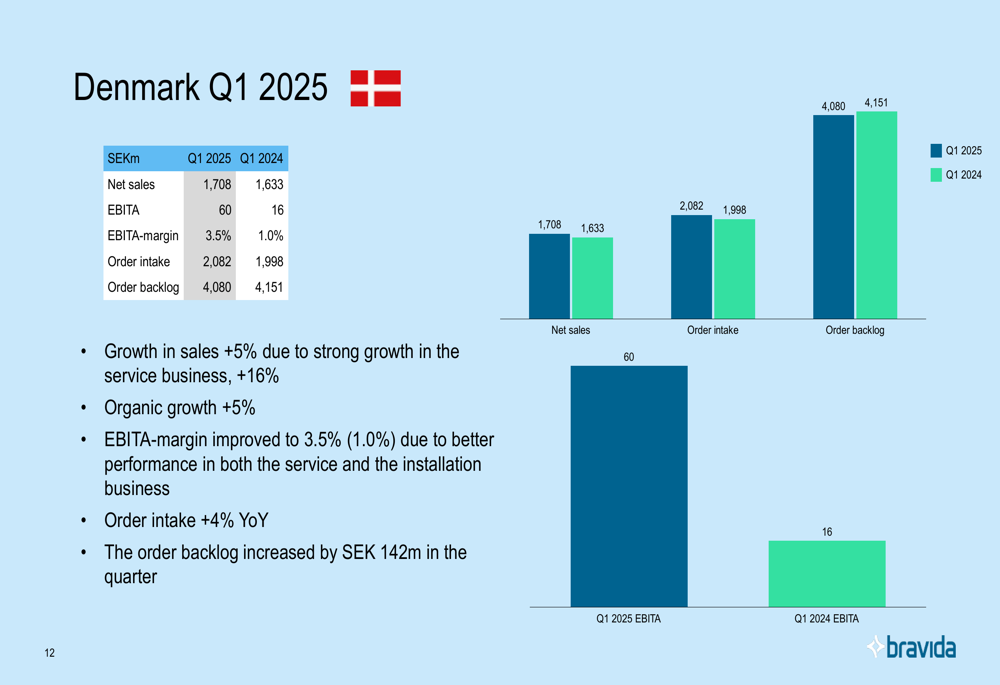

Denmark was the standout performer, with sales growth of 5% to SEK 1,708 million, driven by a robust 16% increase in service business. The most impressive improvement came in profitability, with EBITA margin more than tripling to 3.5% from 1.0% in Q1 2024. This significant margin expansion reflects better performance in both service and installation segments.

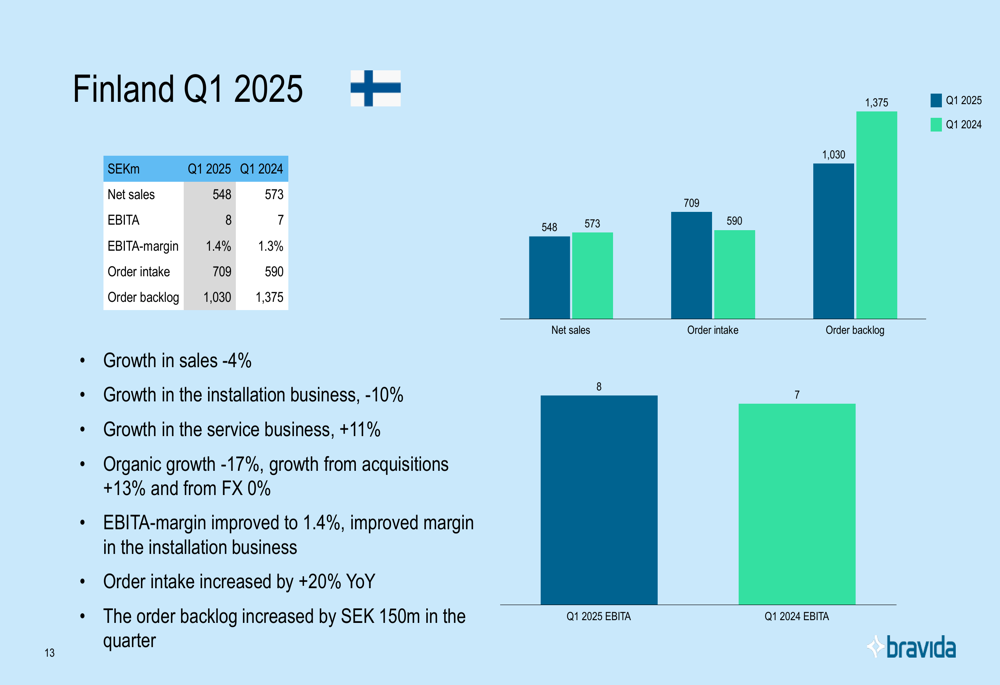

Finland reported a 4% sales decline to SEK 548 million, with installation sales down 10% while service sales grew by 11%. The country’s EBITA margin improved slightly to 1.4% from 1.3%. Order intake showed strong growth of 20% year-over-year, suggesting potential improvement in coming quarters.

Strategic Initiatives

Bravida’s presentation highlighted several strategic initiatives aimed at improving profitability and positioning the company for future growth. The company continues to implement its selective tender strategy, focusing on projects with better margin potential rather than pursuing volume at the expense of profitability.

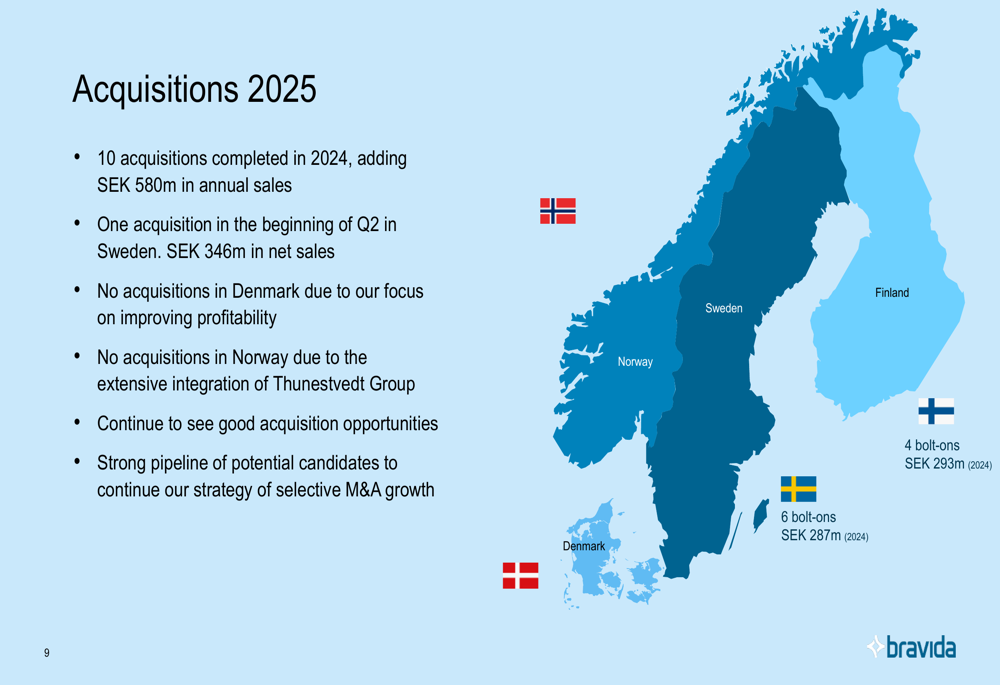

The company completed 10 acquisitions in 2024, adding SEK 580 million in annual sales. In early Q2 2025, Bravida completed one acquisition in Sweden with annual sales of SEK 346 million. The company noted that it continues to see good acquisition opportunities and maintains a strong pipeline of potential candidates.

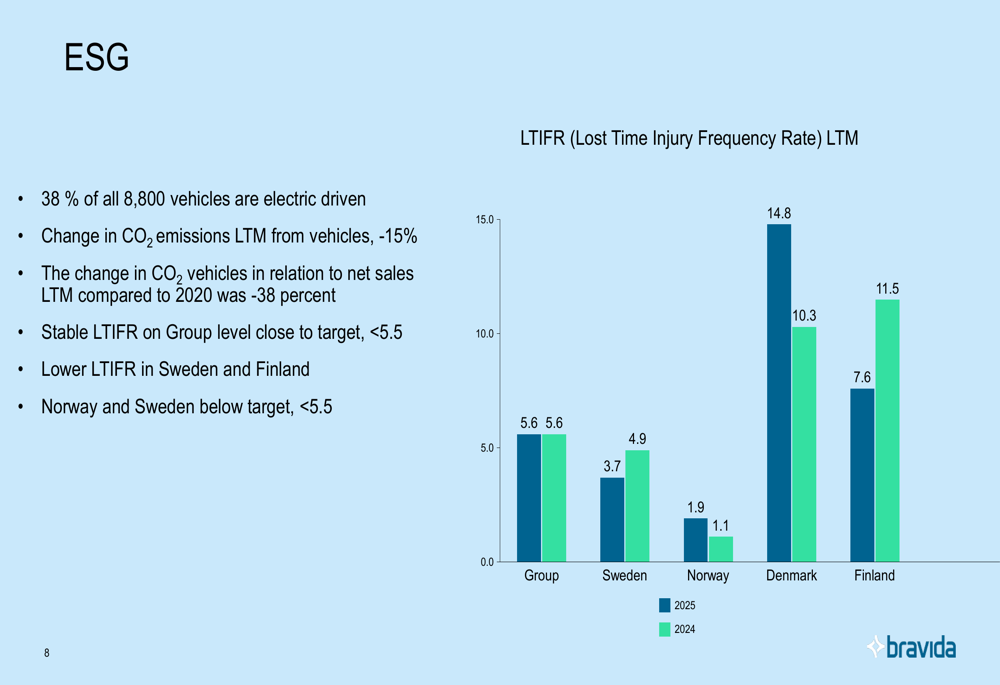

Bravida also emphasized its ESG initiatives, reporting that 38% of its 8,800 vehicles are now electric-driven. CO2 emissions from vehicles decreased by 15% on a last-twelve-months basis, and the company has reduced CO2 emissions relative to net sales by 38% compared to 2020 levels.

Forward-Looking Statements

Looking ahead, Bravida expects service activity to remain stable while challenges in the installation segment continue, with variations across geographic markets. The company sees favorable market conditions in infrastructure, industry, defense facilities, and civil engineering, which could provide business opportunities despite the overall challenging environment.

Bravida reaffirmed its financial targets, which include an EBITA margin above 7% (compared to the current 4.5%), cash conversion exceeding 100%, and sales growth above 5%. The company also targets a dividend payout ratio of more than 50% of net profit and aims to maintain a net debt to EBITDA ratio below 2.5x.

The company’s management emphasized that it will maintain its project-selective strategy with continued focus on cost control across all projects, prioritizing "margin over volume." Bravida also noted that it continues to see an attractive pipeline of acquisition opportunities, suggesting that M&A will remain a key component of its growth strategy.

While 2025 is viewed as a transition year with ongoing market challenges, the company’s improved margins across all regions and strong financial position indicate that Bravida is navigating the difficult environment effectively. The market is expected to bottom out in 2025, with projects won now likely to start contributing to growth in 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.