FTSE 100 today: Index, pound edge higher; StanChart, Revolution Beauty jump

Introduction & Market Context

BrightSpring Health Services Inc (NYSE:BTSG) presented its first quarter 2025 earnings results on May 2, 2025, showcasing strong growth across its business segments and raising its full-year guidance. The healthcare provider, which focuses on serving complex, high-cost populations in home and community settings, continues to build on the momentum seen in its previous quarter.

The company’s stock has shown significant volatility over the past year, with a 52-week range of $10.15 to $24.82. Following the presentation, BrightSpring shares were up 6.31% in premarket trading at $19.03, suggesting a positive market reaction to the quarterly results and improved outlook.

Quarterly Performance Highlights

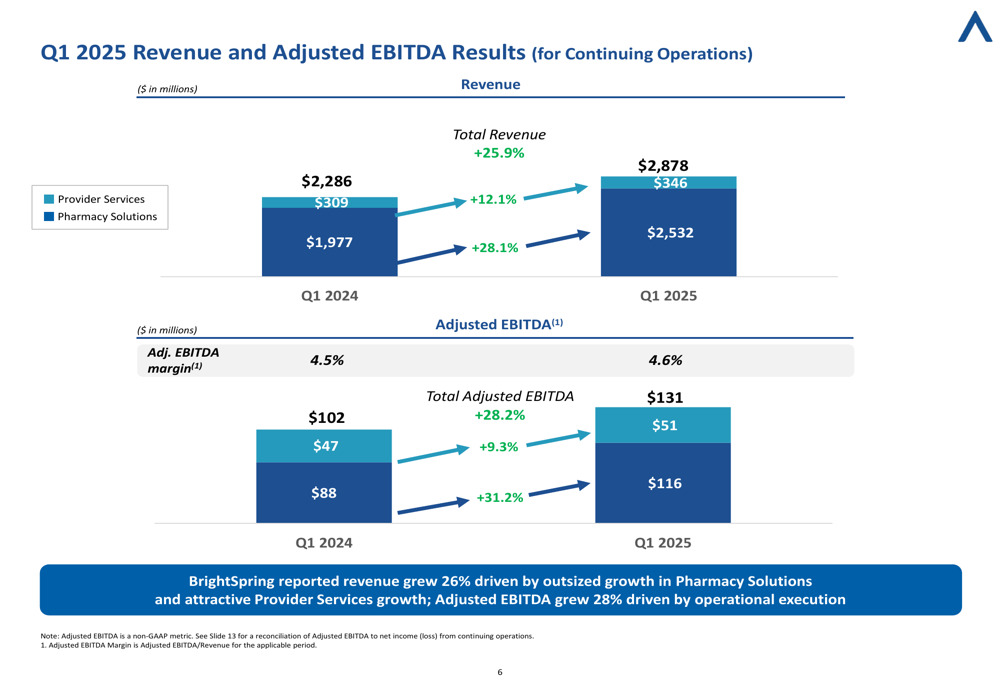

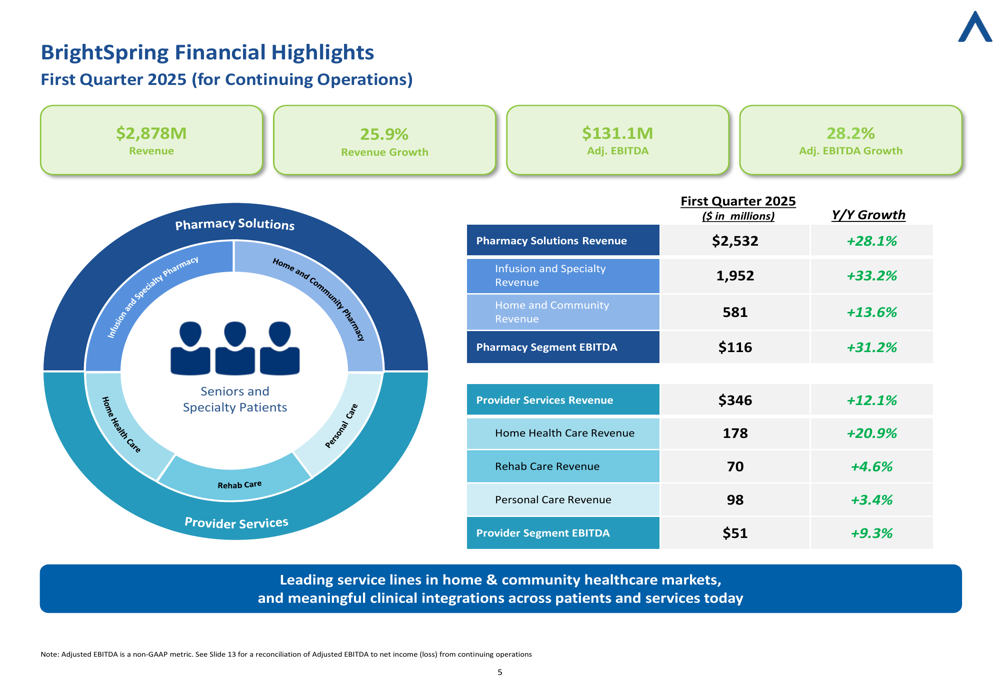

BrightSpring reported impressive financial results for Q1 2025, with total revenue reaching $2,878 million, representing a 25.9% increase compared to the same period last year. Adjusted EBITDA grew even faster at 28.2%, totaling $131.1 million for the quarter. The company also achieved a slight improvement in Adjusted EBITDA margin, which increased from 4.5% to 4.6% year-over-year.

As shown in the following chart of quarterly revenue and EBITDA results:

The growth was primarily driven by the company’s Pharmacy Solutions segment, which saw a 28.1% revenue increase, while Provider Services delivered a solid 12.1% revenue growth. Both segments contributed to the overall EBITDA improvement, with Pharmacy Solutions EBITDA increasing by 31.2% and Provider Services EBITDA growing by 9.3%.

Segment Analysis: Pharmacy Solutions

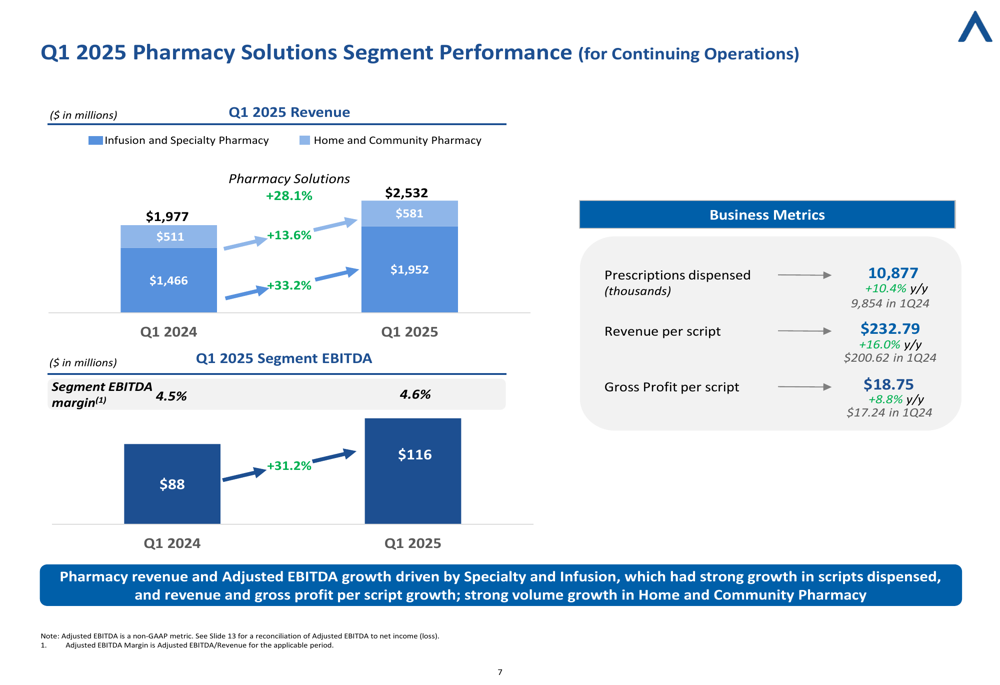

The Pharmacy Solutions segment was the primary growth driver for BrightSpring in Q1 2025, with revenue increasing from $1,977 million to $2,532 million. This growth was particularly strong in the Infusion and Specialty Pharmacy business, which grew 33.2% to reach $1,952 million in revenue. The Home and Community Pharmacy business also performed well, with 13.6% growth to $581 million.

The segment’s operational metrics showed robust performance across key indicators. The company dispensed 10.9 million prescriptions during the quarter, representing a 10.4% increase year-over-year. Revenue per script grew by 16.0% to $232.79, while gross profit per script increased by 8.8% to $18.75.

The following chart illustrates the Pharmacy Solutions segment’s performance metrics:

Management attributed the strong performance to volume growth in both specialty medications and home and community pharmacy services, along with improved operational execution.

Segment Analysis: Provider Services

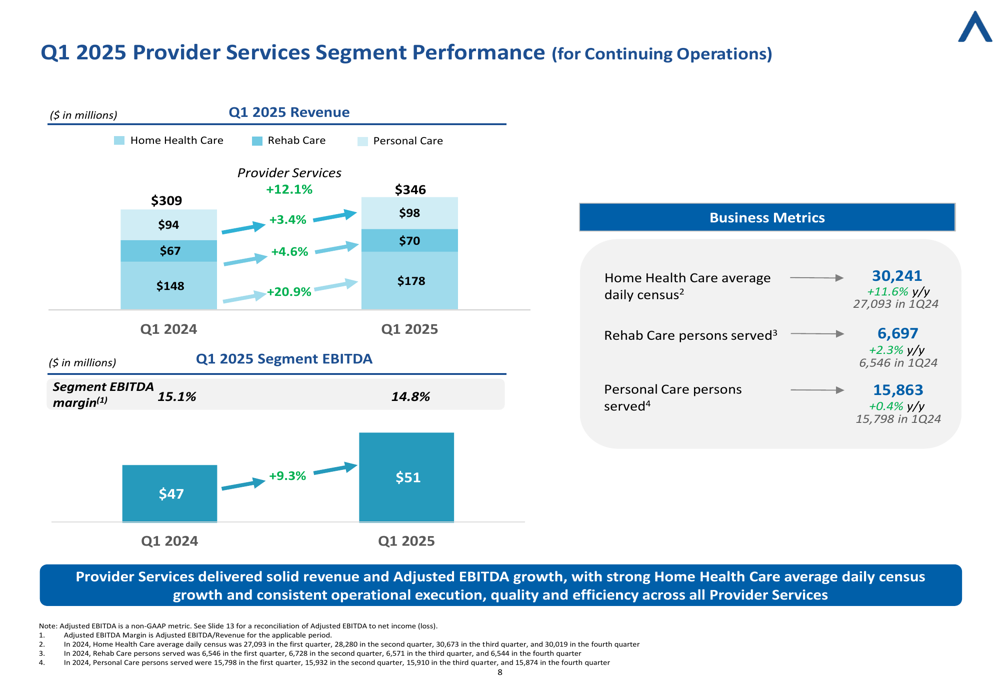

BrightSpring’s Provider Services segment, which includes Home Health Care, Rehab Care, and Personal Care, delivered revenue of $346 million in Q1 2025, a 12.1% increase from the prior year. The Home Health Care business was the standout performer with 20.9% growth, while Rehab Care and Personal Care grew at more modest rates of 4.6% and 3.4%, respectively.

The segment’s operational metrics reflected this growth pattern, with Home Health Care average daily census increasing by 11.6% to 30,241 patients. Rehab Care persons served grew by 2.3% to 6,697, and Personal Care persons served increased slightly by 0.4% to 15,863.

The Provider Services segment’s performance is illustrated in the following chart:

Despite the strong revenue growth, the segment’s EBITDA margin decreased slightly from 15.1% to 14.8%, though absolute EBITDA still grew by 9.3% to $51 million. Management emphasized that the Provider Services segment continues to focus on operational execution, quality improvements, and efficiency initiatives.

Updated 2025 Guidance

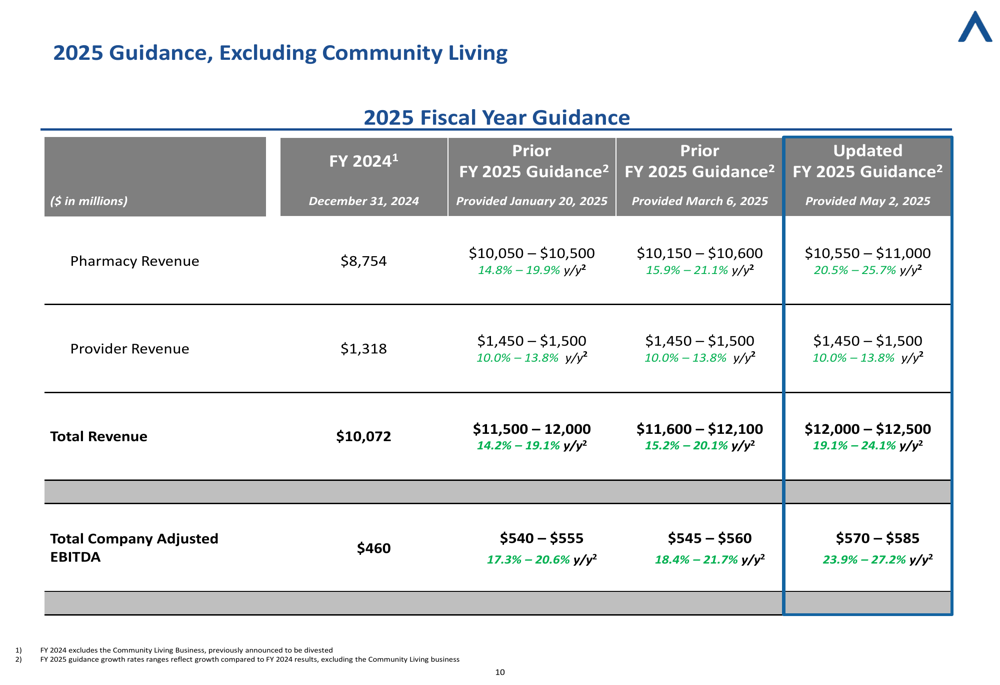

In a significant vote of confidence, BrightSpring raised its 2025 guidance for Pharmacy Solutions revenue while maintaining its Provider Services revenue outlook. The company now expects Pharmacy Solutions revenue to reach $10,550-$11,000 million, up from the initial guidance of $10,050-$10,500 million. This represents year-over-year growth of 20.5%-25.7%.

The Provider Services revenue guidance remained unchanged at $1,450-$1,500 million. The company also updated its total Adjusted EBITDA guidance to $570-$585 million, representing growth of 23.9%-27.2% compared to 2024.

The updated guidance is detailed in the following table:

It’s worth noting that this guidance excludes the Community Living business, which is pending sale as part of the company’s strategic realignment.

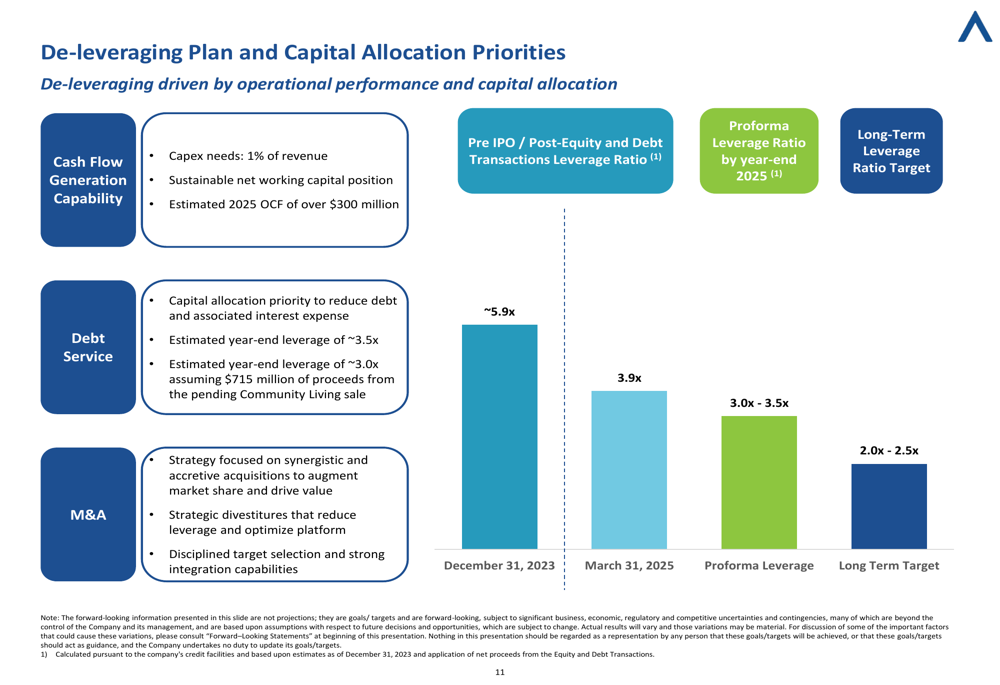

Deleveraging Strategy and Capital Allocation

BrightSpring continues to make significant progress on its deleveraging journey. The company’s net leverage ratio has decreased from approximately 5.9x as of December 31, 2023, to approximately 3.9x as of March 31, 2025. Following the pending sale of the Community Living business, the company expects its proforma leverage to further decrease to 3.0x-3.5x, moving closer to its long-term target of 2.0x-2.5x.

The company’s deleveraging plan and capital allocation priorities are illustrated in the following chart:

Management highlighted that BrightSpring’s strong cash flow generation capabilities, with operating cash flow expected to exceed $300 million in 2025, will support both debt reduction and strategic growth initiatives. The company’s capital expenditure needs remain modest at approximately 1% of revenue, providing additional financial flexibility.

Forward-Looking Statements

Looking ahead, BrightSpring appears well-positioned to continue its growth trajectory. The company’s focus on serving high-cost, complex populations in preferred settings aligns with broader healthcare trends toward home-based care and cost containment. Management emphasized three key strategic pillars: addressing attractive markets with needed solutions, focusing on growth and operational excellence, and leveraging scale and service integration.

The company’s financial highlights for Q1 2025 are summarized in the following comprehensive overview:

While the presentation naturally emphasized positive developments, it’s important to note that challenges remain. The previous earnings report mentioned potential impacts from the Inflation Reduction Act, market saturation in specialty pharmacy, and rising operational costs as potential headwinds. However, the strong Q1 2025 performance and raised guidance suggest that management believes it can navigate these challenges effectively.

With its continued focus on deleveraging while pursuing strategic acquisitions, BrightSpring is balancing financial discipline with growth ambitions. The company’s integrated approach to pharmacy and healthcare services positions it as a significant player in the evolving healthcare landscape, particularly in the high-growth areas of home and community-based care.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.