Microvast Holdings announces departure of chief financial officer

BrightSpring Health Services Inc (NYSE:BTSG) reported robust second-quarter results on August 1, 2025, showcasing accelerated growth across its business segments. The healthcare services provider posted significant revenue expansion, with particularly strong performance in its Pharmacy Solutions division.

Quarterly Performance Highlights

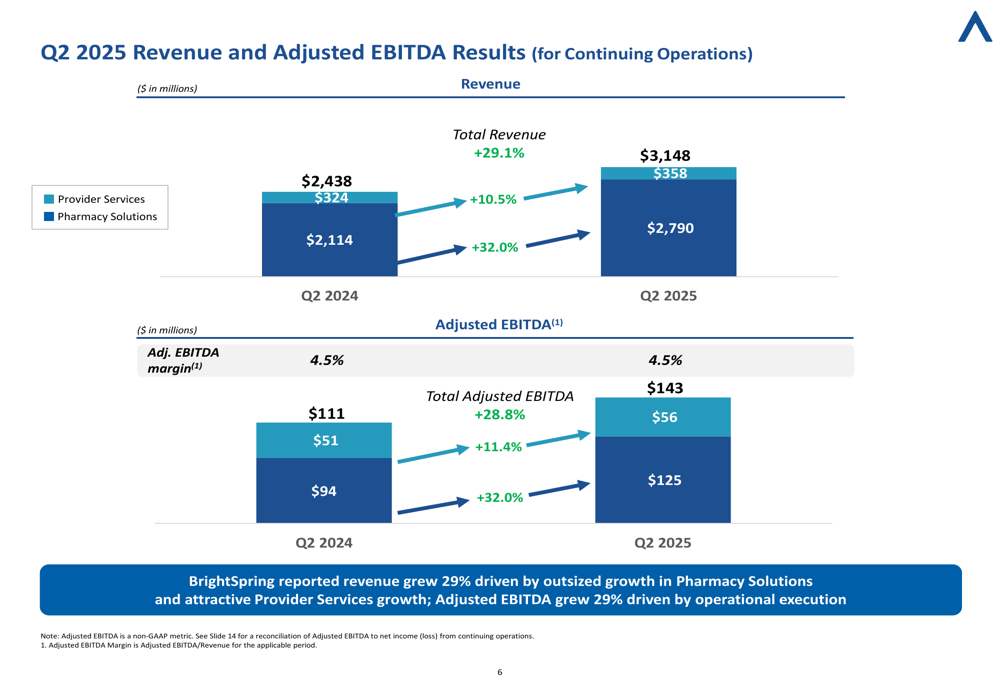

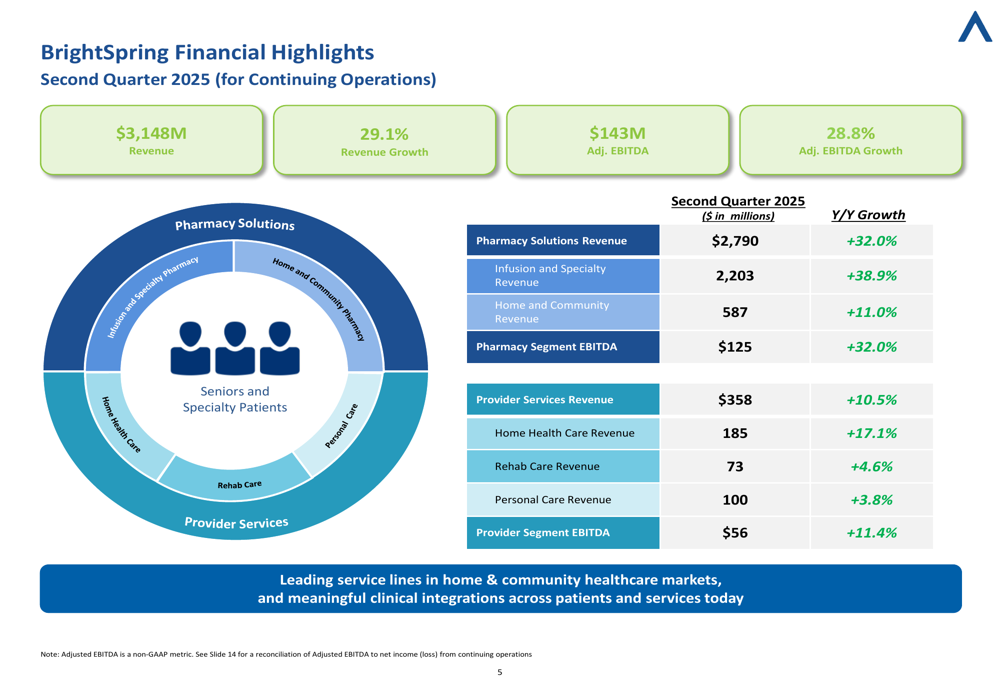

BrightSpring reported total revenue of $3.15 billion for Q2 2025, representing a 29.1% increase compared to the same period last year. Adjusted EBITDA grew at a similar pace, rising 28.8% to $143 million. The company maintained a stable adjusted EBITDA margin of 4.5% despite the rapid expansion.

"We continue to deliver high-quality, preferred and lower-cost health services to large and complex populations," said the company in its presentation materials, highlighting its focus on operational capabilities and integrated care model.

The Q2 results show an acceleration from the company’s Q1 2025 performance, which saw revenue growth of 26% year-over-year. This positive momentum has supported the stock’s performance, though shares have retreated slightly from their 52-week high of $25.57, closing at $20.65 on July 31, 2025.

As shown in the following chart of quarterly financial performance:

Pharmacy Solutions Segment Analysis

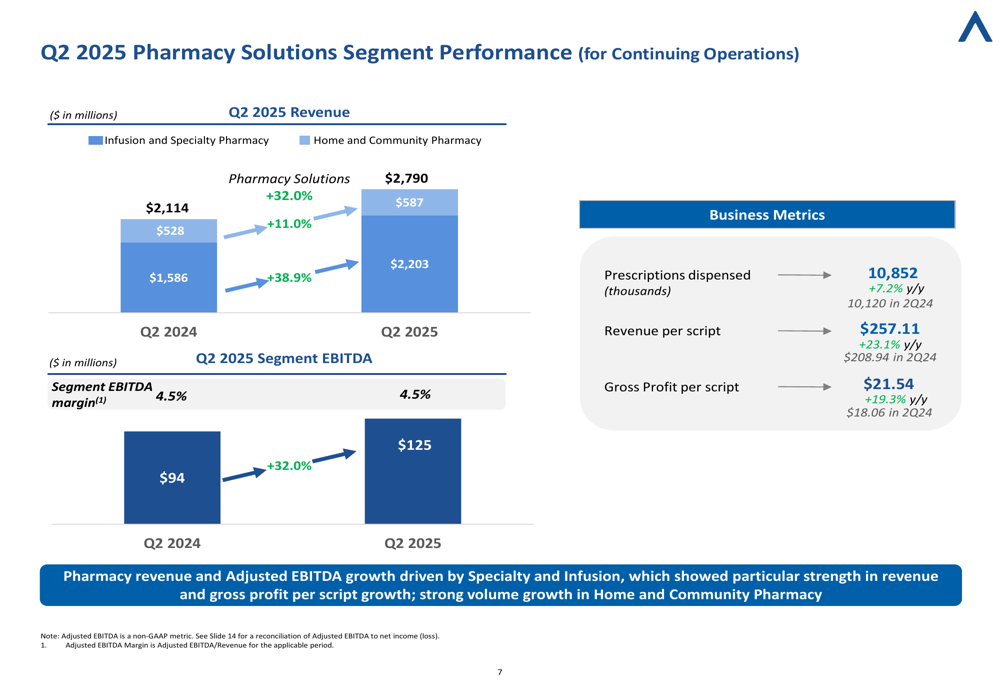

The Pharmacy Solutions segment, which accounts for nearly 89% of total revenue, was the primary growth driver. This division generated $2.79 billion in revenue, up 32.0% year-over-year, with adjusted EBITDA also increasing by 32.0% to $125 million.

Within this segment, Infusion and Specialty Pharmacy services showed exceptional growth of 38.9%, reaching $2.2 billion in revenue. Home and Community Pharmacy services grew by 11.0% to $587 million.

Key operational metrics also showed improvement, with prescriptions dispensed increasing 7.2% year-over-year to 10,852. Revenue per script rose significantly by 23.1% to $257.11, while gross profit per script grew 19.3% to $21.54, indicating improved pricing and operational efficiency.

The following chart illustrates the Pharmacy Solutions segment’s performance:

Provider Services Segment Analysis

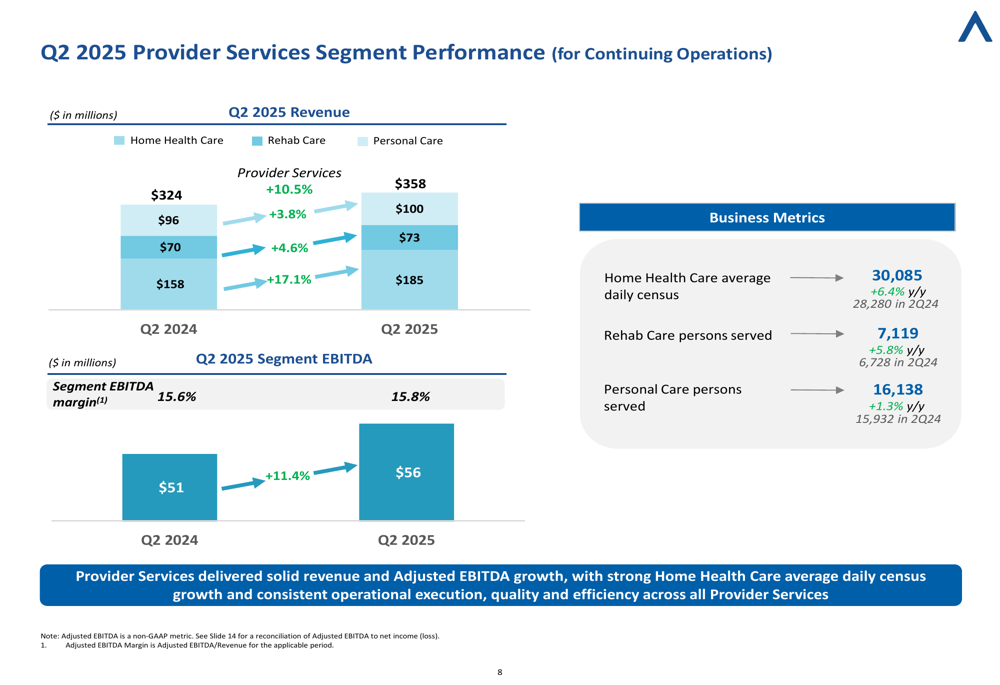

The Provider Services segment generated $358 million in revenue, representing a 10.5% increase compared to Q2 2024. This segment’s adjusted EBITDA grew 11.4% to $56 million, with margins slightly improving from 15.6% to 15.8%.

Home Health Care led the growth within this segment, with revenue increasing 17.1% to $185 million. Rehab Care and Personal Care services showed more modest growth of 4.6% and 3.8%, respectively.

Operational metrics remained positive, with Home Health Care average daily census growing 6.4% to 30,085 patients, while Rehab Care and Personal Care persons served increased by 5.8% and 1.3%, respectively.

The following chart details the Provider Services segment’s performance:

Updated Guidance and Strategic Outlook

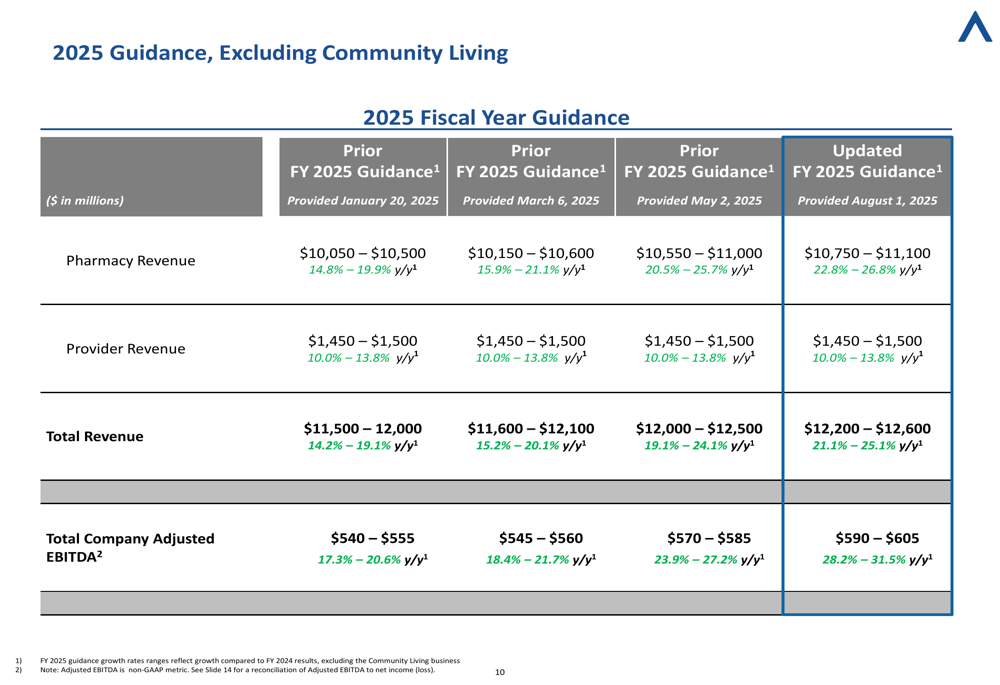

BrightSpring raised its full-year 2025 guidance, reflecting confidence in continued strong performance. The company now expects total revenue between $12.2 billion and $12.6 billion, representing year-over-year growth of 21.1% to 25.1%. Total (EPA:TTEF) company adjusted EBITDA is projected to reach between $590 million and $605 million, a 28.2% to 31.5% increase from the previous year.

This updated guidance excludes the Community Living business, which the company plans to divest in the second half of 2025, as previously announced. The revised outlook represents an increase from earlier guidance provided throughout the year.

The following chart shows the updated 2025 guidance:

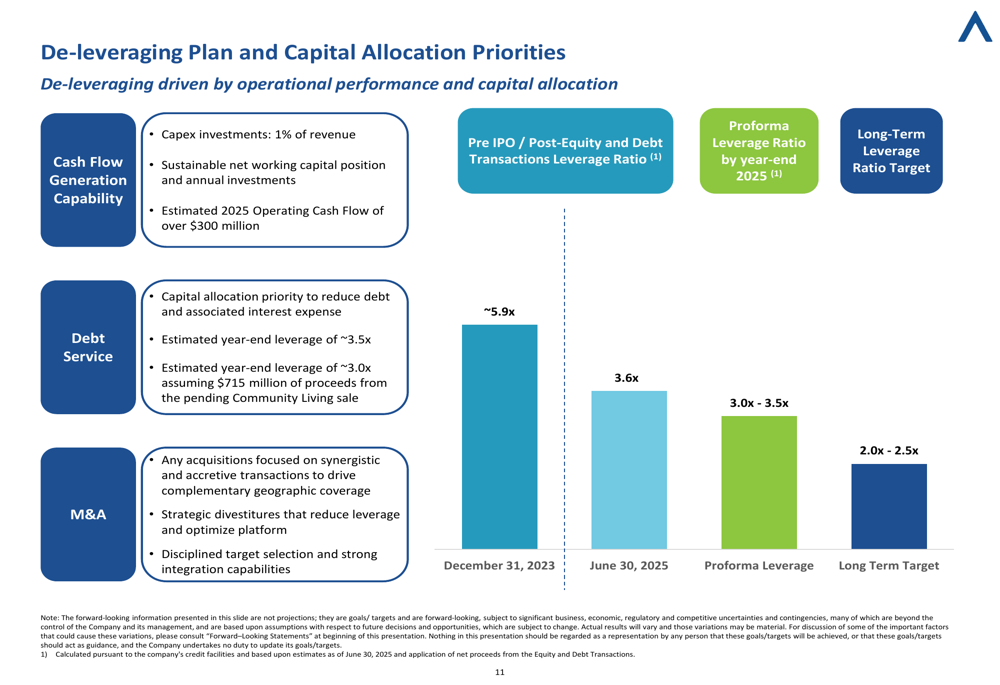

Deleveraging Progress and Capital Allocation

BrightSpring continues to make progress on its deleveraging strategy. The company’s leverage ratio has improved significantly from approximately 5.9x at the end of 2023 (post-IPO) to 3.6x as of June 30, 2025. Management expects to further reduce this to approximately 3.5x by year-end, or potentially to around 3.0x if the pending Community Living sale is completed.

The company projects operating cash flow of over $300 million for 2025, with capital expenditures maintained at approximately 1% of revenue. Management has emphasized that debt reduction remains the primary capital allocation priority, with a long-term leverage target of 2.0x to 2.5x.

The following chart illustrates the company’s deleveraging plan:

Financial Analysis

BrightSpring’s Q2 2025 results demonstrate the company’s ability to maintain strong growth momentum while simultaneously improving its financial position. The 29.1% revenue growth represents an acceleration from the 26% growth reported in Q1 2025, indicating strengthening business fundamentals.

The company’s detailed financial breakdown shows consistent performance across segments, with particularly strong results in the high-margin Infusion and Specialty Pharmacy business. The stability in overall EBITDA margins, despite rapid expansion, suggests effective cost management and operational discipline.

As shown in the comprehensive financial highlights:

Looking ahead, BrightSpring appears well-positioned to continue its growth trajectory, supported by strong demand in its core markets and strategic focus on high-growth segments. The planned divestiture of the Community Living business should further strengthen the company’s balance sheet and allow for greater investment in its faster-growing pharmacy and healthcare service lines.

Investors will likely focus on the company’s ability to maintain this growth rate while continuing to improve margins and reduce leverage in the coming quarters. The stock’s performance, which has seen significant volatility over the past year, will likely depend on the company’s execution against its updated guidance and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.