BofA update shows where active managers are putting money

Introduction & Market Context

Burgundy Diamond Mines Ltd (ASX:BDM) released its Q2 2025 quarterly results presentation on July 31, highlighting significant operational changes amid challenging financial performance. The company, which positions itself as "a reliable producer of ethical premium diamonds to the global luxury market," is implementing a strategic pivot to underground mining operations while facing substantial revenue declines.

The presentation comes as Burgundy’s stock trades near its 52-week low of AU$0.021, closing at AU$0.033 on July 30 with a modest 3.13% gain. This follows a concerning trend of declining financial performance that began in previous quarters, with the company’s Q1 2025 results showing similar challenges.

Quarterly Performance Highlights

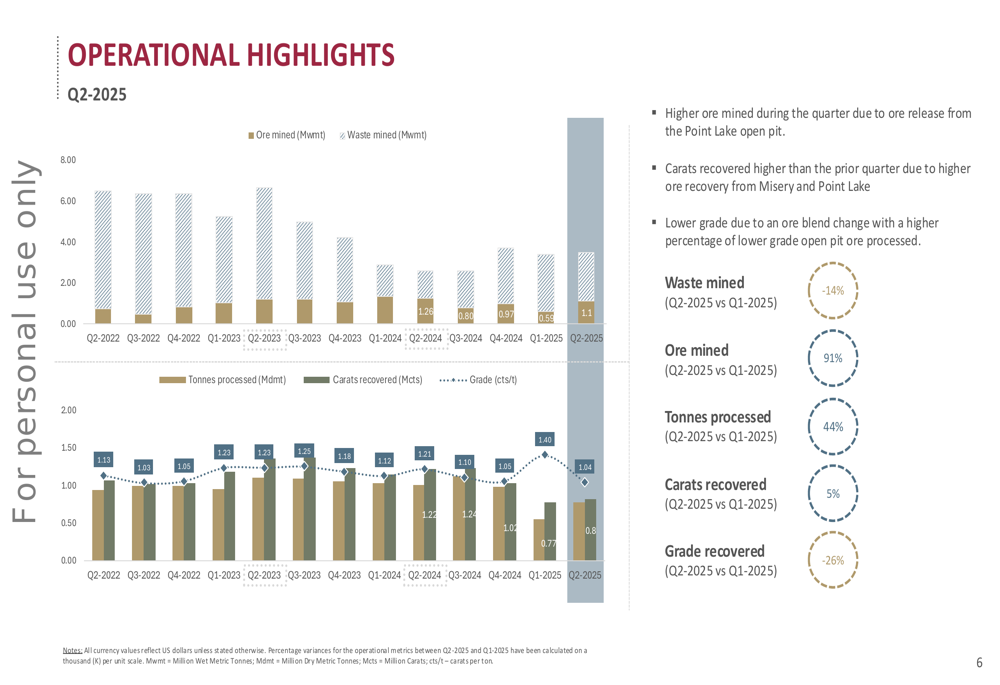

Burgundy’s Q2 2025 operational metrics showed mixed results, with significant increases in ore mining and processing volumes, but declining financial outcomes. The company reported higher ore mined due to increased production from the Point Lake open pit, along with a 5% increase in carats recovered compared to the previous quarter.

As shown in the following operational highlights chart, the company achieved substantial quarter-over-quarter increases in ore mined (91%) and tonnes processed (44%), while reducing waste mining by 14%:

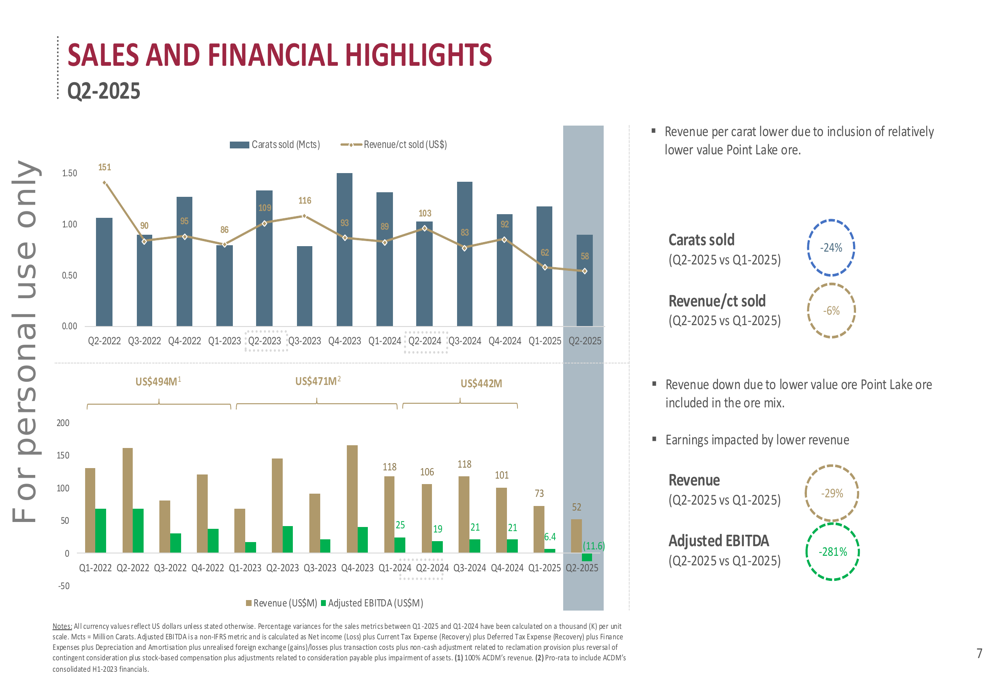

However, these operational improvements did not translate to stronger financial performance. The company’s sales and financial metrics revealed concerning trends, with revenue declining 29% and Adjusted EBITDA falling 28.1% compared to the previous quarter. This decline was driven by a 24% decrease in carats sold and a 6% reduction in revenue per carat, which the company attributed to the inclusion of relatively lower value Point Lake ore.

The following chart illustrates the declining sales performance:

Financial Position and Cash Flow

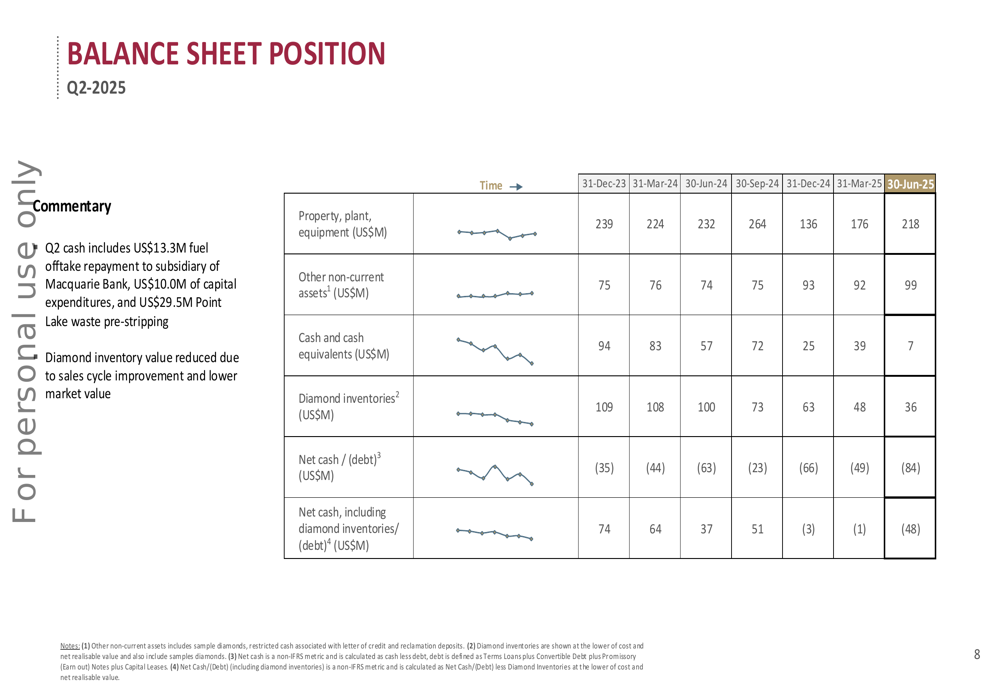

Burgundy’s financial position deteriorated significantly during Q2 2025, with cash reserves plummeting from $38.8 million on March 31, 2025, to just $7.2 million by June 30. This rapid cash depletion represents a concerning trend for investors, particularly given the company’s declining revenue.

The balance sheet position over the past six months shows the downward trajectory in cash reserves and net cash position:

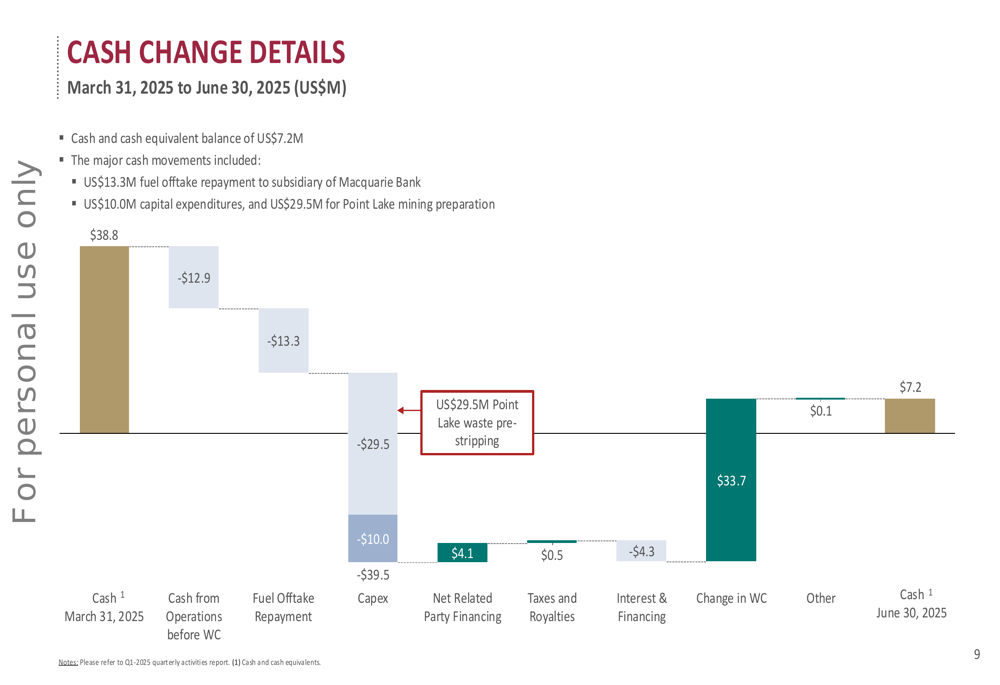

The company’s cash flow waterfall chart provides a detailed breakdown of the major cash movements during the quarter, including a $13.3 million fuel offtake repayment, $10.0 million in capital expenditures, and $29.5 million for Point Lake mining preparation. These substantial outflows were only partially offset by working capital improvements:

This rapid cash burn aligns with concerns raised in previous earnings reports, where analysts noted the company was quickly depleting its cash reserves despite maintaining healthy liquidity ratios.

Strategic Initiatives and Operational Changes

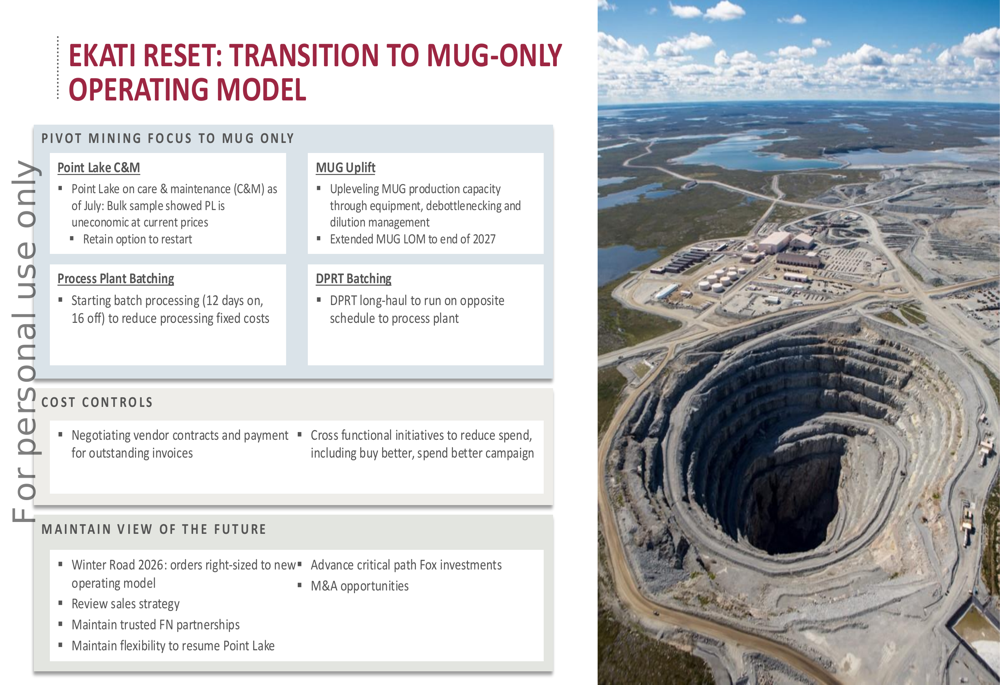

Facing these financial challenges, Burgundy is implementing a significant strategic shift, transitioning to what it calls a "MUG-only operating model." This involves pivoting mining focus exclusively to underground operations at the Misery Underground (MUG) mine, while placing the Point Lake open pit on care and maintenance.

The company outlined this strategic reset in its presentation:

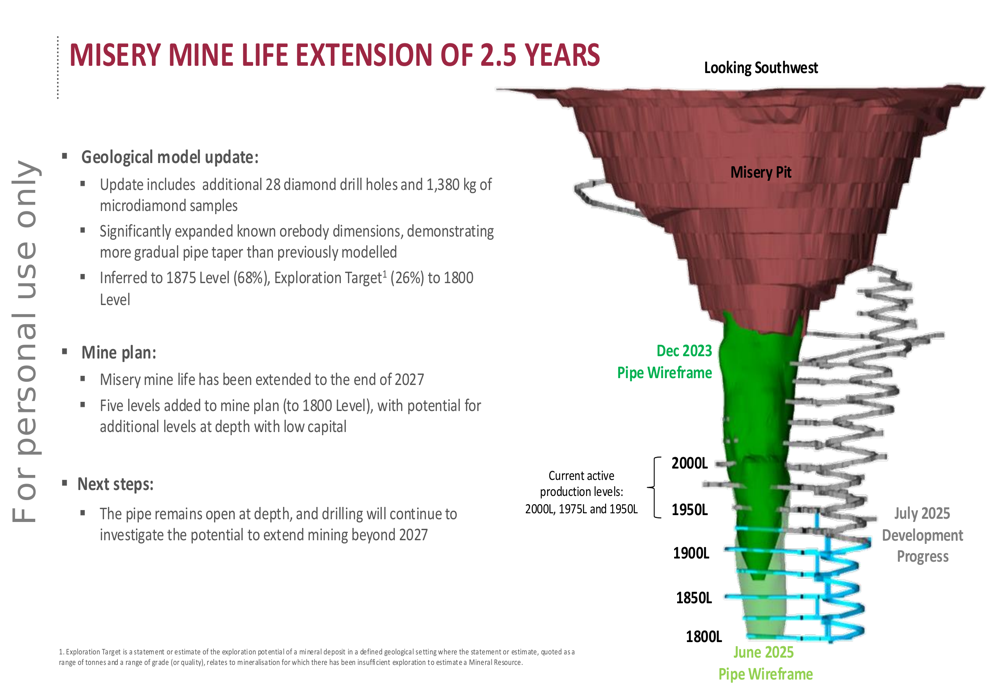

A key component of this strategy is the extension of the Misery mine life by 2.5 years to the end of 2027. This extension is based on an updated geological model that incorporates additional diamond drill holes and microdiamond samples, significantly expanding the known orebody dimensions:

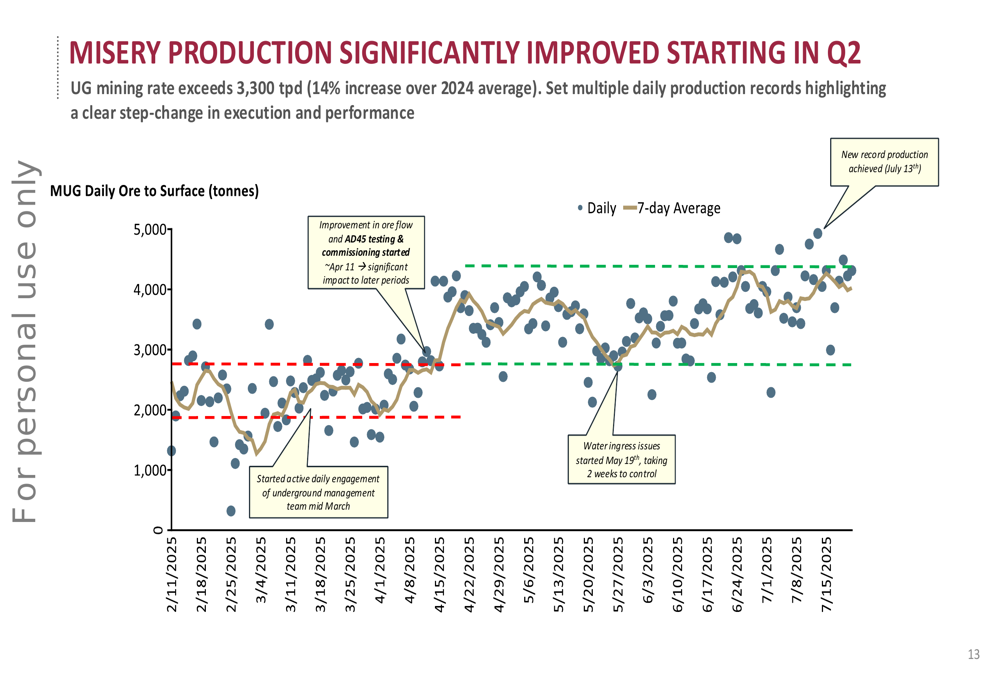

Burgundy also highlighted improving production metrics at the Misery mine, with underground mining rates exceeding 3,300 tonnes per day in Q2, representing a 14% increase over the 2024 average:

Forward-Looking Statements

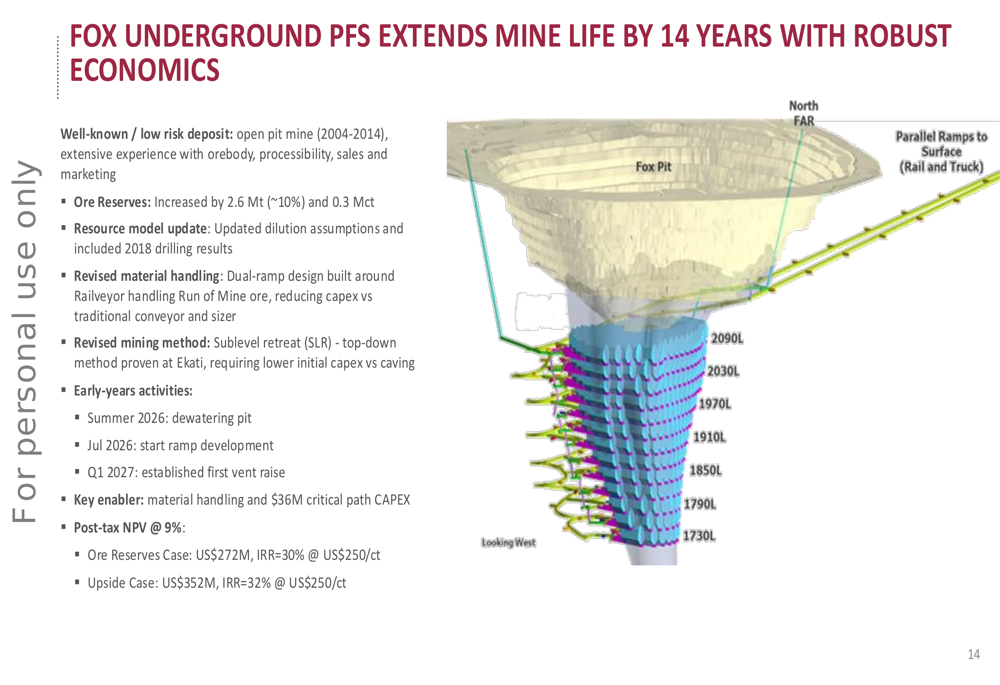

Looking beyond immediate challenges, Burgundy presented the results of its Fox Underground Pre-Feasibility Study (PFS), which indicates potential for extending mine life by 14 years with what the company describes as "robust economics." The study projects a post-tax NPV of $272 million (IRR=30%) for the Ore Reserves Case:

This long-term growth potential stands in stark contrast to the company’s current financial difficulties, creating a narrative of short-term pain for potential long-term gain. However, with rapidly depleting cash reserves and declining revenue, Burgundy faces significant challenges in funding these growth initiatives.

The company’s strategic pivot represents a critical juncture for Burgundy Diamond Mines as it attempts to navigate current market challenges while positioning for future growth. Investors will be closely watching whether the operational changes can stabilize financial performance before cash reserves are further depleted.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.