Canopy Growth stock tumbles after announcing $200 million share sale plan

Introduction & Market Context

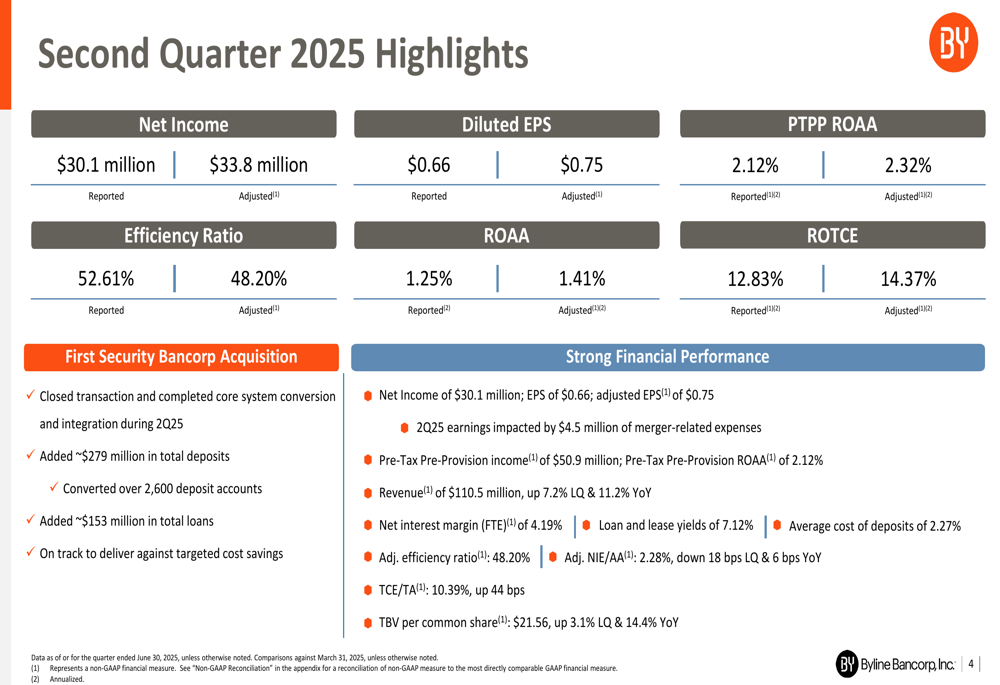

Byline Bancorp (NYSE:BY) presented its second quarter 2025 earnings results on July 25, highlighting improved profitability metrics and the successful completion of its First Security Bancorp acquisition. The Chicago-based financial institution, which ranks as the second-largest bank headquartered in the city, reported total assets of $9.7 billion and a market capitalization of $1.2 billion.

The bank’s stock closed at $27.04 on July 25, 2025, showing a modest gain of 0.07% for the day. The shares have been trading within a 52-week range of $22.63 to $32.89, reflecting the broader market’s cautious optimism toward regional banking stocks.

Quarterly Performance Highlights

Byline reported adjusted earnings per share of $0.75 for Q2 2025, representing a significant improvement from the $0.64 reported in the previous quarter. On a reported basis, EPS came in at $0.66, with the difference primarily attributed to merger-related expenses.

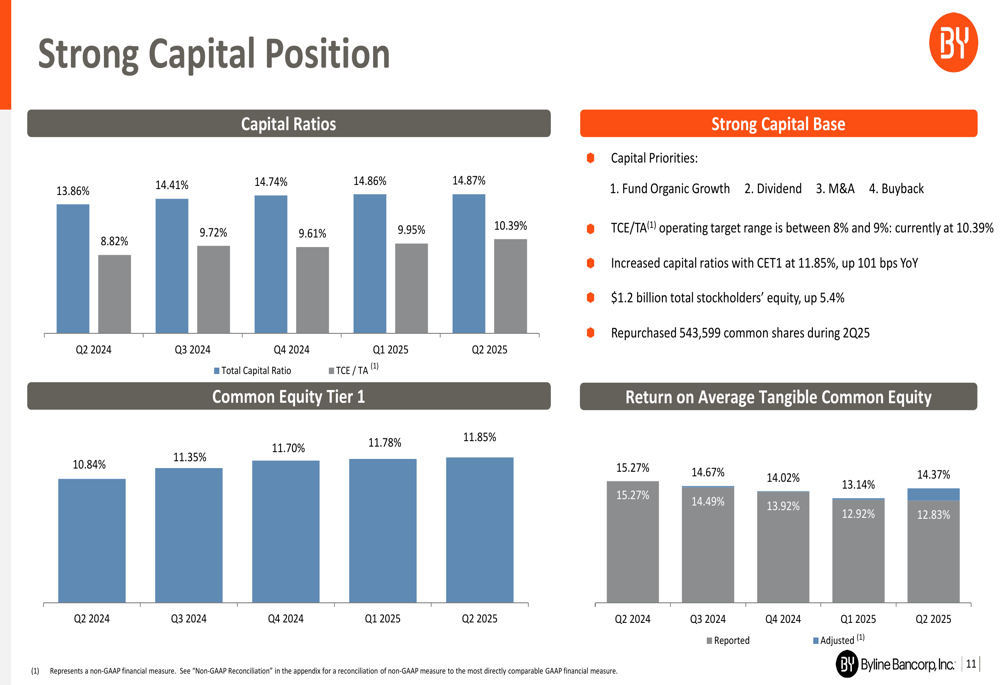

The bank’s adjusted return on average tangible common equity (ROTCE) reached 14.37%, while its adjusted return on average assets (ROAA) stood at 1.41%. The efficiency ratio improved to 48.20% on an adjusted basis, demonstrating the bank’s effective cost management despite integration expenses.

As shown in the following summary of second quarter highlights:

Acquisition Impact and Integration

A significant milestone during the quarter was the completion of the First Security Bancorp acquisition, which had been anticipated in the previous quarter’s guidance. The transaction added approximately $279 million in total deposits and $153 million in loans to Byline’s balance sheet. The bank successfully converted over 2,600 deposit accounts and completed the core system conversion, indicating a smooth integration process.

"We remain comfortable and confident about crossing $10 billion in assets," stated Roberto Harencia, Chairman and CEO, in the previous quarter’s earnings call, a sentiment that appears well-founded given the successful execution of this acquisition and the bank’s continued organic growth.

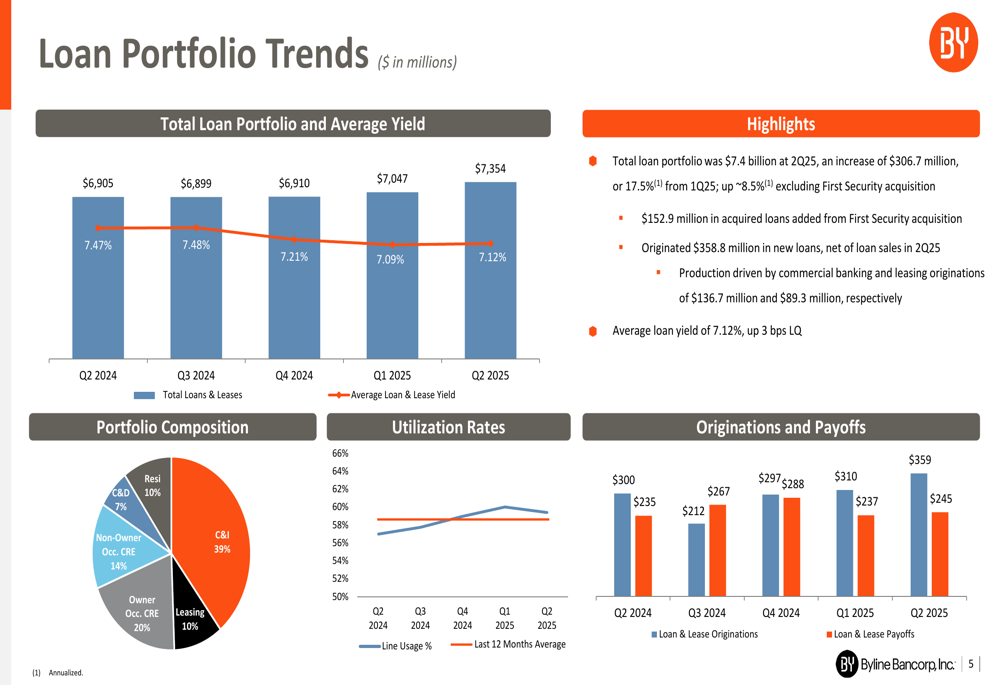

Loan and Deposit Trends

Byline’s total loan portfolio increased to $7.35 billion in Q2 2025, up from $6.91 billion in the same period last year. Commercial and industrial (C&I) loans constitute the largest segment at 39% of the portfolio, followed by owner-occupied commercial real estate at 20%. The average yield on loans decreased slightly year-over-year from 7.47% to 7.12%, reflecting the evolving interest rate environment.

The following chart illustrates the composition and trends in the loan portfolio:

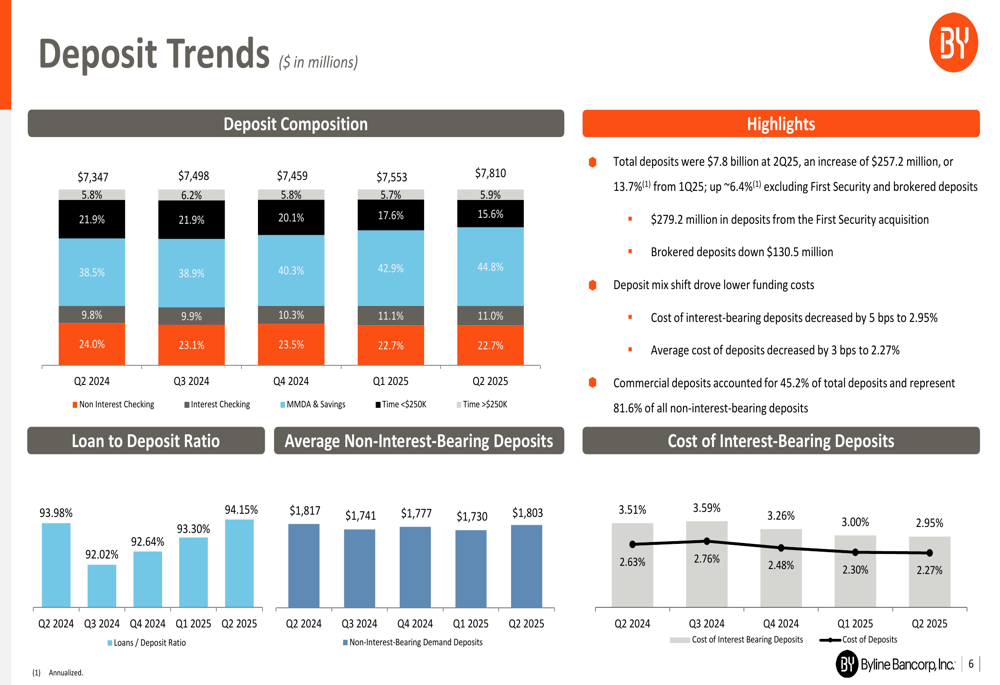

On the funding side, total deposits grew to $7.8 billion, representing a substantial 13.7% increase from the previous quarter. This growth was partially driven by the First Security acquisition, which contributed $279.2 million in deposits. The loan-to-deposit ratio improved to 92.64%, down from 93.98% a year earlier, indicating enhanced liquidity.

The deposit composition shows a diversified funding base with money market and savings accounts comprising 44.8% of total deposits, while non-interest-bearing deposits account for 5.9%.

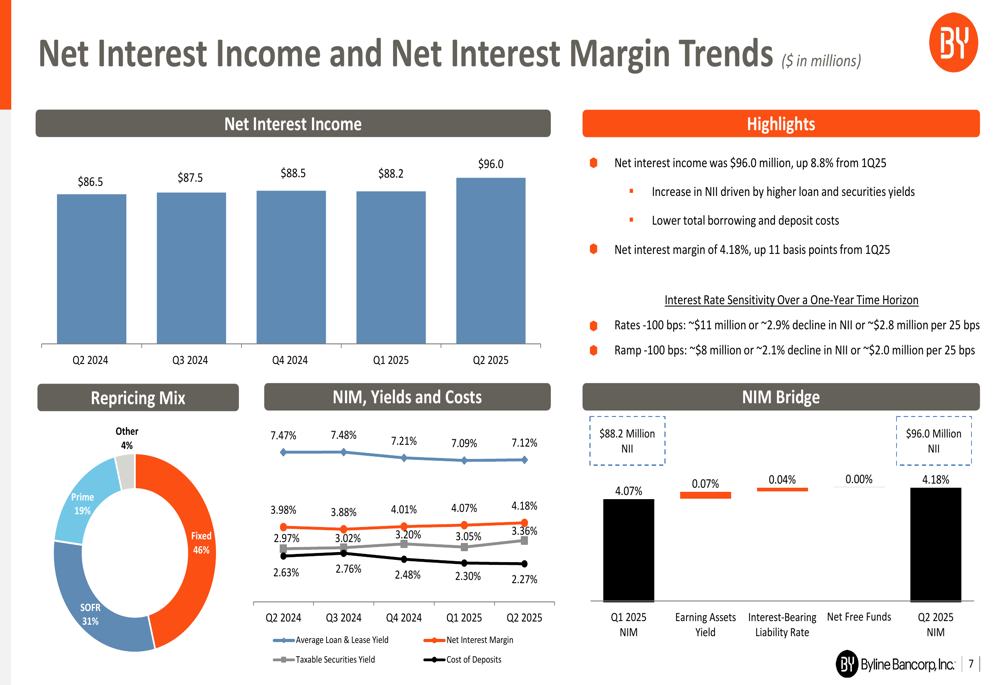

Net Interest Income and Margin

Net interest income reached $96.0 million in Q2 2025, up from $86.5 million in Q2 2024. The net interest margin expanded to 4.19%, an increase of 11 basis points from the previous quarter’s 4.07%. This improvement was driven by higher loan and securities yields, coupled with lower borrowing and deposit costs.

The bank’s interest rate positioning appears well-managed, as illustrated in the following net interest income and margin trends:

Capital Position and Strategic Priorities

Byline maintained a strong capital position with total stockholders’ equity of $1.2 billion, up 5.4% from the previous period. During the quarter, the bank repurchased 543,599 common shares, demonstrating confidence in its financial outlook and commitment to delivering shareholder value.

The bank’s capital deployment priorities remain focused on funding organic growth, maintaining dividend payments, pursuing strategic M&A opportunities, and continuing share repurchases when appropriate.

Looking ahead, Byline outlined several strategic priorities for 2025, including:

1. Preparing for crossing the $10 billion asset threshold with appropriate regulatory readiness

2. Maintaining strong capital ratios and liquidity profile

3. Growing low-cost, core deposits while navigating the interest rate environment

4. Sustaining top-quartile profitability metrics

5. Actively managing risk through disciplined credit monitoring

6. Capitalizing on market opportunities arising from industry consolidation

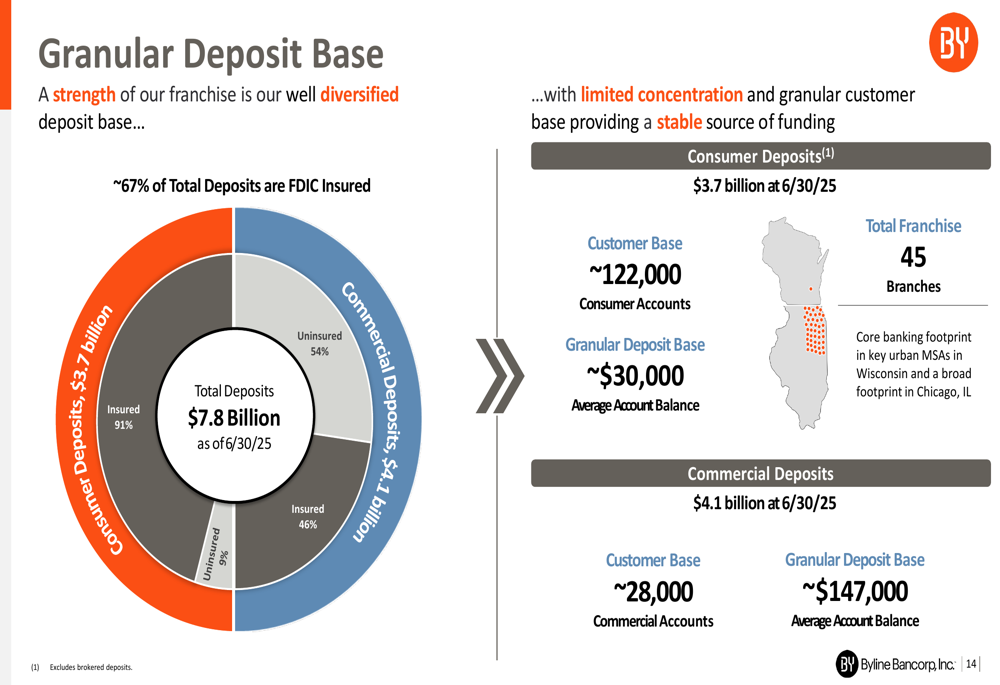

Deposit Stability and Liquidity

A notable strength highlighted in the presentation is Byline’s granular and diversified deposit base. Approximately 67% of total deposits are FDIC insured, providing stability to the funding structure. The bank serves approximately 122,000 consumer accounts with an average balance of $30,000, and 28,000 commercial accounts with an average balance of $147,000.

This granularity helps mitigate concentration risk and supports the bank’s liquidity position, as illustrated in the following breakdown:

Forward-Looking Statements

While the Q2 2025 results demonstrate solid performance, Byline faces several challenges in the coming quarters. These include navigating potential Federal Reserve rate adjustments, managing the regulatory complexities of crossing the $10 billion asset threshold, and addressing competitive pressures in the Chicago banking market.

The bank appears well-positioned to address these challenges through its focus on commercial banking relationships, strategic acquisitions, and operational efficiency. With the successful integration of First Security Bancorp and improved profitability metrics, Byline enters the second half of 2025 with momentum to execute on its strategic priorities while maintaining its position as a leading Chicago-based financial institution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.