SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Calumet Inc. (NASDAQ:CLMT) released its second quarter 2025 financial results presentation on August 8, highlighting modest overall growth driven by its Montana Renewables segment, while continuing to focus on cost reduction and deleveraging efforts. The company’s stock was up 0.87% in premarket trading to $15.04, following a 2.04% decline in the previous session.

The presentation comes after a challenging first quarter where Calumet reported a significant earnings miss, with actual EPS of -$1.87 compared to the forecasted -$0.38. Despite this earlier setback, the company appears to be making operational progress, particularly in its renewable fuels business, which is benefiting from a supportive regulatory environment.

Quarterly Performance Highlights

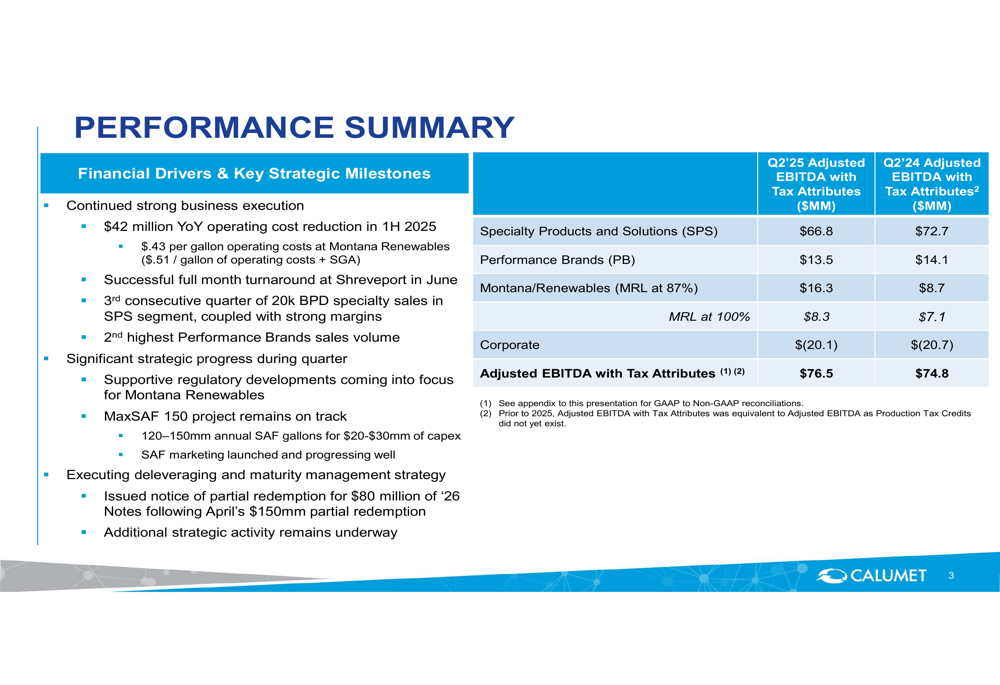

Calumet reported total Adjusted EBITDA with Tax Attributes of $76.5 million for Q2 2025, representing a slight improvement from $74.8 million in Q2 2024. This modest growth was primarily driven by the Montana/Renewables segment, which more than offset declines in the company’s traditional business segments.

The company highlighted several operational achievements, including a $42 million year-over-year operating cost reduction in the first half of 2025 and achieving $0.43 per gallon operating costs at Montana Renewables. A successful turnaround at the Shreveport facility and consistent strong specialty sales were also noted as key drivers.

As shown in the following performance summary:

Segment Analysis

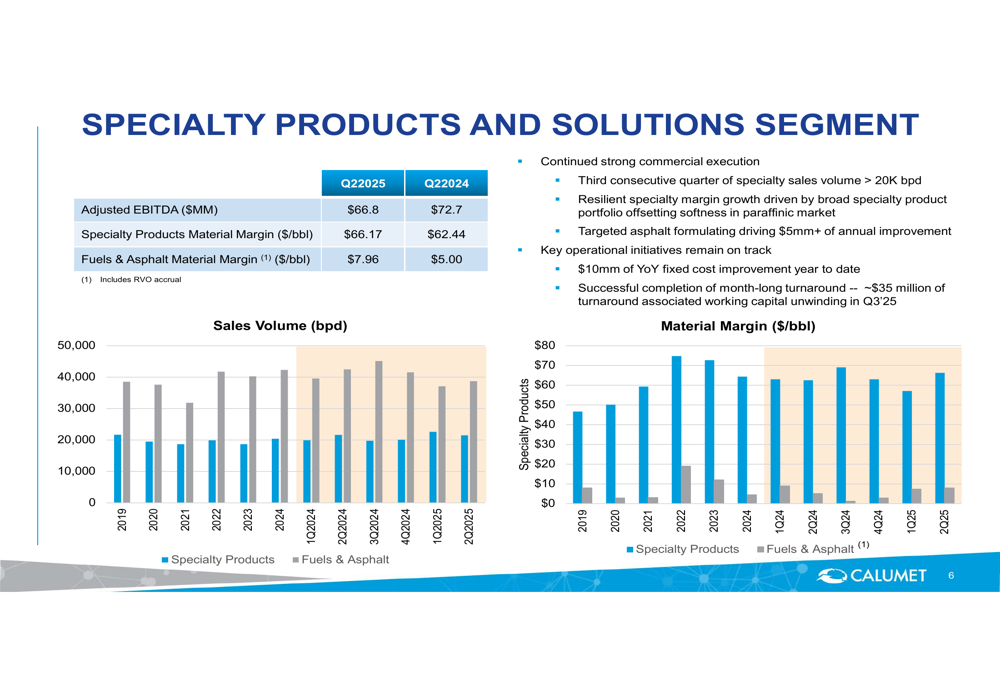

The Specialty Products and Solutions (SPS) segment, which remains Calumet’s largest business unit, posted Adjusted EBITDA of $66.8 million in Q2 2025, down from $72.7 million in the same period last year. Despite the decline, the company emphasized positive developments, including a third consecutive quarter of specialty sales volume exceeding 20,000 barrels per day and improved material margins for both specialty products and fuels.

The segment benefited from $10 million of year-over-year fixed cost improvements year-to-date and successfully completed a month-long turnaround operation. Material margins for specialty products improved to $66.17/bbl in Q2 2025 from $62.44/bbl in Q2 2024.

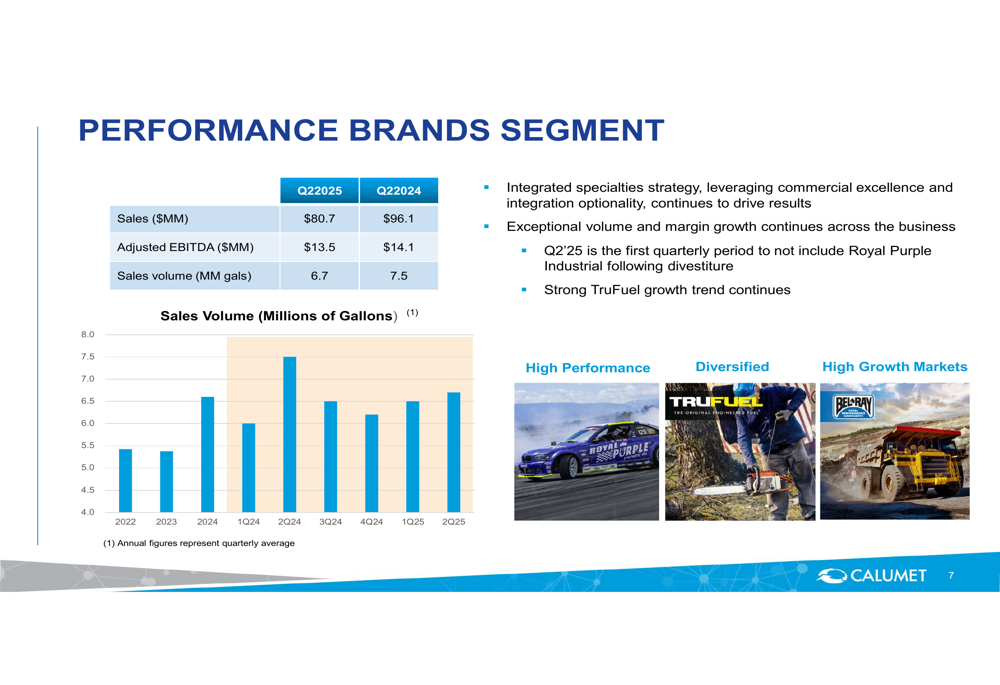

The Performance Brands segment reported Adjusted EBITDA of $13.5 million, slightly down from $14.1 million in Q2 2024. Sales decreased to $80.7 million from $96.1 million, while sales volume declined to 6.7 million gallons from 7.5 million gallons in the prior-year period. The company noted that Q2 2025 was the first quarter not to include Royal Purple Industrial following its divestiture, which partially explains the volume decline.

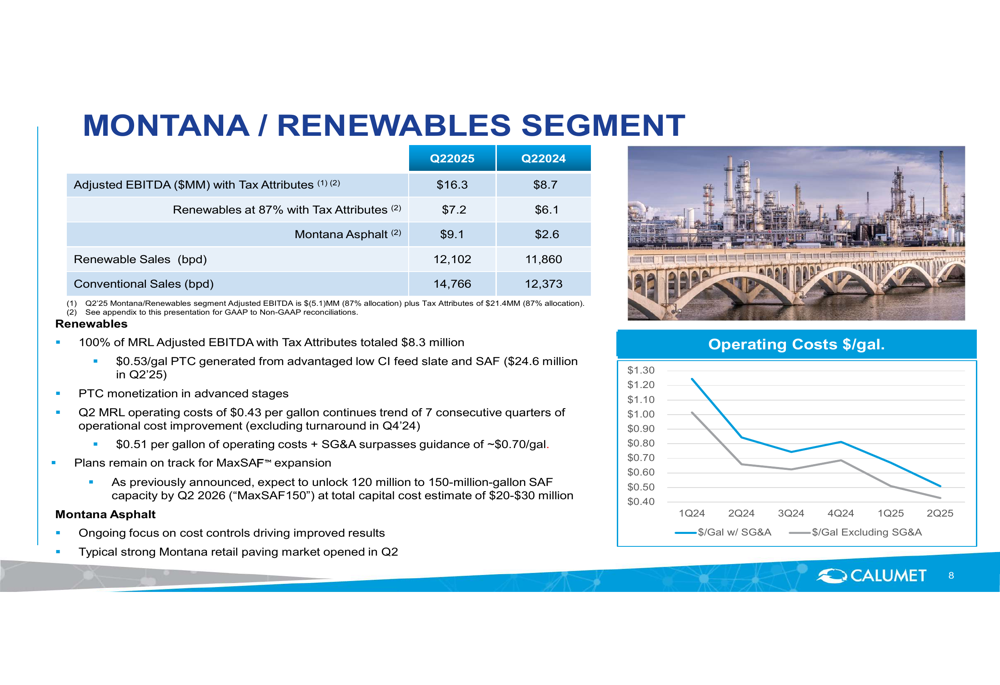

The Montana/Renewables segment emerged as the growth driver, with Adjusted EBITDA more than doubling to $16.3 million from $8.7 million in Q2 2024. This improvement was driven by both the renewables business, which contributed $7.2 million (up from $6.1 million), and Montana Asphalt, which saw a significant increase to $9.1 million from $2.6 million. Renewable sales reached 12,102 barrels per day, slightly up from 11,860 barrels per day in Q2 2024.

Strategic Initiatives

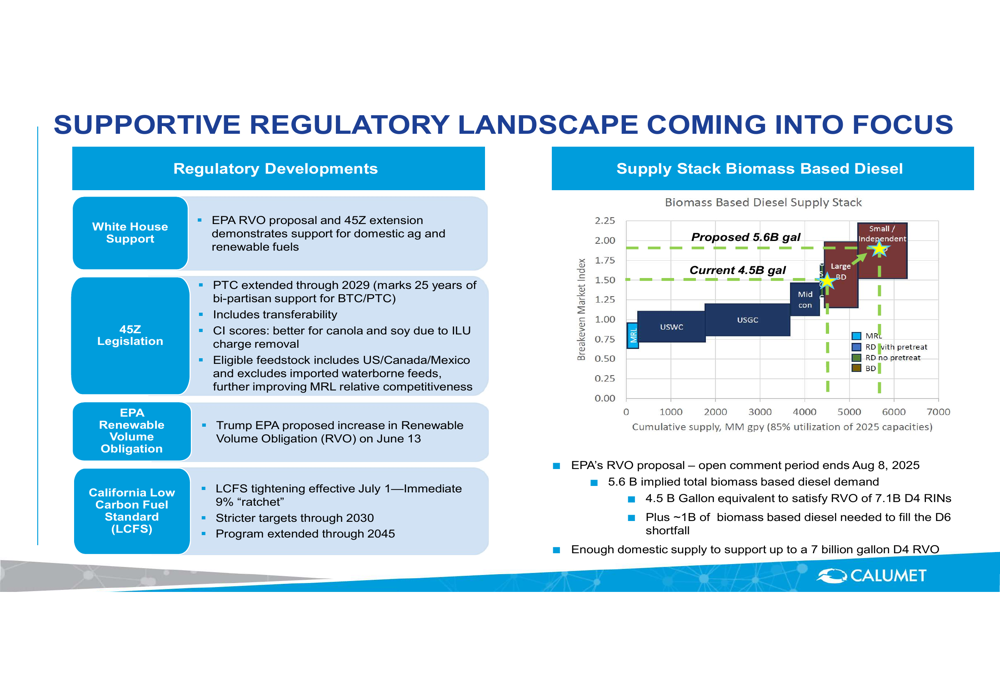

Calumet’s presentation emphasized its strategic focus on renewable fuels, particularly Sustainable Aviation Fuel (SAF), amid a supportive regulatory landscape. The company highlighted White House support and the EPA’s Renewable Volume Obligation (RVO) proposal, which would increase biomass-based diesel demand from the current 4.5 billion gallons to a proposed 5.6 billion gallons.

The company is accelerating its MaxSAF expansion plans, which are expected to unlock 120-150 million gallons of SAF capacity by Q2 2026 with an investment of $20-30 million. This initiative aligns with regulatory developments, including the extension of Production Tax Credits ( PTC (NASDAQ:PTC)) through 2029 and California’s tightening of Low Carbon Fuel Standard (LCFS) requirements.

As illustrated in the regulatory landscape overview:

Calumet’s deleveraging and value creation strategy focuses on four key areas: driving cashflow from the business, supporting balance sheet improvements, executing portfolio optimization through asset sales, and positioning Montana Renewables for potential monetization.

Financial Position & Outlook

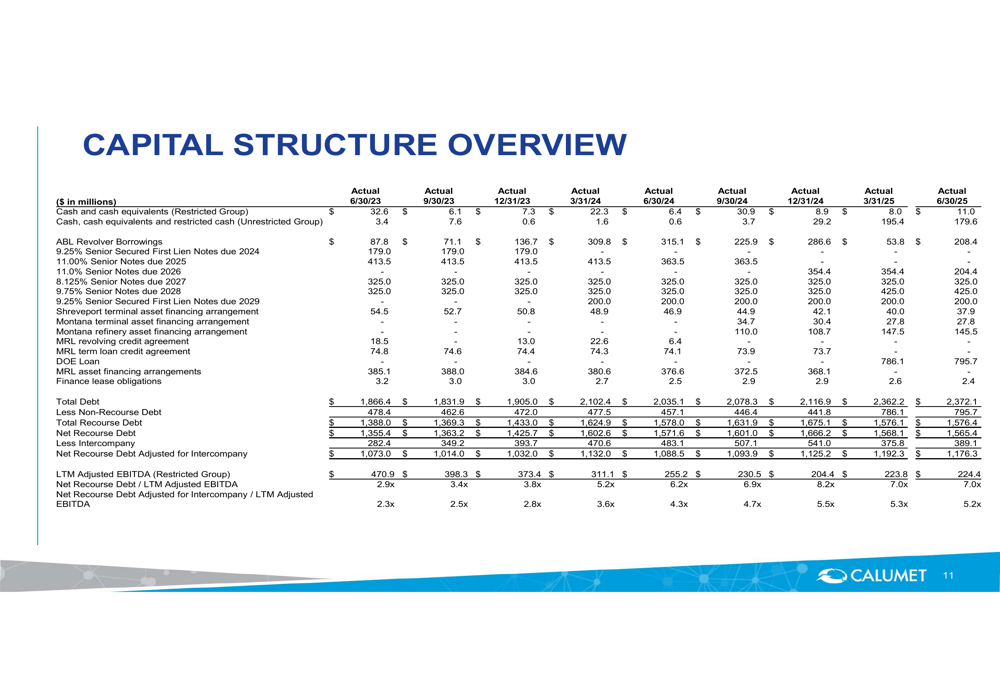

Despite operational improvements, Calumet continues to face challenges with its debt burden. As of June 30, 2025, the company reported total debt of $2,372.1 million, with net recourse debt of $1,565.4 million and a net leverage ratio of 7.0x. This high leverage remains a concern, though the company highlighted its efforts to improve the balance sheet through partial note redemptions and Department of Energy (DOE) loan funding.

The company’s focus on deleveraging aligns with statements made during the Q1 2025 earnings call, where CEO Todd Gordman emphasized the goal of reducing restricted debt to $800 million. The presentation suggests that Calumet is making progress on operational improvements and cost reductions, but significant work remains to address the debt burden.

Looking ahead, Calumet appears positioned to benefit from the growing renewable fuels market, particularly in SAF, while continuing to optimize its traditional specialty products business. The success of the Montana Renewables segment and the planned MaxSAF expansion will likely be critical factors in the company’s future performance and potential deleveraging efforts.

Investors will be watching closely to see if the operational improvements highlighted in the presentation translate into improved earnings performance in upcoming quarters, particularly given the significant EPS miss in Q1 2025 and the company’s ongoing balance sheet challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.