Palantir shares slip premarket despite posting record revenue in third quarter

Introduction & Market Context

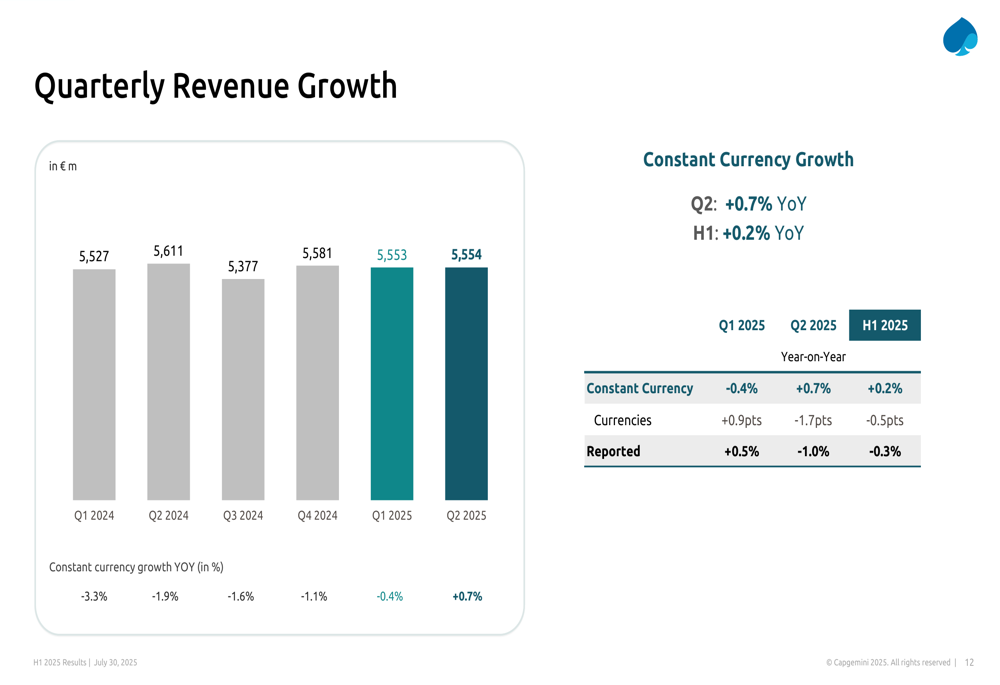

Capgemini (EURONEXT:CAP) released its H1 2025 results on July 30, showing a return to positive growth in the second quarter after several consecutive quarters of decline. The IT services and consulting firm reported H1 2025 revenues of €11,107 million, representing a modest 0.2% year-over-year increase at constant currency, with Q2 showing stronger momentum at 0.7% growth.

The results demonstrate Capgemini’s gradual recovery amid challenging market conditions, with the company narrowing its full-year revenue growth guidance while maintaining its profitability targets. The firm’s strategic focus on artificial intelligence appears to be gaining traction, with 7% of Q2 bookings being AI-powered.

Quarterly Performance Highlights

Capgemini’s quarterly revenue trend shows a steady improvement throughout 2024 and into 2025, finally returning to positive territory in Q2 2025 after five consecutive quarters of year-over-year declines.

As shown in the following chart of quarterly revenue growth, the company has been steadily improving its performance trajectory:

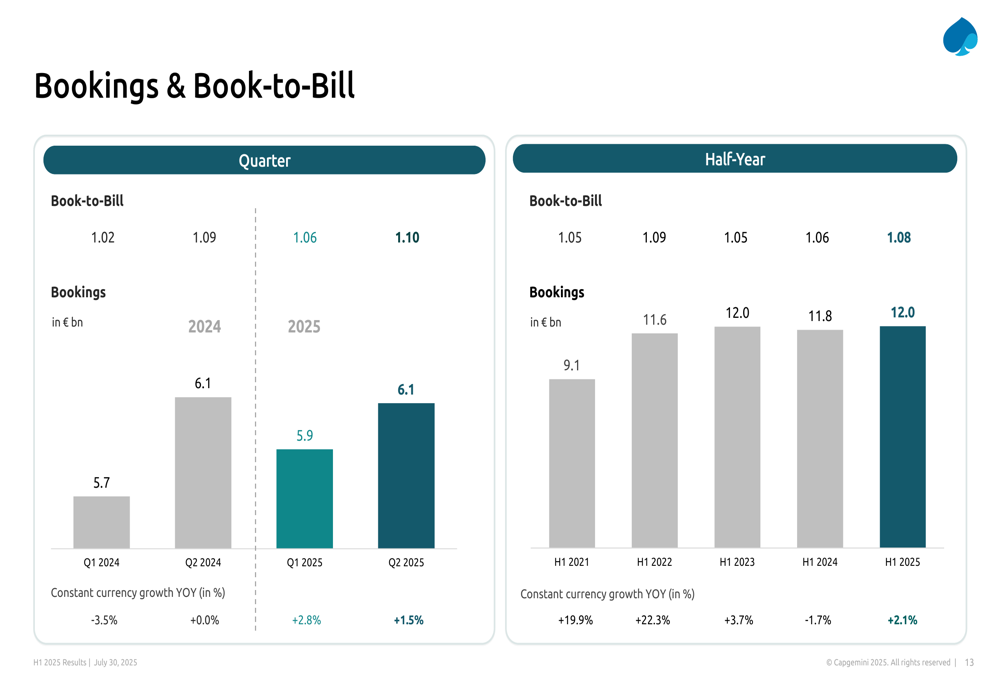

The company’s bookings reached €11,993 million for H1 2025, with Q2 bookings at €6,109 million. The book-to-bill ratio stood at 1.08 for the half-year and 1.10 for Q2, indicating healthy demand for Capgemini’s services despite market challenges.

The following chart illustrates the evolution of bookings and book-to-bill ratio over recent quarters:

Regional and Sector Analysis

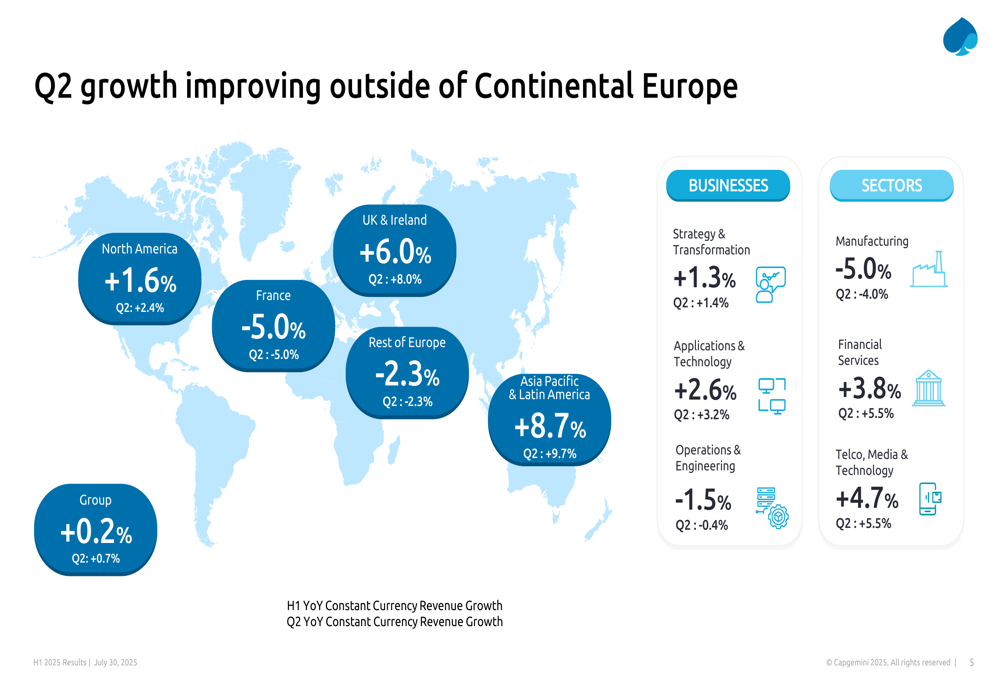

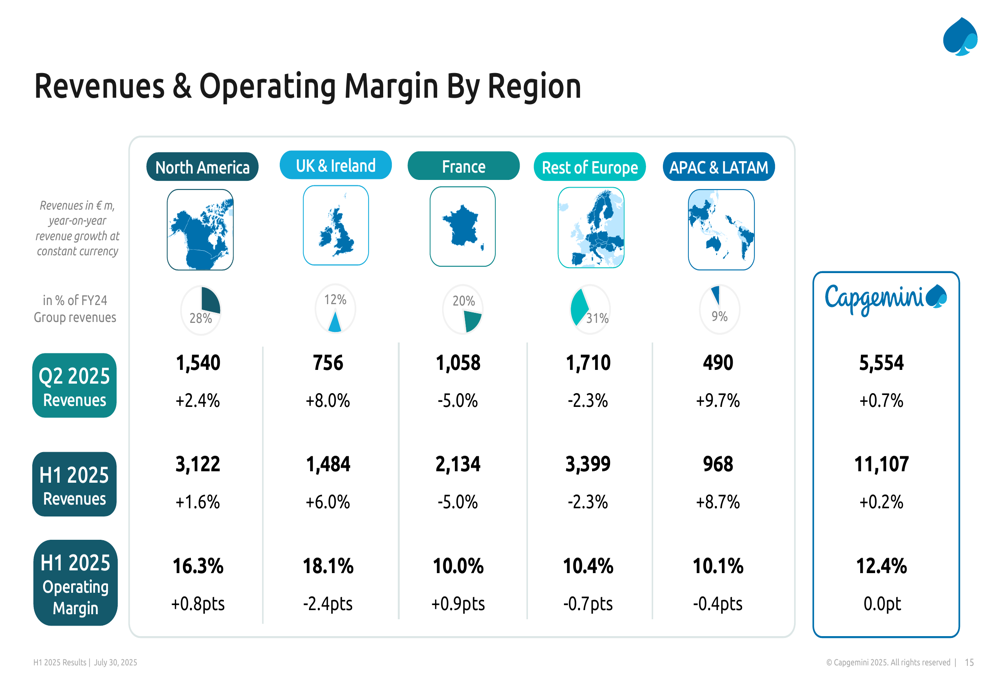

Capgemini’s performance varied significantly across regions and sectors. The UK & Ireland and Asia-Pacific & Latin America regions showed strong growth at 8.0% and 9.7% respectively in Q2, while France declined by 5.0% and the Rest of Europe contracted by 2.3%.

The geographical performance breakdown is illustrated in this chart:

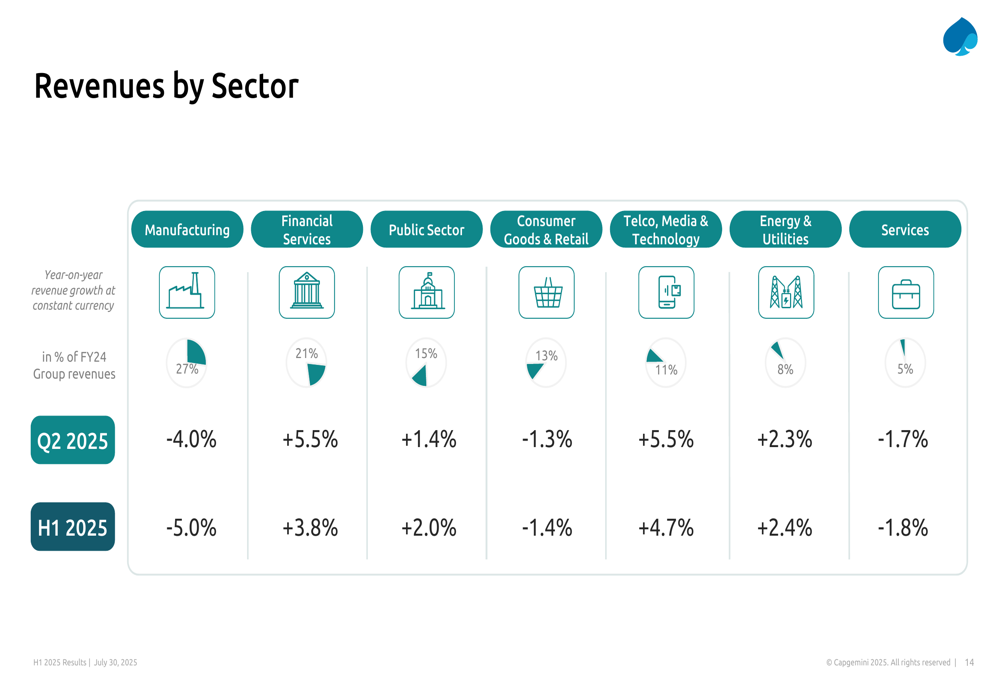

By sector, Financial Services (+5.5% in Q2) and Telecommunications, Media & Technology (+5.5% in Q2) were the strongest performers, while Manufacturing continued to struggle with a 4.0% decline in Q2.

The following breakdown shows revenue by sector and the corresponding growth rates:

Operating margins also varied significantly by region, with the UK & Ireland achieving the highest margin at 18.1%, followed by North America at 16.3%. Other regions maintained margins around 10%, resulting in an overall group operating margin of 12.4%.

This regional margin performance is detailed in the following table:

Strategic Initiatives

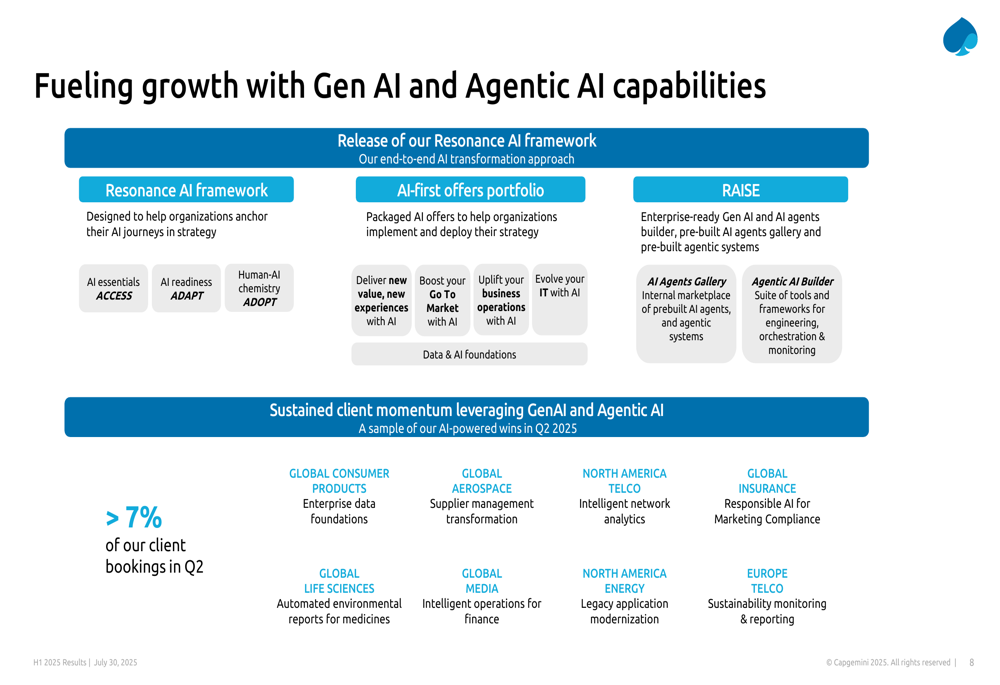

Capgemini is increasingly focusing on artificial intelligence as a key growth driver, with the company highlighting its "Resonance AI Framework" and "Agentic AI" offerings. The company reported that 7% of client bookings in Q2 were AI-powered, indicating growing traction for these services.

CEO Aiman Ezzat emphasized the company’s AI strategy during the presentation, showcasing several AI-powered client wins across various sectors:

The company also highlighted its focus on cloud technologies, data services, and digital transformation as areas of "proven solutions with continuous momentum," while identifying GenAI, Agentic AI, and Defense & Sovereignty as areas with "fast-rising and accelerating momentum."

Financial Analysis

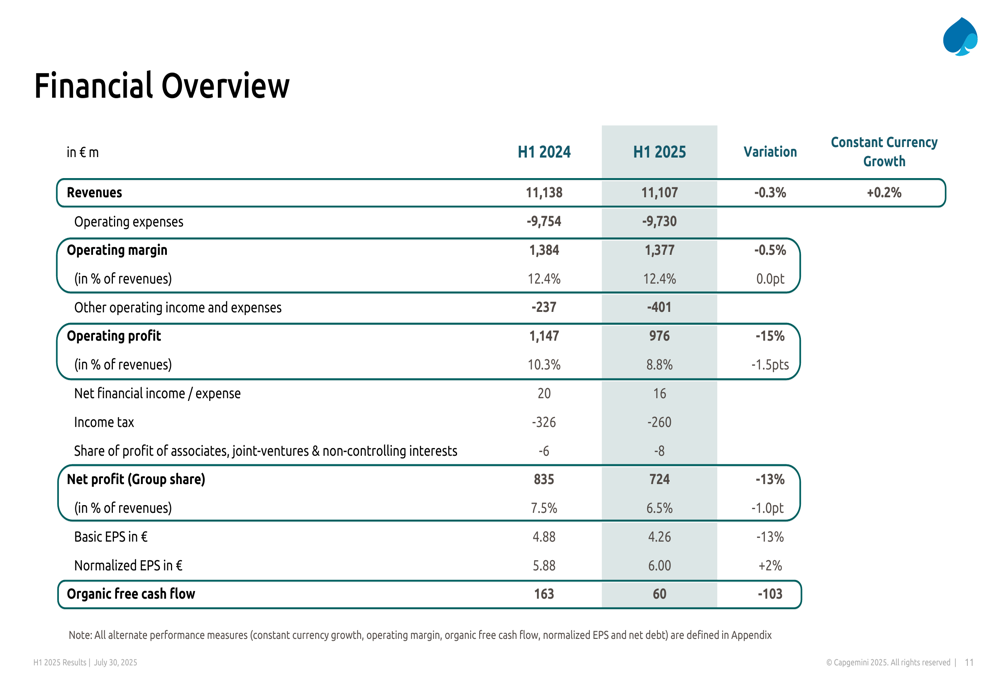

Despite the return to revenue growth, Capgemini’s profitability metrics showed mixed results. The operating margin remained stable at 12.4% of revenues (€1,377 million), consistent with H1 2024. However, net profit (Group share) declined by 13% to €724 million, with basic EPS falling to €4.26 from €4.88 in H1 2024.

The following table provides a comprehensive overview of Capgemini’s financial performance:

Normalized EPS, which excludes exceptional items, increased by 2% to €6.00, suggesting that the underlying business performance remains resilient despite one-time charges affecting reported earnings.

Organic free cash flow declined to €60 million from €163 million in H1 2024, representing a decrease of €103 million. Net debt remained stable at €2.8 billion as of June 30, 2025, unchanged from the same period last year.

Forward-Looking Statements

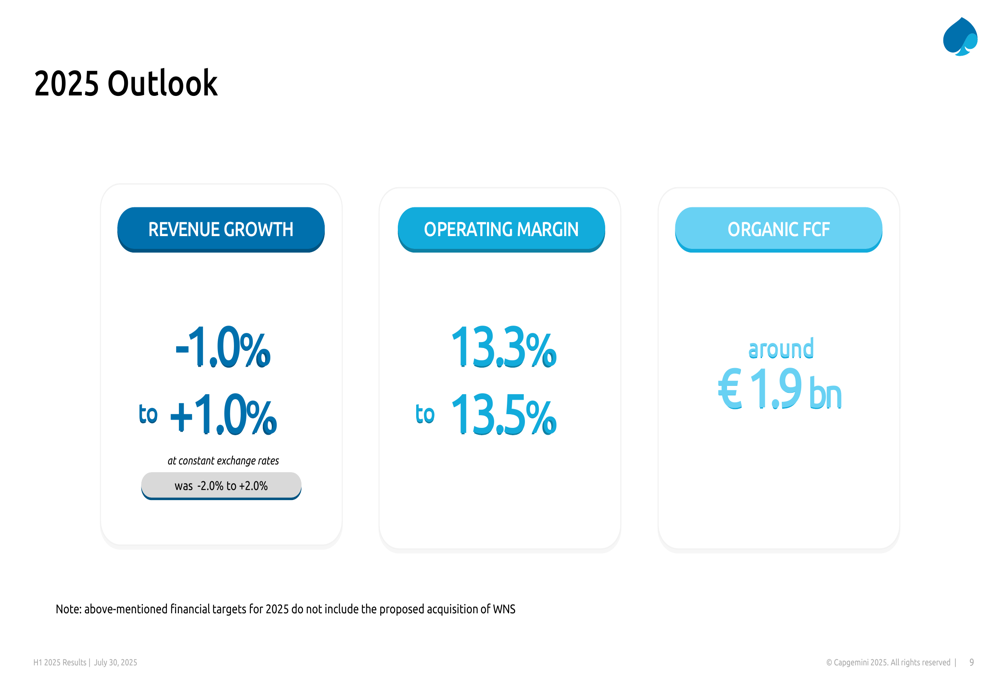

Capgemini has narrowed its revenue growth guidance for 2025 to a range of -1.0% to +1.0% at constant exchange rates, compared to the previous guidance of -2.0% to +2.0%. This adjustment reflects both the improved performance in Q2 and continued caution about market conditions.

The company maintained its operating margin target of 13.3% to 13.5% and expects organic free cash flow to be around €1.9 billion for the full year. These targets exclude the impact of the proposed acquisition of WNS (NYSE:WNS).

The updated outlook is summarized in this slide:

Operational Metrics

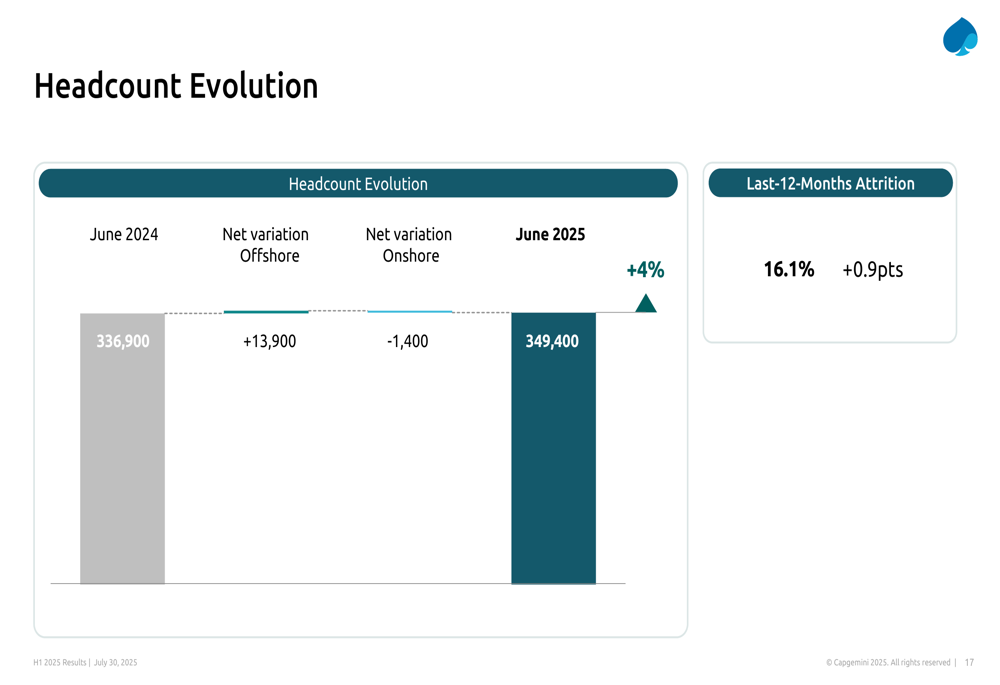

Capgemini’s total headcount increased to 349,400 employees as of June 2025, representing a 4% increase year-over-year. The growth was primarily driven by offshore resources, which increased by 13,900, while onshore headcount decreased by 1,400.

The company’s attrition rate stood at 16.1%, an increase of 0.9 percentage points compared to the previous year, indicating some challenges in employee retention amid a competitive talent market.

The following chart illustrates the headcount evolution:

In conclusion, Capgemini’s H1 2025 results show signs of recovery with a return to positive growth in Q2, driven by strong performance in Financial Services and Technology sectors, as well as in the UK & Ireland and Asia-Pacific regions. The company’s strategic focus on AI appears to be gaining traction, though challenges remain in the Manufacturing sector and in certain European markets. The narrowed revenue guidance reflects both the improved trajectory and continued caution about market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.