BofA update shows where active managers are putting money

Introduction & Market Context

Capstone Copper Corp. (TSX:CS) presented its Q2 2025 results on July 31, showcasing record copper production and improved cost metrics across its operations. The company, which operates five mines across the Americas, has positioned itself to benefit from strong copper market fundamentals with prices averaging $4.32/lb during the quarter.

The presentation highlighted Capstone’s progress in executing its growth strategy while maintaining financial discipline, with the stock closing at $7.53 on July 31, representing a 3.19% increase on the day of the announcement.

Quarterly Performance Highlights

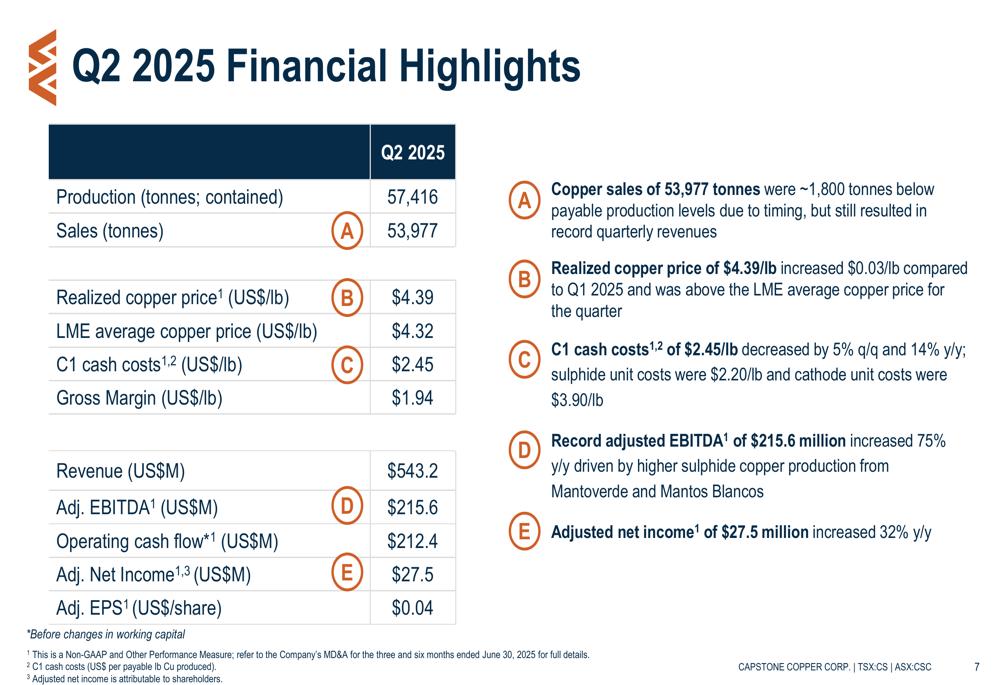

Capstone delivered consolidated copper production of 57,416 tonnes in Q2 2025, with year-to-date production reaching 111,212 tonnes. The company achieved C1 cash costs of $2.45/lb, representing a 5% decrease quarter-over-quarter and a 14% improvement year-over-year.

As shown in the following quarterly performance summary:

Financial results were equally strong, with revenue of $543.2 million and adjusted EBITDA of $215.6 million. The company generated operating cash flow of $212.4 million, while adjusted net income came in at $27.5 million, translating to adjusted earnings per share of $0.04.

The following slide details the key financial metrics for the quarter:

Management noted that copper sales were approximately 1,800 tonnes below payable production levels during the quarter. The realized copper price of $4.39/lb represented a $0.03/lb increase compared to Q1 2025, contributing to the strong financial performance.

Operational Updates by Mine

Mantoverde

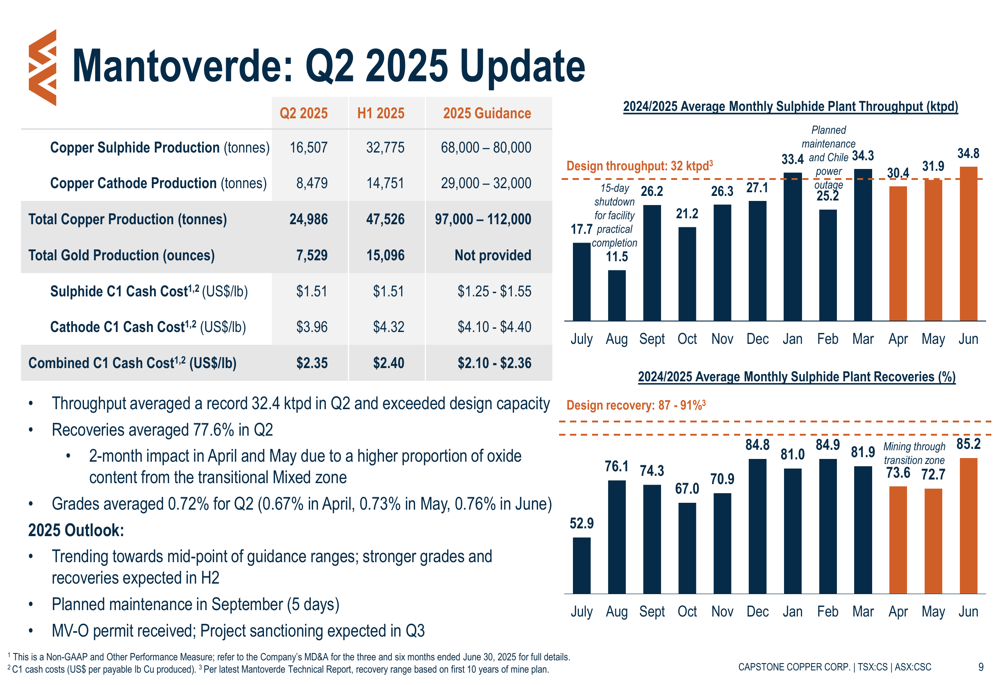

Mantoverde emerged as a standout performer with total copper production of 24,986 tonnes in Q2, comprising 16,507 tonnes from sulphide operations and 8,479 tonnes from cathode production. The operation also produced 7,529 ounces of gold. C1 cash costs were particularly impressive at $1.51/lb for sulphide operations and $2.35/lb combined.

The mine achieved record throughput averaging 32.4 ktpd in Q2, with recoveries averaging 77.6% and grades of 0.72%. The following slide illustrates Mantoverde’s performance:

The company highlighted the successful ramp-up of the Mantoverde Development Project, which achieved commercial production in September 2024 and reached design throughput rates in the fourth quarter of operation.

Mantos Blancos

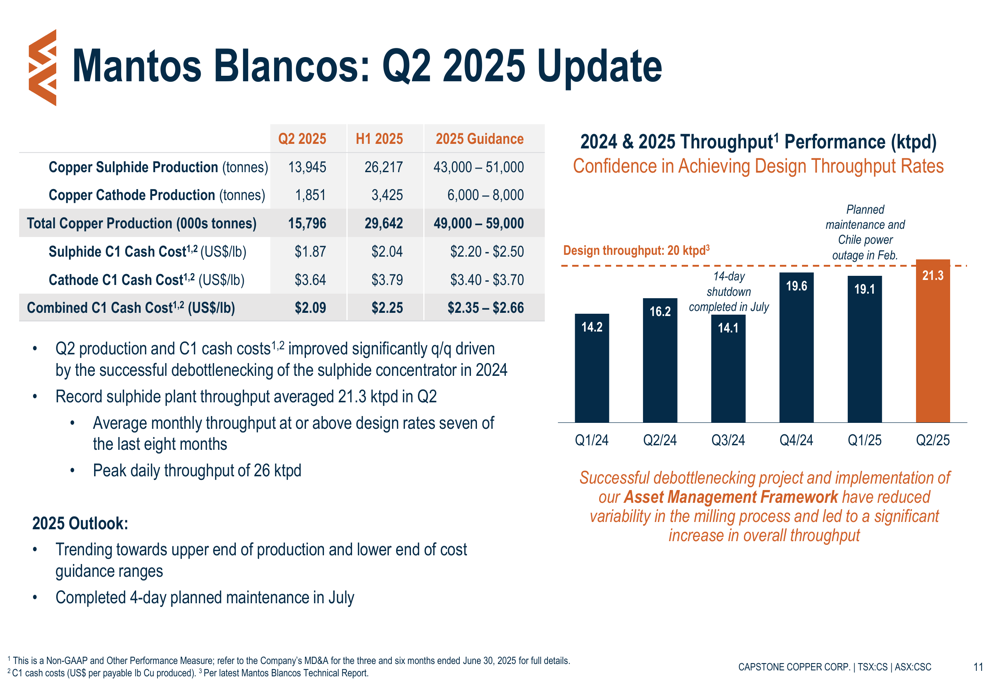

Mantos Blancos delivered total copper production of 15,796 tonnes in Q2, with combined C1 cash costs of $2.09/lb. The operation achieved average throughput of 21.3 ktpd and is trending toward the upper end of its production guidance.

Pinto Valley and Cozamin

Pinto Valley produced 10,125 tonnes of copper at C1 cash costs of $3.89/lb, with production impacted by throughput restrictions during the quarter. Meanwhile, Cozamin delivered 6,509 tonnes of copper at industry-leading C1 cash costs of $1.49/lb, representing a 16% year-over-year improvement driven by higher production.

Growth Strategy and Outlook

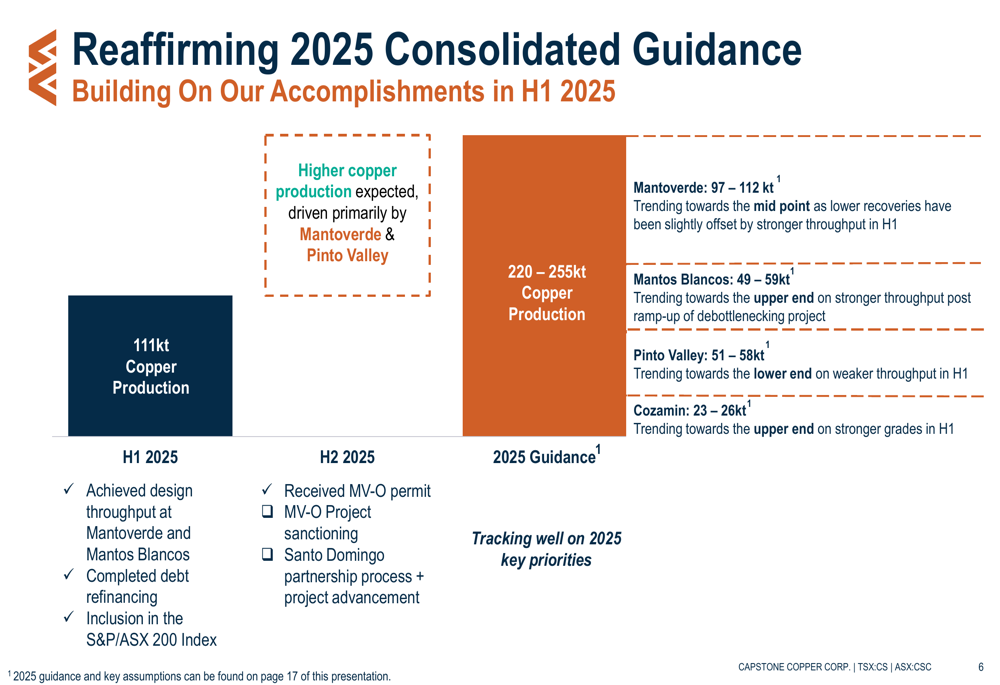

Capstone reaffirmed its 2025 consolidated copper production guidance of 220-255 kt, with the company on track to meet these targets following first-half production of 111 kt. Management highlighted several key milestones achieved in H1 2025 and outlined priorities for the second half of the year, including the recently received Mantoverde Optimization Project permit and upcoming project sanctioning.

The following slide details the company’s 2025 guidance by operation:

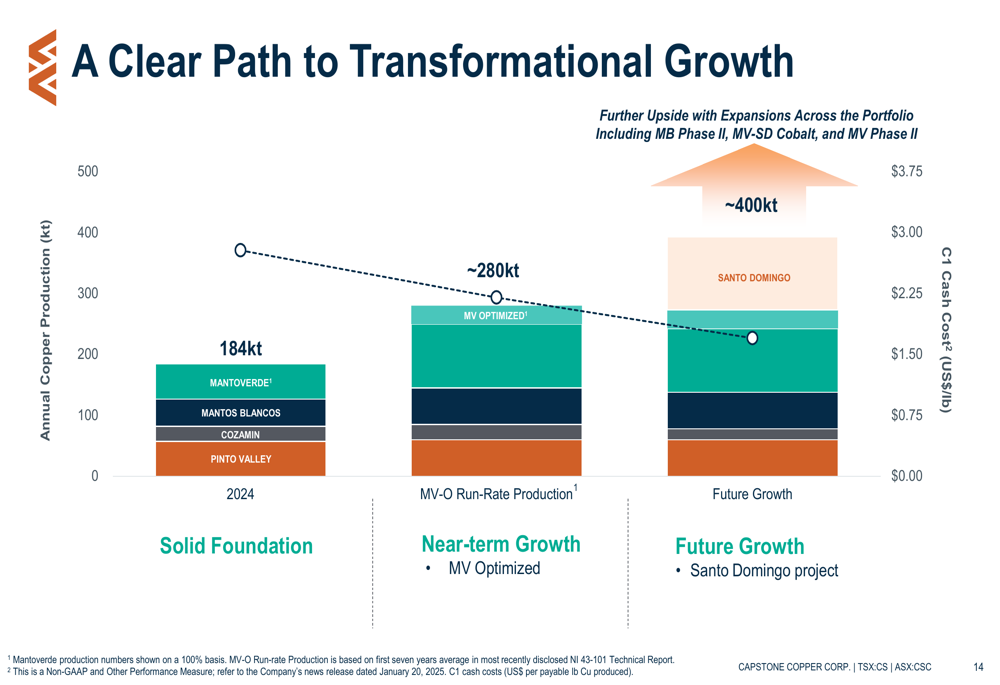

Looking beyond 2025, Capstone presented a clear growth trajectory aimed at nearly doubling annual copper production from 184 kt in 2024 to approximately 400 kt through a series of expansion projects. This growth strategy is illustrated in the following slide:

The company’s growth plan includes near-term expansion through the Mantoverde Optimization Project, followed by future growth initiatives including the Santo Domingo project, Mantos Blancos Phase II, and Mantoverde Phase II.

Financial Position and Flexibility

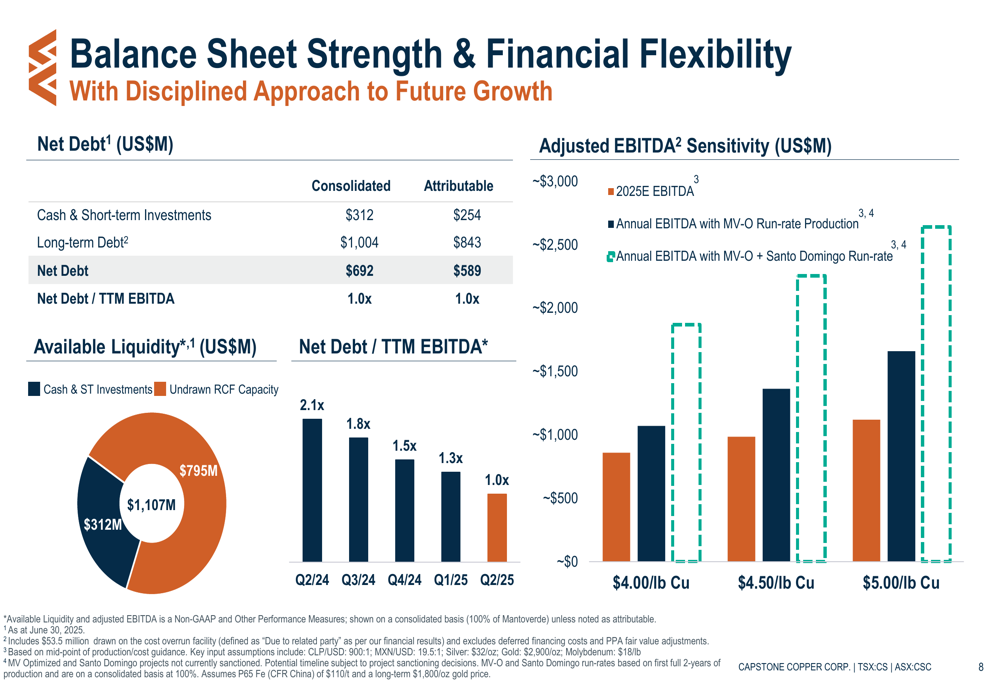

Capstone reported a strong balance sheet with net debt of $692 million (consolidated) and $589 million (attributable), representing a net debt to trailing twelve-month EBITDA ratio of 1.0x. Available liquidity stood at $1.1 billion, comprising $312 million in cash and short-term investments plus $795 million in undrawn revolving credit facility capacity.

The following slide illustrates the company’s financial position and flexibility:

Management emphasized that this financial strength provides the company with ample flexibility to fund its growth initiatives, including the development of the Santo Domingo project. The company also presented EBITDA sensitivity analysis at various copper price scenarios, demonstrating significant upside potential as expansion projects come online.

Capstone completed a debt refinancing during the quarter, with its debt maturity profile now extending from 2026 to 2033, further enhancing financial flexibility.

In summary, Capstone Copper’s Q2 2025 results demonstrate operational excellence across its portfolio, with record production, improving costs, and a clear path to growth supported by a robust balance sheet. The company appears well-positioned to execute its ambitious expansion plans while maintaining financial discipline in a favorable copper price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.