SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Castle Biosciences, Inc. (NASDAQ:CSTL) presented its Q2 2025 corporate results on August 4, 2025, highlighting strong test volume growth alongside declining margins and profitability metrics. The molecular diagnostics company, which specializes in tests for dermatology, ophthalmology, and gastroenterology, saw its shares trading near 52-week lows at $14.65 despite reporting positive test adoption trends.

The company’s presentation comes after a challenging first quarter that saw a significant net loss and an EPS miss that triggered market concerns. While Q2 shows improvement in some metrics, the overall financial picture remains mixed as Castle continues to invest in strategic growth initiatives.

Quarterly Performance Highlights

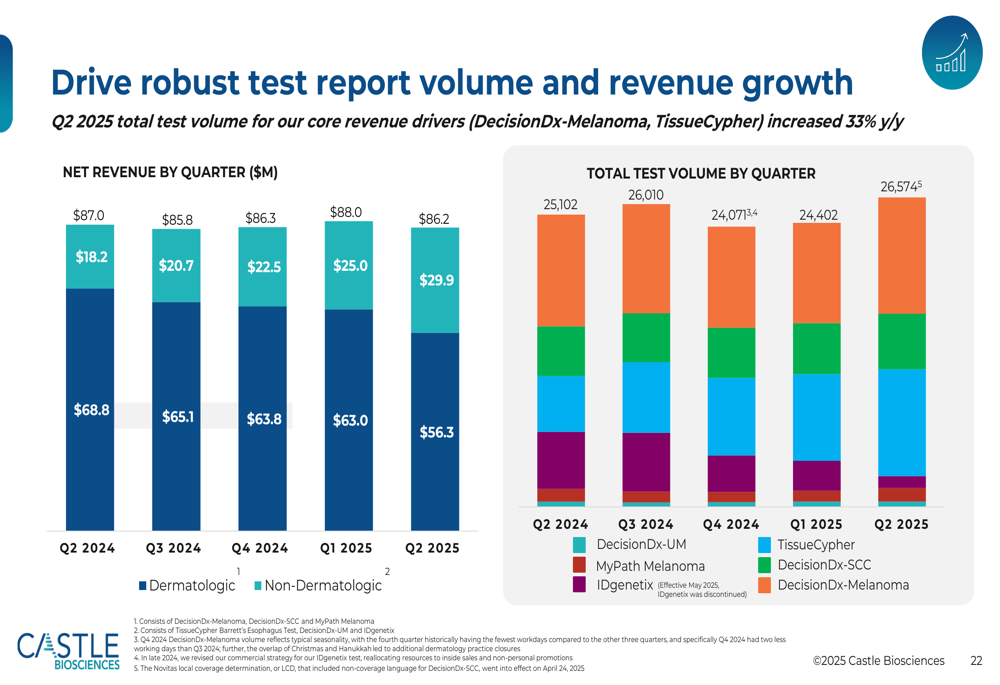

Castle Biosciences reported that its Q2 2025 total test reports for core revenue drivers (DecisionDx-Melanoma and TissueCypher) increased 33% compared to Q2 2024, demonstrating strong market adoption of its diagnostic solutions.

As shown in the following quarterly test volume chart, the company delivered 26,574 total test reports in Q2 2025, up from 25,102 in the same period last year:

Total (EPA:TTEF) revenue for Q2 2025 was $86.2 million, reflecting a slight decrease from $88.0 million in Q1 2025. Notably, the revenue mix continues to shift, with dermatology revenue declining to $56.3 million (from $63.0 million in Q1) while non-dermatology revenue increased to $29.9 million (from $25.0 million in Q1), indicating the growing importance of Castle’s diversification strategy.

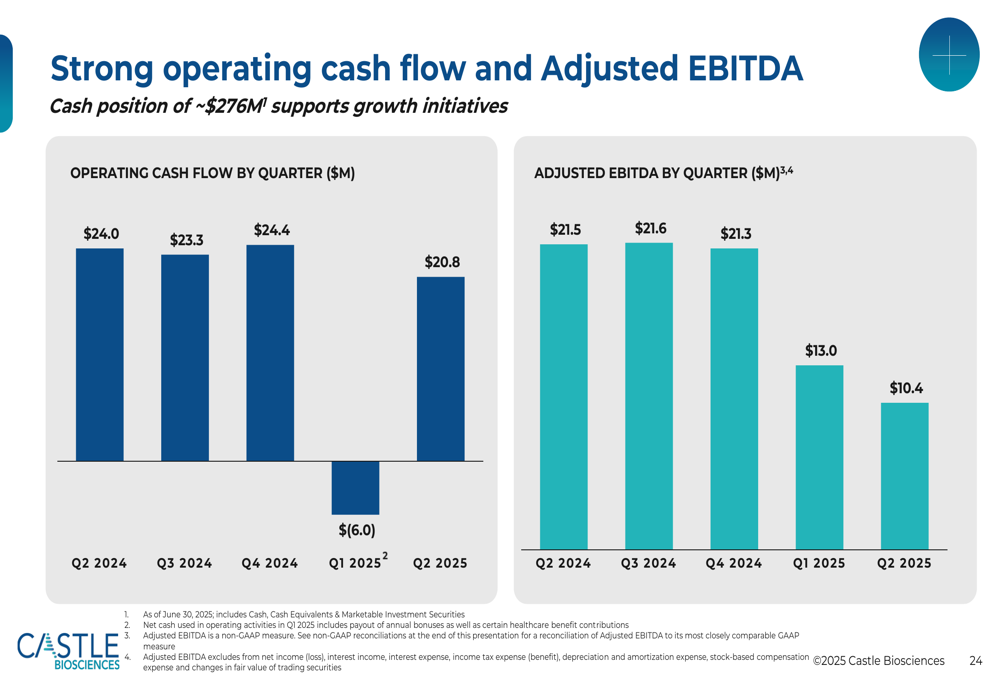

The company reported net income of $4.5 million for Q2 2025, a significant improvement from the $25.8 million net loss reported in Q1. However, profitability metrics show concerning trends, with Adjusted EBITDA declining to $10.4 million in Q2 2025 compared to $21.5 million in Q2 2024.

The following chart illustrates the company’s quarterly operating cash flow and Adjusted EBITDA trends:

Strategic Initiatives

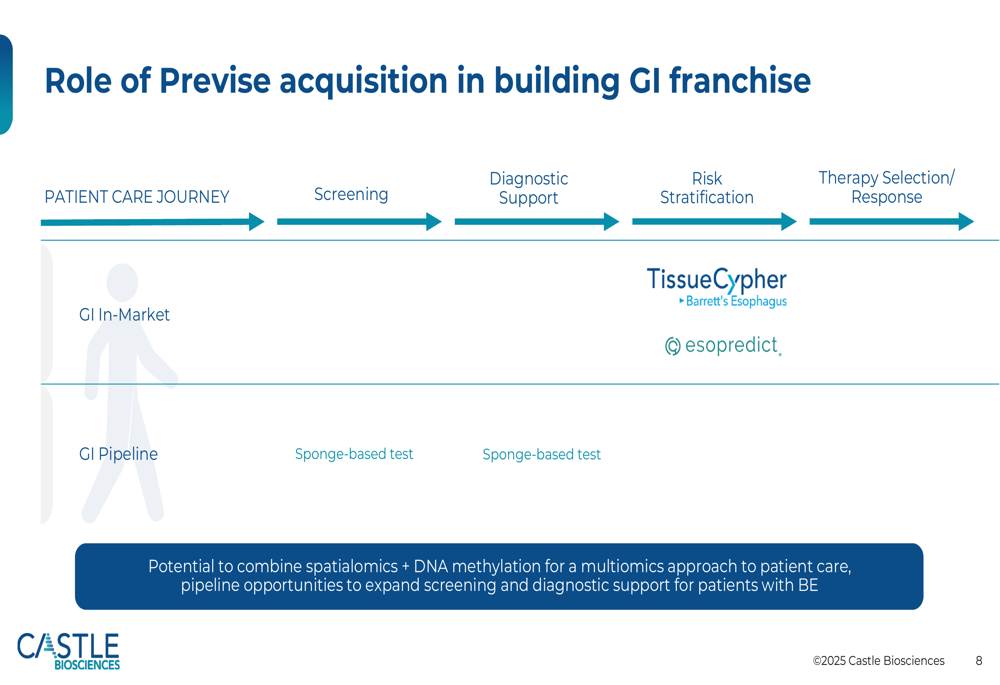

Castle Biosciences highlighted two significant strategic developments in its presentation: the acquisition of Previse, a gastrointestinal health company, and a new collaboration and license agreement with SciBase.

The Previse acquisition strengthens Castle’s gastroenterology franchise, complementing its existing TissueCypher test for Barrett’s Esophagus. As illustrated in the following slide, the acquisition helps Castle build a comprehensive GI testing portfolio across the patient care journey:

Similarly, the SciBase collaboration aims to expand Castle’s presence in the atopic dermatitis (AD) market, which affects approximately 24 million diagnosed patients in the United States. The partnership focuses on developing tests for both mild AD patients using topical treatments and moderate-to-severe AD patients requiring systemic therapies.

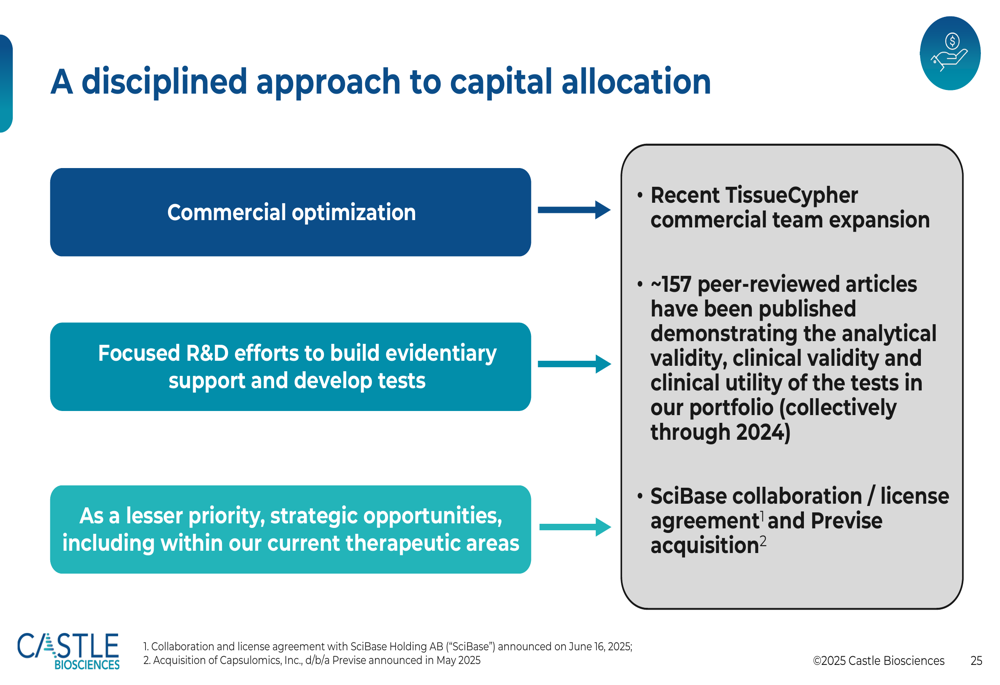

The company also highlighted its disciplined approach to capital allocation, prioritizing commercial optimization and focused R&D efforts:

Detailed Financial Analysis

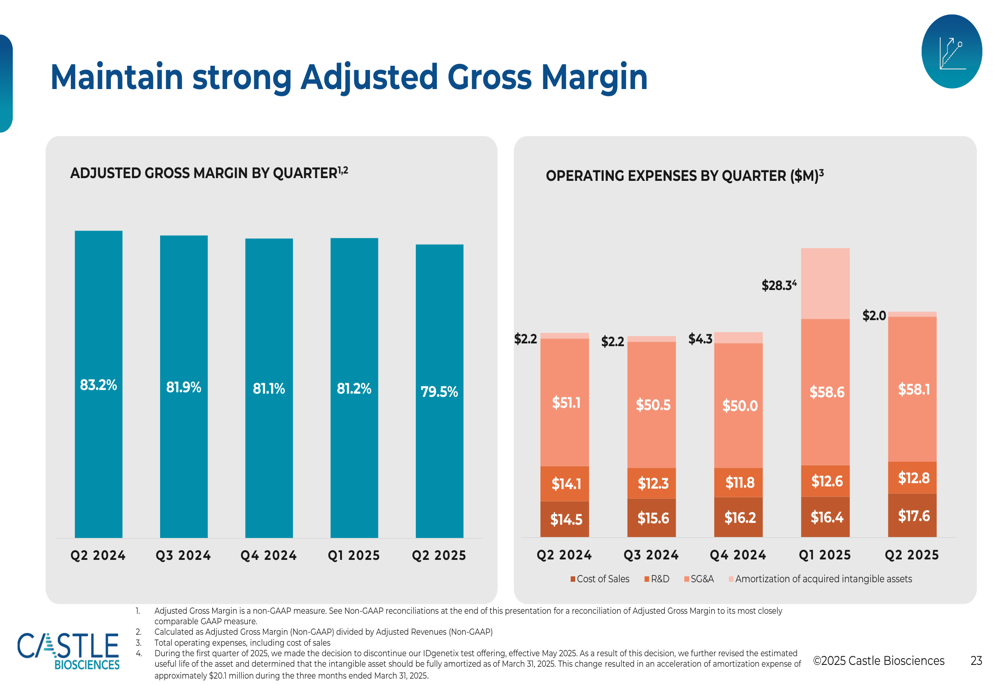

Castle Biosciences’ Q2 2025 financial results reveal several important trends. While Gross Margin for Q2 2025 was 77% and Adjusted Gross Margin was 80%, both metrics declined compared to Q2 2024 levels of 81% and 83% respectively. This margin compression is illustrated in the following chart:

Net cash provided by operations in Q2 2025 was $20.8 million, down from $24.0 million in Q2 2024, though still representing a significant improvement from the negative operating cash flow of $(6.0) million in Q1 2025. The company maintained a strong balance sheet with cash, cash equivalents and marketable investment securities totaling $275.9 million as of June 30, 2025.

Operating expenses have increased across several categories, potentially contributing to the declining EBITDA. The company appears to be investing heavily in its commercial infrastructure and R&D initiatives to support long-term growth, though this is creating near-term pressure on profitability.

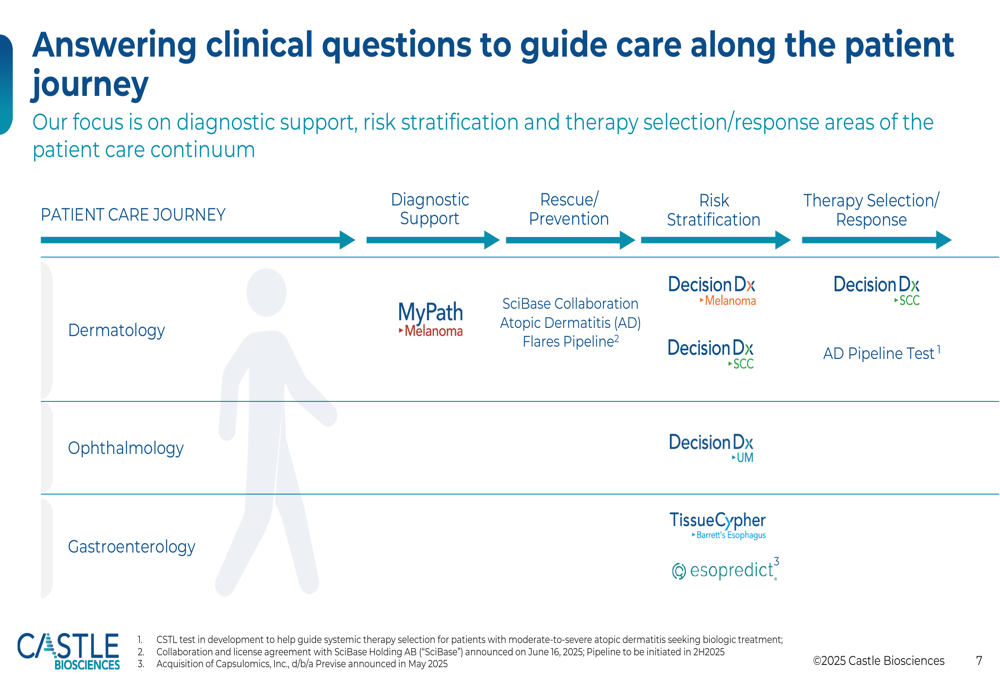

Product Portfolio and Clinical Evidence

Castle Biosciences emphasized the clinical value of its diagnostic tests throughout the presentation. The company’s tests address critical clinical questions across the patient journey in dermatology, ophthalmology, and gastroenterology.

As shown in the following slide, Castle’s tests provide valuable clinical information that guides patient care decisions:

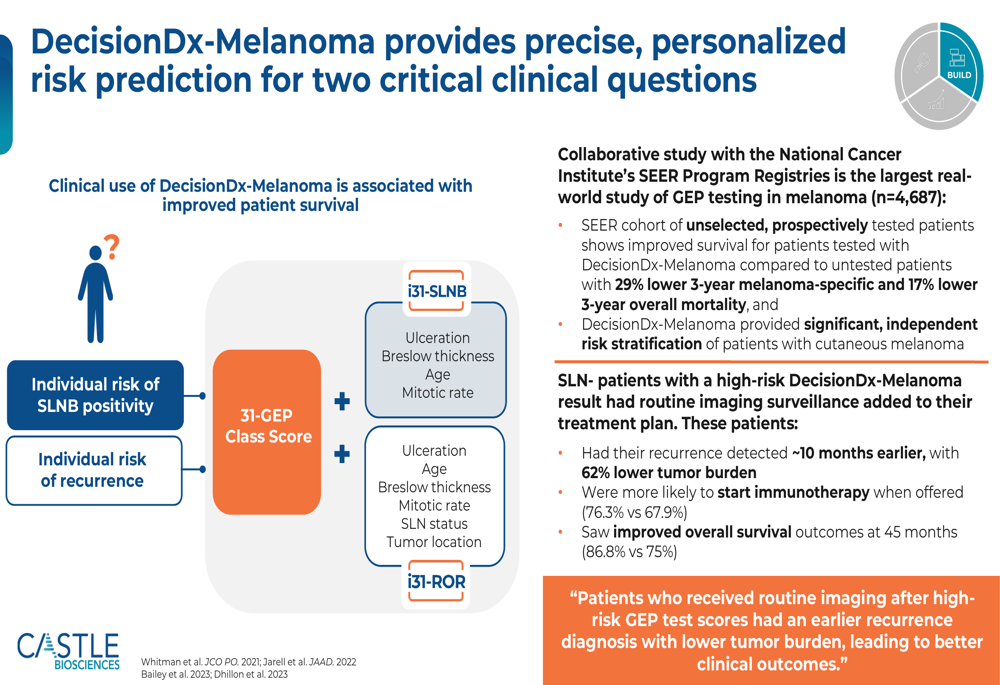

The company highlighted strong clinical evidence supporting its flagship tests, including DecisionDx-Melanoma, DecisionDx-SCC, and TissueCypher. For example, DecisionDx-Melanoma provides personalized risk prediction for melanoma patients, potentially reducing unnecessary procedures and improving patient outcomes:

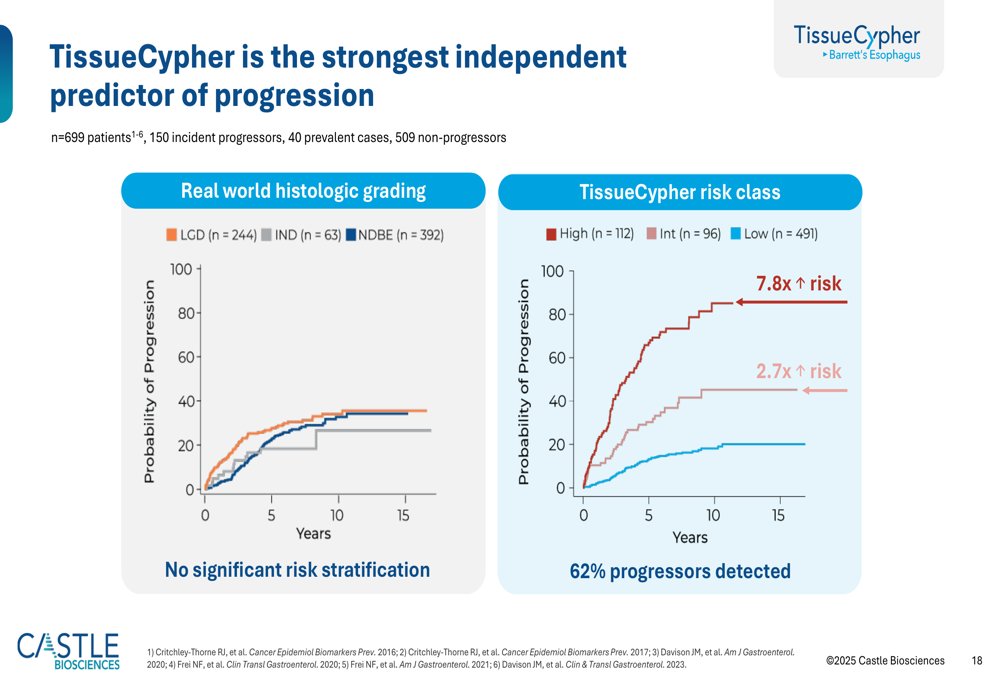

Similarly, TissueCypher was presented as the strongest independent predictor of progression to high-grade dysplasia or esophageal adenocarcinoma, offering significant clinical value:

Forward-Looking Statements

Castle Biosciences outlined its strategy for continued value creation, focusing on driving robust test volume growth, maintaining strong adjusted gross margins, and achieving operating cash flow positivity by the end of 2025.

The company’s pipeline includes an Atopic Dermatitis Gene Expression Profile Test, expected to launch by the end of 2025. This test aims to help identify appropriate therapies for patients with moderate to severe atopic dermatitis, potentially expanding Castle’s footprint in the dermatology market.

Despite the positive outlook presented in the slides, investors should note the declining margins and EBITDA trends, which may explain the stock’s current trading near 52-week lows. The company’s ability to reverse these trends while continuing to invest in strategic growth initiatives will likely be critical for future stock performance.

Market Reaction and Analyst Perspectives

Following the presentation, Castle Biosciences’ stock remained under pressure, trading at $14.65, just above its 52-week low of $14.59. This represents a significant disconnect between the company’s narrative of strong test adoption and strategic expansion and the market’s apparent concerns about profitability and financial performance.

According to the previous earnings report context, analyst consensus remains bullish on Castle Biosciences, with price targets ranging from $30-$44, suggesting significant upside potential from current levels. However, the market appears to be focusing on the company’s financial challenges rather than its long-term growth potential.

The mixed Q2 2025 results, featuring strong test volume growth but declining margins and profitability metrics, reflect a company in transition as it expands beyond its core dermatology business into gastroenterology and new dermatology applications. Whether this strategic diversification will ultimately deliver shareholder value remains to be seen, as the company works toward its goal of operating cash flow positivity by year-end.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.