Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Cathay General Bancorp (NASDAQ:CATY) presented its first quarter 2025 financial results on April 21, 2025, revealing a decline in earnings compared to previous periods while maintaining solid fundamentals. The bank’s stock responded positively in aftermarket trading, rising 3.6% to $39.99, suggesting investors may have anticipated worse results.

The presentation comes as banks continue to navigate a challenging interest rate environment, with the Federal Reserve having begun its rate-cutting cycle in late 2024. Cathay’s results reflect both the opportunities and challenges presented by this transition.

Quarterly Performance Highlights

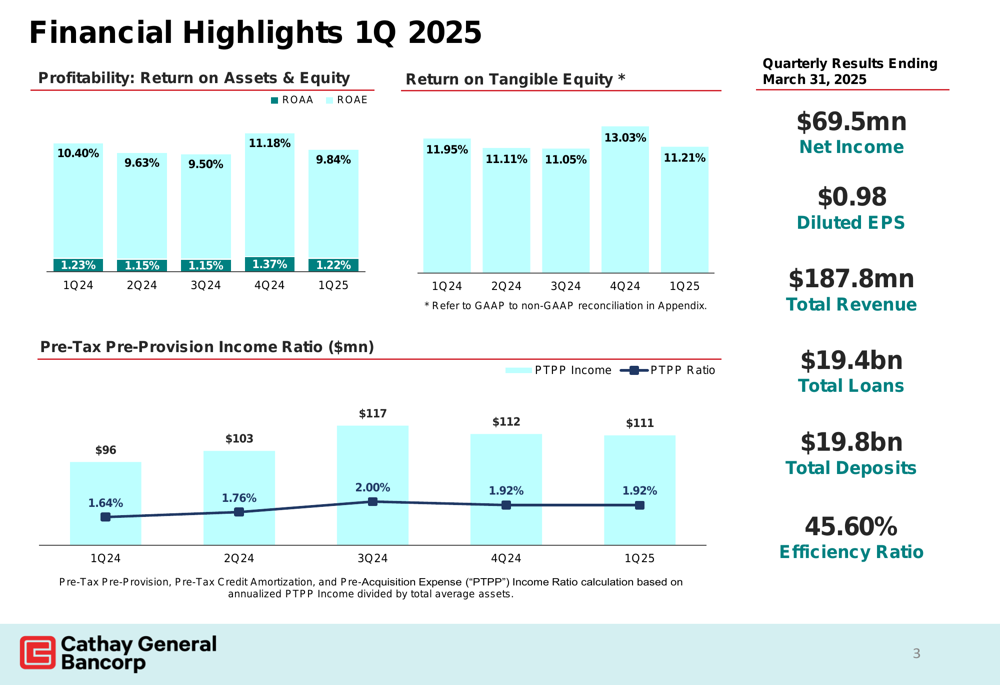

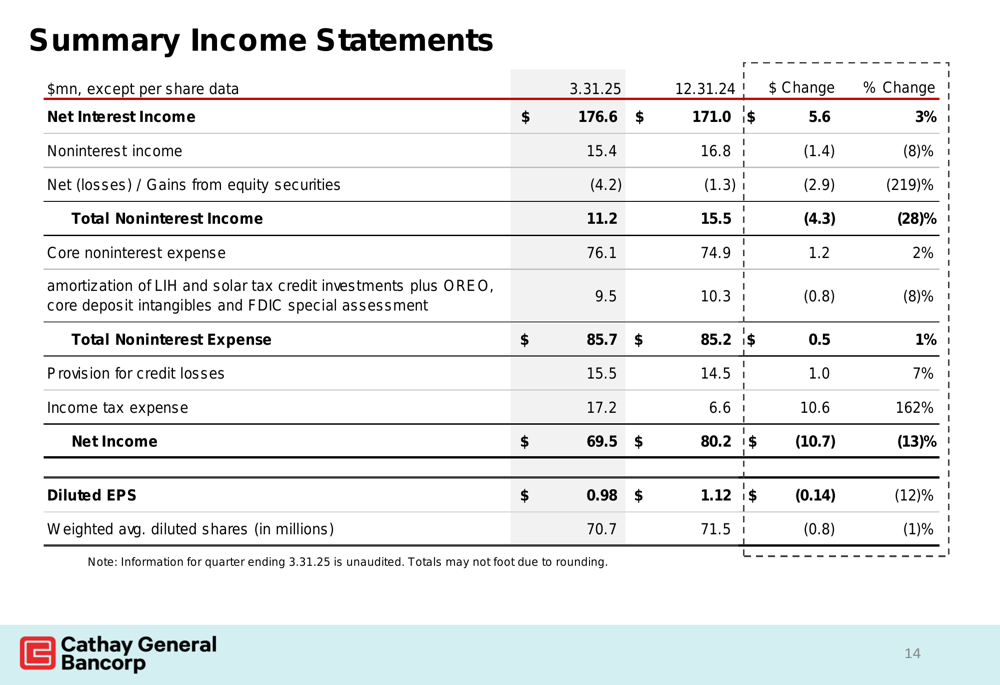

Cathay reported net income of $69.5 million for Q1 2025, representing a 13% decrease from the previous period’s $80.2 million. Diluted earnings per share fell 12% to $0.98 from $1.12. Despite this decline, the bank maintained strong profitability metrics and an efficiency ratio of 45.60%.

As shown in the following financial highlights chart, the bank generated total revenue of $187.8 million, with total loans at $19.4 billion and total deposits at $19.8 billion:

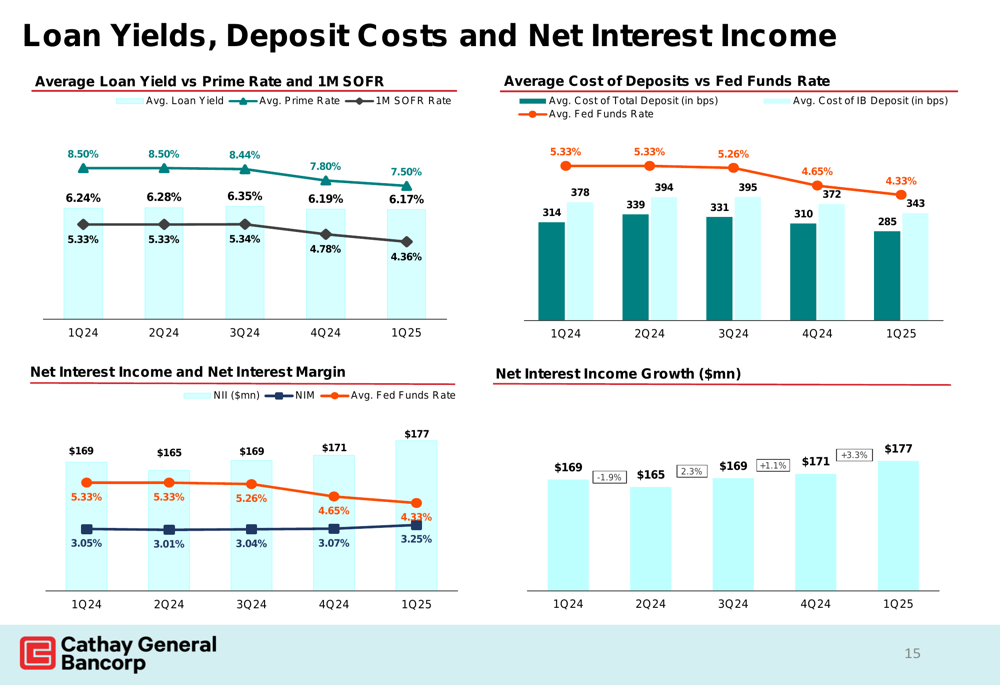

Net interest income increased by $5.6 million or 3% compared to the previous period, reaching $176.6 million. However, this was offset by a significant decline in noninterest income, which fell by $4.3 million or 28% to $11.2 million. The presentation highlighted net losses from equity securities of $4.2 million as a contributing factor to this decline.

The bank’s summary income statement provides a clear picture of these financial trends:

Balance Sheet and Capital Position

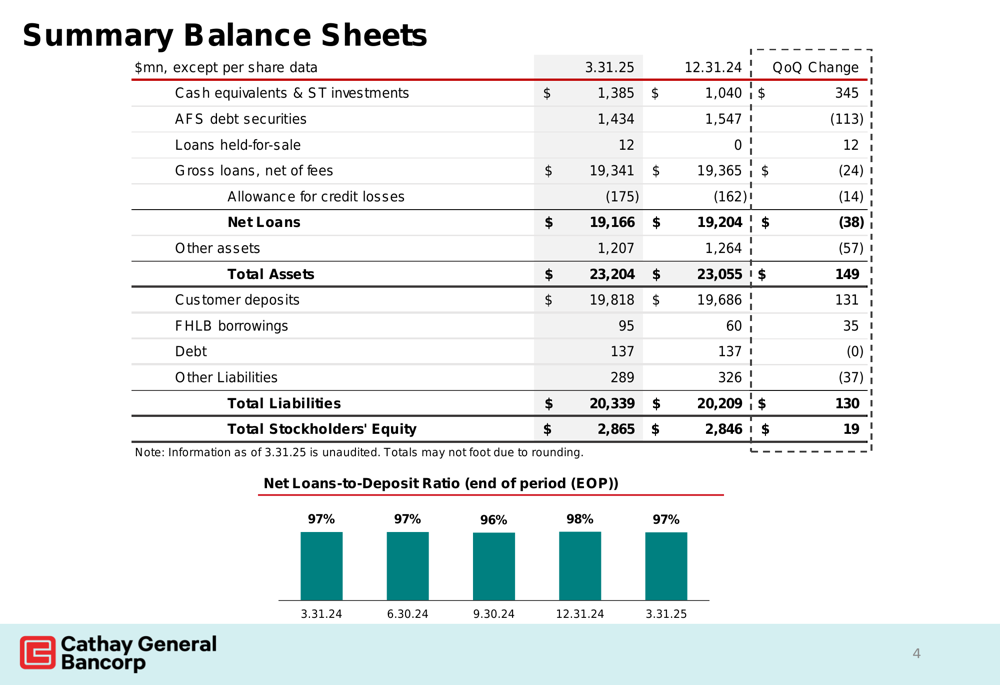

Cathay’s balance sheet showed modest growth, with total assets increasing by $149 million to $23.2 billion as of March 31, 2025. Customer deposits grew by $131 million to $19.8 billion, while total stockholders’ equity increased by $19 million to $2.9 billion.

The following summary balance sheet highlights these changes:

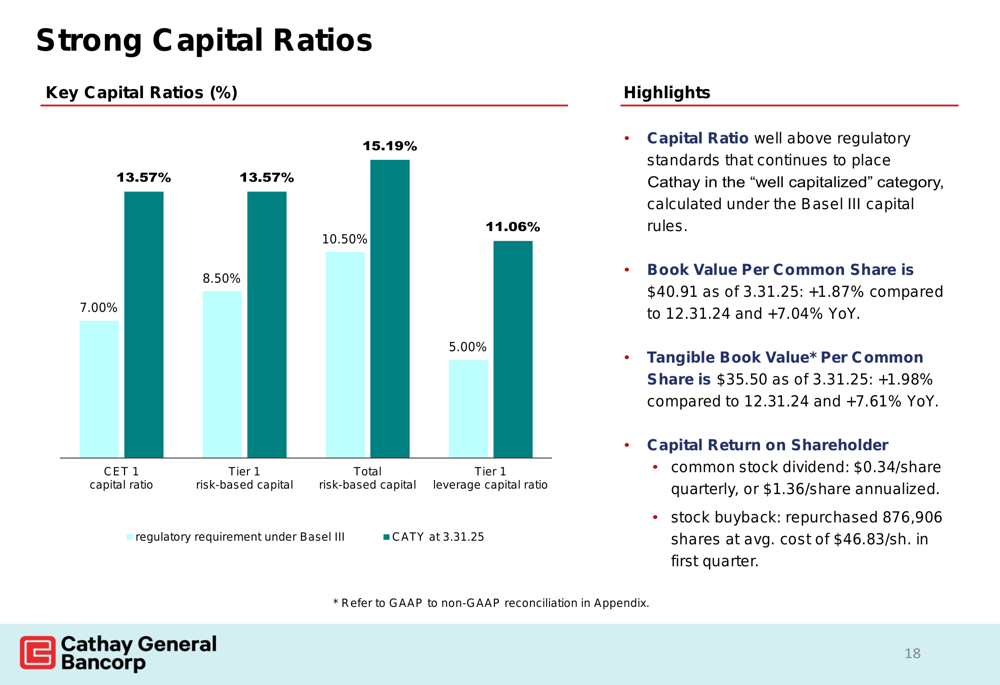

The bank maintained strong capital ratios, well above regulatory requirements, positioning it to weather potential economic challenges. Cathay’s capital strength is also supporting continued shareholder returns through stock repurchases.

The following chart illustrates the bank’s robust capital position:

Loan Portfolio and Risk Management

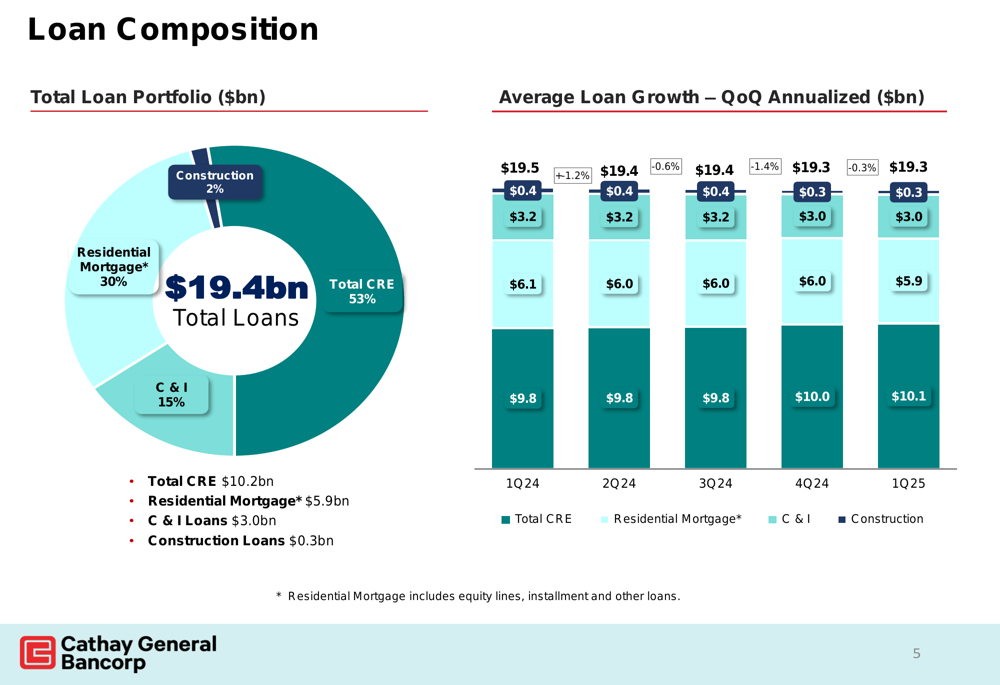

Cathay’s loan portfolio remained relatively stable at $19.4 billion, with a slight decrease of $24 million in gross loans compared to the previous quarter. The portfolio maintains a diversified composition with commercial real estate (CRE) loans representing 53%, residential mortgages 30%, commercial and industrial (C&I) loans 15%, and construction loans 2%.

The following chart provides a detailed breakdown of the loan portfolio composition:

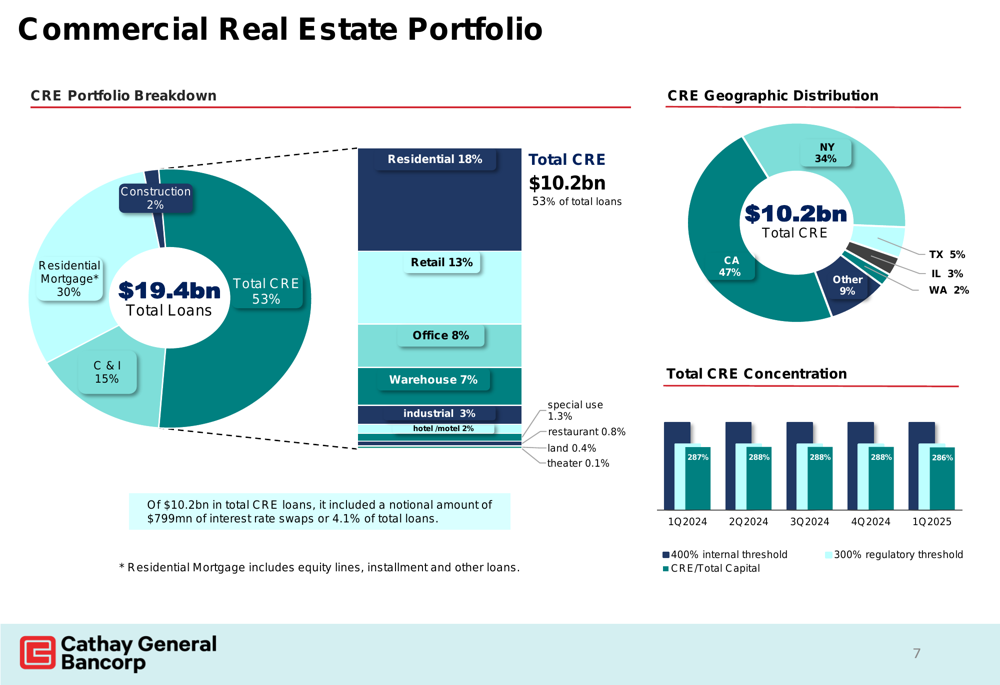

The bank continues to closely monitor its commercial real estate exposure, particularly in potentially higher-risk segments. Cathay’s CRE portfolio is geographically concentrated in California (47%) and New York (34%), with an average loan-to-value ratio of 49%, indicating a conservative approach to lending.

The presentation provided detailed insights into the CRE portfolio’s composition:

Office properties, which have faced challenges in many markets, represent only 8% of Cathay’s total loan portfolio. Importantly, only 3% of these office loans are in central business districts, which have experienced higher vacancy rates nationwide.

Deposit Structure and Funding

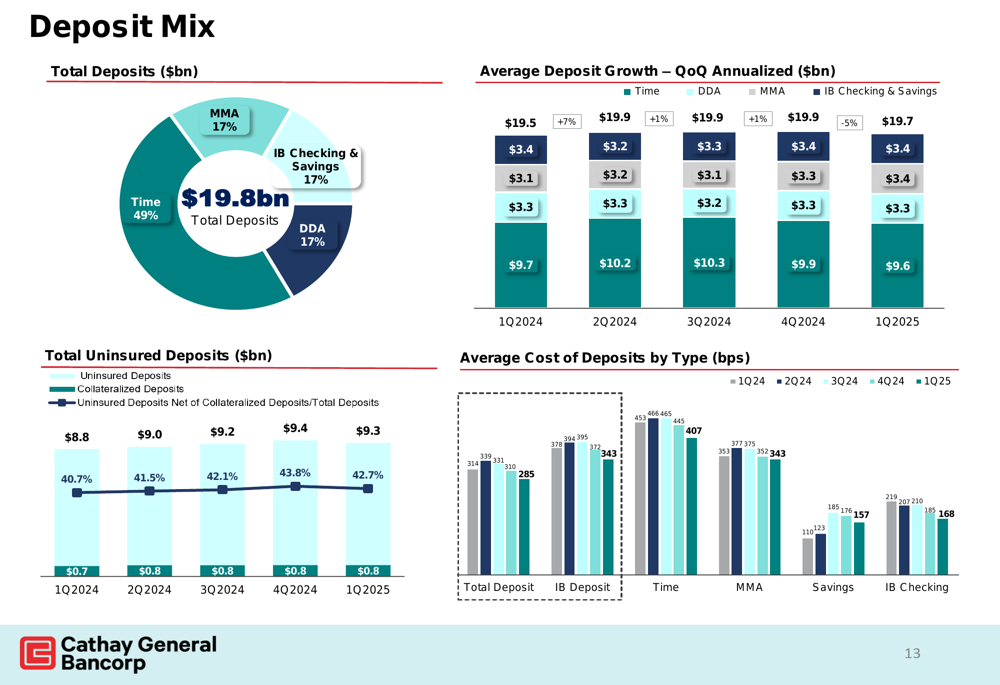

Cathay’s deposit base totaled $19.8 billion as of March 31, 2025, with time deposits comprising 49% of the total. The bank’s deposit mix also includes money market accounts (17%), interest-bearing checking and savings (17%), and demand deposits (17%).

The following chart illustrates this deposit composition:

The bank’s loan-to-deposit ratio remained stable at 97%, indicating a balanced approach to lending relative to its deposit funding. Cathay’s focus on maintaining a diverse deposit base helps support stable funding costs, which will be particularly important as interest rates continue to evolve.

Interest Rate Environment and Margin

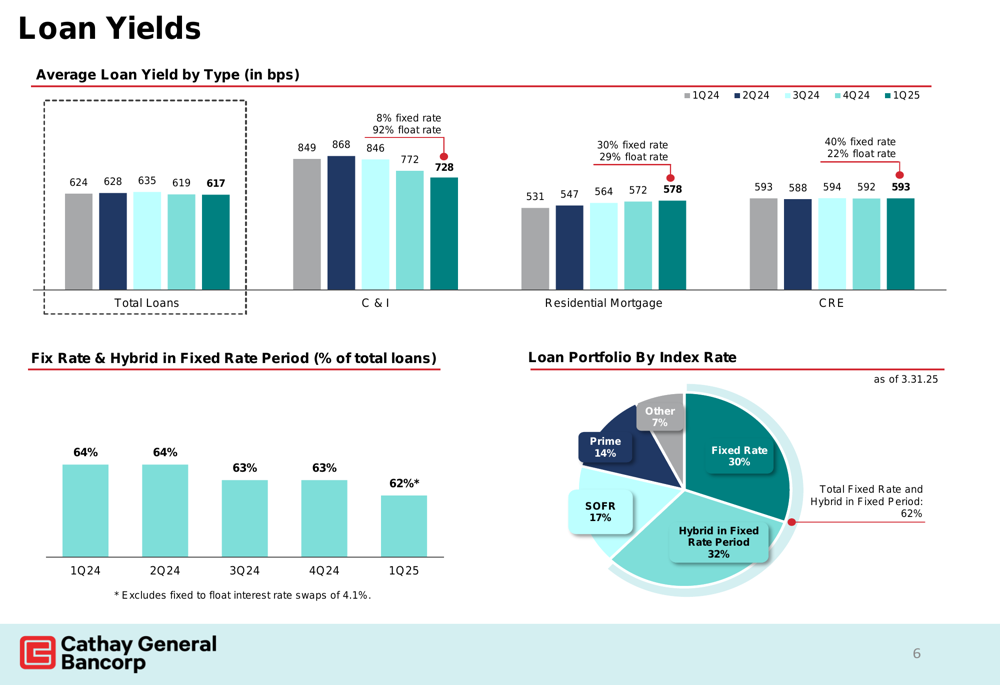

Cathay’s net interest margin appears to be benefiting from the changing interest rate environment. The bank’s loan portfolio includes 62% fixed-rate and hybrid loans, which helps maintain yield stability as market rates fluctuate.

The following chart shows the composition of the loan portfolio by interest rate type:

The presentation also provided insights into how loan yields, deposit costs, and net interest income are responding to changes in benchmark rates:

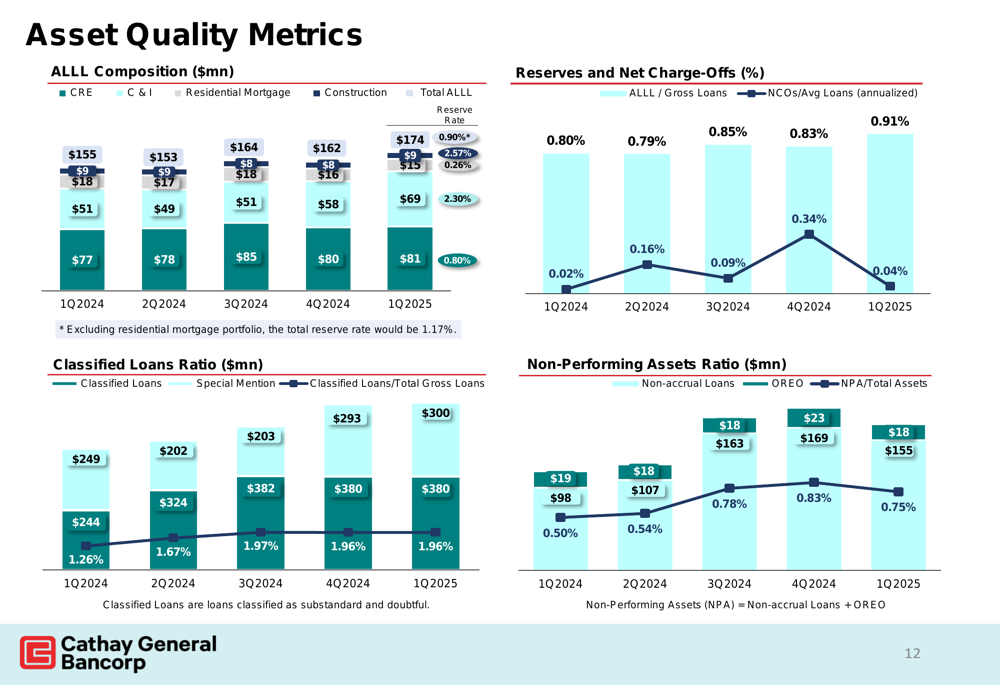

Asset Quality

The bank reported increased attention to asset quality metrics, with allowance for credit losses rising to $175 million from $162 million in the previous quarter. This conservative approach to potential credit issues reflects prudent risk management in an uncertain economic environment.

The following chart details key asset quality metrics:

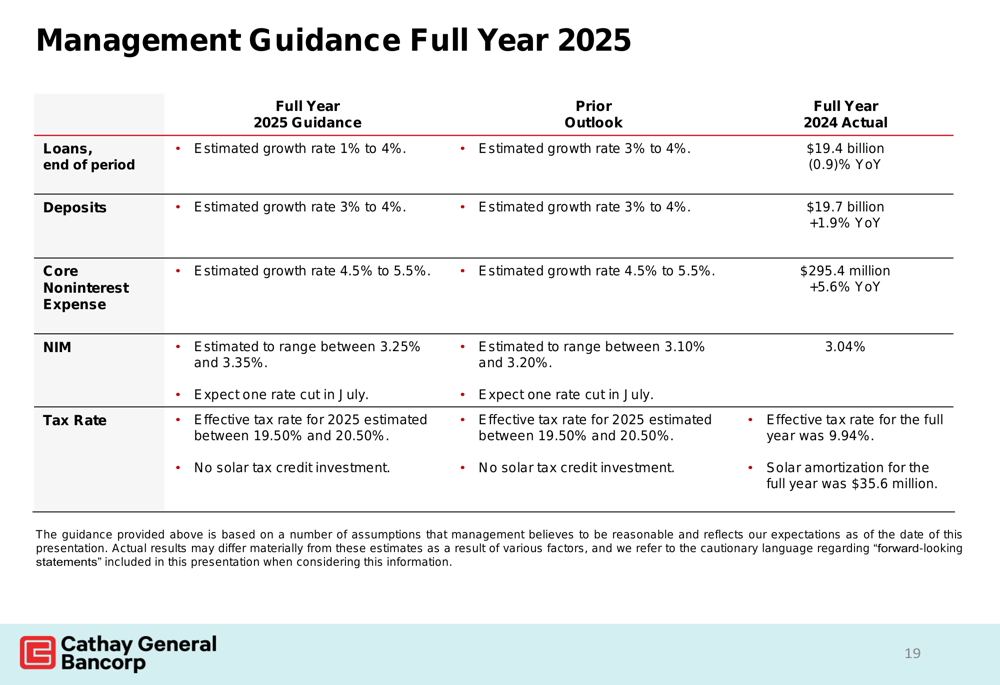

Forward Guidance and Outlook

Management provided guidance for the full year 2025, outlining expectations for loan growth, deposit growth, net interest margin, and other key metrics. This forward-looking information gives investors insight into how the bank plans to navigate the evolving economic landscape.

Conclusion

Cathay General Bancorp’s Q1 2025 financial results reflect both challenges and opportunities in the current banking environment. While earnings declined compared to previous periods, the bank maintained solid fundamentals, strong capital ratios, and a conservative approach to risk management. The positive stock market reaction suggests investors may be focusing on these strengths rather than the short-term earnings pressure.

As interest rates continue to evolve, Cathay’s substantial fixed-rate loan portfolio and diversified funding sources position it to potentially benefit from the changing rate environment. The bank’s detailed disclosures around commercial real estate exposure also demonstrate transparency in addressing one of the key concerns for regional banks in the current market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.