Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

CAVA Group Inc (NYSE:CAVA) released its first quarter 2025 earnings presentation on May 15, highlighting continued strong growth for the Mediterranean fast-casual restaurant chain. Despite reporting impressive financial results and raising its full-year guidance, CAVA’s stock fell 5.12% in after-hours trading to $93.99, following a modest 0.48% decline during the regular session.

The company’s Q1 results demonstrated sustained momentum in both revenue growth and restaurant expansion, building on the strong performance reported in the previous quarter. CAVA has maintained its aggressive growth strategy, focusing on new restaurant openings while delivering double-digit same-restaurant sales growth.

Quarterly Performance Highlights

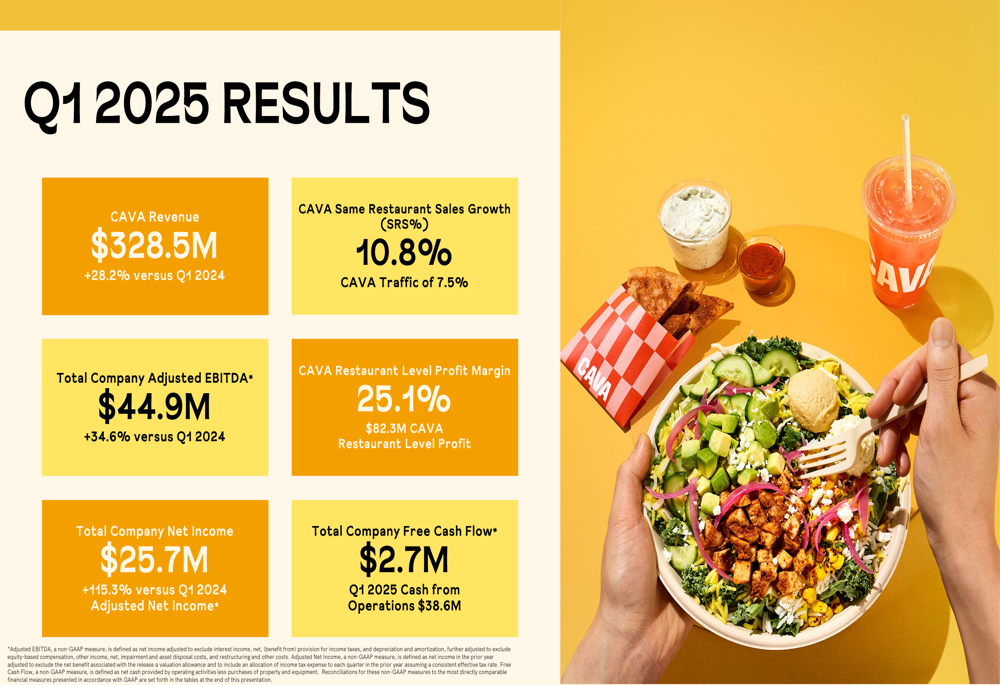

CAVA reported total revenue of $328.5 million for Q1 2025, representing a 28.2% increase compared to the same period in 2024. This growth was driven by both new restaurant openings and robust same-restaurant sales performance.

As shown in the following quarterly performance chart:

Same-restaurant sales grew 10.8% year-over-year, with traffic growth contributing 7.5% of that increase. This marks the fifth consecutive quarter of positive same-restaurant sales growth, though the pace has moderated from the 21.2% reported in Q4 2024.

The company’s profitability metrics also showed improvement, with total company Adjusted EBITDA reaching $44.9 million, up 34.6% compared to Q1 2024. Net income more than doubled, rising 115.3% to $25.7 million. Restaurant-level profit margin remained strong at 25.1%, generating $82.3 million in restaurant-level profit.

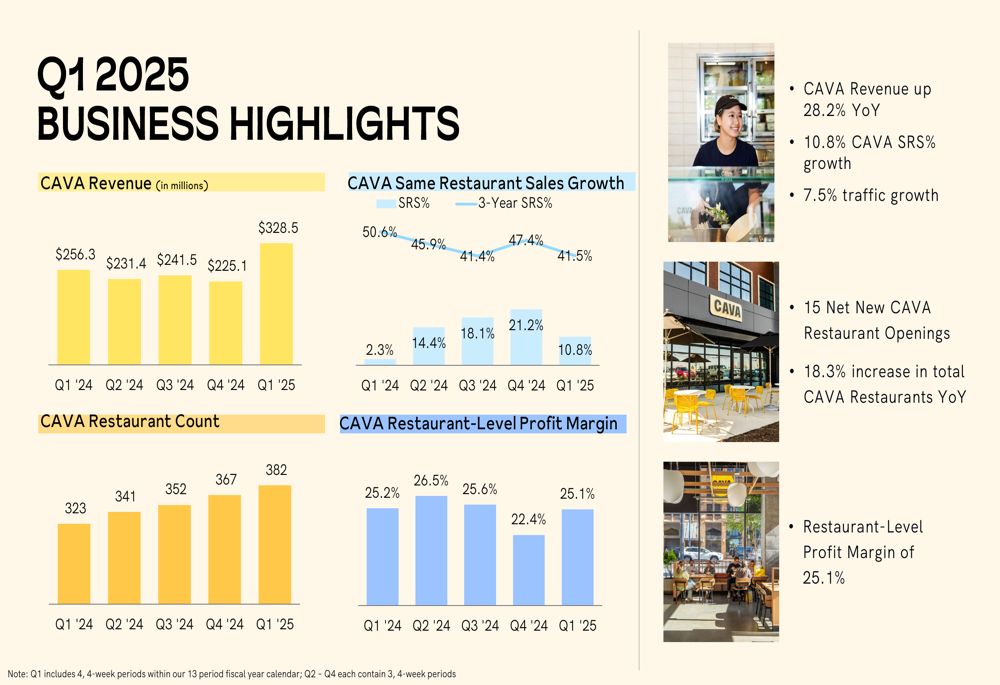

The following business highlights chart illustrates CAVA’s consistent growth trajectory across key metrics:

CAVA continued its expansion efforts, opening 15 net new restaurants during the quarter to reach a total of 382 locations, an 18.3% increase from Q1 2024. The company has maintained a steady opening pace, adding 59 new restaurants over the trailing twelve months.

Strategic Initiatives

The presentation outlined four strategic pillars guiding CAVA’s approach for 2025:

These pillars emphasize geographic expansion, personalized guest relationships, operational excellence, and team performance. The company’s focus on these areas appears to be yielding results, as evidenced by the strong traffic growth and consistent restaurant-level margins.

CAVA also highlighted its product innovation efforts, including the recent launch of its "Spice World" campaign featuring limited-time offerings. The campaign introduces Hot Harissa Pita Chips and a Steak + Harissa Bowl, aimed at driving guest engagement and traffic during the summer months.

As shown in the following product launch slide:

The company continues to leverage seasonal offerings and limited-time products to maintain customer interest and drive traffic to its restaurants. These initiatives, combined with CAVA’s focus on digital engagement and personalization, appear to be resonating with customers based on the quoted guest reactions.

Forward-Looking Statements

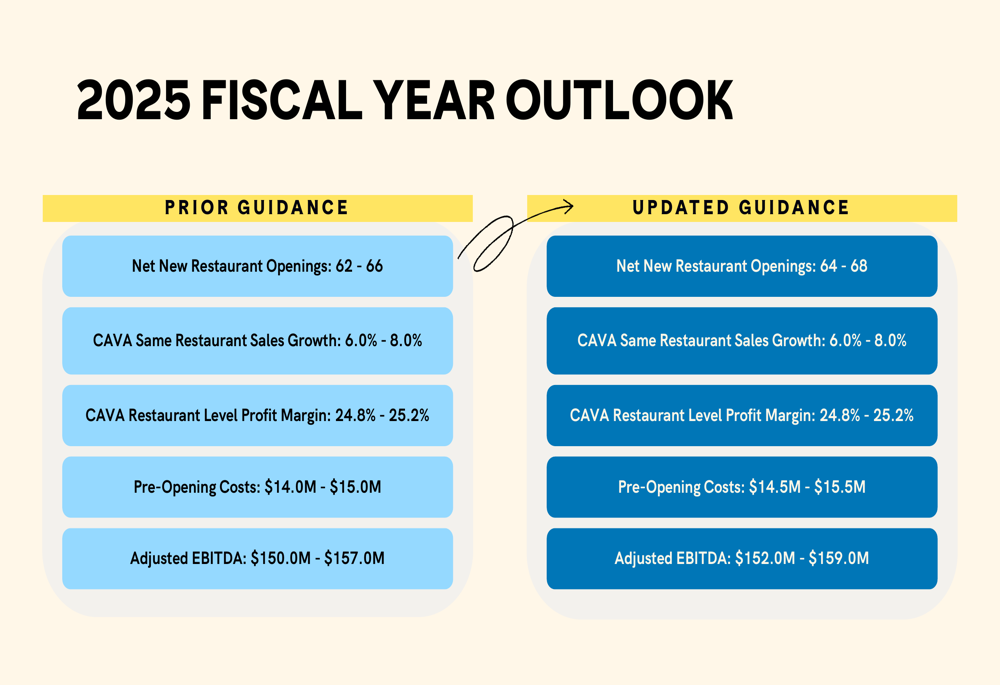

CAVA slightly raised its fiscal year 2025 guidance, reflecting confidence in its growth trajectory despite the moderation in same-restaurant sales growth. The updated outlook includes:

The company now expects to open 64-68 net new restaurants in 2025, up from the previous guidance of 62-66. CAVA maintained its same-restaurant sales growth forecast of 6.0%-8.0% and restaurant-level profit margin projection of 24.8%-25.2%.

Adjusted EBITDA guidance was increased to $152.0-$159.0 million, up from the previous range of $150.0-$157.0 million, reflecting the company’s confidence in its ability to maintain profitability while investing in growth.

Market Reaction

Despite the positive results and raised guidance, CAVA’s stock declined in after-hours trading. This reaction may reflect elevated investor expectations following the stock’s strong performance over the past year, with shares trading significantly above their 52-week low of $70.

The company’s fundamentals remain strong, with consistent revenue growth, healthy restaurant-level margins, and a clear expansion strategy. However, the deceleration in same-restaurant sales growth from 21.2% in Q4 2024 to 10.8% in Q1 2025 may have raised concerns about the sustainability of CAVA’s growth trajectory.

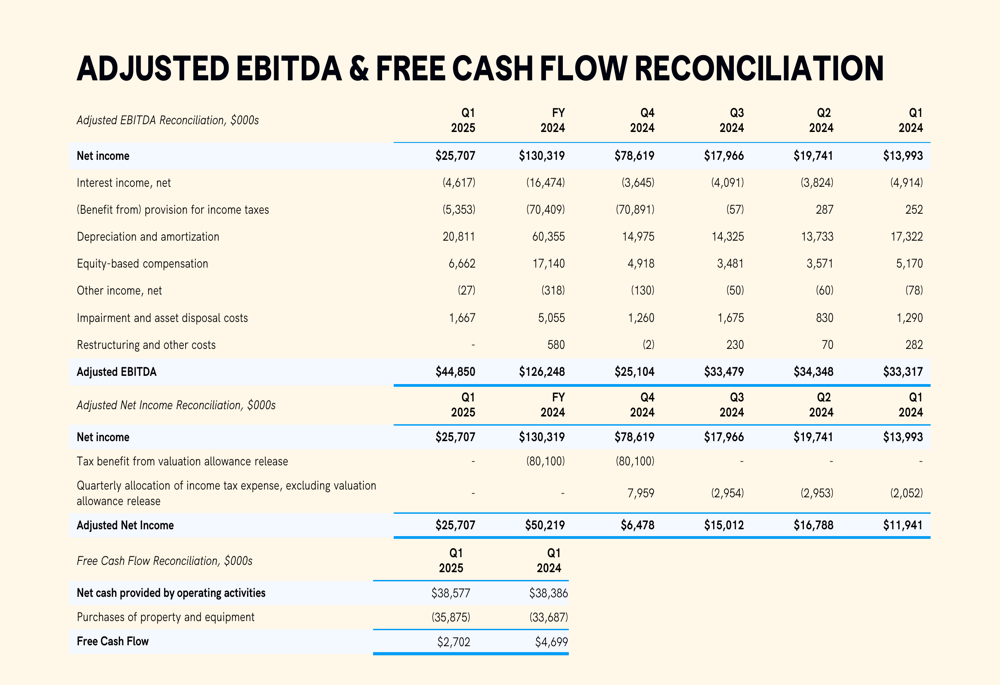

CAVA’s detailed financial reconciliation provides additional context for its performance metrics:

The reconciliation highlights the components of CAVA’s adjusted EBITDA and free cash flow calculations, providing transparency into the company’s financial reporting practices.

As CAVA continues its expansion efforts, investors will likely focus on the company’s ability to maintain strong same-restaurant sales growth while successfully opening new locations. The updated guidance suggests management remains confident in CAVA’s growth prospects for the remainder of fiscal year 2025, despite the mixed market reaction to the Q1 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.