Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Cellnex Telecom SA (BME:CLNX) reported solid H1 2025 results on August 1, highlighting organic revenue growth of 6.0% despite challenging market conditions. The European telecom infrastructure leader’s shares have faced pressure recently, with the stock declining 2.88% in the latest trading session to €27.34, continuing a downward trend seen after the earnings announcement.

The company’s performance demonstrates resilience in its business model, which focuses on long-term infrastructure agreements with major telecommunications operators across Europe. While reported revenue growth was more modest at 1.1% due to divestments in Ireland and Austria, the underlying organic growth reflects strong demand for Cellnex’s infrastructure services.

Quarterly Performance Highlights

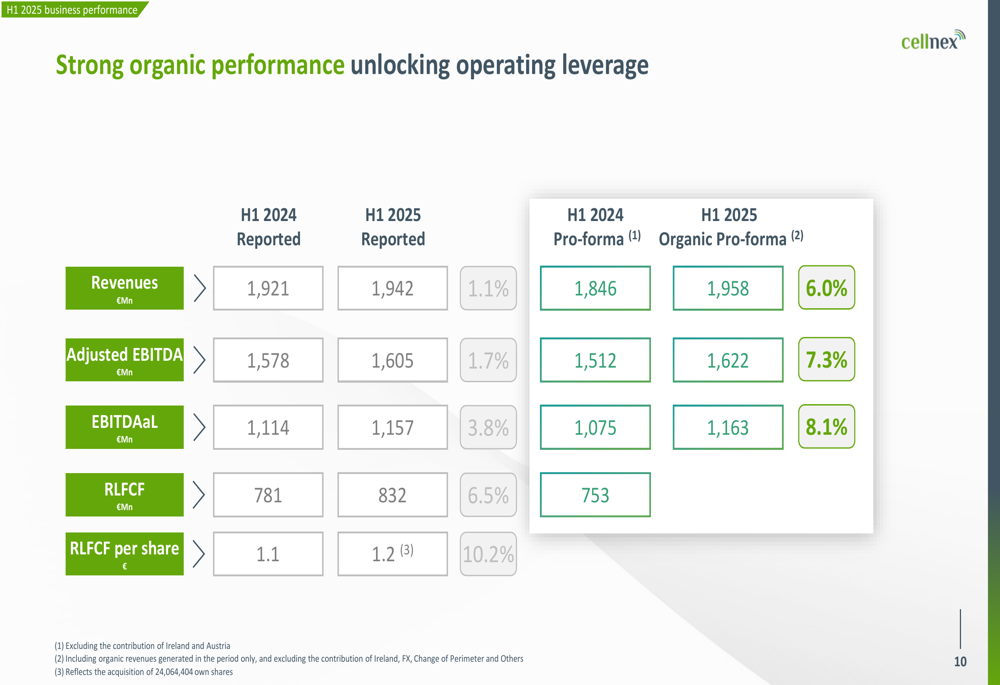

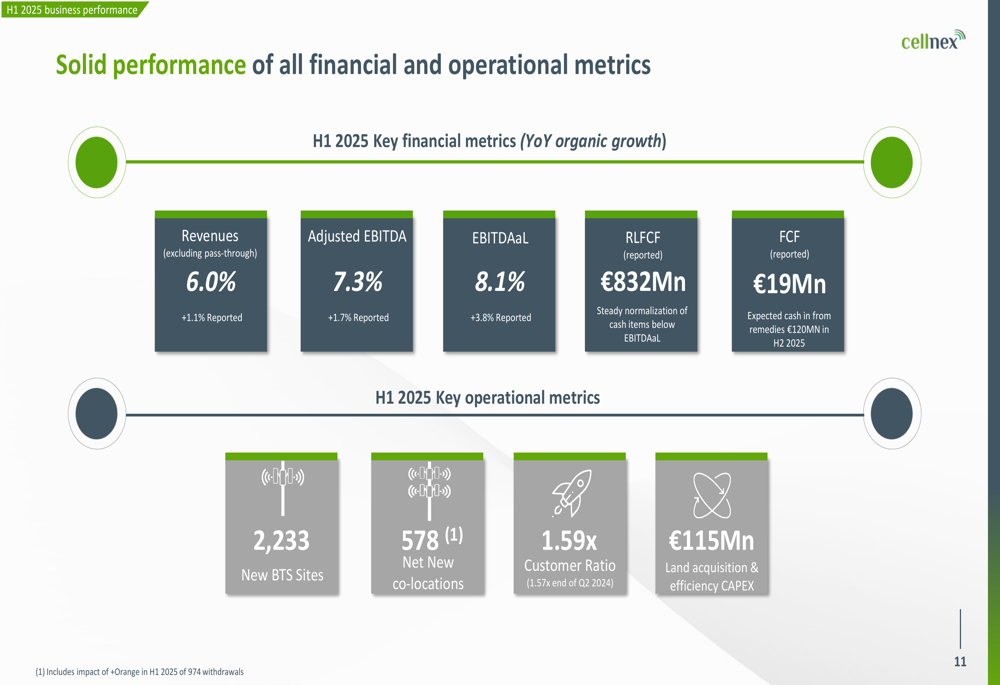

Cellnex delivered robust financial results for the first half of 2025, with revenues excluding pass-through reaching €1,942 million, representing 6.0% organic growth compared to the same period last year. The company’s adjusted EBITDA grew 7.3% on an organic basis to €1,605 million, while EBITDA after leases (EBITDAaL) increased 8.1% to €1,157 million.

As shown in the following financial results comparison:

Recurring levered free cash flow (RLFCF) showed particularly strong improvement, increasing 6.5% to €832 million, with RLFCF per share growing 10.2% to €1.2. This cash flow performance underscores the company’s ability to generate consistent returns from its infrastructure assets.

Operational metrics also demonstrated positive momentum, with the addition of 2,233 new build-to-suit sites and 578 net new co-locations during the period. The company’s customer ratio improved to 1.59x, reflecting Cellnex’s success in attracting multiple tenants to its infrastructure.

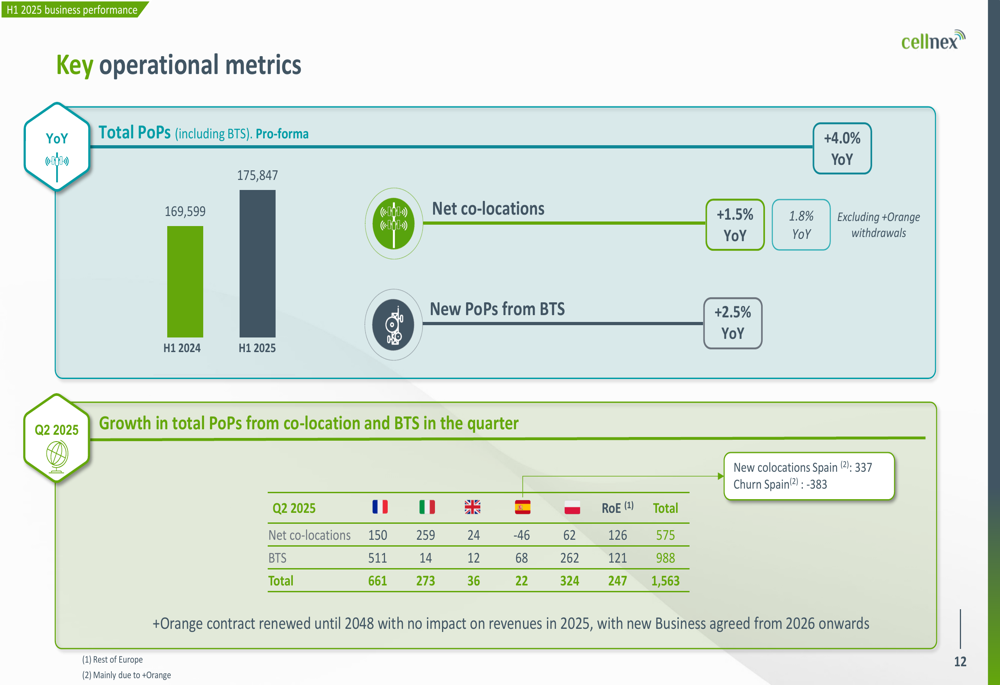

Total points of presence (PoPs) increased 4.0% year-over-year to 175,847, with growth coming from both co-locations (+1.5%) and new PoPs from build-to-suit arrangements (+2.5%). This expansion of the company’s infrastructure footprint provides a foundation for future revenue growth.

Strategic Initiatives

Cellnex made significant progress on strategic initiatives during H1 2025, reinforcing its long-term business stability. A key development was the renewal of its agreement with Odido in the Netherlands, extending their collaboration for an additional 15 years with CPI-linked terms that maintain revenue levels.

The company also strengthened its relationship with Telefónica, supporting the deployment of 110 additional physical PoPs and enabling the activation of up to 3,000 RAN Sharing DIGI PoPs over the next eight years. These contract renewals and expansions demonstrate Cellnex’s position as a preferred infrastructure partner for major telecommunications operators.

Cellnex completed a share buyback program during the period, acquiring 24,064,404 shares (3.41% of share capital) at an average price of €33.24, representing approximately €800 million. This capital allocation decision reflects management’s confidence in the company’s valuation and commitment to shareholder returns.

The company’s financial position was further strengthened by the issuance of a €750 million bond with a 7-year term and 3.5% coupon, along with the refinancing of a €2,800 million syndicated credit facility. These actions, combined with S&P’s decision to upgrade Cellnex’s rating outlook from stable to positive (maintaining BBB- rating), highlight the company’s improved financial profile.

Detailed Financial Analysis

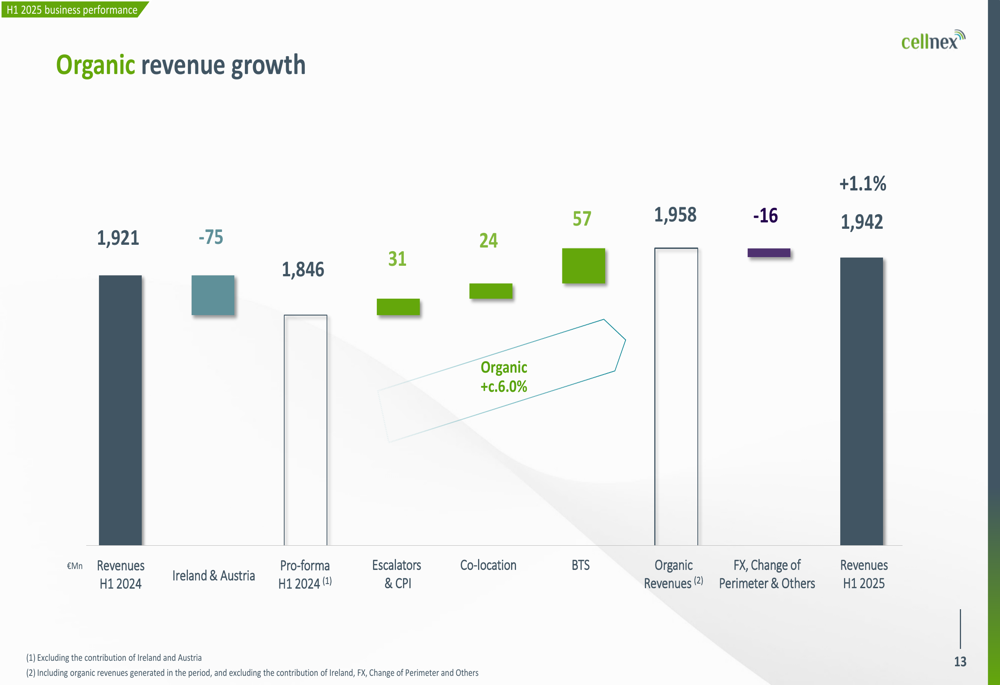

Breaking down Cellnex’s organic revenue growth reveals the diverse drivers of the company’s performance. As illustrated in the following waterfall chart, the 6.0% organic growth was primarily driven by build-to-suit sites (+€57 million), escalators and CPI adjustments (+€31 million), and co-location revenues (+€24 million):

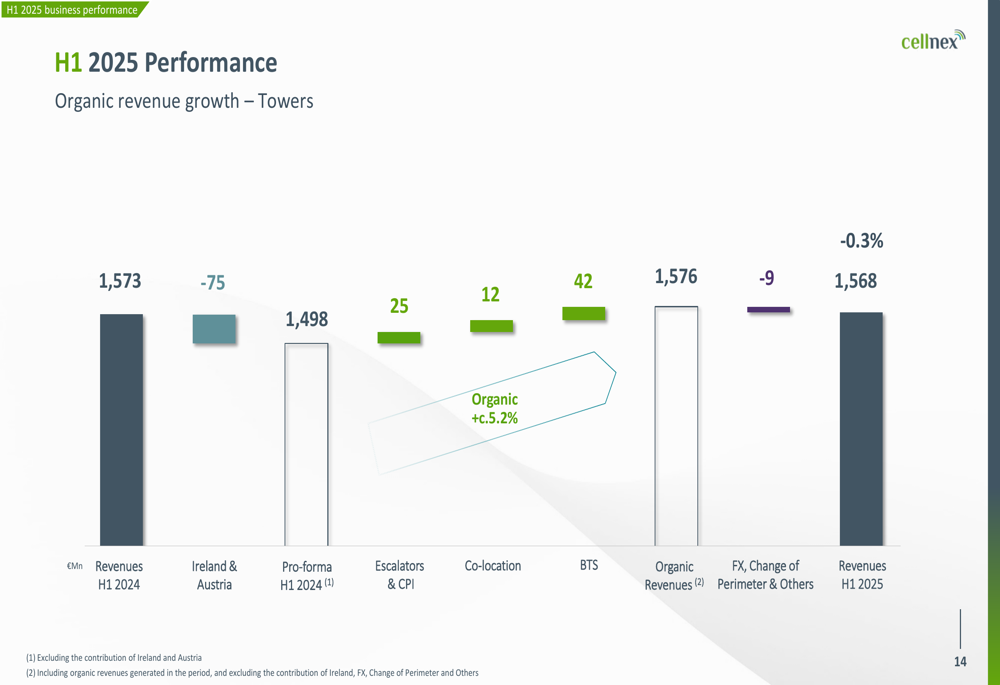

Tower business, which represents the core of Cellnex’s operations, showed strong organic growth of 5.2%, though reported revenues declined slightly by 0.3% to €1,568 million due to divestments:

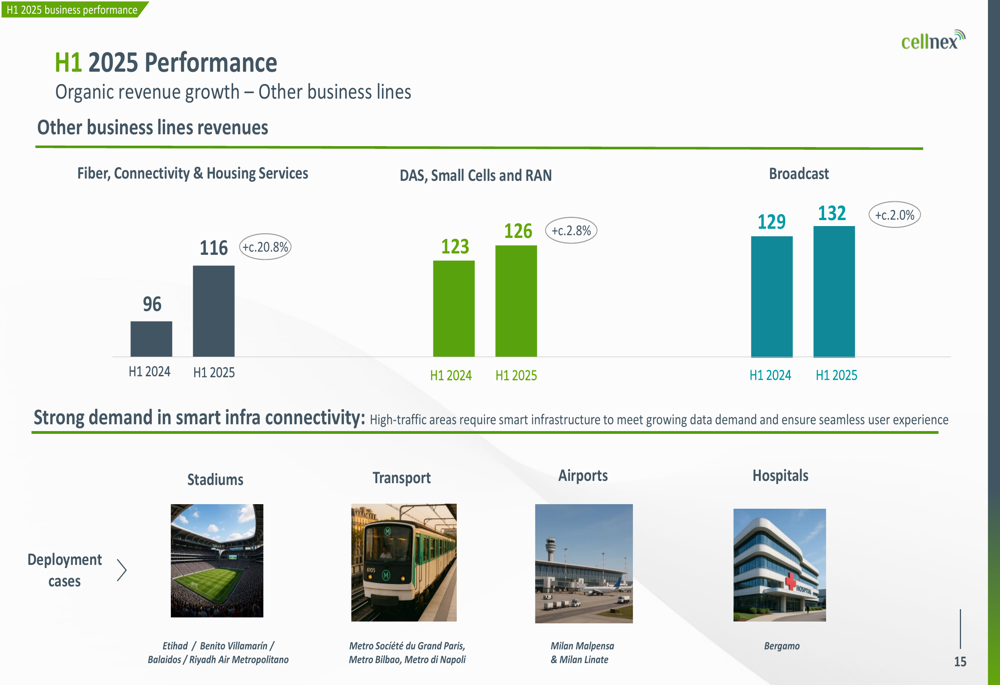

Non-tower business lines demonstrated impressive growth, particularly in Fiber, Connectivity & Housing Services, which increased 20.8% to €116 million. DAS, Small Cells, and RAN grew 2.8% to €126 million, while Broadcast revenues increased 2.0% to €132 million:

Cellnex continued to improve operational efficiency, with reductions in staff, repair and maintenance, SG&A, and lease costs on a per-tower basis. These improvements contributed to the strong EBITDA and cash flow performance:

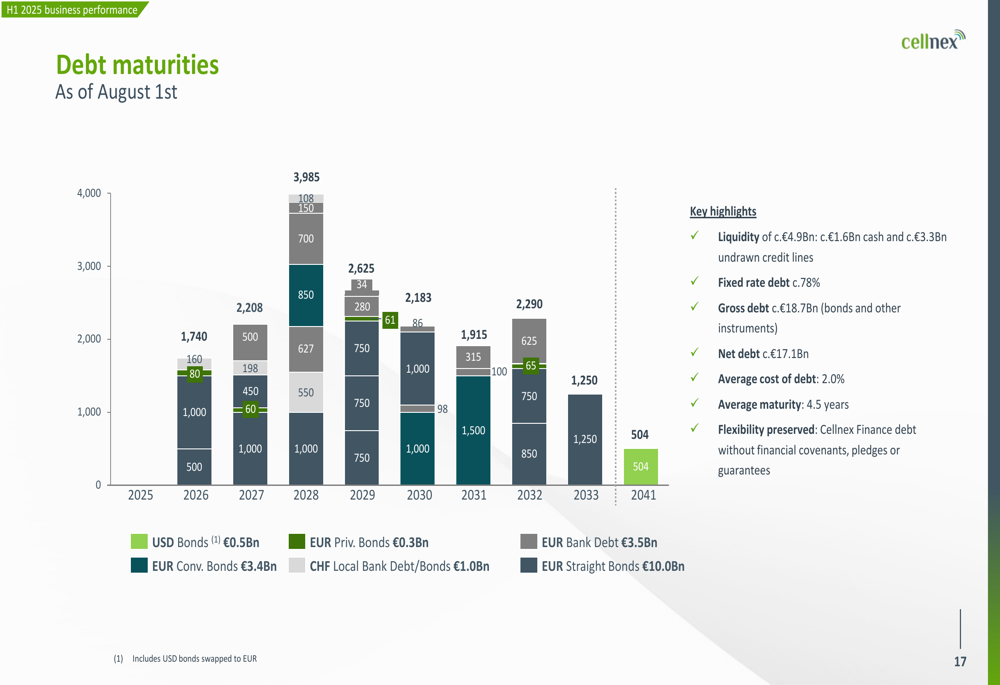

The company maintained a solid financial position with liquidity of approximately €4.9 billion and an average cost of debt of 2.0% with an average maturity of 4.5 years. The debt maturity profile shows a well-distributed schedule, providing financial flexibility:

ESG Achievements

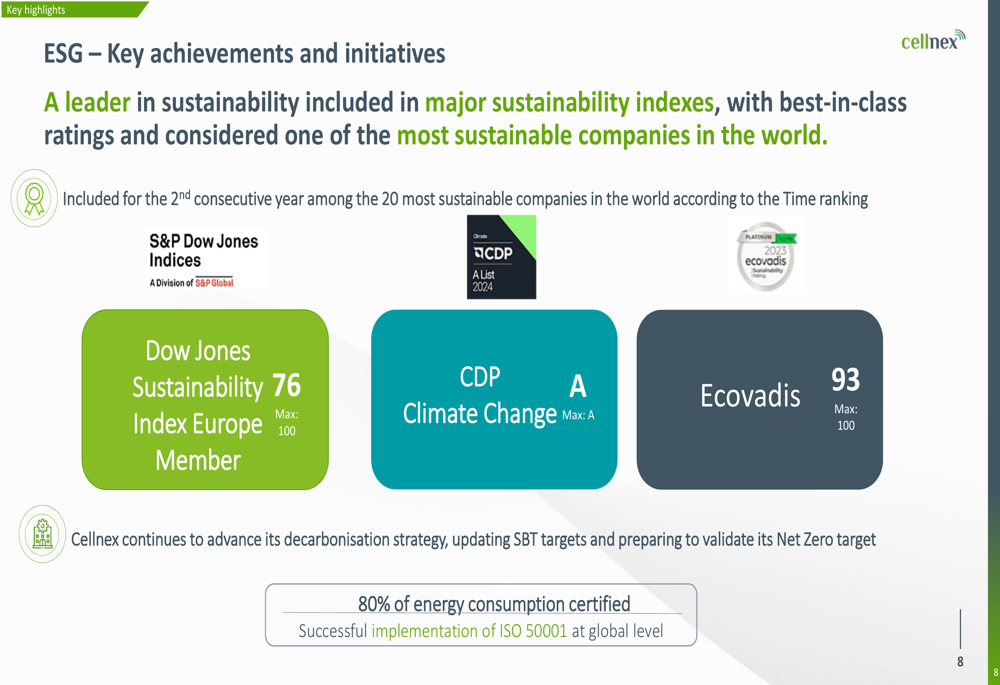

Cellnex continues to demonstrate leadership in sustainability, being included for the second consecutive year among the 20 most sustainable companies in the world according to Time magazine. The company achieved high scores across major sustainability indices, including a CDP Climate Change score of A and an EcoVadis Platinum rating with a score of 93/100.

The company has certified 80% of its energy consumption and successfully implemented ISO 50001 at a global level, reflecting its commitment to environmental responsibility:

Forward-Looking Statements

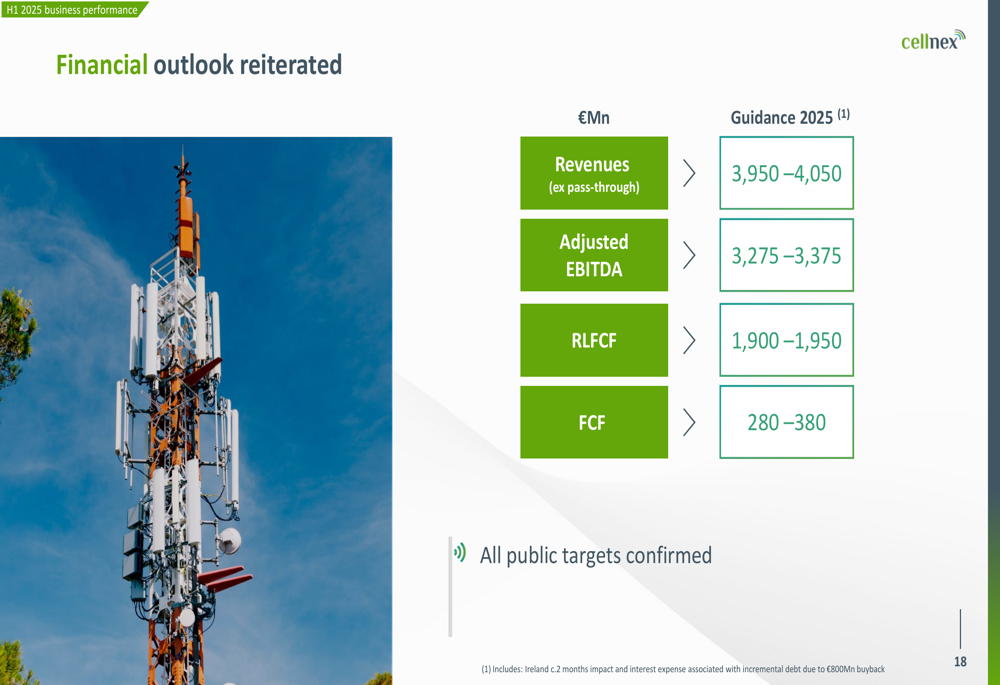

Cellnex reiterated its financial outlook for 2025, maintaining guidance for revenues (excluding pass-through) of €3,950-4,050 million, adjusted EBITDA of €3,275-3,375 million, RLFCF of €1,900-1,950 million, and FCF of €280-380 million:

The company’s business model continues to be underpinned by solid fundamentals, including long-term contracts with major telecommunications operators, limited churn, and inflation protection through CPI and escalator clauses. With a backlog of more than €100 billion, Cellnex has strong visibility on future cash flows.

While potential market consolidation in France could impact the competitive landscape, Cellnex’s management believes the company is well-positioned to navigate these changes, with limited exposure to consolidation scenarios and potential upside opportunities. The company’s focus on operational efficiency and strategic contract renewals should support continued organic growth in the second half of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.