Gold prices hold sharp gains as soft US jobs data fuels Fed rate cut bets

CenterPoint Energy (NYSE:CNP) reported a slight decrease in first-quarter earnings while reaffirming its full-year guidance and announcing an increased long-term capital investment plan, according to its Q1 2025 investor presentation released on April 24.

Quarterly Performance Highlights

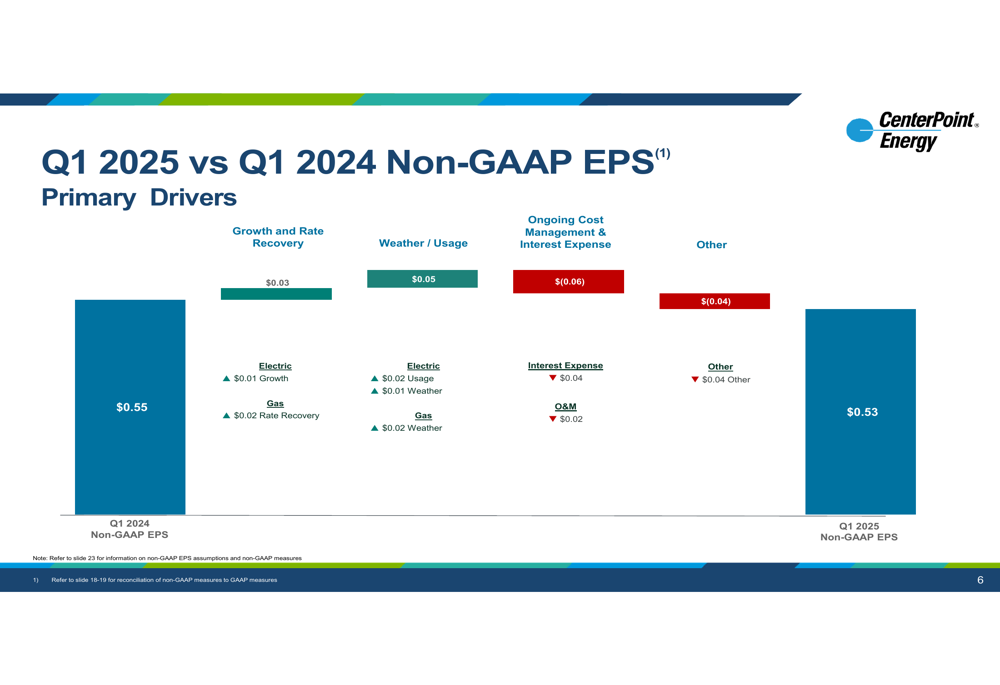

The Houston-based utility reported non-GAAP earnings per share of $0.53 for the first quarter of 2025, down slightly from $0.55 in the same period last year. Despite this modest decline, the company reaffirmed its 2025 non-GAAP EPS guidance target range of $1.74-$1.76.

The primary drivers behind the quarterly EPS change included positive contributions from growth and rate recovery (+$0.03) and favorable weather/usage patterns (+$0.05), which were more than offset by ongoing cost management and interest expense (-$0.06) and other factors (-$0.04).

As shown in the following chart detailing the drivers of quarterly performance:

The company noted that 2025 will have a different earnings profile than typical years due to the timing of recovery of Texas investments post rate cases. While CenterPoint typically sees 50-60% of earnings in the first half of the year, the 2025 profile is expected to be weighted toward the second half, with 50-60% of earnings coming in that period.

Strategic Initiatives

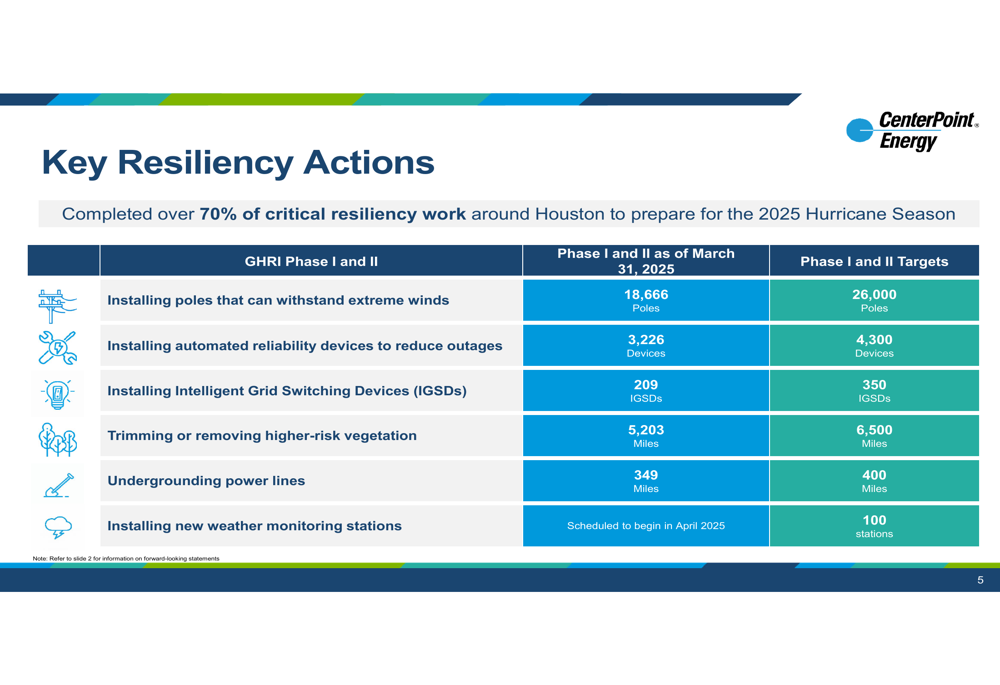

CenterPoint highlighted significant progress on its Greater Houston Resiliency Initiative (GHRI), reporting that over 70% of critical resiliency work is complete around Houston in preparation for the 2025 hurricane season. This includes installing poles that can withstand extreme winds, automated reliability devices, and intelligent grid switching devices, as well as trimming higher-risk vegetation and undergrounding power lines.

The following chart shows the company’s progress on key resiliency actions:

Looking forward, CenterPoint plans to invest approximately $5.5 billion from 2026 through 2028 to improve customer experience through accelerated and increased investment in system resiliency. This investment is expected to strengthen overall resiliency by 30%, reduce outages by 1.3 billion minutes, and save approximately $50 million per year.

The company’s system resiliency plan includes multiple components as illustrated here:

Capital Investment Plans

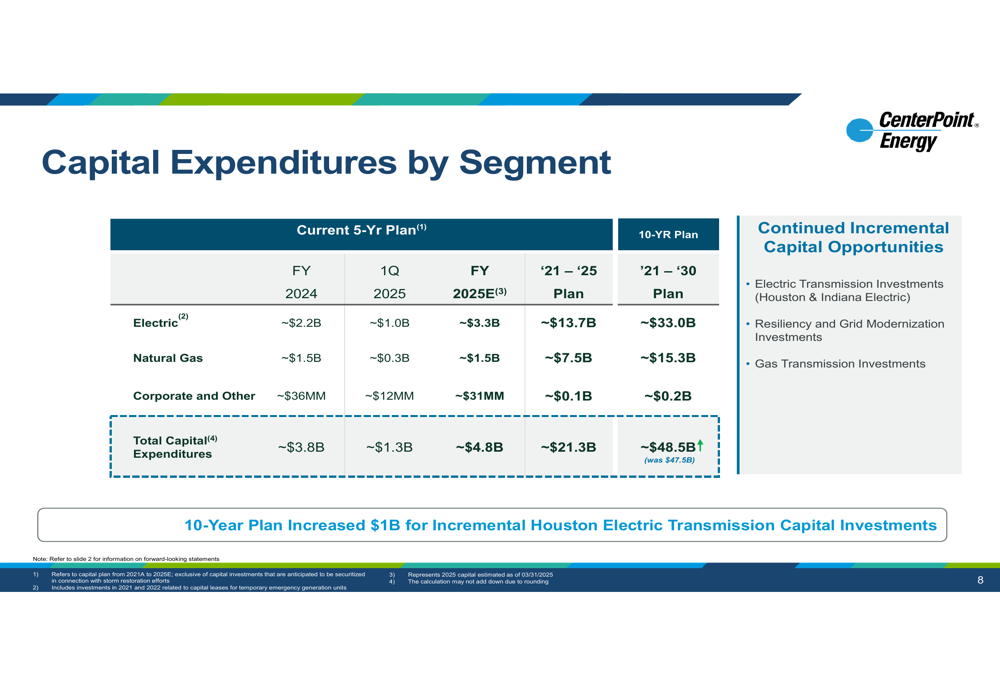

In a significant update, CenterPoint increased its 10-year capital investment plan by $1 billion for incremental Houston Electric Transmission investments, bringing the total to approximately $48.5 billion across all segments through 2030.

For the current year, the company plans to invest approximately $4.8 billion in capital expenditures for FY 2025, with the electric segment accounting for about $3.3 billion and natural gas for approximately $1.5 billion.

The detailed breakdown of capital expenditures by segment is shown in the following table:

CenterPoint emphasized that over 80% of its 10-year capital plan is expected to be recoverable through interim regulatory mechanisms, which should allow for timely recovery of investments and storm costs.

Regulatory Environment

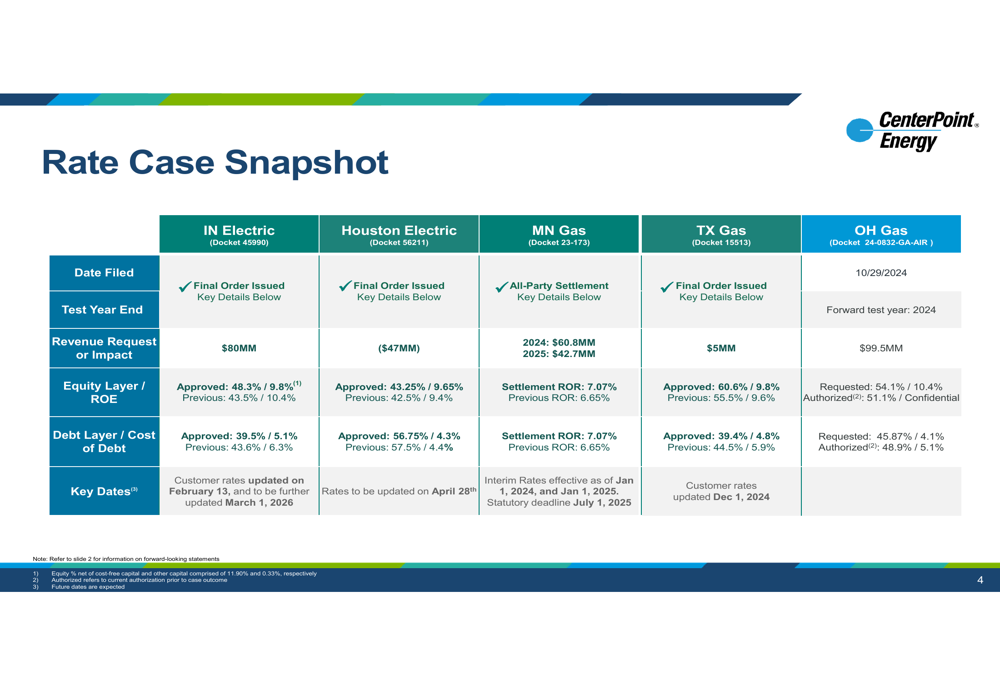

The company provided a comprehensive snapshot of its rate cases across different jurisdictions, including Indiana Electric, Houston Electric, Minnesota Gas, Texas Gas, and Ohio Gas. Notable outcomes include an approved ROE of 9.8% with an equity layer of 48.3% for Indiana Electric and a rate decrease of $47 million with an equity layer of 43.25% and ROE of 9.65% for Houston Electric.

The following table details the company’s rate case status across jurisdictions:

CenterPoint also highlighted its regulatory schedule, which outlines upcoming regulatory proceedings and timelines for its various gas and electric entities. This regulatory visibility provides a clearer picture of potential recovery timelines for the company’s significant capital investments.

Growth Drivers and Financial Strength

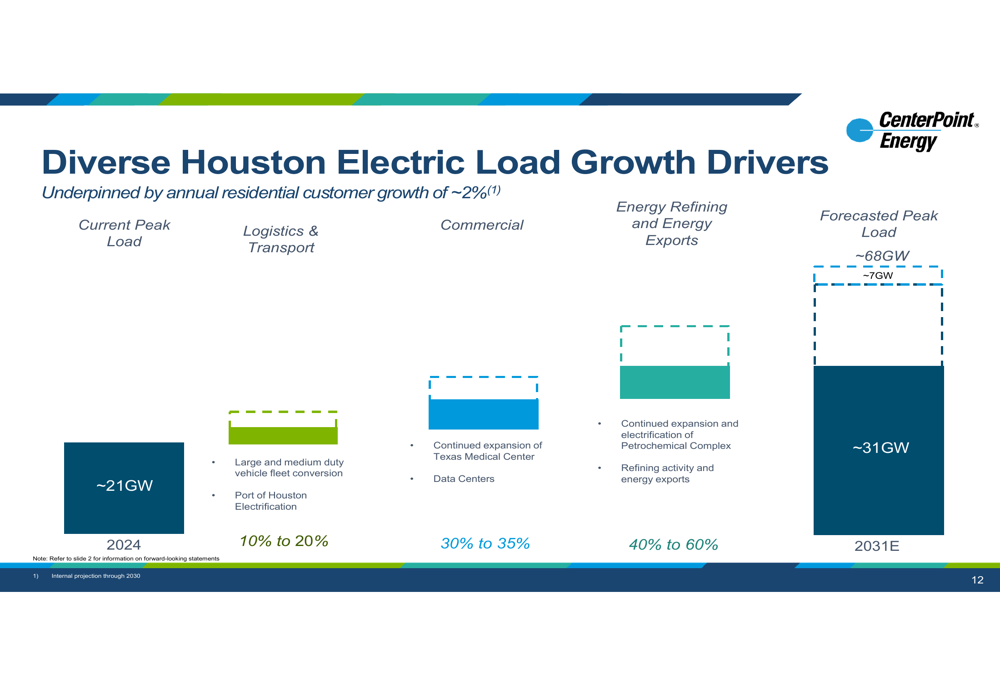

The company identified diverse drivers of electric load growth in Houston, underpinned by annual residential customer growth of approximately 2%. By 2031, CenterPoint forecasts its peak load to reach approximately 68GW, up from the current 21GW, with growth coming from logistics and transport (10-20%), commercial development (30-35%), and energy refining and exports (40-60%).

This growth outlook is illustrated in the following chart:

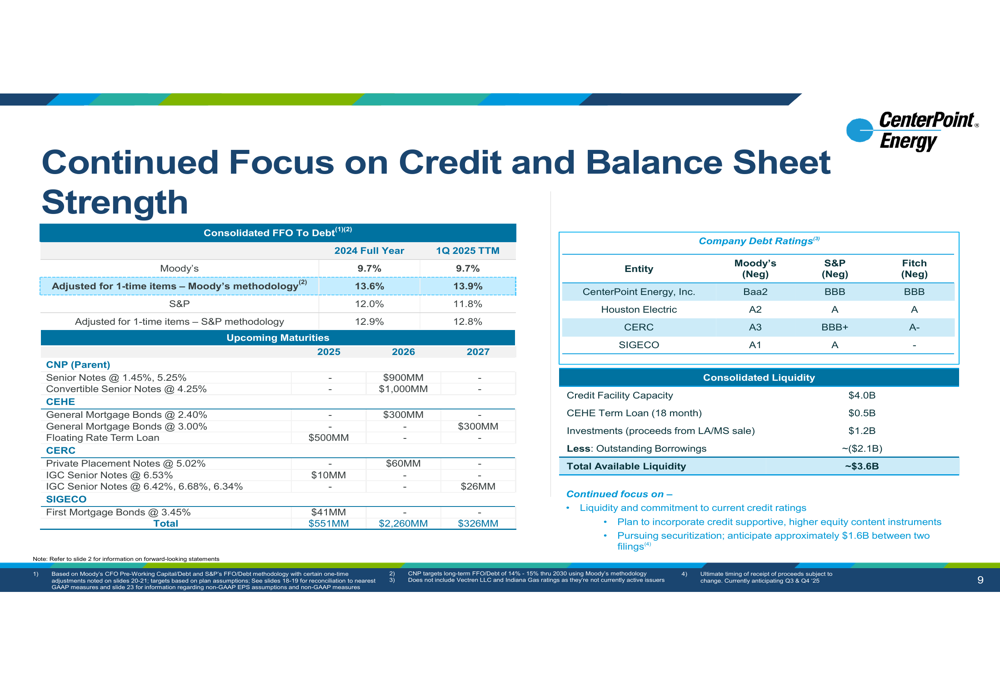

On the financial front, CenterPoint reported a trailing twelve-month FFO to Debt ratio of 13.9% for Q1 2025 (based on Moody’s methodology), showing a slight improvement from 13.6% for full-year 2024. The company highlighted its strong liquidity position, with approximately $3.6 billion in available liquidity, including $4.0 billion in credit capacity and $1.2 billion from the recently completed sale of its Louisiana and Mississippi LDCs.

The following slide details the company’s credit and balance sheet metrics:

Forward-Looking Statements

CenterPoint reaffirmed its long-term strategic objectives, which include targeting top quartile non-GAAP EPS annual growth of 8% in 2025 and 6-8% annually through 2030. The company also aims to maintain balance sheet health with a long-term FFO/Debt target of 14%-15% through 2030.

Funding for its ambitious capital investment plan will come from multiple sources, including asset recycling gross proceeds of nearly $3 billion in 2025 and beyond, as well as $2.75 billion in equity or equity-like proceeds through 2030.

In conclusion, while CenterPoint Energy experienced a slight dip in quarterly earnings, the company’s reaffirmed guidance, increased capital investment plan, and progress on strategic initiatives suggest confidence in its long-term growth trajectory. The focus on grid resiliency and modernization, particularly in the Houston area, positions the company to meet growing demand while improving service reliability for customers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.