TSX runs higher on rate cut expectations

Introduction & Market Context

Champion Iron Ltd (ASX:CIA) released its fourth quarter and full-year 2025 financial results on May 29, 2025, highlighting record quarterly sales despite facing headwinds in the iron ore market. The company’s focus on high-purity iron ore production continues to position it as a key player in the green steel transition.

During the quarter, the P65 iron ore index averaged US$116.9 per tonne, with the premium over the P62 index remaining near recent lows. This pricing environment reflects ongoing market challenges, though Champion benefited from a 9.9% quarter-over-quarter decrease in the C3 freight index, helping to partially offset pricing pressures.

Quarterly Performance Highlights

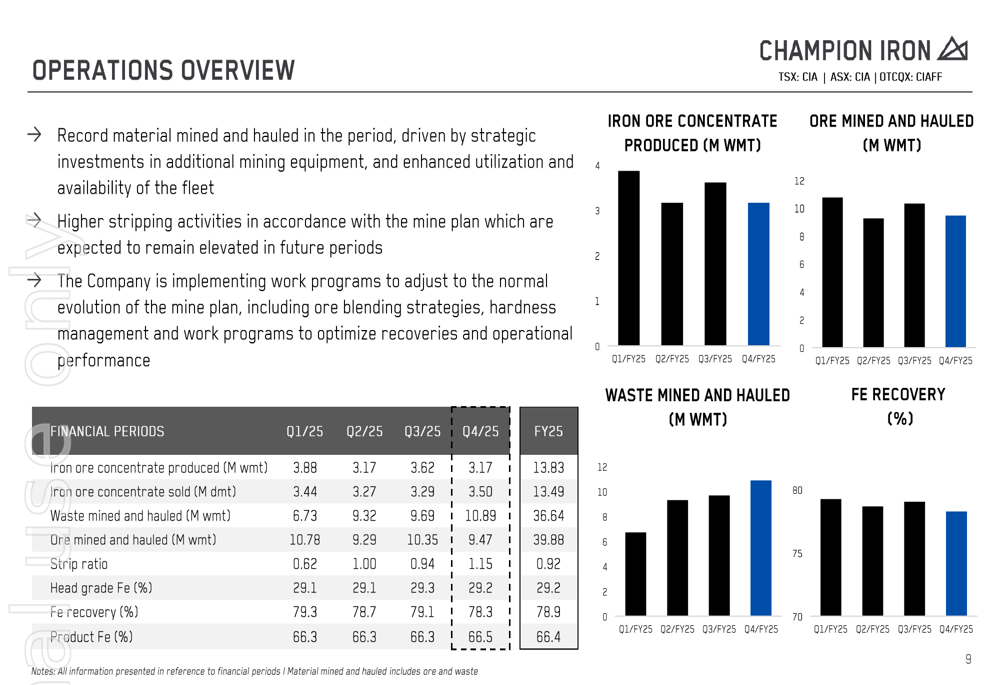

Champion Iron achieved record quarterly sales of 3.5 million dry metric tonnes (dmt) in Q4 FY2025, while producing 3.2 million wet metric tonnes (wmt) of iron ore concentrate. The company reported strong operational metrics, including a 78.3% ore recovery rate.

As shown in the following operational overview, the company implemented work programs to adjust to the normal evolution of its mine plan while maintaining production levels:

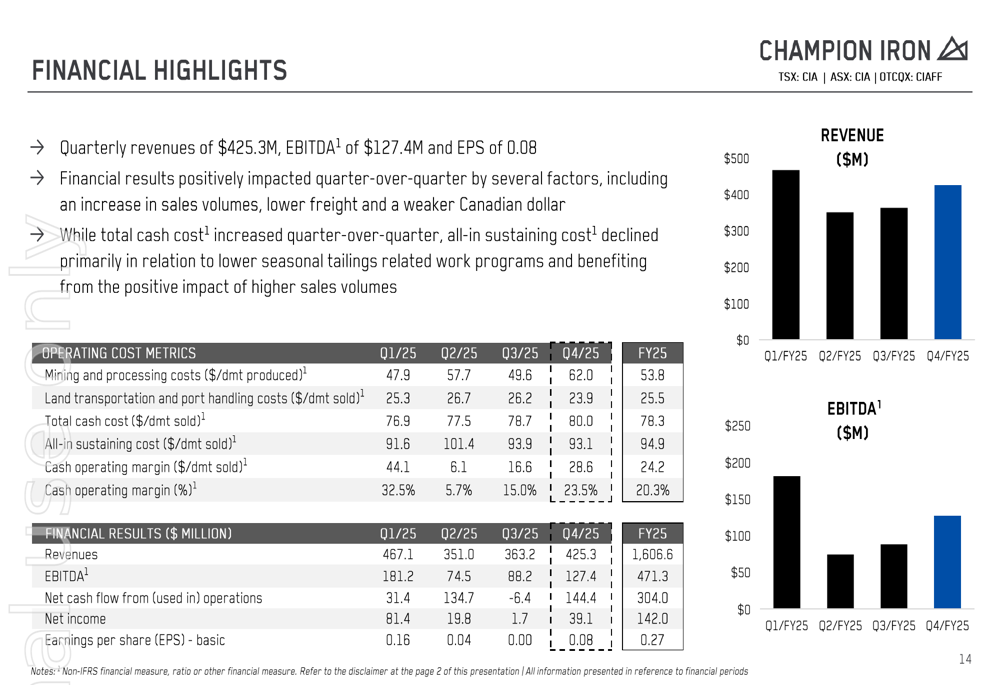

Financial results for the quarter included revenues of $425.3 million, EBITDA of $127.4 million, and net income of $39.1 million, translating to earnings per share of $0.08. The company declared a semi-annual dividend of $0.10 per share, demonstrating confidence in its financial stability despite market fluctuations.

The following chart illustrates key financial metrics across recent quarters:

Financial Analysis

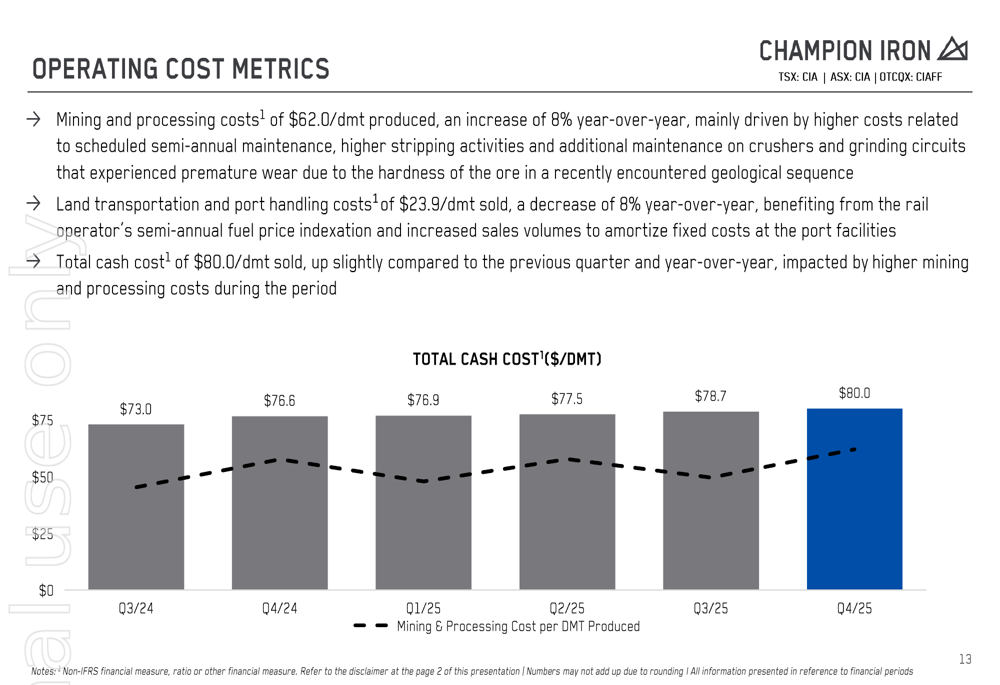

Champion’s total cash cost was $80.0 per dmt sold, with all-in sustaining costs of $93.1 per dmt. Mining and processing costs increased 8% year-over-year to $62.0 per dmt produced, while land transportation and port handling costs decreased 8% to $23.9 per dmt sold.

The company’s cost structure and trends are illustrated in this chart:

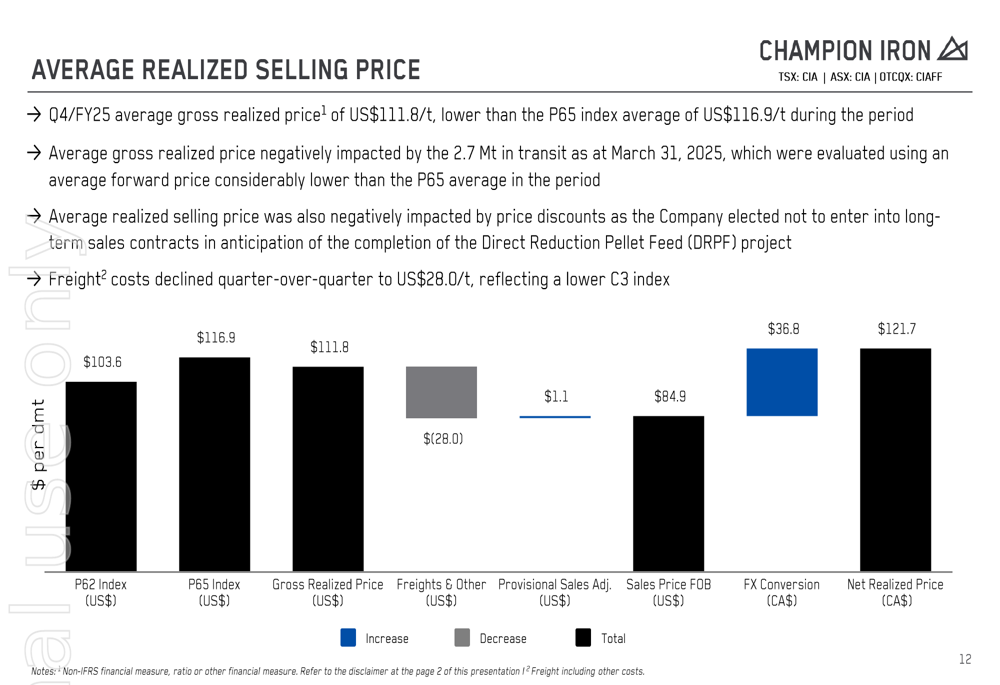

Champion’s realized average selling price was US$111.8 per tonne, below the P65 index average of US$116.9 per tonne. The quarter included a positive provisional pricing adjustment of US$3.7 million, representing a US$1.1 per dmt positive impact on the average realized price.

The following diagram breaks down the company’s average realized selling price components:

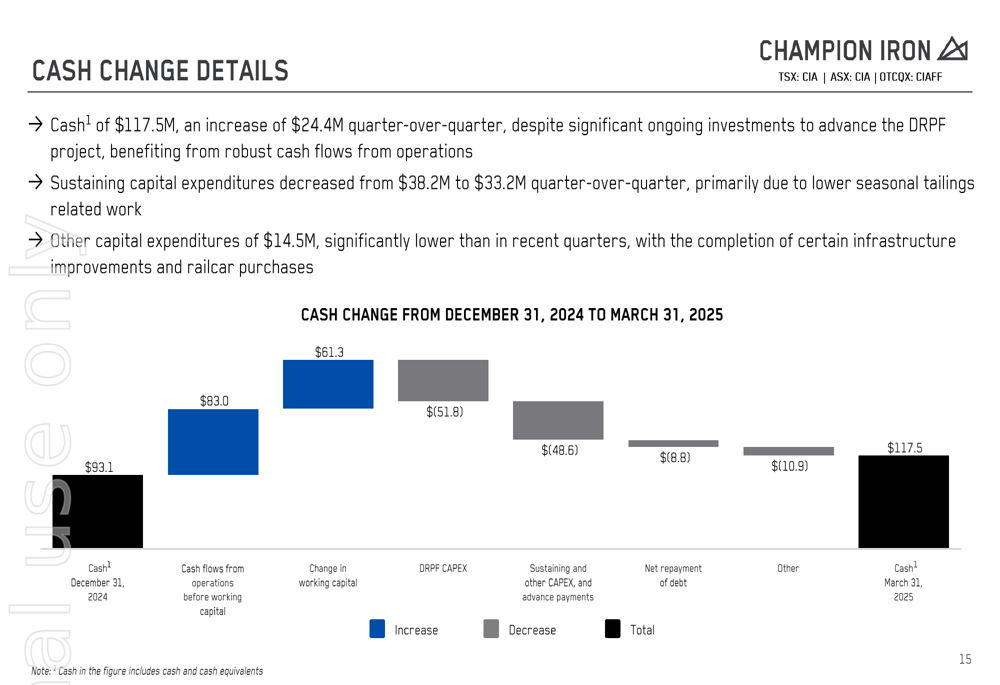

The company’s balance sheet remains solid with $117.5 million in cash and cash equivalents, representing an increase of $24.4 million from December 31, 2024. Working capital stood at $296.9 million, with total debt of $718.0 million and available loans of $488.4 million.

This chart details the cash flow changes during the quarter:

ESG and Sustainability Performance

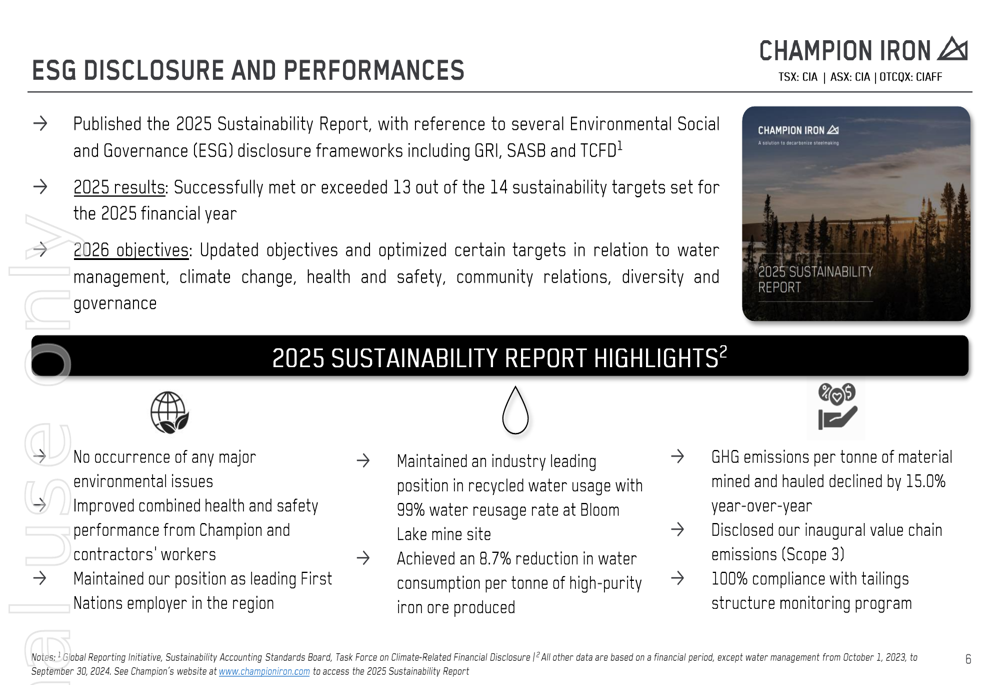

Champion Iron reported strong environmental, social, and governance (ESG) results for FY2025, successfully meeting or exceeding 13 out of 14 sustainability targets. The company maintained an industry-leading 99% water reusage rate at its Bloom Lake mine site and achieved an 8.7% reduction in water consumption per tonne of high-purity iron ore produced.

Other notable sustainability achievements included a 15.0% year-over-year reduction in greenhouse gas emissions per tonne of material mined and hauled, and 100% compliance with the tailings structure monitoring program. The company also disclosed its inaugural value chain emissions (Scope 3).

The following slide summarizes Champion’s ESG performance:

Growth Projects and Strategic Initiatives

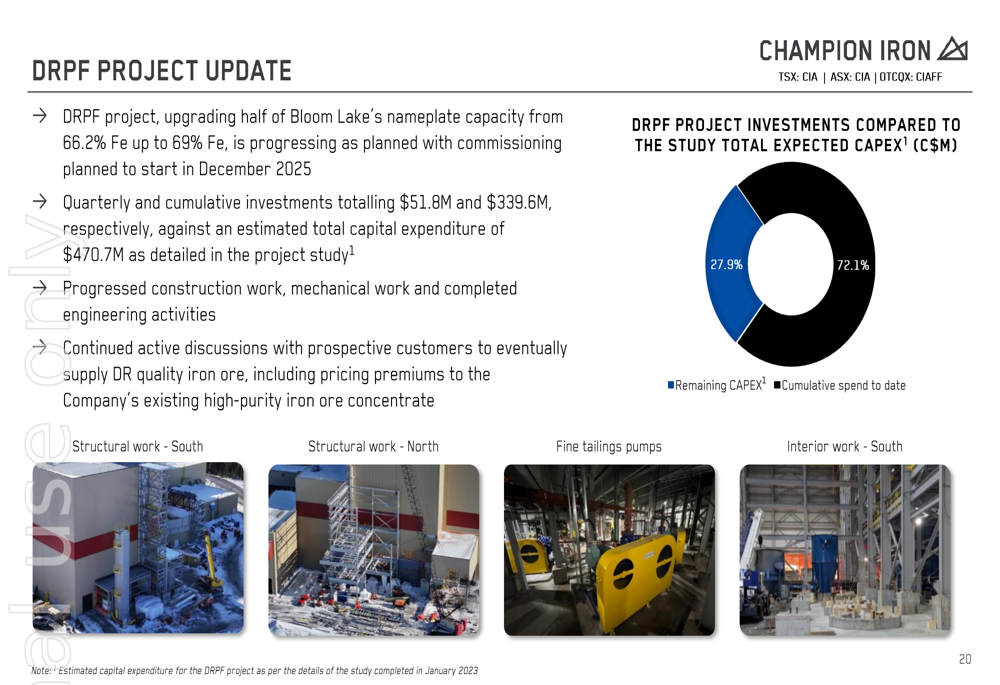

Champion Iron’s Direct Reduction Pellet Feed (DRPF) project continues to progress as planned, with commissioning scheduled to begin in December 2025. This strategic initiative will upgrade half of Bloom Lake’s nameplate capacity from 66.2% Fe up to 69% Fe, positioning the company to meet growing demand for higher-grade iron ore products used in green steel production.

Quarterly investments in the DRPF project totaled $51.8 million, with cumulative investments reaching $339.6 million. The project remains on schedule and budget as shown in the following update:

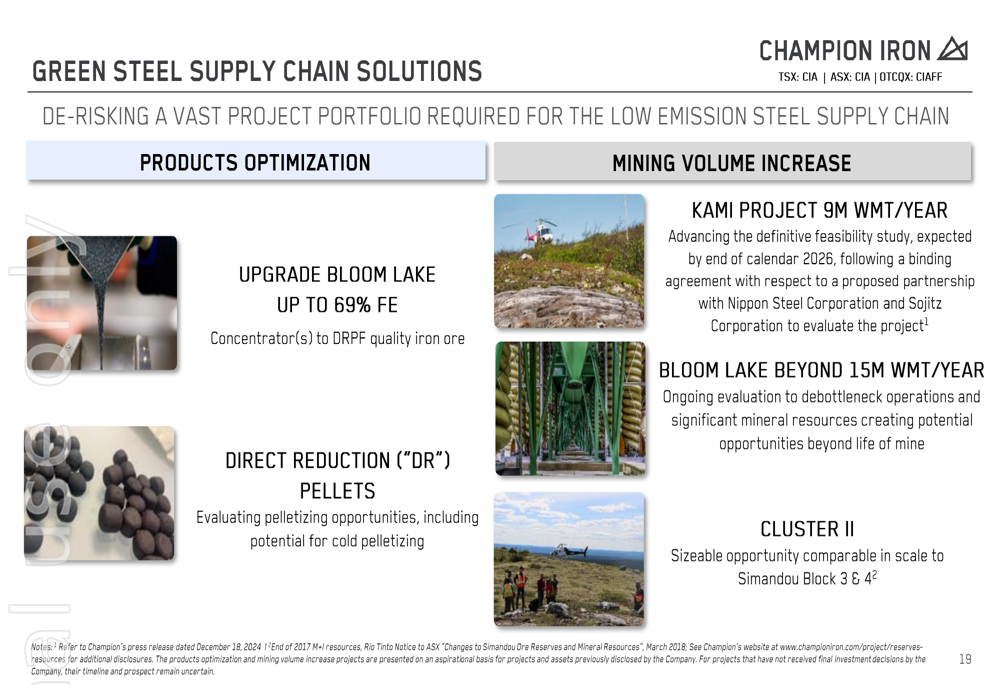

The company’s broader strategy includes multiple initiatives aimed at supporting the green steel supply chain. These include product optimization projects to upgrade Bloom Lake output to 69% Fe and produce direct reduction pellets, as well as mining volume increase projects such as the Kami Project (9M WMT/Year), Bloom Lake expansion beyond 15M WMT/Year, and Cluster II development.

The following slide illustrates Champion’s green steel supply chain solutions:

Market Outlook

Looking ahead, Champion Iron noted that while tariffs have been implemented in some markets, the impact on the company is mitigated by its diversified customer mix and lack of direct sales to the United States. The company remains focused on the ongoing green steel transition, which continues to gain momentum globally.

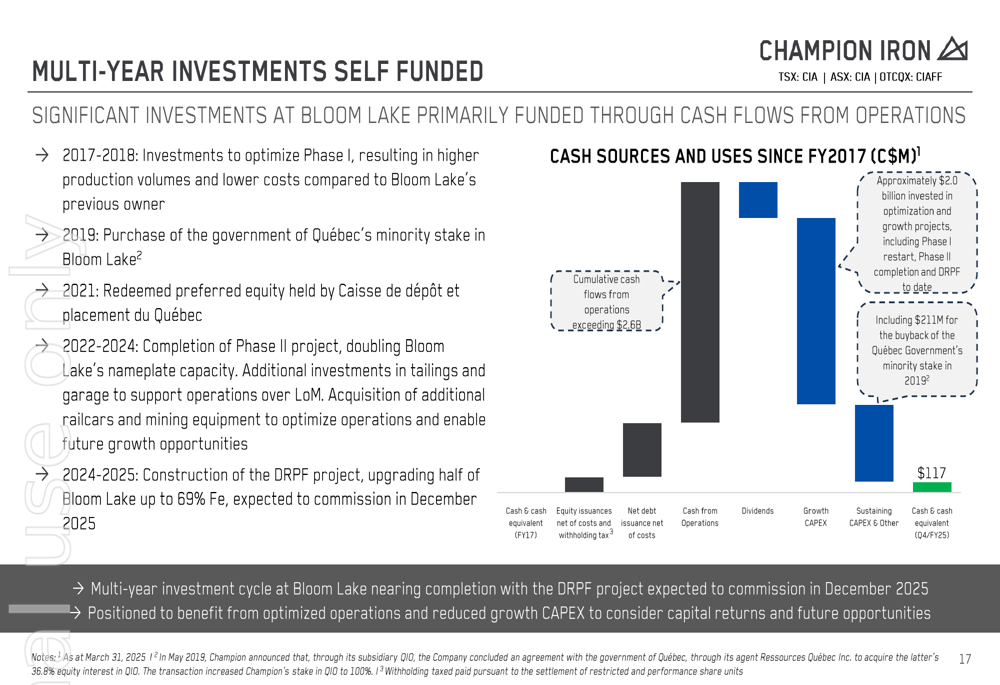

Champion’s multi-year investments, primarily funded through operational cash flows, have positioned the company well for future growth. Since 2017, cumulative cash flows from operations have exceeded $2.6 billion, with approximately $2.0 billion invested in optimization and growth projects.

This chart shows the company’s self-funded investment approach:

As the iron ore market navigates current challenges, Champion Iron’s focus on high-purity products, operational efficiency, and strategic growth initiatives appears to provide a solid foundation for navigating the evolving industry landscape and capitalizing on the green steel transition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.