ReElement Technologies stock soars after securing $1.4B government deal

Charles River Laboratories (NYSE:CRL) reported better-than-expected second quarter 2025 results on August 6, raising its full-year guidance as the company sees signs of stabilization in the biopharma market. The stock jumped over 4% in premarket trading following the presentation.

Quarterly Performance Highlights

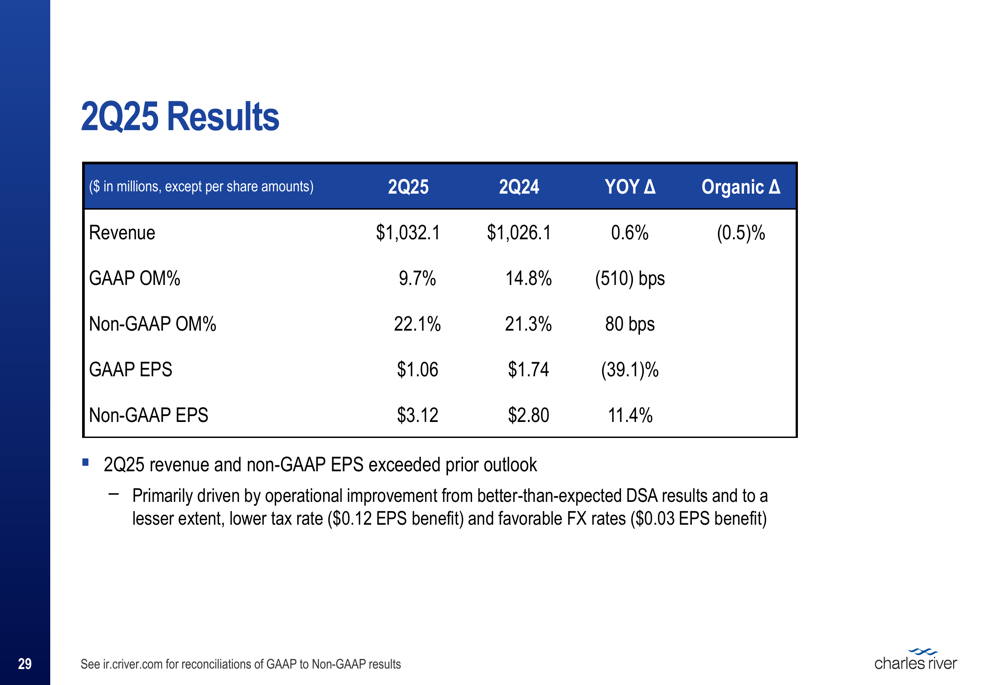

Charles River reported Q2 2025 revenue of $1,032.1 million, representing a 0.6% year-over-year increase but a 0.5% organic decline. Non-GAAP earnings per share reached $3.12, up 11.4% from the prior year, while GAAP EPS declined 39.1% to $1.06. The company’s non-GAAP operating margin improved by 80 basis points to 22.1%.

As shown in the following comprehensive results summary, the company exceeded its prior outlook for both revenue and earnings:

The outperformance was primarily driven by better-than-expected results in the Discovery (NASDAQ:WBD) and Safety Assessment (DSA) segment, a lower tax rate that contributed $0.12 to EPS, and favorable foreign exchange rates that added $0.03 to EPS.

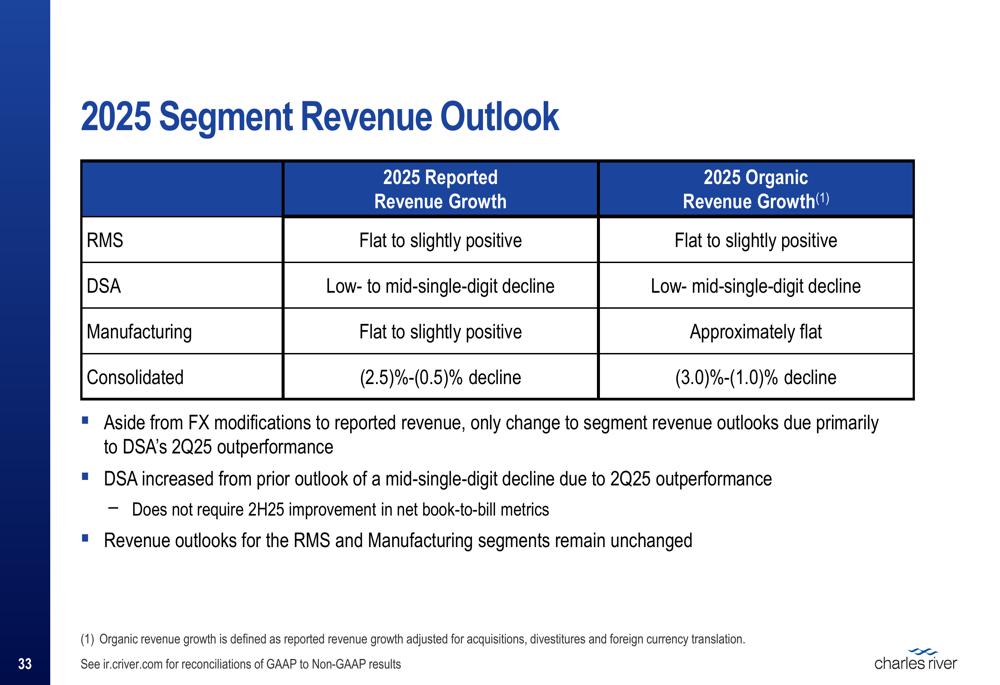

Segment performance was mixed, with the Research Models and Services (RMS) segment growing 3.3% (2.3% organic) and Manufacturing Solutions increasing 4.4% (2.9% organic), while DSA declined 1.5% (2.4% organic).

Signs of Market Stabilization

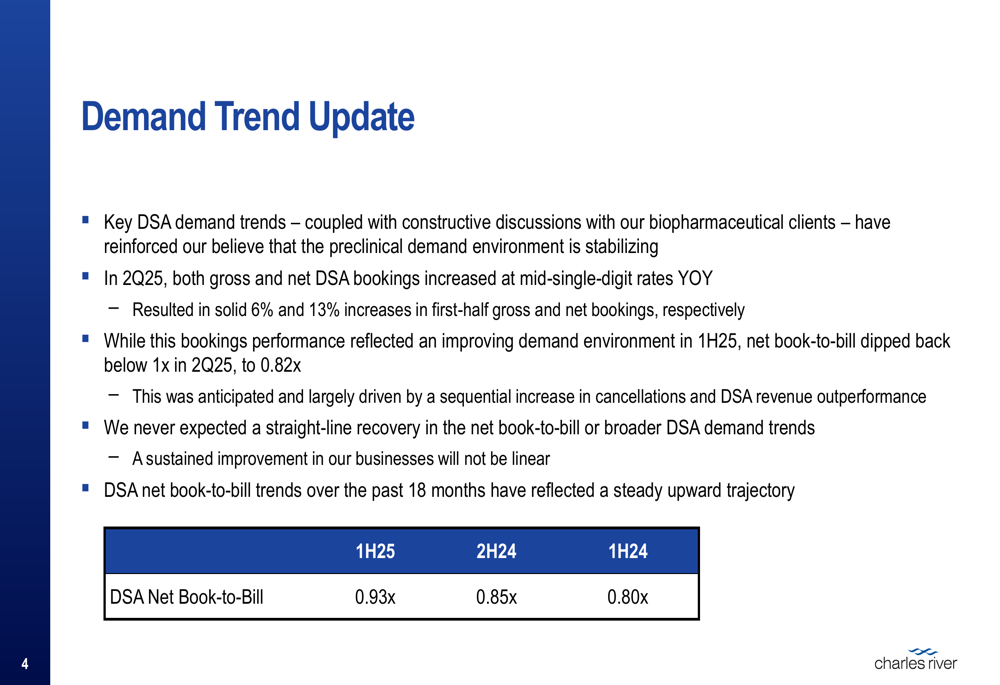

A key highlight from the presentation was evidence of stabilizing demand in the preclinical research market, particularly in the critical DSA segment. The company reported that DSA gross and net bookings increased at mid-single-digit rates year-over-year in Q2, with first-half increases of 6% and 13% for gross and net bookings, respectively.

The following slide illustrates the improving trend in DSA book-to-bill ratios, with the first half of 2025 reaching 0.93x compared to 0.80x in the first half of 2024:

Management noted that while the DSA net book-to-bill dipped below 1x in Q2 to 0.82x, this was anticipated due to cancellations and DSA revenue outperformance. The company emphasized that sustained improvement will be non-linear but pointed to the steady upward trajectory in DSA net book-to-bill trends.

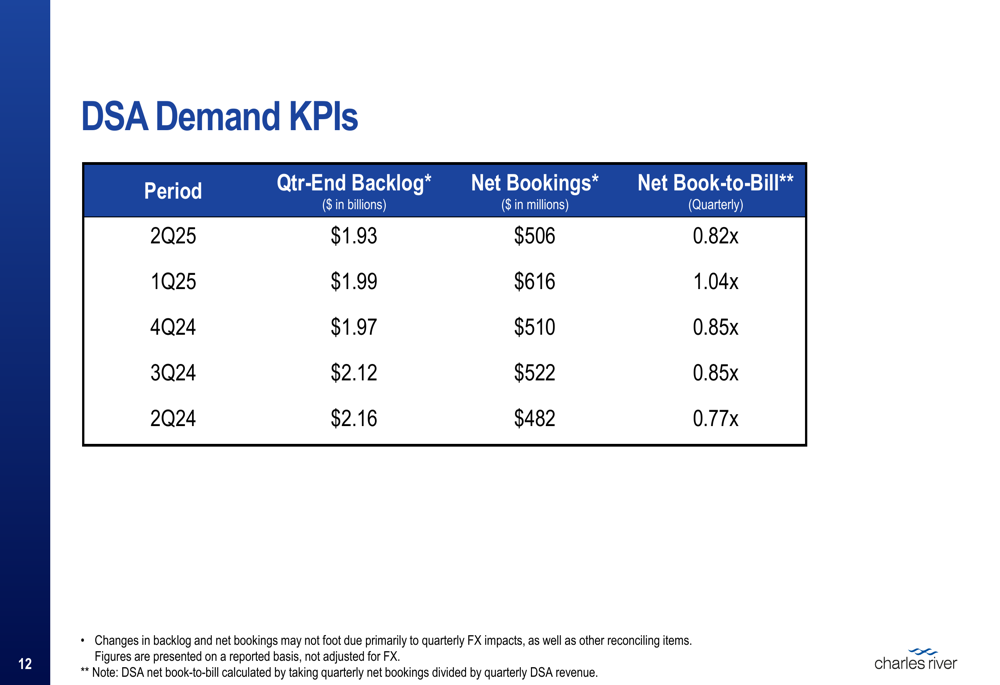

The detailed DSA demand KPIs further support this stabilization narrative:

The company described the broader biopharma environment as "bottoming out and moving slowly upward," while characterizing the biotech environment as "stable but mixed," with smaller biotechs remaining cash-constrained due to funding slowdowns, while mid-sized biotechs are performing better.

Strategic Initiatives

Charles River highlighted its progress on New Approach Methodologies (NAMs) as alternatives to animal testing. The company’s NAMs portfolio currently generates approximately $200 million annually in DSA revenue, with client interest building. Management emphasized that while NAMs-enabled approaches represent a long-term transition, the scientific capabilities to fully replace animal models do not currently exist.

The company also provided an update on its strategic review, stating that it is "progressing well" but offering few details. Management indicated they are evaluating avenues for value creation, including portfolio optimization, capital allocation, and market positioning, with the goal of enhancing shareholder value.

In a positive development for the company’s non-human primate (NHP) supply chain, Charles River announced that the Department of Justice is no longer conducting investigations related to NHP shipments, and the U.S. Fish and Wildlife Service has cleared all NHP shipments from Cambodia for legal entry into the U.S.

Updated 2025 Guidance

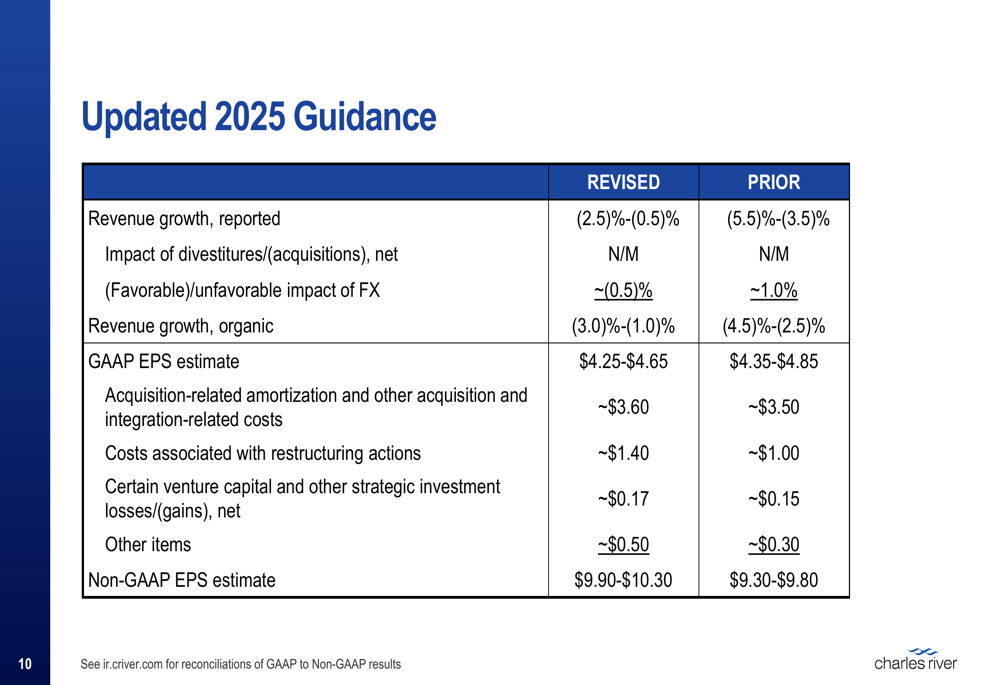

Based on the strong Q2 performance, Charles River raised its full-year 2025 guidance. The company now expects reported revenue to decline 0.5% to 2.5% (organic decline of 1.0% to 3.0%), an improvement from the previous outlook of a 3.5% to 5.5% reported decline.

The following detailed guidance table shows the revisions across key metrics:

Non-GAAP EPS guidance was increased to $9.90-$10.30, up $0.55 at the midpoint from the previous range of $9.30-$9.80. This increase reflects both operational outperformance in Q2 and favorable foreign exchange movements, which are expected to contribute approximately $0.14 to full-year EPS.

The updated segment revenue outlook is summarized below:

Operational Improvements and Challenges

Charles River highlighted its cost-saving initiatives, noting that restructuring efforts are expected to deliver over $175 million in savings this year and approximately $225 million next year. These savings have contributed to the improved operating margin performance.

However, the company also identified several headwinds for the second half of 2025, including:

1. Non-repeating commercial cell therapy revenue that generated approximately $20 million in the first half

2. Increased hiring in the DSA segment, adding approximately $10 million to second-half costs

3. Timing of annual merit increases

4. Tax rate increases due to recent U.S. tax legislation changes

Despite these challenges, the company maintained a positive outlook on its ability to navigate the evolving market environment and capitalize on signs of stabilization in biopharma demand.

Conclusion

Charles River’s Q2 2025 presentation paints a picture of a company seeing early signs of recovery after a challenging period. The improved guidance and evidence of stabilizing demand in the key DSA segment suggest the worst may be behind the company, though management remains cautious about the pace of recovery.

With strategic initiatives like NAMs development and the ongoing strategic review, Charles River appears positioned to capitalize on market improvements while adapting to evolving industry trends. Investors responded positively to the presentation, with the stock rising over 4% in premarket trading to $174.37.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.