Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Charter Communications (NASDAQ:CHTR) presented its second quarter 2025 results on July 25, showing minimal revenue and EBITDA growth that failed to impress investors, sending shares plummeting more than 18% during regular trading hours and continuing to fall in the after-market session.

Introduction & Market Context

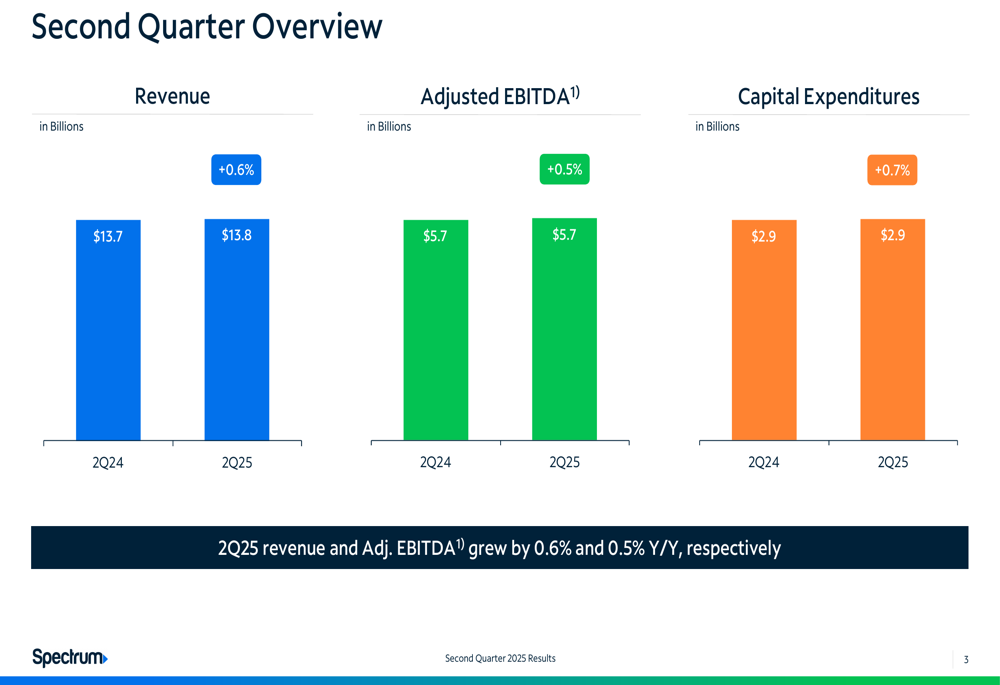

Charter reported Q2 2025 revenue of $13.8 billion, up just 0.6% year-over-year, while Adjusted EBITDA grew 0.5% to $5.7 billion. These modest gains, coupled with continued customer losses in core segments, triggered a significant market selloff, with the stock closing down 18.49% at $309.75 and falling an additional 13.16% in after-hours trading to $329.98.

The disappointing market reaction stands in stark contrast to the company’s Q1 2025 earnings report, which saw shares surge nearly 9% after slightly beating analyst expectations.

Quarterly Performance Highlights

Charter’s presentation highlighted its Q2 2025 financial performance, showing minimal growth across key metrics compared to the same period last year.

As shown in the following chart of quarterly financial results:

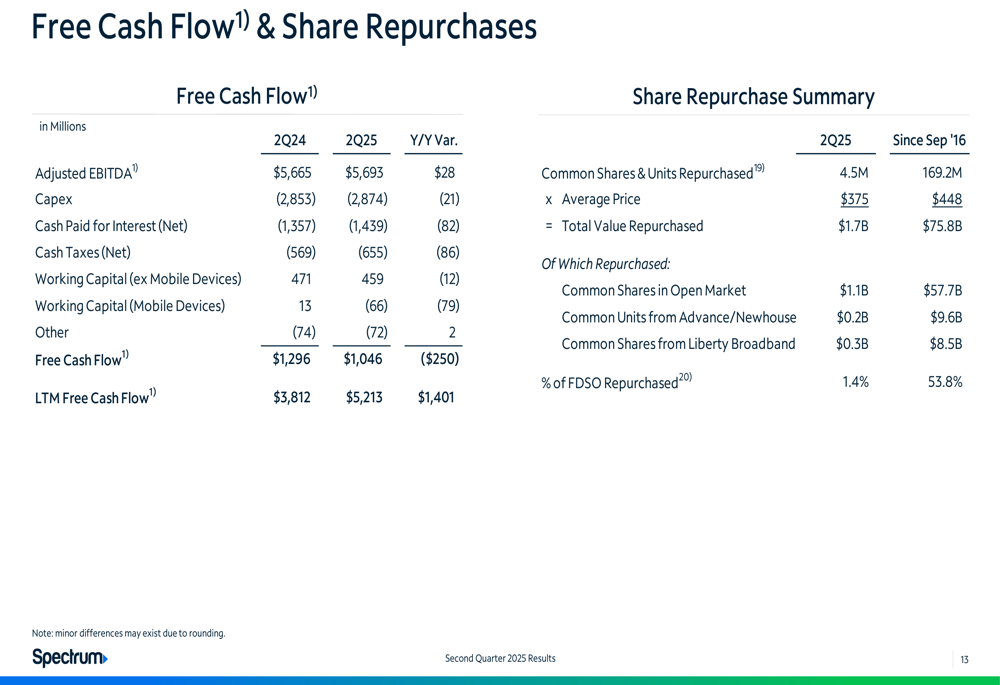

The company’s capital expenditures increased 0.7% year-over-year to $2.9 billion, while free cash flow reached $1,046 million for the quarter. Charter maintained a net leverage ratio of 4.10x, or 4.18x pro forma for the Liberty Broadband (NASDAQ:LBRDA) transaction.

Revenue performance was mixed across segments, with residential revenue declining 0.4% to $10.7 billion while commercial revenue grew 0.8% to $1.8 billion.

On the expense side, total costs increased at the same rate as revenue (0.6%), reaching $8.1 billion for the quarter, which limited EBITDA growth to just 0.5%.

Customer Trends

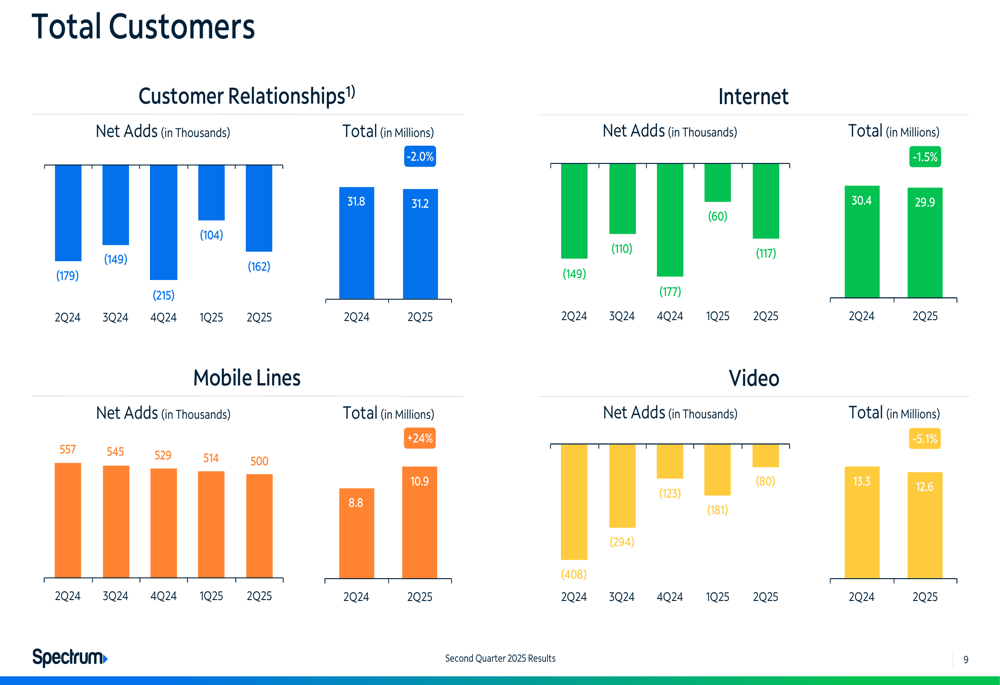

The most concerning aspect of Charter’s presentation was the continued erosion of its traditional customer base, with total customer relationships declining 2.0% year-over-year to 31.2 million. Internet customers, a critical growth segment for cable operators, fell 1.5% to 29.9 million, while video subscribers dropped 5.1% to 12.6 million.

The lone bright spot was Charter’s mobile business, which grew 24% year-over-year to reach 10.9 million lines. However, this growth was insufficient to offset declines in the company’s core business segments.

The following chart illustrates these customer trends:

Competitive Positioning

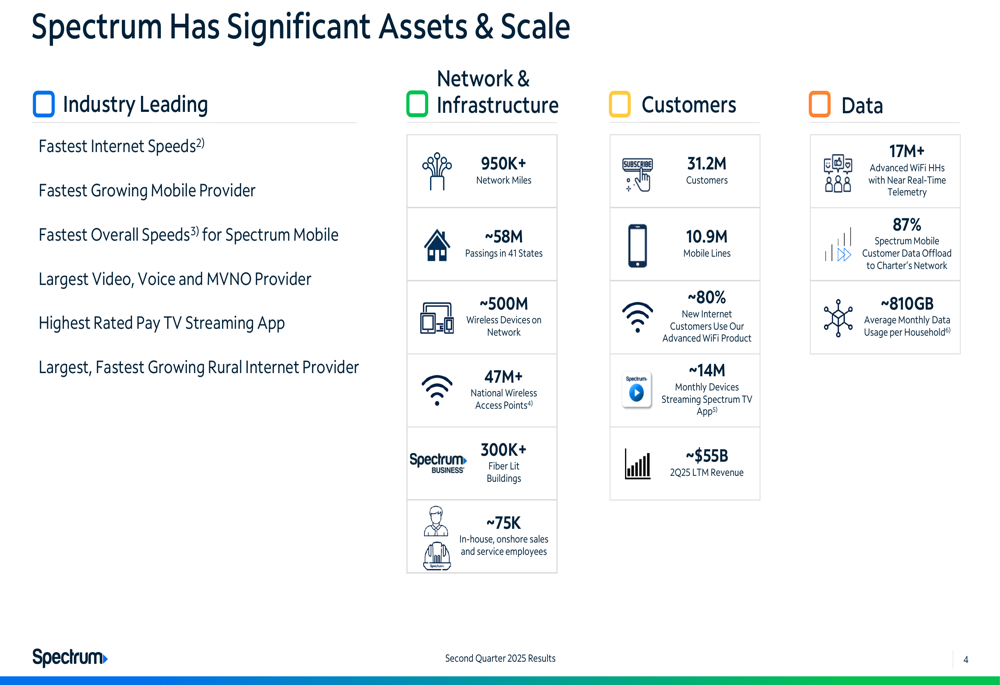

Despite the challenging quarter, Charter emphasized its competitive advantages, particularly its extensive network infrastructure and pricing strategy versus telecom competitors.

The company highlighted its significant network assets, including over 950,000 network miles, approximately 58 million passings in 41 states, and 10.9 million mobile lines. Charter also emphasized its data capabilities, noting that the average household uses approximately 810GB of data monthly.

As illustrated in this comprehensive overview of Charter’s assets:

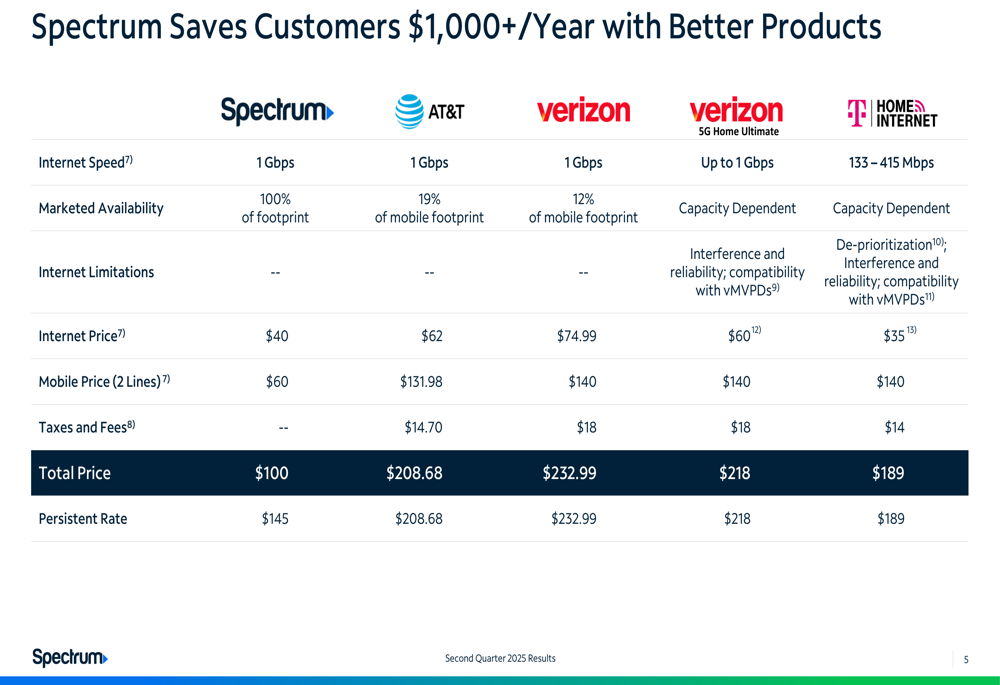

Charter positioned its pricing as more competitive than major telecom providers, offering 1 Gbps internet with full footprint availability at $100 ($145 persistent rate), compared to significantly higher prices from AT&T (NYSE:T), Verizon (NYSE:VZ), and T-Mobile, which also have more limited availability of comparable services.

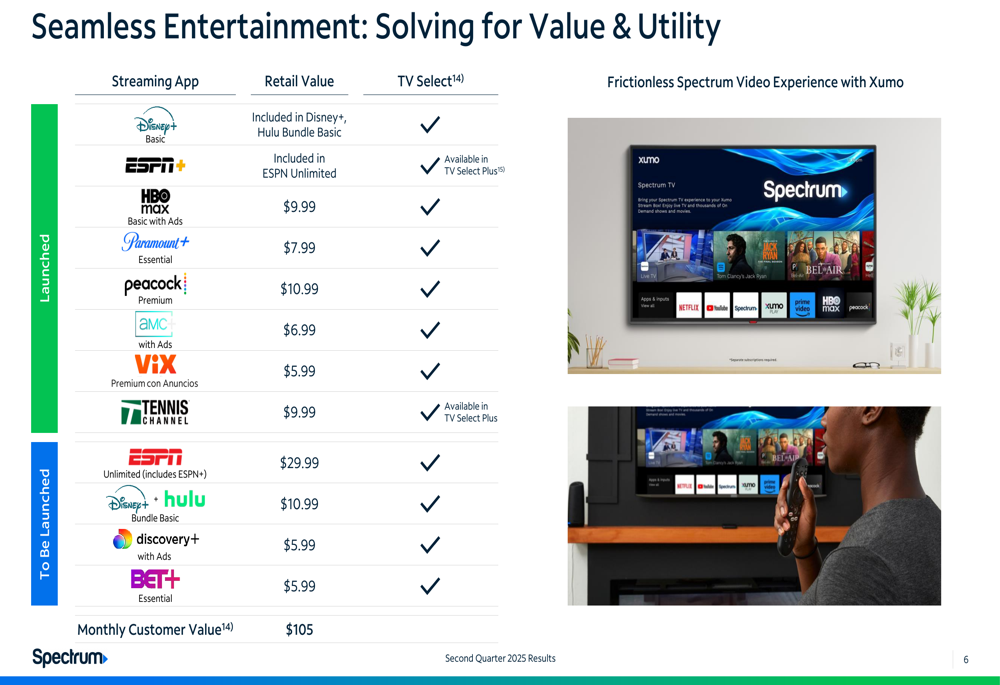

The company also emphasized its streaming partnerships, highlighting the value of its TV Select and TV Select Plus packages, which include popular streaming services like Disney+, HBO Max, Paramount+, and Peacock.

Strategic Initiatives

Charter outlined its strategy for long-term value creation, focusing on three key pillars: operating strategy, strategic initiatives, and shareholder value.

The operating strategy emphasizes high-quality products, unique customer value, commitment to service, and ties to local communities. Strategic initiatives focus on evolution, expansion, and execution, while shareholder value centers on long-term revenue and cash flow growth, along with levered equity returns.

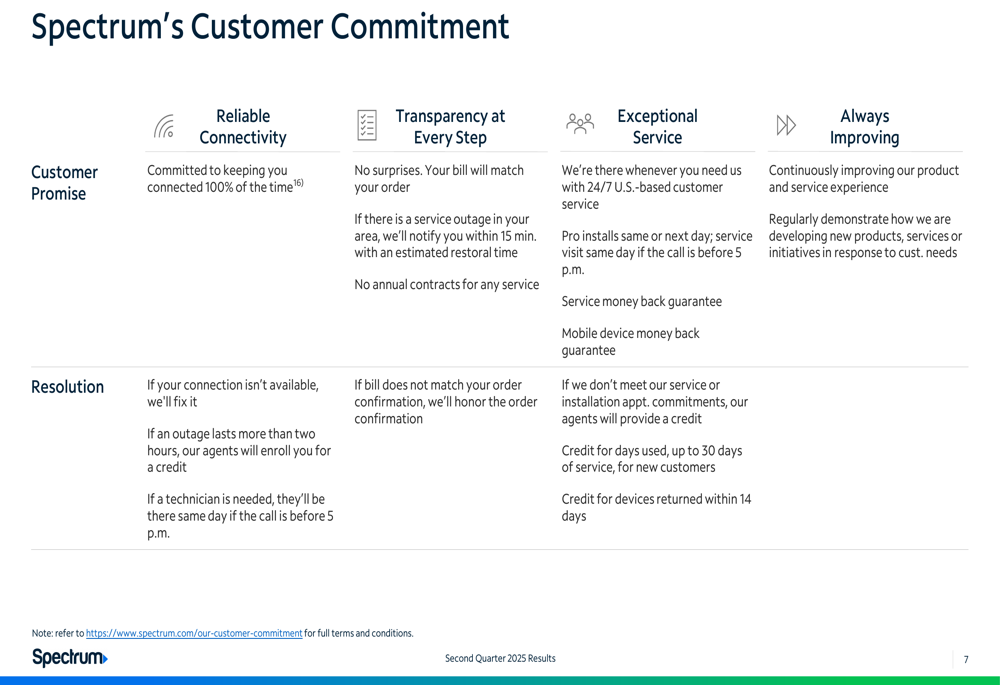

The company also detailed its customer commitment, focusing on reliable connectivity, transparency, exceptional service, and continuous improvement. Charter promised to be connected 100% of the time, match bills to orders, provide notifications for service outages within 15 minutes, and offer U.S.-based customer service.

Forward-Looking Statements

While the presentation did not provide specific forward guidance, the significant stock decline suggests investors are concerned about Charter’s ability to reverse customer losses in its core internet business and accelerate overall growth.

The continued strength in mobile lines (24% growth) provides a potential avenue for future expansion, but the company will need to address the ongoing erosion in its traditional cable and internet segments to restore investor confidence.

The stark contrast between the modest financial growth presented (0.6% revenue, 0.5% EBITDA) and the severe market reaction indicates investors had significantly higher expectations for the quarter or are concerned about longer-term competitive pressures in the broadband market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.