SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Chegg Inc (NYSE:CHGG) released its Q2 2025 investor presentation on August 5, 2025, revealing significant year-over-year declines in revenue and subscribers as the education technology company continues its strategic pivot toward skills-based offerings. The stock closed at $1.39 before the earnings release, down 7.91% during the regular trading session, and fell an additional 2.16% in after-hours trading.

The company’s presentation portrayed Q2 as "good" despite showing substantial declines across key metrics, highlighting instead its progress on cost-cutting initiatives and strategic alternatives exploration. This comes after a challenging Q1 2025 where Chegg reported a 30% year-over-year revenue decline, a trend that has worsened in the second quarter.

Quarterly Performance Highlights

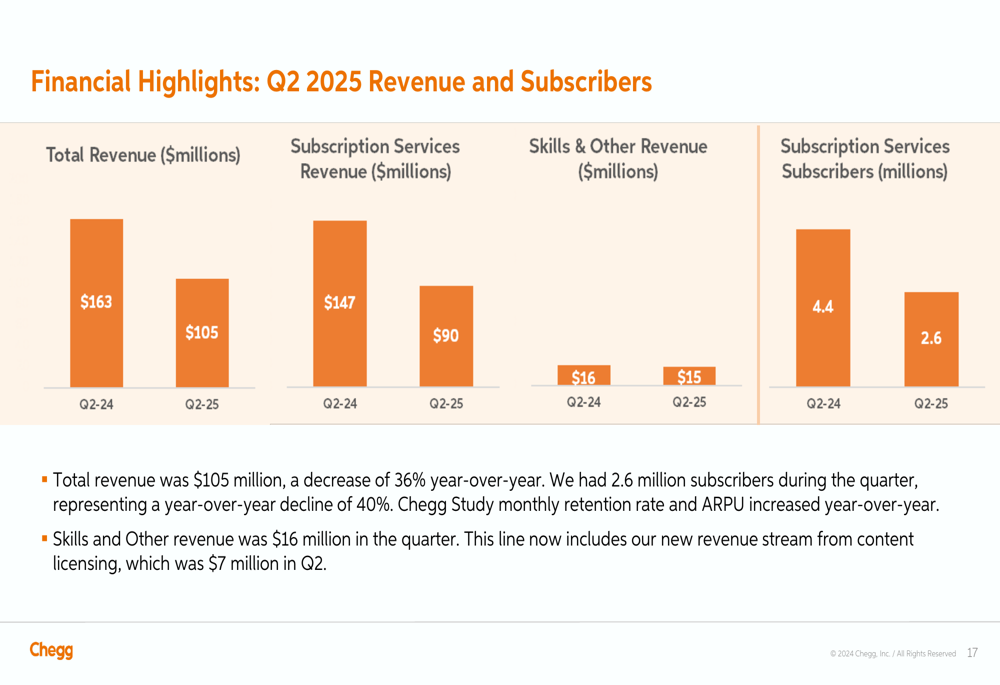

Chegg reported total revenue of $105 million for Q2 2025, representing a 36% decrease from $163 million in the same period last year. Subscription services revenue, which forms the core of Chegg’s business, fell 39% year-over-year to $90 million.

As shown in the following chart of Chegg’s Q2 2025 revenue and subscribers:

The company’s subscriber base contracted significantly, falling 40% year-over-year to 2.6 million subscribers. This accelerating decline follows the 31% drop in subscribers reported in Q1 2025, indicating worsening challenges in Chegg’s core business.

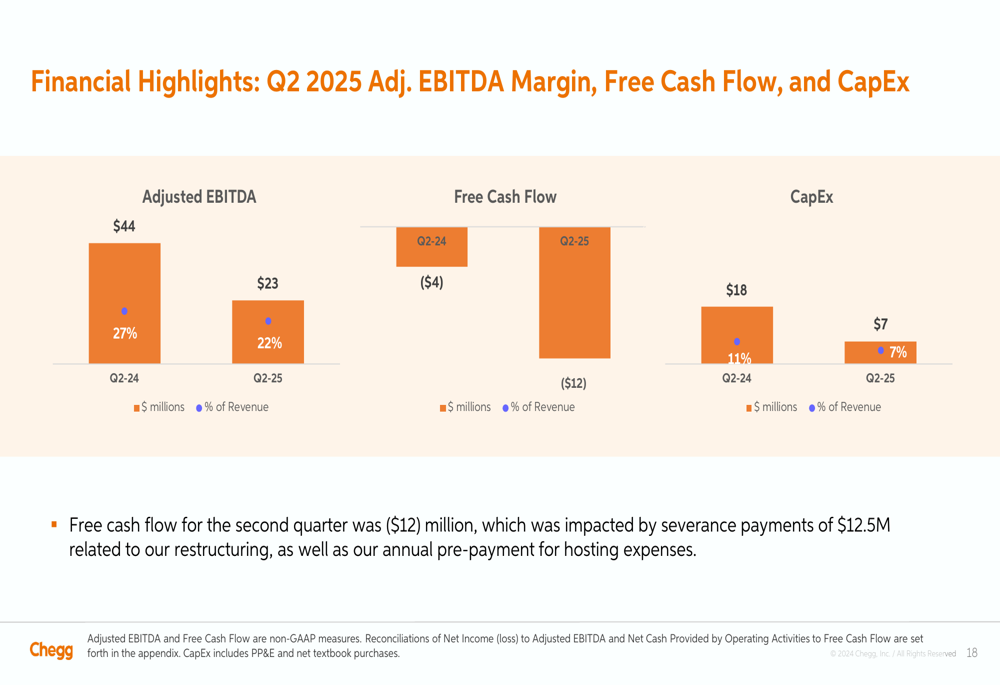

Adjusted EBITDA for the quarter was $23 million, representing a 22% margin, down from $44 million (27% margin) in Q2 2024. Free cash flow was negative $12 million, compared to negative $4 million in the prior year period, with the company noting the impact of $12.5 million in severance payments related to restructuring efforts.

The following chart illustrates these financial metrics:

Strategic Initiatives

Facing significant headwinds in its core business, Chegg is aggressively cutting costs while pivoting toward skills-focused offerings. The company identified an additional $17 million in cost savings for 2026, bringing total expected non-GAAP expense savings for that year to $110-120 million. Chegg remains on track to reduce non-GAAP expenses by $165-175 million in 2025.

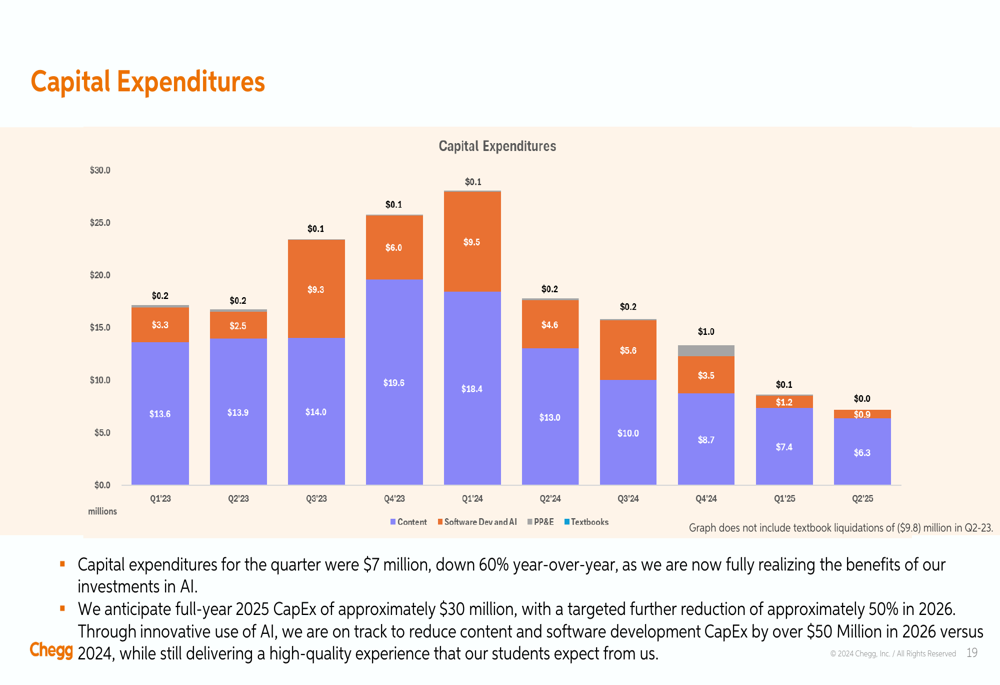

Capital expenditures have been dramatically reduced, falling 60% year-over-year to $7 million in Q2 2025. The company expects full-year 2025 CapEx of approximately $30 million, with a targeted further reduction of approximately 50% in 2026.

The following chart shows Chegg’s capital expenditure trends:

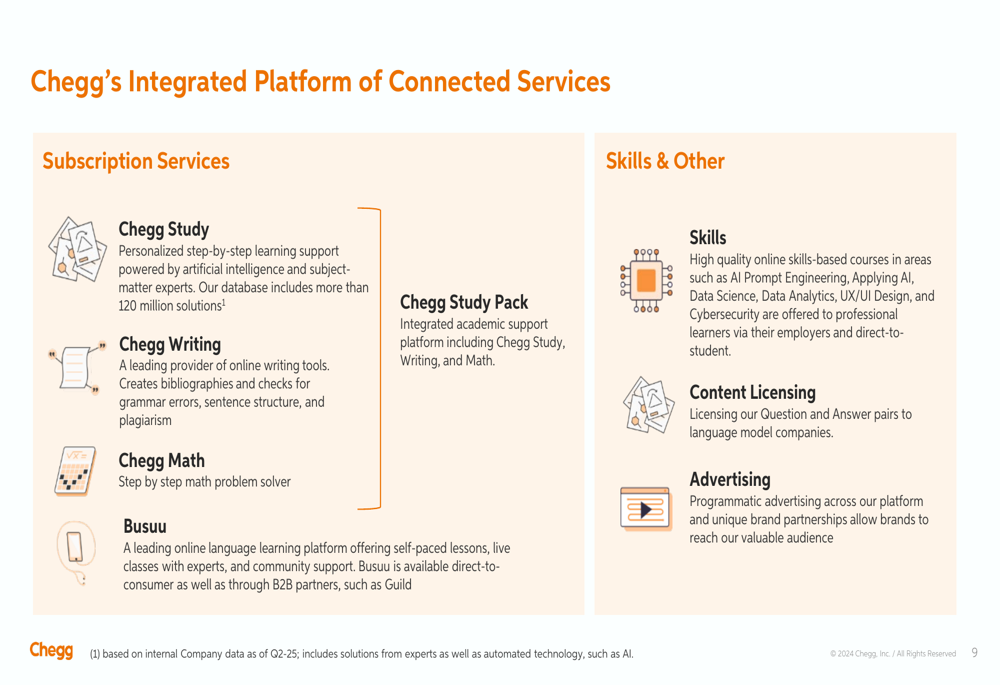

Chegg is evolving its product portfolio, with a particular focus on workplace readiness and upskilling programs. The company’s integrated platform now spans subscription services like Chegg Study and Chegg Math, alongside growing skills-based offerings.

As illustrated in this overview of Chegg’s platform:

The company is placing significant emphasis on its Chegg Skills offerings, targeting what it describes as a ~$40 billion market opportunity in workplace readiness and upskilling. These programs combine industry-aligned curriculum, personalized coaching, and AI-enabled tools across various certificate programs.

The following image details Chegg’s skills-based offerings:

Detailed Financial Analysis

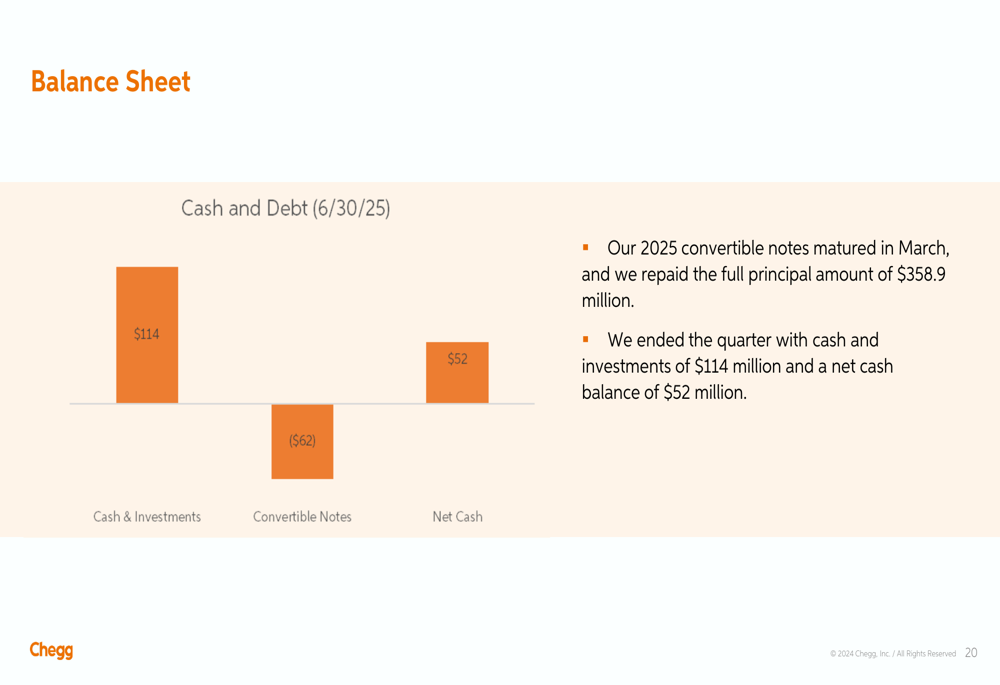

Chegg ended Q2 2025 with $114 million in cash and investments and $62 million in convertible notes, resulting in a net cash position of $52 million. The company repaid the full principal amount of $358.9 million for its 2025 convertible notes that matured in March.

As shown in this balance sheet summary:

The company’s revenue now includes a new stream from content licensing, which contributed $7 million in Q2 2025. This represents a strategic move to monetize Chegg’s content library amid challenges in its subscription business.

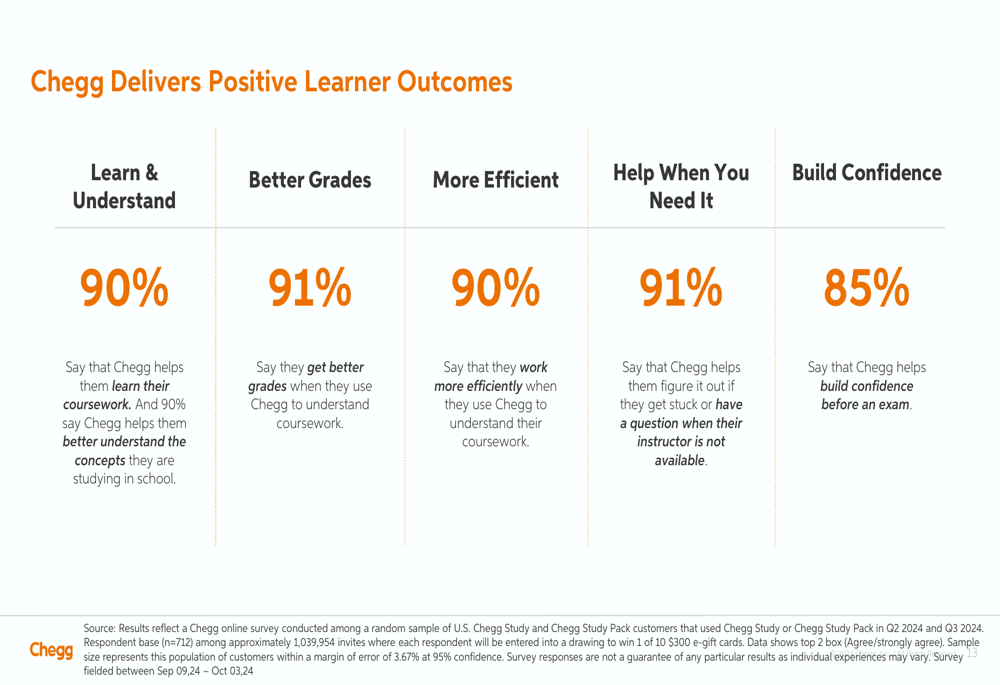

Despite the overall revenue decline, Chegg continues to highlight the positive outcomes its platform delivers for students. According to company surveys, 90% of students say Chegg helps them learn coursework, 91% report getting better grades, and 90% say they work more efficiently.

The following chart presents these learner outcomes:

Forward-Looking Statements

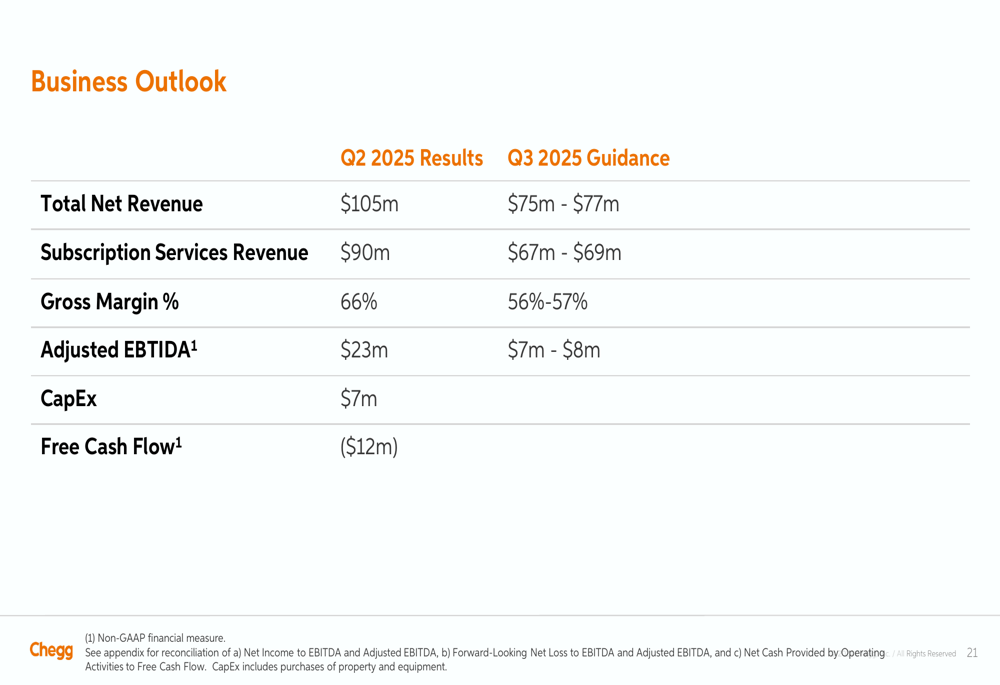

For Q3 2025, Chegg provided guidance of $75-77 million in total revenue, representing a significant sequential decline from Q2’s $105 million. Subscription services revenue is expected to be $67-69 million, with gross margin projected at 56-57% and adjusted EBITDA of $7-8 million.

The following table details Chegg’s Q3 2025 outlook:

Beyond immediate financial guidance, Chegg disclosed that it is making progress on its strategic alternatives process, exploring options including potential acquisition or remaining a public standalone company. This exploration comes as the company faces mounting challenges in its core business.

Looking toward 2026, Chegg is positioning itself as a skills-focused organization, investing in language learning, workplace readiness, and upskilling. The company is also introducing new AI-powered products like Solution Scout, which provides side-by-side comparisons of solutions from multiple large language models alongside Chegg’s expert solutions.

Competitive Industry Position

Chegg continues to emphasize its understanding of students and learning, highlighting its database of over 100 million question-and-answer pairs and approximately 3 billion monthly data interaction points. The company segments its U.S. college market of 15 million students into three persona types: Satisfiers (18%), Achievers (39%), and Knowledge Seekers (44%).

The company also underscores the diversity of its user base, noting that 28% are first-generation college students, 53% are minorities, 61% are female, and 26% are over 25 years old. Additionally, 38% of users work either full-time (5%) or part-time (33%) while studying.

Despite these strengths, Chegg faces significant challenges from the proliferation of AI-powered educational tools and changing student behaviors. The company’s strategic pivot toward skills-based offerings and workplace readiness programs appears to be a response to these competitive pressures, as it seeks to differentiate itself in an increasingly crowded educational technology landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.