US stock futures muted as rate cut bets wane ahead of Jackson Hole

Introduction & Market Context

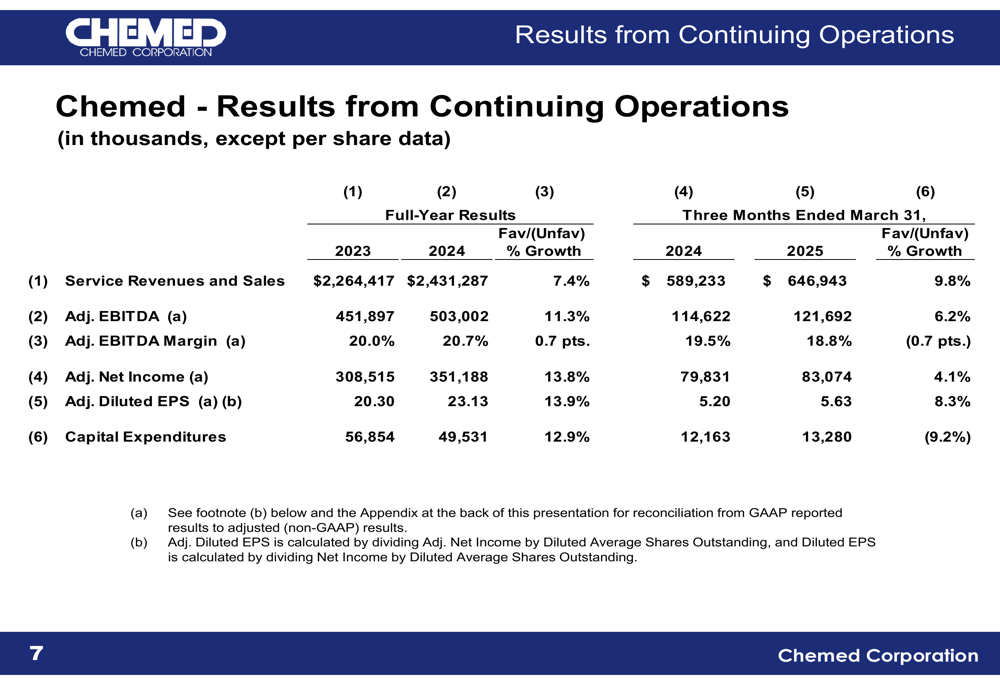

Chemed Corporation (NYSE:CHE) recently presented its Q1 2025 financial results, highlighting a 9.8% increase in service revenues and sales compared to the same period last year. Despite beating analyst expectations with earnings per share of $5.63 and revenue of $646.9 million, the company’s stock fell 5.15% in after-hours trading following the announcement, reflecting investor concerns about mixed performance across its business segments.

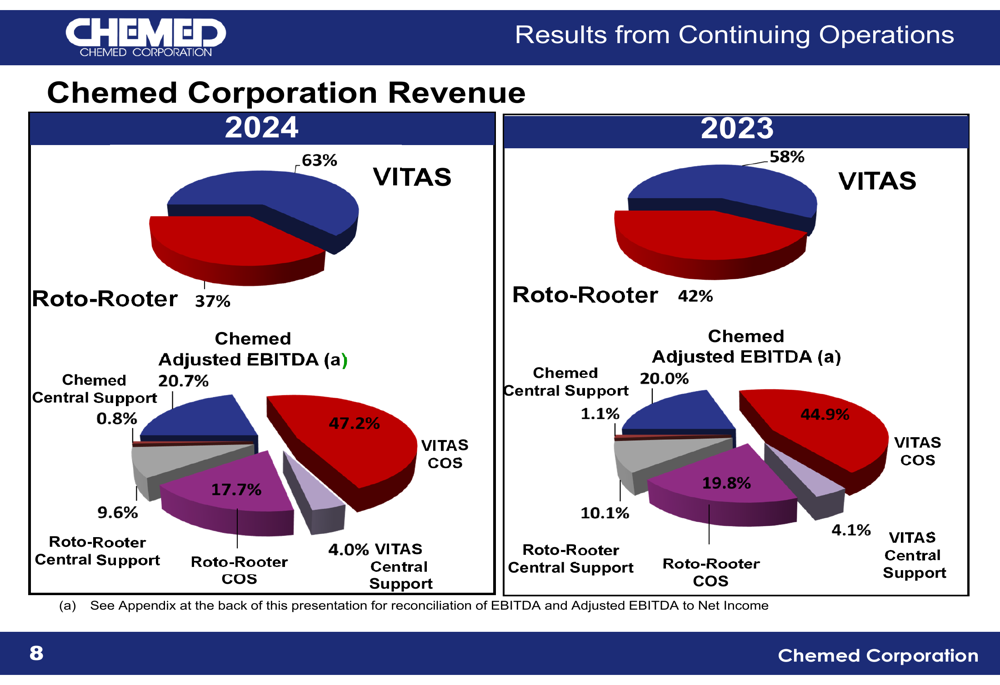

Chemed operates through two primary business segments: VITAS Healthcare, which provides hospice services, and Roto-Rooter, which offers plumbing and water cleanup services. The presentation revealed a continued shift in the company’s revenue mix, with VITAS now representing 63% of total revenue in 2024, up from 58% in 2023, while Roto-Rooter’s contribution declined from 42% to 37%.

Quarterly Performance Highlights

Chemed’s Q1 2025 results demonstrated solid overall growth, with adjusted EBITDA increasing 6.2% and adjusted net income rising 4.1% compared to Q1 2024. Notably, adjusted diluted EPS grew by 8.3%, reflecting the impact of the company’s ongoing share repurchase program.

As shown in the following chart of Chemed’s continuing operations results, the company has maintained consistent growth in key financial metrics:

The VITAS Healthcare segment was the primary driver of growth, with revenue increasing 15.1% year-over-year to $407.4 million in Q1 2025. This strong performance helped offset challenges in the Roto-Rooter segment, which experienced a modest 3.1% growth in gross branch revenue but faced a 2.4% decline in adjusted EBITDA.

The following chart illustrates the shift in revenue contribution between Chemed’s two business segments:

Detailed Financial Analysis

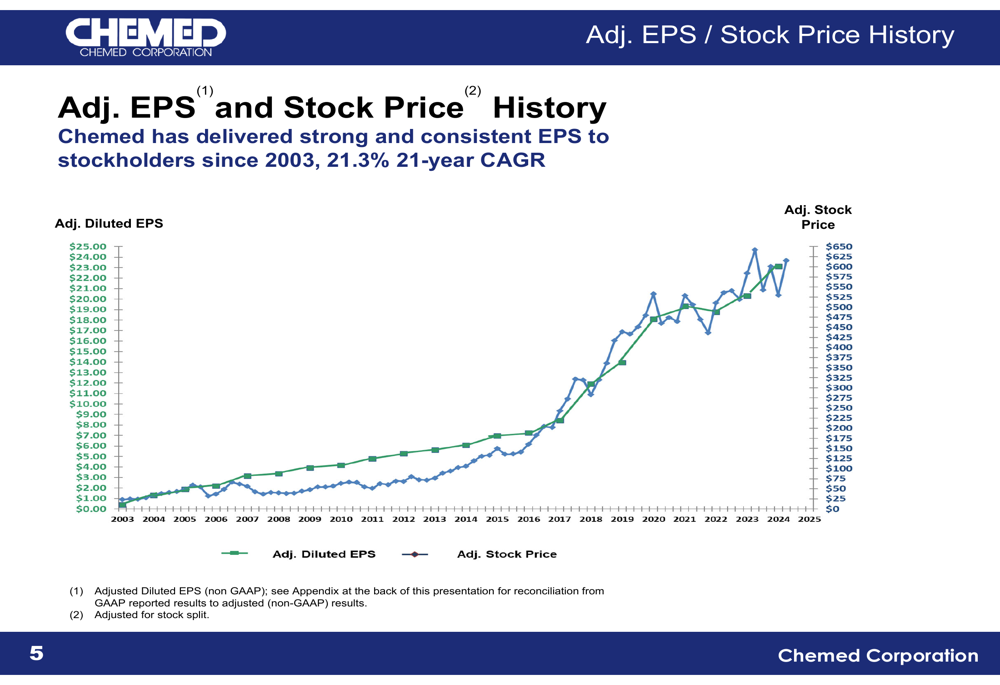

Chemed’s long-term financial performance remains impressive, with a 21-year compound annual growth rate (CAGR) of 21.3% for adjusted diluted EPS since the VITAS acquisition in 2003. The company has consistently generated strong free cash flow, which has supported its capital allocation strategy focused on share repurchases and dividends.

The following chart illustrates Chemed’s adjusted EPS growth and stock price performance since 2003:

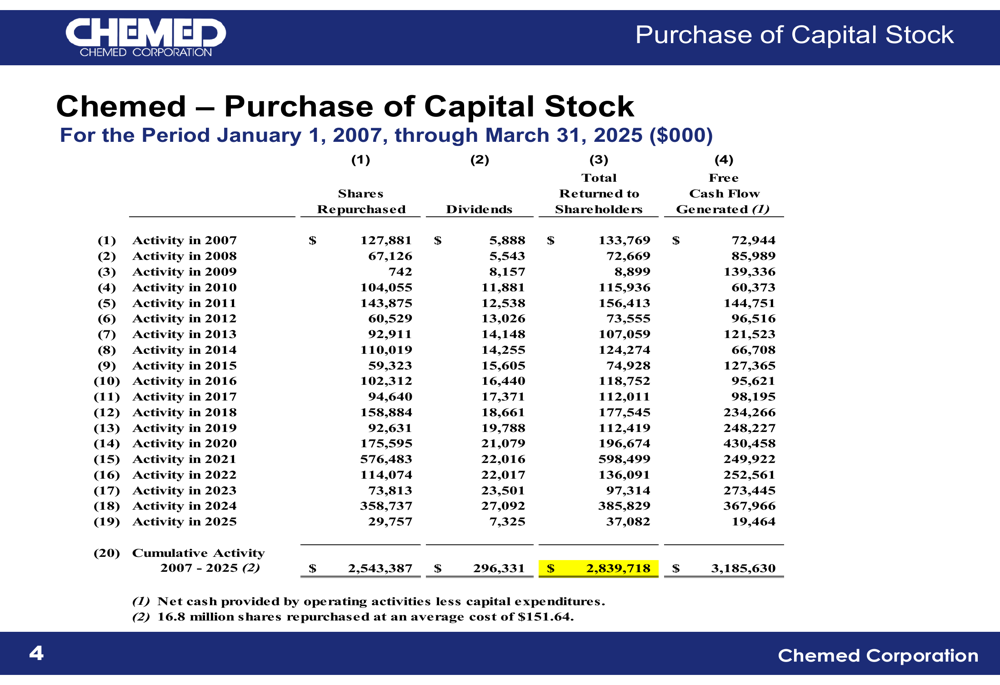

Chemed has maintained a disciplined approach to capital allocation, returning significant value to shareholders through share repurchases and dividends. Since 2007, the company has repurchased 16.8 million shares at an average cost of $151.64 and paid $296.3 million in dividends, totaling $2.84 billion returned to shareholders.

As shown in the following table detailing Chemed’s capital stock purchases:

Strategic Initiatives

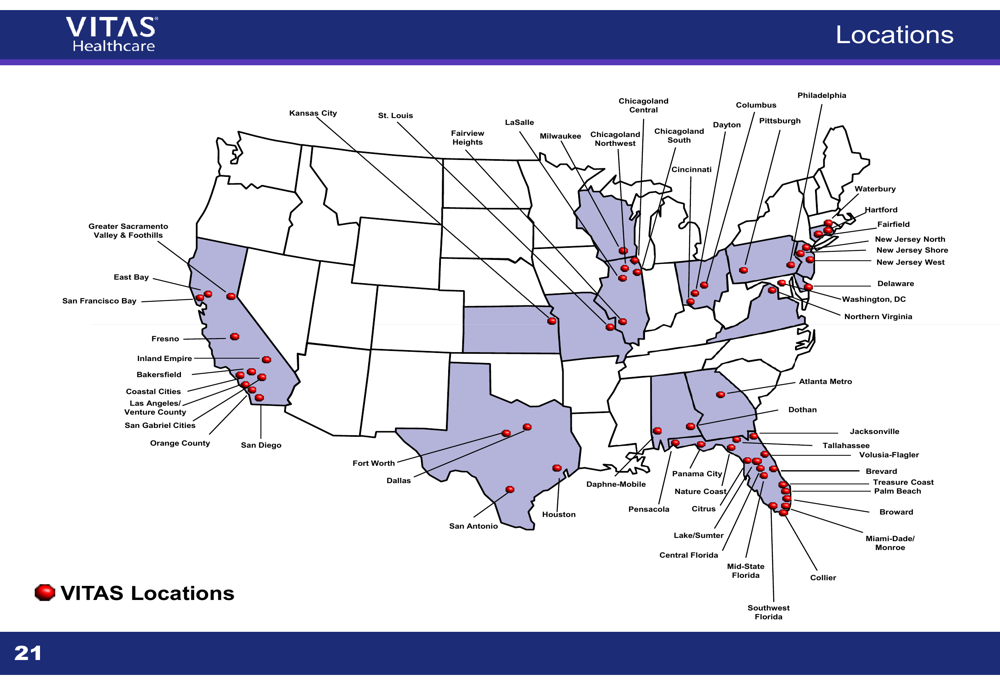

VITAS Healthcare continues to be the growth engine for Chemed, operating 55 hospice programs across 16 states and the District of Columbia with approximately 7-8% of the U.S. hospice market share. The segment’s average daily census per established program is approximately 400, with the largest single program serving around 2,700 patients.

The following map illustrates VITAS Healthcare’s geographic footprint:

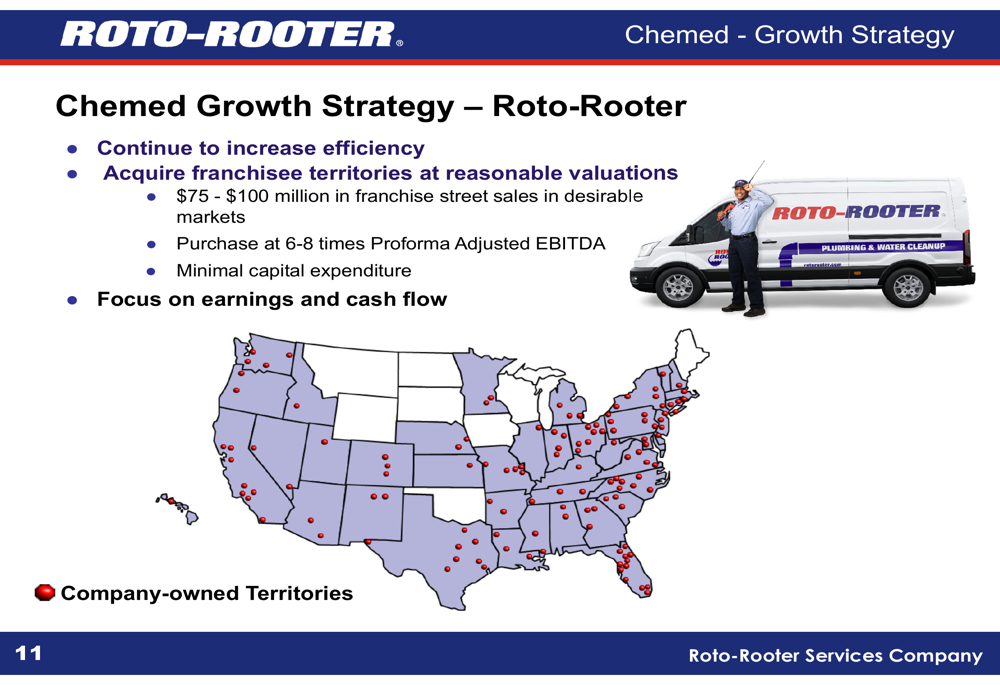

For the Roto-Rooter segment, Chemed’s strategy includes continuing to consolidate franchises through acquisitions at reasonable valuations and improving operational efficiency. The company estimates there are $75-100 million in franchise street sales in desirable markets that could be acquired at 6-8 times proforma adjusted EBITDA.

The company’s growth strategy for Roto-Rooter is illustrated in the following map showing company-owned territories:

Notably, the presentation included discussion of potential Roto-Rooter divestiture considerations. The company indicated it would consider such a move if after-tax proceeds could be reinvested at higher risk-adjusted returns, if Chemed’s capital structure and cash flow without Roto-Rooter would provide significant flexibility to support continued VITAS growth, and if a tax-free spin-off would create long-term stockholder value.

Forward-Looking Statements

During the earnings call, Chemed executives indicated they anticipate providing updated earnings guidance in June 2025. The company expects sustainable growth in 2026, driven by continued expansion in Florida markets for VITAS and strategic pricing adjustments in the Roto-Rooter division.

VITAS CEO Nick Westfall expressed optimism about maintaining above-average growth through organic expansion and acquisitions. Meanwhile, Chemed CEO Kevin McNamara highlighted the strategic management of Medicare caps, a key consideration for the hospice business.

The company faces several challenges, including Medicare cap management in the hospice market, declining leads in the Roto-Rooter segment, broader market volatility affecting investor sentiment, potential supply chain disruptions, and regulatory changes impacting healthcare operations.

Analyst Perspectives

Despite the mixed Q1 2025 results and subsequent stock price decline, analysts maintain an optimistic outlook for Chemed. According to available data, price targets suggest up to 14% upside potential from current levels. The stock currently trades with low volatility (Beta:0.49) and remains below its 52-week high of $623.61 but above the 52-week low of $512.12.

Investors will be closely watching for Chemed’s updated guidance in June 2025, particularly regarding strategies to address challenges in the Roto-Rooter segment and capitalize on growth opportunities in VITAS Healthcare. The potential strategic considerations regarding Roto-Rooter’s future within the company will also be a key focus for analysts in upcoming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.